Lessons learned from initial margin calls during the March 2020 market turmoil

Published as part of the Financial Stability Review, November 2021.

Margin requirements on derivatives portfolios increased significantly in March 2020, exacerbating liquidity stress as entities took action to meet margin demands. In particular, some non-bank financial entities met margin calls by redeeming shares in money market funds, selling bonds or borrowing in repo markets.[1] Extraordinary interventions by public authorities were ultimately crucial in stemming stress in these markets.[2] While margin consists of two main components – initial margin and variation margin – this box focuses on initial margin (IM), since it is subject to model risk and depends heavily on the calibration choices of central counterparties (CCPs) (for centrally cleared transactions) or counterparties (for non-centrally cleared transactions).[3] As IMs are calibrated to reflect possible future changes in market prices, they are sensitive to market volatility. However, if IMs are overly procyclical (too low in good times and/or too high in bad times), their movements can amplify liquidity stress and lead to selling pressures in financial markets.

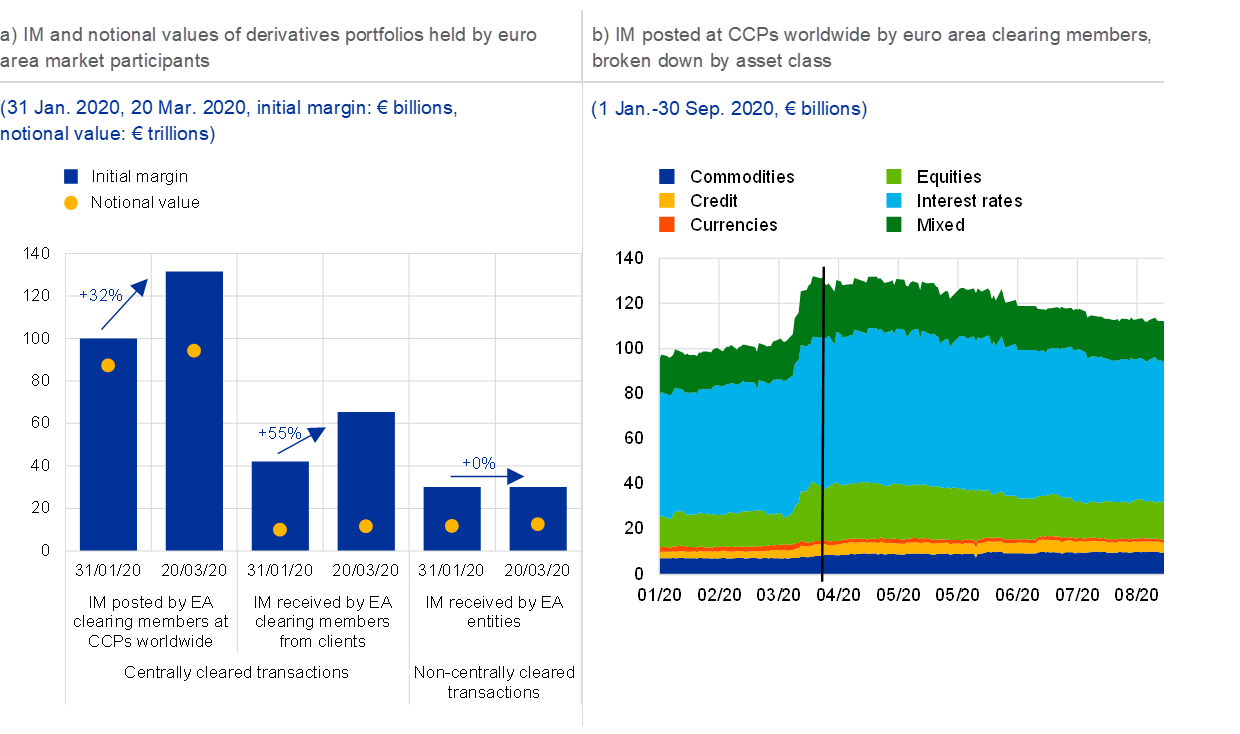

Chart A

Centrally cleared IM increased significantly, driven mainly by equity, credit and interest rate portfolios

Sources: European Market Infrastructure Regulation (EMIR) data and authors’ calculations.

Note: Panel a: counterparties to euro area clearing members (CCPs or clients) include both euro area and non-euro area counterparties. Among “client” sectors, the investment fund sector experienced the largest increase in IM requested by euro area clearing members, amounting to €14 billion. Panel b: vertical line indicates the announcement of the pandemic emergency purchase programme. Data on four dates are excluded owing to outliers and/or low data coverage (13 January, 17 and 18 February, 28 September).

The increase in IM amid the March 2020 turmoil was concentrated almost entirely in centrally cleared derivatives and driven mainly by equity, credit and interest rate portfolios (see Chart A, panel b). Between 31 January and 20 March 2020, CCPs collected roughly €30 billion of additional IM from euro area clearing members (a 32% increase), who largely met this by collecting IM from their clients (€23 billion; a 55% increase), most notably from investment funds (€14 billion).[4] The IM remained elevated throughout the rest of 2020 as – among other factors – the high volatility from the turmoil continued to feed into CCP models over an extended period of time. For non-centrally cleared derivatives, IM remained broadly unchanged, likely reflecting design features of the underlying margin model – the standard initial margin model (SIMM) – which is less responsive to short-term fluctuations in market volatility.[5]

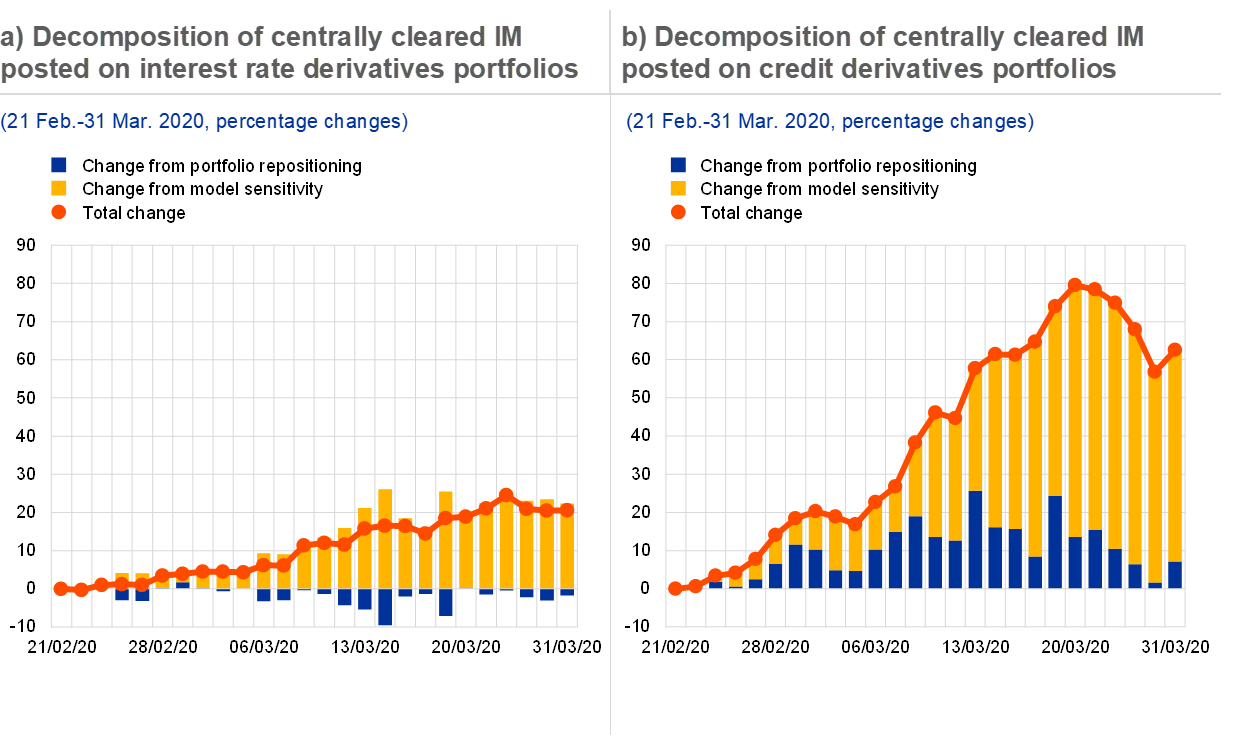

Analysis of portfolios of centrally cleared interest rate and credit derivatives suggests that CCP model sensitivity to market volatility was the main driver of the increase in IM. In addition to model sensitivity to market volatility, the increase in IM may also reflect portfolio repositioning by investors, motivated by factors like changes in risk appetite and hedging needs. The IM increase is decomposed into the impact from market volatility and repositioning by comparing static portfolios with those where repositioning took place (see Chart B).[6] For both types of derivative, the results suggest that the increase in IM was mostly driven by model sensitivity to the rise in market volatility. While portfolio repositioning contained the IM increase for interest rate derivatives, it worked in the opposite direction for credit derivatives, reflecting the increased activity in the credit default swap market.

Chart B

The key driver of the increase in IM was the sensitivity of CCP models to market volatility

Sources: EMIR data and authors’ calculations.

Notes: The charts show the relative increase in IM posted by euro area clearing members to CCPs worldwide. The decomposition is obtained by analysing the change in IM for those portfolios that did not alter in composition during the period observed (static portfolios) and projecting the same change to those portfolios that did alter during the same period (dynamic portfolios). The method relies on the assumption that for static portfolios, changes in IM requirements are attributable to changes in volatility only.

The IM developments of March 2020 suggest that it is important to develop a clearer understanding of the models which CCPs use to calibrate IMs and possibly review such models. This would also be welcomed by some market participants, who would prefer higher margin levels in good times to help reduce the risk of unexpected large margin calls in bad times. Any recalibration should build on a common understanding of “excessive procyclicality”, a concept that would determine when margin calls should be considered too large because they could result in significant repercussions for systemic liquidity. Such a “macro” concept would provide guidance for recalibrating IM models on a “micro” level and also facilitate comparisons of the different models used by CCPs. To increase the resilience of the financial system to liquidity shocks, it would also be important to enhance the transparency of IM models in both centrally and non-centrally cleared markets. The supervisory and regulatory framework governing the liquidity management of market participants, and in particular that of some non-bank financial intermediaries, should also be strengthened (see Section 5.2).

- See Box 8 entitled “Interconnectedness of derivatives markets and money market funds through insurance corporations and pension funds”, Financial Stability Review, ECB, November 2020 and BCBS, CPMI and IOSCO, “Consultative report: Review of margining practices”, Bank for International Settlements and International Organization of Securities Commissions, October 2021.

- See, for instance, “The ECB’s commercial paper purchases: A targeted response to the economic disturbances caused by COVID-19”, blog post by Luis de Guindos and Isabel Schnabel, April 2020; Box 7 entitled “Recent stress in money market funds has exposed potential risks from the wider financial system”, Financial Stability Review, ECB, May 2020; Holistic Review of the March Market Turmoil, Financial Stability Board, November 2020.

- Initial margins are typically collected to cover potential future exposure over the appropriate close-out period in case of counterparty default. IMs are calibrated using historical market price volatility during a certain “look-back period” and tend to increase when recent volatility significantly exceeds previously observed values – but the exact sensitivity to market volatility depends on the underlying model and its calibration. Variation margins are collected and paid out to set the current market exposure to zero, reflecting market prices changes.

- IM collected by CCPs rose by around USD 300 billion globally. See Graph 2.2 in “Lessons Learnt from the COVID-19 Pandemic from Financial Stability Perspective”, Financial Stability Board, July 2021.

- See the article entitled “Investigating initial margin procyclicality and corrective tools using EMIR data”, Macroprudential Bulletin, ECB, October 2019.

- Given that the composition of equity derivatives portfolios changes very frequently, such an approach is not suitable for this asset class.