Macroprudential policy measures

Published as part of the Macroprudential Bulletin 11, October 2020.

This annex provides an overview of macroprudential capital requirements in euro area countries as at 1 October 2020. In addition, it also provides information on other macroprudential measures taken by the member countries since the last issue of the Macroprudential Bulletin in October 2019. An overview of all measures reported to the ECB under Article 5 of the SSM Regulation[1] is provided on the ECB’s website. The macroprudential policy measures are defined in the ECB’s macroprudential policy and financial stability glossary. Their aim is described in more detail in the first issue of the Macroprudential Bulletin.

1 Capital requirements – an overview

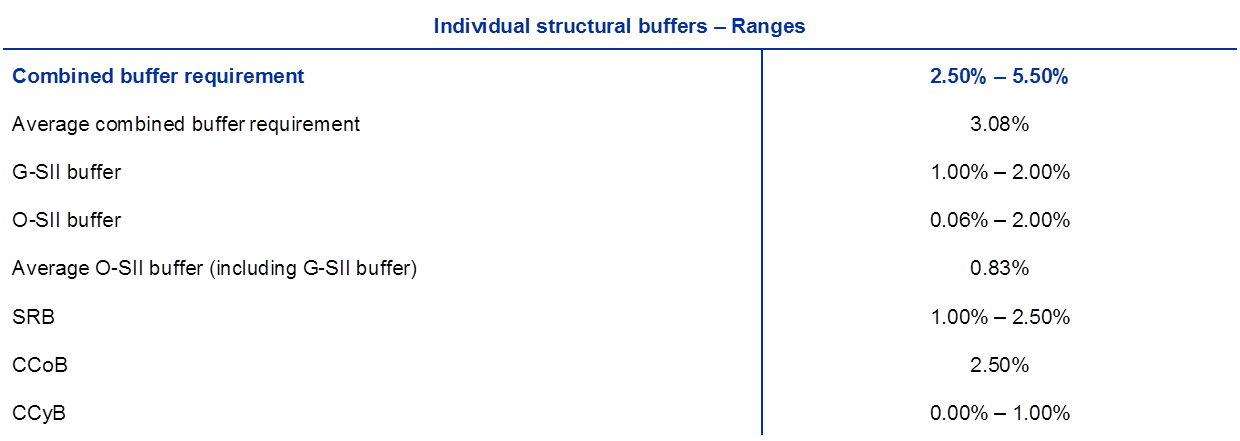

Table A.1 provides an overview of macroprudential capital measures in the euro area as at 1 October 2020.

Table A.1

Macroprudential capital measures

(1 October 2020)

Source: National notifications.

Notes: The figures only include information on supervised banks (e.g. excluding O‑SII buffer requirements for Cyprus-based investment firms). Small and medium-sized investment firms are exempted from the CCyB and/or the CCoB in Italy, Lithuania, Luxembourg, Malta and Slovakia. For Slovakia, the SRB is applied only to domestic exposures, meaning that the buffer applies in addition to the O‑SII or G‑SII buffer, whichever is greater. The CBR is calculated in accordance with Article 131 CRD IV but excludes mandatory or voluntary reciprocity of foreign macroprudential measures in accordance with Recommendation ESRB/2015/2. It consists of CET1 capital and is in addition to a minimum requirement of 8% total capital (4.5% CET1 + 1.5% AT1 + 2% T2). Pillar 2 measures are not included. The minimum combined buffer requirement at country level corresponds to a bank not subject to any individual bank-level structural buffer (G‑SII, O‑SII, SRB). Abbreviations: combined buffer requirement (CBR); global systemically important institution (G‑SII); other systemically important institution (O‑SII); systemic risk buffer (SRB); countercyclical capital buffer (CCyB); capital conservation buffer (CCoB); Capital Requirements Directive (CRD IV); Common Equity Tier 1 (CET1); Additional Tier 1 (AT1); and Tier 2 (T2). * Reflects only countries that have already activated a positive CCyB.

2 Capital requirements at the country level

Chart A.1 shows the minimum and maximum CBR, as well as the banks affected by the maximum CBR. Whereas the minimum CBR (blue) is usually applicable to all banks in one country, taking into account the CCoB and the CCyB, the maximum CBR (yellow) relates to financial institutions that are required to apply an O‑SII buffer, G‑SII buffer or SRB, whichever is greater.

Chart A.1

Overview of combined buffer requirements

(left-hand scale: percentage of total risk exposure; right-hand scale: total number; measures applicable as at 1 October 2020)

Source: National notifications.

Notes: The figures only include information on supervised banks (e.g. excluding O‑SII buffer requirements for Cyprus-based investment firms). In some countries, certain financial institutions are designated as O‑SIIs, but no additional buffer requirement applies at this time. Small and medium-sized investment firms are exempted from the CCyB and/or the CCoB in Italy, Lithuania, Luxembourg, Malta and Slovakia. For Slovakia, the SRB is applied only to domestic exposures, meaning that the buffer applies in addition to the O‑SII or G‑SII buffer, whichever is greater. The CBR is calculated in accordance with Article 131 CRD IV but excludes mandatory or voluntary reciprocity of foreign macroprudential measures in accordance with Recommendation ESRB/2015/2. It consists of CET1 capital and is in addition to a minimum requirement of 8% total capital (4.5% CET1 + 1.5% AT1 + 2% T2). Pillar 2 measures are not included. The minimum combined buffer requirement at country level corresponds to a bank not subject to any individual bank-level structural buffer (G‑SII, O‑SII, SRB). Abbreviations: combined buffer requirement (CBR); global systemically important institution (G‑SII); other systemically important institution (O‑SII); systemic risk buffer (SRB); countercyclical capital buffer (CCyB); capital conservation buffer (CCoB); Capital Requirements Directive (CRD IV); Common Equity Tier 1 (CET1); Additional Tier 1 (AT1); and Tier 2 (T2).

3 Changes to macroprudential policy measures since 29 October 2019

Countercyclical capital buffers

Majority of euro area countries

In order to address the impact of the coronavirus (COVID-19) pandemic, the national competent authorities (NCAs) of six euro area countries have decided to revoke the implementation of previously announced CCyBs and to release already activated CCyBs.

Currently, two euro area countries report a positive CCyB rate: Luxembourg, 0.25% as of 1 January 2020, which will be increased to 0.5% as of 1 January 2021, and Slovakia, 1% as of 1 August 2020.

The NCAs of 12 euro area countries decided to maintain the CCyB rate at 0%.

Belgium

In March 2020, the Nationale Bank van België/Banque Nationale de Belgique (NBB/BNB) revoked the previously announced activation of the CCyB (from 0% to 0.5%) to address the challenges posed by the coronavirus crisis. The implementation of the CCyB had been planned for 1 July 2020. The buffer is now to remain at 0% until at least July 2021.

France

The Haut Conseil de Stabilité Financière (HCSF) revoked the decision to increase the CCyB and released the already implemented CCyB of 0.25%. It had been planned to increase the CCyB rate from 0.25% to 0.5% as of 2 April 2020.

Germany

The Federal Financial Supervisory Authority (BaFin) revoked the previously announced activation of the CCyB (from 0% to 0.25%). The implementation of the CCyB had been planned for 1 July 2020. The buffer is now to remain at 0% until at least 31 December 2020.

Ireland

In March 2020, the Central Bank of Ireland decided to release the CCyB. The CCyB rate was reduced from 1% to 0% as of 2 April 2020. The buffer is to remain at 0% until at least the first quarter 2021.

Lithuania

Lietuvos bankas announced its decision to reduce the CCyB from 1% to 0% as of 1 April 2020. The buffer is to remain at 0% until at least 1 April 2021.

Luxembourg

In December 2019, the Commission de Surveillance du Secteur Financier (CSSF) decided to raise the CCyB rate from 0.25% to 0.50% to increase the resilience of banks. This measure will come into effect on 1 January 2021. The increase is motivated by growing cyclical vulnerabilities in the short and medium‑term.

Slovakia

Národná banka Slovenska decided, in response to the spread of the coronavirus, to revoke the raising of the CCyB rate from 1.5% to 2%, planned for 1 August 2020. The decision entered into force on 1 May 2020. Moreover, the CCyB was lowered to 1% as of 1 August 2020. The main reason for reducing the CCyB rate is to free bank capital for lending, as well as to give banks sufficient capacity to make further provisions for impairments, reflecting a conservative approach to potential future losses.

O‑SII/G‑SII buffers and the SRB

Majority of euro area countries

NCAs decided to revise O‑SII buffers and plan to phase them in in five countries and the SRB in three countries in response to the coronavirus crisis.

O‑SII buffers remained unchanged in eight countries, G‑SIIs buffers remained unchanged in four countries and the SRB remained unchanged in two countries. Phasing-in plans previously announced were not revised.

Cyprus

The Central Bank of Cyprus decided, in October 2019, to introduce an O‑SII buffer plan for one additional institution. The newly identified institution is Astrobank Ltd, for which a 0.25% O‑SII buffer applies with the same phase-in period as buffers for other O‑SIIs starting on 1 January 2020.

Furthermore, in response to the pandemic, the NCA has decided to postpone the phase-in plan by 12 months for all O‑SIIs. The O‑SII buffers will be fully loaded as of 1 January 2023.

Estonia

In March 2020, Eesti Pank announced the reduction of the systemic risk buffer from 1% to 0%. The release entered into force on 1 May 2020 as a response to the coronavirus pandemic.

Finland

Finanssivalvonta (FIN-FSA) announced two measures in response to the pandemic crisis. The SRB has been reduced to 0% for all institutions. In addition, FIN-FSA reduced the O‑SII buffer rate for one bank, OP Group, from 2% to 1%. The decision was announced on 17 March 2020.

Germany

In the context of the annual review of O‑SII buffers, BaFin decided in December 2019 that Volkswagen Bank GmbH will no longer be designated as an O‑SII, since it does not satisfy the criteria of the EBA Guidelines.

In addition, the O‑SII buffer rate of Norddeutsche Landesbank was lowered from 1.00% to 0.50%. This is due to the bank being assigned to a lower bucket in view of the decline in its score.

Moreover, in December 2019, BaFin decided to lower the G‑SII buffer applicable to Deutsche Bank AG from 2.00% to 1.50%, starting from 1 January 2021. The institution had been allocated to a lower bucket following a decrease in its score.

Greece

In November 2019, the Bank of Greece decided to lower the O‑SII buffer applicable to Piraeus Bank S.A. from 1.00% to 0.75% as of 1 January 2021. The decrease is due to a lower score for the bank.

Ireland

In its review of O‑SII buffers in December 2019, the Central Bank of Ireland identified two new credit institutions, Bank of America Merrill Lynch International DAC and Barclays Bank Ireland plc, as systemically important. An O‑SII buffer of 0.50% will apply to both of these institutions, with a phasing-in period from 1 July 2020 to 1 July 2021. In addition, two credit institutions, DePfa Bank plc and UniCredit Bank Ireland plc, scored below the threshold and are no longer recognised as O‑SIIs.

Italy

In November 2019, Banca d’ Italia announced a new O‑SII, Gruppo Monte dei Paschi di Siena. A buffer rate of 0.25% will be fully implemented for the newly identified O‑SII as of 1 January 2022.

Lithuania

Lietuvos bankas decided in November 2019 to drop Luminor Bank AB from the list of identified O‑SIIs. The decision is due to the change in the legal status of the bank, to a branch of Luminor Bank AS with headquarters in Estonia, as of 2 January 2019.

Following the coronavirus pandemic, the Lithuanian NCA further decided to postpone by one year the remaining phase-in for Šiaulių bankas AB. The postponement involves O‑SIIs whose buffer rates had not been fully applied. The O‑SII buffer rate for Šiaulių bankas will be fully implemented as of 31 December 2021.

Malta

In December 2019, the Central Bank of Malta and the Malta Financial Services Authority identified APS Bank plc as a new O‑SII. The bank will be subject to an O‑SII buffer of 0.25%, which will be fully loaded as of 1 January 2023.

The Netherlands

In April 2020, De Nederlandsche Bank (DNB) decided to lower the SRB from 3% of global risk-weighted exposures to 2.5% for ING, 2% for Rabobank and 1.5% for ABN Amro.

Moreover, the O‑SII buffer rate for ABN AMRO Bank N.V. has been decreased from 2% to 1.5%.

Portugal

In its annual review of O‑SIIs in October 2019, Banco de Portugal made a number of changes. Banco Comercial Português, S.A. was moved up one bucket, implying an upward revision of its O‑SII buffer by 0.25 percentage points to the new level of 1%. In addition, LSF Nani Investments S.à.r.l. was identified as a new O‑SII and was assigned a buffer rate of 0.50%. Novo Banco was, in turn, removed from the list of O‑SIIs. This was due to the bank becoming a 75%-owned subsidiary of LSF Nani Investments S.à.r.l.

Moreover, Banco de Portugal decided to postpone by 12 months the phase-in of the O‑SII buffer rates. The buffer rates will be fully implemented as of 1 January 2022 for all O‑SIIs with the exception of Banco Comercial Português, S.A., for which the implementation phase will continue until 1 January 2023.

Slovakia

In May 2020, Národná banka Slovenska announced the reduction of the O‑SII buffer rate for Poštová banka, a.s. from 1% to 0.25%. The 75 basis point reduction is justified by a significant decrease in the bank’s overall O‑SII score in 2019 and will be effective from 1 January 2021.

Slovenia

Banka Slovenije identified, in December 2019, Intesa Sanpaolo as an additional O‑SII. A buffer rate of 0.25% will be applicable for the bank as of 1 January 2021.

Other macroprudential measures

Belgium

In January 2020, the NBB/BNB notified its intention to extend the period of application of its current macroprudential measure based on Article 458(2)(d)(vi) of the Capital Requirements Regulation (CRR). The measure implies higher risk weights (by more than 25% on average) for exposures to Belgian residential real estate for banks using the internal ratings based (IRB) approach. The measure consists of two components. The first component imposes a five percentage point risk weight add-on for IRB banks’ exposures to Belgian mortgage loans. The second, more targeted, component further increases the risk weights in line with the risk profile of the IRB bank’s mortgage portfolio – by applying a multiplier of 1.33 to the (microprudential) risk weight of the residential mortgage loan portfolio. The measure has been renewed for an additional year, from 1 May 2020 to 30 April 2021.

Furthermore, in October 2019, the NBB/BNB decided to introduce supervisory expectations regarding sound credit standards in mortgage lending for banks and insurance companies active in the residential real estate market. More specifically, the supervisory expectations consist of benchmark thresholds for loan-to-value (LTV) (i.e. 90% for owner-occupied housing and 80% for buy-to-let housing) and debt repayment burdens. The supervisory expectations were implemented from 1 January 2020 and aim to improve credit quality and limit additional build-up of credit risk in future mortgage portfolios.

France

In December 2019, the HCSF made a recommendation to financial institutions regarding lending standards on new mortgage loans. The recommendation consists of (a) a maximum debt service-to-income (DSTI) ratio of 33% of the borrower’s net income and (b) a maximum maturity of 25 years. Up to 15% of the amount of new loans can deviate from the previous recommendations, of which 75% should be reserved to first-time buyers and buyers of a main residence, with a maximum loan-to-income (LTI) ratio of seven. The implementation of the recommendation has been effective since 1 January 2020.

Moreover, in April 2020, the HCSF decided to extend for one more year the application of the large exposure limits applicable to highly indebted large non-financial corporations (NFCs) that are resident in France. Systemically important institutions must not incur an exposure that exceeds 5% of their eligible capital to NFCs or groups of connected NFCs assessed to be highly indebted. The measure was implemented on 1 July 2018 under Article 458 CRR and will be extended from 1 July 2020.

Latvia

In November 2019, the Financial and Capital Market Commission (FCMC) approved amendments to the Regulation on Credit Risk Management which add new requirements to the existing supervisory framework. The FCMC decided on the following borrower-based measures, which will come into effect on 1 June 2020: a DSTI ratio of 40%, a debt-to-income (DTI) ratio of six, loan maturity caps and an LTV cap of 70% for buy‑to-let mortgage loans.

The Netherlands

In December 2019, the DNB decided to impose a minimum average risk weight for the calculation of regulatory capital requirements applicable to exposures to natural persons secured by mortgages on residential property located in the Netherlands, based on Article 458(2)(d)(vi) of the CRR. The introduction of the measure has now been postponed in response to the coronavirus pandemic. The measure implies that for each individual exposure item in scope of the measure, a 12% risk weight is assigned to the portion of the loan not exceeding 55% of the market value of the property that serves to secure the loan, and a 45% risk weight is assigned to the remaining portion of the loan. The stricter requirement will be applicable to credit institutions that use the IRB approach for calculating regulatory capital requirements.

Portugal

In January 2020, Banco de Portugal tightened the Macroprudential Recommendation on new credit agreements for consumers with respect to the original maturity limits on new personal loans and the exceptions on DSTI ratios above 50%. These amendments came into force on 1 April 2020. The maturity limit on new personal loans was tightened from ten years to seven years, except for credit granted to education, health and renewable energies, whose maturity limit is still ten years. In addition, the exceptions on DSTI ratios above 50% consist of the following: up to 10% of the total amount of credit granted under this measure by each institution may be granted to borrowers with a DSTI ratio of up to 60%; up to 5% of the total amount of credit granted under this measure by each institution may exceed the limits laid down regarding the DSTI ratio.

Slovakia

In December 2019, Národná banka Slovenska tightened the DSTI ratio limit for both housing loans and consumer loans from 80% to 60%, applicable as of 1 January 2020. There are some exceptions: 5% of new loans can be granted with a DSTI ratio of up to 70% (applicable to any new loans), and 5% of new consumer loans with a maturity not exceeding five years can be granted with a DSTI ratio of up to 70%.

Slovenia

In September 2019, Banka Slovenije decided to change the macroprudential recommendation for household lending into binding macroprudential restrictions. The Regulation on macroprudential restrictions on household lending has been applicable since 1 November 2019. The aim of the measure is to ensure prudent lending standards and to restrain lending to excessively risky borrowers. The Regulation sets a binding cap on the DSTI ratio, which may not exceed (a) 50% for borrowers whose income is less than twice the gross minimum wage and (b) 67% for the part of the borrower’s income in excess of this threshold. It also sets a binding maturity limit of seven years for consumer loans. The requirement with regard to LTV ratios remains in the form of a recommendation. The Regulation allows for some exemptions from these restrictions.