The great trade collapse of 2020 and the amplification role of global value chains

Published as part of the ECB Economic Bulletin, Issue 5/2020.

This box assesses the economic effects of the coronavirus (COVID-19) pandemic as transmitted through global value chains (GVCs). The world economy is facing an unprecedented shock and, as the impact of the pandemic unfolds, world trade will be particularly hard hit. This box analyses the role of GVCs in the pandemic with a view to quantifying the ensuing effects on world trade. Our findings indicate that GVCs could significantly amplify the decline in world trade.

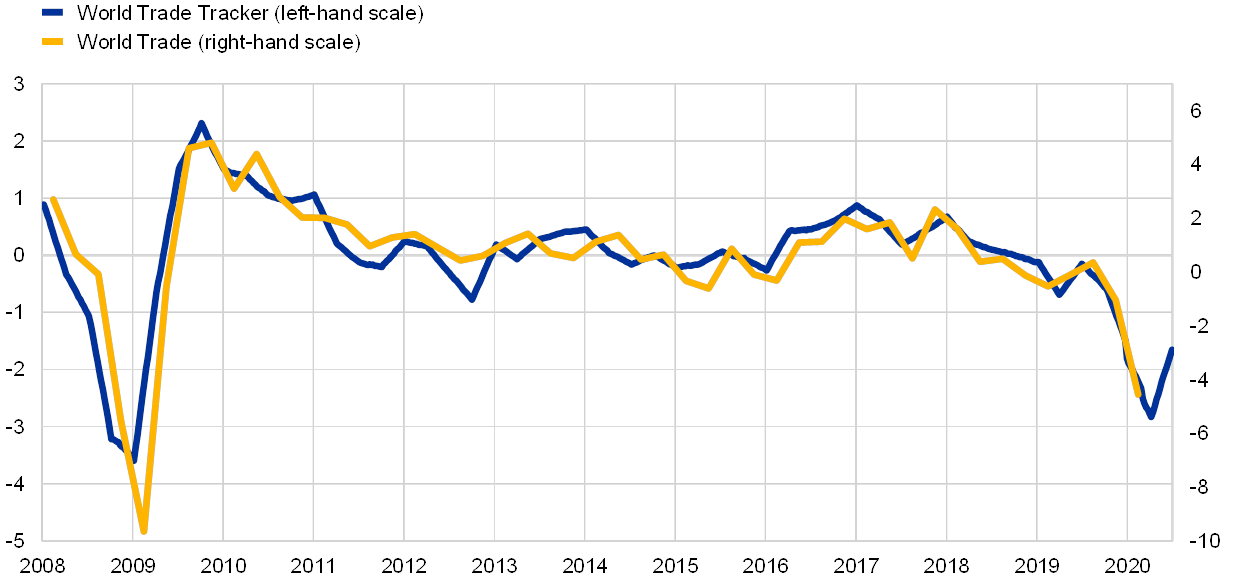

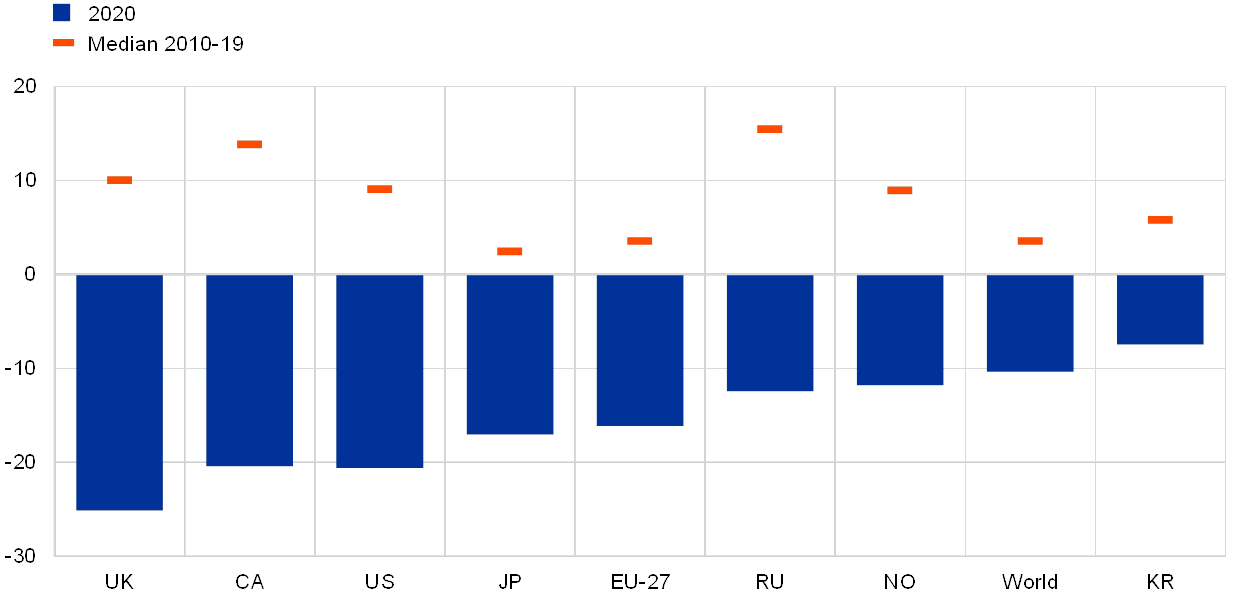

World trade has been falling sharply on the back of the COVID-19 pandemic, with value chains hit globally. National accounts data for key economies point to a sharp fall in both exports and imports in the first quarter of 2020. A new weekly trade tracker based on trade indicators available on a timely basis suggests a larger contraction in the second quarter of 2020 (see Chart A), although some signs of a recovery have emerged recently. In the June 2020 Eurosystem staff macroeconomic projections, world real imports (excluding the euro area) are expected to decline at an unprecedented pace of around 13% in 2020 before returning to positive rates of growth of 8.0% and 4.3% in 2021 and 2022 respectively. The decline also stems from disruptions in GVCs, among other factors. COVID-19 has struck value chains in Asia, Europe and the Americas, raising the risk of a domino effect with feedback loops that could amplify the collapse in global trade. The sharp fall in Chinese exports of intermediate goods across most destinations in the first quarter of 2020 (see Chart B) suggests that GVCs have already been hit widely as a result of the lockdown in China.

Chart A

Weekly trade tracker

(left-hand scale: standard deviations from mean; right-hand scale: quarterly percentage changes)

Sources: Haver and ECB calculations.

Notes: The tracker is based on a regression of world imports (excluding the euro area) on a principal component of a small panel of weekly indicators of trade (including lags), some monthly indicators, a constant and lags of the dependent variable. The indicators featuring in the weekly principal component were chosen on the basis of their correlation with world trade, availability and timeliness.

Chart B

Chinese exports of intermediate goods

(annual percentage changes)

Sources: Trade data monitor and ECB staff calculations.

Notes: Data are nominal. The chart includes data from January to March 2020. Countries shown are the United Kingdom (UK), Canada (CA), the United States (US), Japan (JP), the 27 European Union Member States (EU-27), Russia (RU), Norway (NO) and South Korea (KR).

Supply chain linkages play an important role in the transmission of shocks across countries. Although the expansion of GVCs has stalled since the 2008 global financial crisis, trade in intermediate goods remains important, accounting for more than 40% of world trade. This has significant implications for the relationship between demand, trade, and production. Traditional models assume that a country’s imports depend on its domestic demand. However, in a world characterised by complex international supply chains, changes in demand in third countries are also an important determinant. On average, more than 20% of world imports serve as inputs in domestic production processes and are embedded into goods which are subsequently re-exported. The complex network of supply linkages is also an important factor in the transmission of shocks across countries. Demand shocks in a particular country may be passed upstream through the global production network to input suppliers, with the initial shock being magnified by the “bullwhip effect”,[1] while supply disruptions can, in turn, be transmitted downstream.

The propagation and amplification effect of demand shocks associated with the pandemic can be gauged through global input-output tables. To assess the role of GVCs in the pandemic, two quantitative assessments were carried out. A first, static, exercise offers a first-order approximation of how demand shocks associated with the outbreak can propagate through a GVC, magnifying the impact on trade and production abroad. Input-output data from the Organisation for Economic Co-operation and Development (OECD) for 20 major advanced and emerging economies were employed to trace sectoral output losses triggered by the pandemic through the global production structure and quantitatively assess the propagation of demand shocks through GVCs.[2] Spillovers were quantified separately for imports and exports through two channels: (a) “direct” effects that materialise as a result of traditional trade, i.e. bilateral trade linkages; and (b) “indirect” effects that stem from demand fluctuations in third countries and concern intermediate goods crossing at least two borders.[3]

GVC linkages could significantly amplify the decline in global trade. Chart C presents estimates of amplification effects generated through supply chain linkages as percentages of the fall in trade occurring through the direct channel. For the United States, for instance, GVC linkages could magnify the decline in imports and exports by 8% and 20% respectively. For China, Japan and the United Kingdom, spillovers could be larger, especially for imports. For the world economy in the short term, GVCs could amplify the decline in imports and exports occurring through direct linkages (i.e. traditional trade) by around 25%. As major supply chain hubs, South Korea, Germany and China account for 20% of the total estimated decline in world exports arising from indirect linkages. However, as the global economy recovers in the coming quarters, GVC linkages could boost world trade. In the June 2020 Eurosystem staff macroeconomic projections, global trade is expected to rebound faster than global activity.

GVC spillovers are also likely to affect activity, with the actual impact depending on the relative positions of individual countries in GVCs. For example, in countries which are positioned downstream in the value chain, like Mexico, imports could fall more than exports (see Chart C), thereby providing a small net boost to activity. This reflects the fact that Mexico’s production is particularly dependent on imported inputs, which are then re-exported as finished products. In contrast, in countries positioned upstream in GVCs like the United Kingdom, there is likely to be a negative impact on activity as exports decline more than imports.

Chart C

Shortfalls generated on the back of GVC spillovers

(percentage) Sources: OECD and ECB staff calculations.

Notes: The chart shows the additional shortfalls that could be generated for each country as a result of GVC-related spillovers. GVC spillovers are expressed as a percentage of losses estimated to occur through traditional trade (i.e. imports and exports of: (1) final goods, and (2) intermediate goods used in production for domestic absorption). The chart refers to the short-term effects of GVC spillovers. Countries shown are the United States (US), China (CN), the United Kingdom (UK), Japan (JP) and Mexico (MX).

A second quantitative exercise indicates that GVCs had become impaired already in the first quarter of 2020. Specifically, the analysis focused on whether exports of countries upstream in the Chinese value chain were hit on the back of COVID-19-related lockdowns and demand shocks in February 2020 in China. Our estimates are based on a monthly panel model covering 37 countries and 22 industries. For each industry and country, changes in total exports of intermediate goods are regressed on a variable obtained by multiplying a dummy variable, which is given a value of 1 in February 2020 (i.e. a proxy for the COVID-19 shock in China), and a measure of upstreamness to China computed for each individual industry-country pair.[4] The analysis suggests that countries upstream to China in the value chain have been hit the hardest, with exports falling by some 3.8% incrementally at each stage, as one moves up the supply chain. The limited period of time available over which to observe the postulated effect requires a cautious interpretation of the results. However, they confirm the presence of amplification caused by GVCs. In addition, a breakdown of the results by region suggests that the decline in Chinese demand has so far been borne mostly by its trading partners in the Asian value chain.

The COVID-19 outbreak has exposed the interdependence of countries in terms of the supply of inputs and final goods. The analysis in this box suggests that GVC spillovers could magnify the decline in world trade, adding some 25% to the effects which could occur on the back of bilateral linkages. Econometric analysis corroborates this, suggesting that China’s upstream suppliers, particularly those in the Asian value chain, might have been hit hardest by the unfolding of the pandemic in China. The disruption related to COVID-19 may leave a longer-term legacy for global supply chains, leading to a review of production processes and substantial reshoring.

- The “bullwhip effect” relates to a situation in which a shock triggers disruption to demand for parts and components which increases the further upstream a firm is located in the supply chain. Firms are induced to adjust their inventories along the supply chain to meet new expected levels of demand. For empirical evidence of this effect, see for example Alessandria, G., Kaboski, J.P., and Midrigan, V., “US Trade and Inventory Dynamics”, American Economic Review, Vol. 101, No 3, May 2011.

- We traced sectoral losses (estimated by ECB staff) for a number of advanced and emerging economies, which could occur on the back of the pandemic, through the global production structure. To do so, we relied on the OECD world input-output data. As sectors differ in terms of the degree of their integration into cross-border production chains, the overall response of world trade depends on the sectoral composition of losses across countries. We computed partial elasticities which, for each country and sector, translate domestic and foreign demand shocks associated with the pandemic into proportional changes in output and imports and exports of final and intermediate goods to and from all countries and sectors. Equipped with these elasticities, we then computed losses associated with the pandemic for imports and exports separately. The analysis focused on the amplification of demand shocks associated with the pandemic. In cases where domestic and foreign sectors experience lockdowns at the same time, there is less scope for amplification of supply disruptions by GVCs. For further information on the methodology, see Bems, R., Johnson, R., and Yi, K.-M., “Demand Spillovers and the Collapse of Trade in the Global Recession”, IMF Economic Review, Issue 58, No 2, 2010.

- This is in line with the definition of GVCs by Borin, A., and Mancini, M., “Follow the Value Added: Tracking Bilateral Relations in Global Value Chains”, November 2017.

- Our index of upstreamness is obtained by measuring the number of intermediate production stages for each industry-country export prior to absorption in China. In particular, the index is constructed by assigning a value of 1 to the share of output of a given country/industry directly sold to final consumers in China, a value of 2 to the share of output sold to consumers in China after being used as an intermediate good by one other industry, and so on. The index is calculated using nominal data provided by the input-output tables from the 2015 edition of the OECD Trade in Value Added database. The results are therefore likely to be sensitive to price effects. See Ferrari, A., “Global Value Chains and the Business Cycle”, February 2019.