Published as part of the ECB Economic Bulletin, Issue 3/2022.

The price of emissions allowances (EUA) traded on the EU’s Emissions Trading System (ETS) has increased from below €10 per metric tonne of carbon to above €90 since the beginning of 2018 (Chart A). In general, as discussed below, EUA prices are mainly driven by demand-side factors (such as economic activity and fuel switching) and public policies. Market commentary suggests that major factors behind the increase since early 2018 are likely to have been the introduction of increasingly stringent climate change policies in the EU and globally, alongside various changes in ETS market design. In April 2018 the introduction of the revised EU ETS Directive[1] – which sets the framework for the fourth trading period, from 2021 to 2030 – appears to have enhanced the credibility of the scheme.[2] The announcement by the European Commission of the European Green Deal in late 2019 is also reported to have supported EUA prices, alongside the endorsement by the European Council of a new EU-wide emission reduction target in late 2020.

The largest share of the EUA price increase has occurred since early 2021 and likely reflects a multitude of factors. Research by the European Commission and commentaries by participants in the EUA market suggest that several factors have led to the acceleration of the price increase since early 2021. First, particularly cold weather in Europe at the beginning of 2021 caused energy demand to rise. In the short term, given production rigidities, higher demand for energy translates directly into an increase in demand for EUA certificates and therefore into higher EUA prices. Second, the announcement of the European Commission’s “Fit for 55” package of legislative proposals reinforced the role of the EU ETS as the EU’s major decarbonisation tool. Third, phase 4 of the ETS, which started in 2021, also entails a shrinking supply of EUAs over time and updated parameters for the Market Stability Reserve, which will further limit the amount of EUAs available in the market.[3] Fourth, the main factor behind the most recent price increases is higher gas prices, which encourage electricity producers to switch from gas to more CO2-intensive coal-fired power generation, thereby increasing the demand for carbon permits.

Chart A

ETS spot and futures prices

(EUR per metric tonne of carbon)

Sources: Refinitiv, Bloomberg and ECB calculations.

Notes: The EU ETS has undergone numerous changes over the years. Introduced in 2005, the system was designed in trading periods and is now in its fourth trading phase. The latest observation is for February 2022 (ETS spot prices, monthly data).

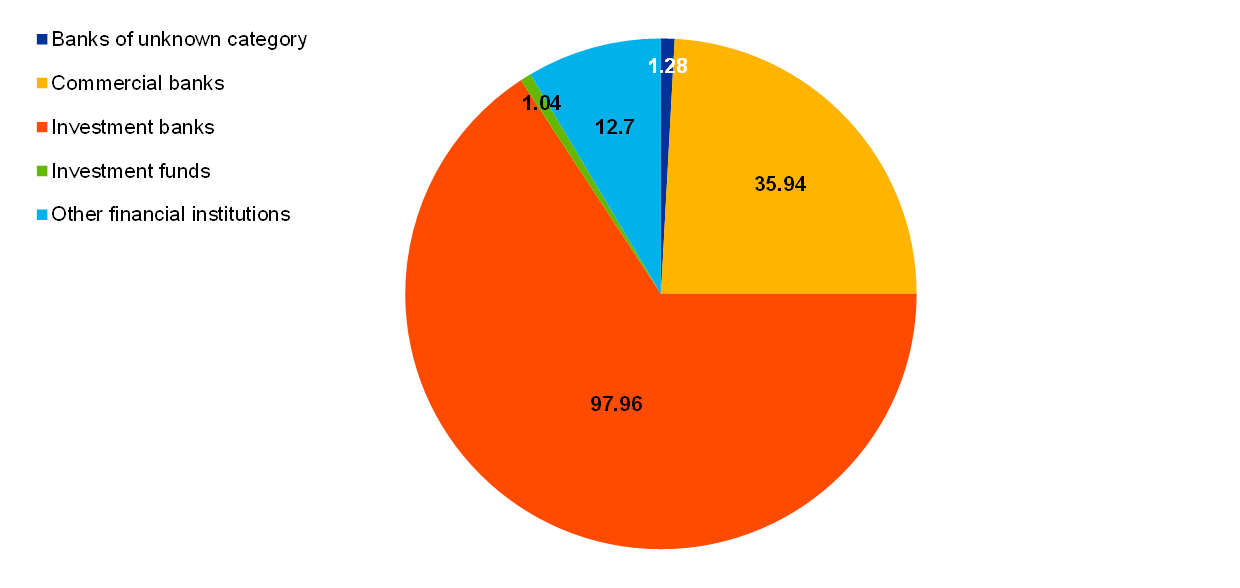

In light of the particularly strong increase in EUA prices over the last two years, the potential role played by speculation has also come into focus. Even if EUA prices are expected to increase to meet increasingly stringent decarbonisation goals, sharp price increases over a short period could imply that firms are faced with quickly rising costs without having sufficient time to adjust production capabilities. In this respect, European Commission research suggests that the price rally may have been supported by increased interest from non-compliance entities, such as investment funds, in the ETS.[4] Market intelligence also suggests that exchange-traded funds and other investment funds may be playing an increasingly important role in the ETS market.

However, the bulk of empirical studies of the drivers of carbon prices have so far focused mainly on structural determinants of price fluctuations and given limited attention to changes in speculation. The “switching” effect, which arises from the substitution between different sources of fuel with different carbon emission levels, has been identified as one of the most important drivers of carbon prices in theory. However, while the substitution in Europe takes place mainly between gas and coal, there is only mixed empirical evidence as regards the effect of fuel switching on carbon prices following changes in coal prices.[5] The literature finds fluctuations in economic activity,[6] alongside changes in end-product prices, mainly in the form of the price of electricity,[7] to be other important price determinants. Finally, weather conditions play a large role since these can influence the demand for emission certificates both through their impact on energy consumption and through their effect on renewable energy production, with the former effect appearing more important.[8] Some studies have also investigated the impact of announcements concerning changes in market design (i.e. the EUA supply schedule), coming to the conclusion that these have indeed had important effects on EUA prices.[9] Finally, only a few studies look at the evolution of the type of trading activity in carbon markets, finding a limited impact of speculation.[10]

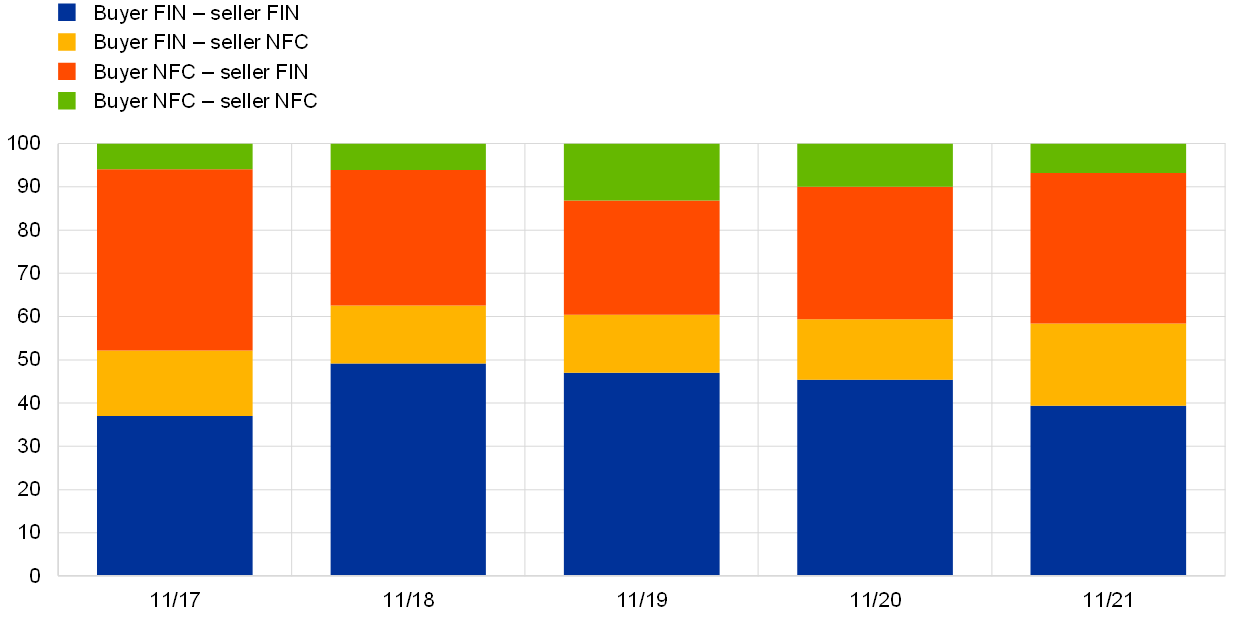

At present, tangible evidence of a strong increase in speculative activity related to potential changes in market structure appears scarce. The European Securities and Markets Authority (ESMA), in its preliminary report on the structure of the carbon market, documented that while the number of counterparties holding EUA futures positions has tended to increase since 2018, this increase has been relatively homogeneous across types of counterparty. [11] In general, market participants can trade both spot EUA and derivatives contracts. Unlike in other derivatives markets, carbon derivatives are almost entirely traded on regulated markets and cleared in central counterparties. Futures are the most common EUA derivatives in the secondary market, with the December future being by far the most liquid. [12] Data collected under the European Market Infrastructure Regulation (EMIR) in a regulatory trade repository, where the exchange of financial derivative contracts such as futures is registered, confirm that there has been little change in the market structure over the past five years (Chart B, panel a). This is despite the fact that the market has more than doubled in the last two years, with the notional value of open positions in EUA derivatives reaching €415 billion in early December 2021.[13] If speculative activity had increased materially, one would expect to see an increase in the share of outstanding open positions between financial institutions (blue bars), which is not the case.[14] This contrasts with information from market intelligence that suggests a recent increase in activity by investment funds in the ETS market, which may indicate a rise in speculation. However, investment funds overall continue to represent a very minor share of outstanding open positions, and this has only increased marginally – from 0.6% in 2020 to 0.7% in late 2021 (Chart B, right panel). These findings are in line with the latest ESMA report on the EU carbon market.[15]

Chart B

EU ETS market structure

a) Development of open positions by entity

(percentages)

b) Shares of open positions by financial subsector

(percentages)

Sources: EMIR data available to the ECB and ECB calculations.

Notes: Panel a): the chart shows the outstanding shares in open positions in forward and futures contracts on carbon emissions by type of entity as buyer and seller. FIN refers to financial corporations and NFC to non-financial corporations. Panel b): the chart shows the shares of financial entity subsectors in open positions. The financial subsectors are classified following Lenoci F.D. and Letizia E., “Classifying Counterparty Sector in EMIR Data”, in Consoli, S., Reforgiato Recupero, D. and Saisana, M. (eds.), Data Science for Economics and Finance, Springer, Cham, 9 January 2021.

A speculation index confirms that, while speculation appears to have increased slightly since early 2019, it seems to remain limited and well below the levels seen during earlier phases of the ETS. A proxy for the level of speculation in the ETS market can be constructed by comparing the overall volume traded with the volume of open positions for all entities.[16] The intuition behind such a proxy is that speculative behaviour leads to an increase in the volume traded but, since speculative positions tend to be closed quickly, not to an equivalent increase in the volume of open positions. A speculation index, calculated as weekly trading volume over the open interest at the end of any given week, currently suggests that speculation may have gradually been increasing over the last two years. [17] However, it remains largely below the levels seen at the creation of the ETS market and during phase 2 (Chart C).[18]

Chart C

Speculation in the EU ETS futures market

(index)

Sources: Refinitiv and ECB calculations.

Notes: The chart shows a two-week moving average of a speculation measure, defined as the ratio between the volume and open interest of futures contracts expiring in December. Volume and open interest are measured at the weekly level: for each week the cumulative volume from Monday to Friday is considered, whereas the weekly open interest is the open interest registered on a Friday. The latest observation is for 11 February 2022 (weekly data).

Directive (EU) 2018/410 of the European Parliament and of the Council of 14 March 2018 amending Directive 2003/87/EC to enhance cost-effective emission reductions and low-carbon investments, and Decision (EU) 2015/1814 (OJ L 76, 19.3.2018, p. 3).

The Directive amended the Market Stability Reserve and increased the rate of reduction of the annual emissions cap from 1.74% to 2.2% for phase 4 of the ETS.

See the box entitled “EU emissions allowance prices in the context of the ECB’s climate change action plan”, Economic Bulletin, Issue 6, 2021 for more information on the characteristics of the EU ETS.

Compliance entities are companies and aircraft operators obliged to participate in the EU ETS. Non-compliance entities, such as credit institutions, investment firms, funds and commodity trading firms (which have no compliance requirements), can also participate.

See e.g. Alberola, E., Chevallier, J. and Chèze, B., “Price drivers and structural breaks in European carbon prices 2005-2007”, Energy Policy, Vol. 36, No 2, February 2008, and Hintermann, B., “Allowance price drivers in the first phase of the EU ETS”, Journal of Environmental Economics and Management, Vol. 59, No 1, 2010, pp. 43-56, for an upward effect of fuel switching on carbon prices. By contrast, other studies, such as Rickels, W., Görlich, D. and Oberst, G., “Explaining European emission allowance price dynamics: Evidence from Phase II”, Kiel Working Papers, No 1650, Kiel Institute for the World Economy (IfW Kiel), 2014, find little support for an effect from fuel switching following changes in the price of coal.

Most studies use stock market indices as a proxy for economic activity (see e.g. Rickels, W. et al., op. cit., and Koch, N., Fuss, S., Grosjean, G. and Edenhofer, O., “Causes of the EU ETS price drop: Recession, CDM, renewable policies or a bit of everything? – New evidence”, Energy Policy, Vol. 73, October 2014, pp. 676-685).

See e.g. Alberola, E. et al., op. cit., and Aatola, P. Ollikainen, M. and Toppinen, A., “Price determination in the EU ETS market: Theory and econometric analysis with market fundamentals”, Energy Economics, Vol. 36, March, 2013, pp. 380-395. Some studies argue that the electricity price should not be included owing to its potential two-way relationship with EUA price (see e.g. Fell, H.,”EU-ETS and Nordic Electricity: A CVAR Analysis”, The Energy Journal, Vol. 31, No 2, 2010, pp. 1-26, and Lovcha, Y., Perez-Laborda, A. and Sikora, I., “The determinants of CO2 prices in the EU emission trading system”, Applied Energy, Vol. 305, Issue C, No S0306261921012162, 2022).

Studies that have focused on energy use agree on the role of additional heating and cooling in the two first phases of the ETS (e.g. Bredin, D. and Muckley, C., “An emerging equilibrium in the EU emissions trading scheme”, Energy Economics, Vol. 33, No 2, 2011, pp. 353-362, and Lutz, B., Pigorsch, U. and Rotfuβ, W., “Nonlinearity in cap-and-trade systems: The EUA price and its fundamentals”, Energy Economics, Vol. 40, Issue C, 2013, pp. 222-232). On the other hand, the role of weather variations in the provision of renewable energies is less clear. Overall, results suggest a marginal effect on EUA prices, also depending on the renewable power and countries considered (e.g. Koch, N. et al., op. cit.).

See Conrad, C., Rittler, D. and Rotfuβ, W., “Modeling and explaining the dynamics of European Union Allowance prices at high-frequency”, Energy Economics, Vol. 34, No 1, 2012, pp. 316-326; Koch, N. et al., op. cit.; and Koch, N., Grosjean, G., Fuss, S. and Edenhofer, O., “Politics matters: Regulatory events as catalysts for price formation under cap-and-trade”, Journal of Environmental Economics and Management, Vol. 78, Issue C, 2016, pp. 121-139.

Lucia, J.J., Mansanet-Bataller and Pardo, A., “Speculative and hedging activities in the European carbon market”, Energy Policy, Vol. 82, Issue C, 2015, pp. 342-351 explores the dynamics of speculative and hedging activities across the first three phases of the ETS and finds that speculation is likely to have played a role to some extent during phase 2, with the highest degree of speculative activity taking place at the time a new contract is listed. Moreover, speculative activity rises during the first quarter of each year. Overall, however, the role of speculation in the price formation process is not found to be very large. Lovcha, Y. et al., op. cit., adds to this by documenting that up to 90% of the fluctuations in the carbon price have historically been explained by variations in fundamental variables.

“Preliminary report – Emission Allowances and derivatives thereof”, European Securities and Markets Authority, 15 November 2021.

See e.g. Lucia, J.J. et al., op. cit., and Quemin, S. and Pahle, M., “Financials Threaten to Undermine the Functioning of Emissions Markets”, available at SSRN, revised 24 March 2022.

The sample of EMIR data used here includes transactions with at least one counterparty located in the euro area or the underlying securities issued by a euro area entity. The data (reported by both trade counterparties) are paired and de-duplicated, then outliers are removed. The final data can still be subject to data quality limitations (e.g. missing values, some transactions remain unpaired, possible under-reporting). The notional amount reported is as of 7 December 2021 to avoid end-of-year effects.

Such an increase sometimes contrasts with an increase in open positions between financial and non-financial institutions, where non-financial entities buy EUA futures to hedge their carbon price exposure, with financial counterparties acting as intermediaries that facilitate trading and provide liquidity to the market. See “Preliminary report – Emission Allowances and derivatives thereof”, European Securities and Markets Authority, 15 November 2021.

“Final Report – Emission allowances and associated derivatives”, European Securities and Markets Authority, 28 March 2022.

Note that the section above considered an increase in the proportion of open positions between financial institutions as a potential sign of speculative behaviour. However, the speculation index considered in this section assumes that the open positions of any market participant are non-speculative. While neither of these two assumptions are always fulfilled, they should largely hold. The two measures should therefore be seen as complementary.

The index follows Lucia, J.J., op. cit. This type of index was first proposed by Garcia, P., Leuthold, R.M. and Zapata, H., “Lead-lag relationships between trading volume and price variability: New evidence”, Journal of Futures Markets, Vol. 6, No 1, 1986, pp. 1-10.

The remarkably high speculative activity in early phase 1 (relative to phases 2 and 3) is probably explained by the novelty of the carbon market, which was launched in early 2005, and thus linked to an initial learning process (see Lucia, J.J. et al., op. cit.). Also, the lower level of hedging in phase 2 than in phase 3 is in line with the fact that during phase 3 allowances were distributed mainly through auctions. This implies that most installations that did not have sufficient allowances to cover their emissions during phase 3 needed to hedge their future positions.