Recent developments in euro area food prices

Published as part of the ECB Economic Bulletin, Issue 5/2020.

Food prices can be an important driver of euro area headline HICP inflation, as food accounts for almost 20% of the HICP consumption basket and food price inflation is highly volatile. In the second quarter of 2020 the contribution of food to HICP inflation was around two-thirds of a percentage point, making it larger than the contribution of services or non-energy industrial goods. As food items are also a prominent example of frequently purchased out-of-pocket goods, their price movements are generally thought to have an important bearing on consumers’ perception of inflation. Against this background, this box reviews recent developments in euro area food prices in an environment that has been affected by the coronavirus (COVID-19) pandemic.

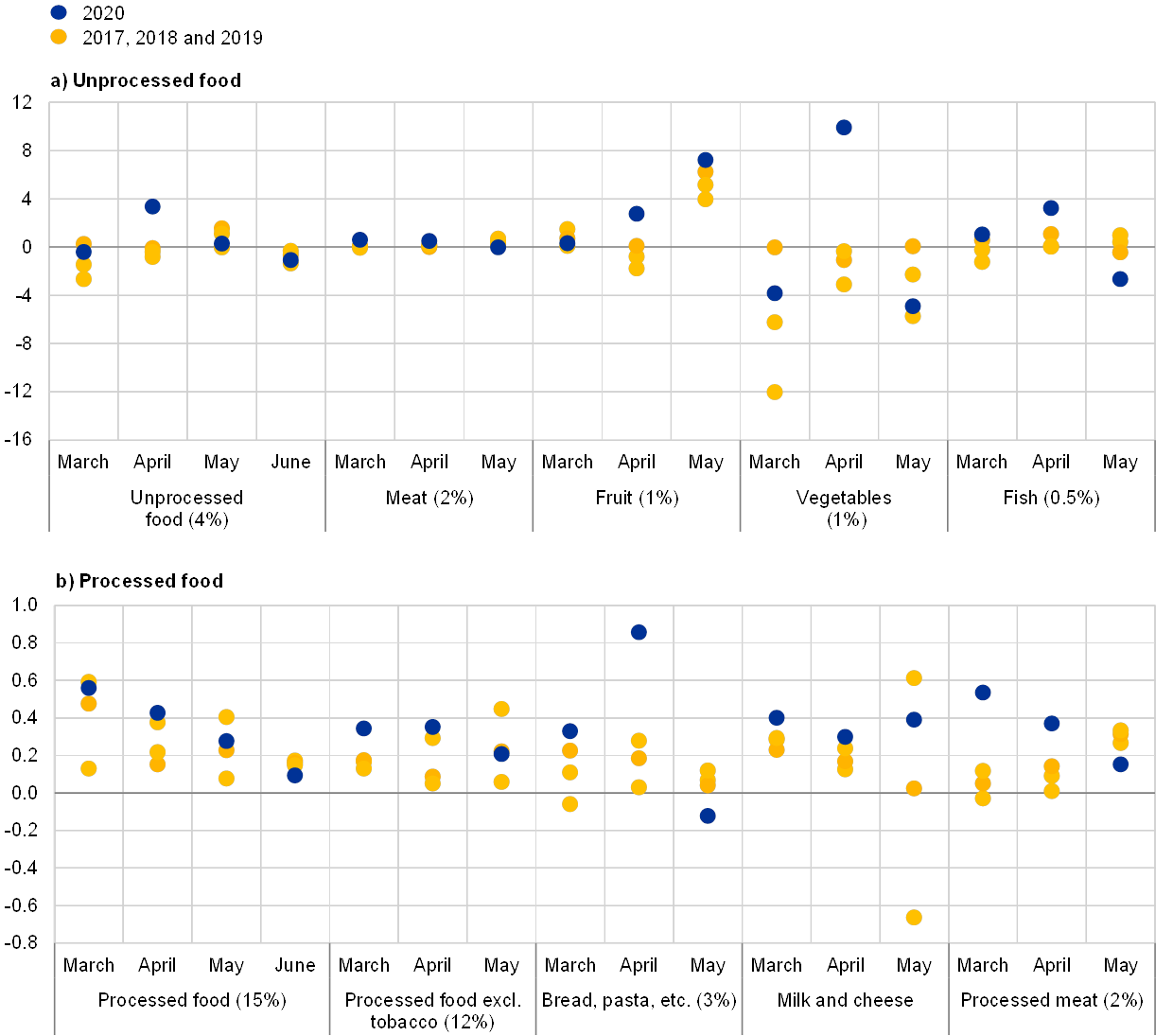

The April 2020 surge in euro area food prices was strong even in the light of food prices having been volatile in the past. The month-on-month increase in total food prices reached an exceptional 1.1% in April, a rate almost never observed since 1999 (excluding the few temporary large hikes due to changes in indirect taxes).[1] The only other increase of a similar magnitude was in January 2002, when the euro cash changeover took place. As food prices are highly seasonal, especially for unprocessed food, changes in a given month should be compared with the same month in other years. Comparing the month-on-month change in April 2020 with the previous three years reveals that the April 2020 change was exceptional, especially for unprocessed food (see Chart A).[2] The more detailed product breakdown shows that, within the unprocessed food component, this exceptional increase was observed mainly in prices for vegetables, and to a slightly lesser extent also in prices for fresh fruit and fish. Although the increase was less pronounced for overall processed food prices, it was clearly higher for certain items such as bread, pasta and other flour products, as well as meat.[3] Month-on-month price changes in May and possibly also June signal some unwinding of the food price increases observed in April for vegetables, fresh fish, and bread, pasta and other flour products. Price increases for processed meat eased, while prices for fresh fruit continued to increase fairly quickly. The preliminary data for June signal a further easing in food price pressures, although a detailed breakdown is not yet available. As a result, annual inflation for unprocessed food decreased to 5.9% in June from the peak of 7.6% in April. The inflation rate for processed food excluding tobacco was 1.8% in May (unchanged from April), whereas the preliminary data for June for total processed food show a slight decline, to 2.3%, from 2.4% in May (a more detailed breakdown is not yet available).

Monthly price developments in euro area consumer food prices during the COVID-19 lockdown

(month-on-month percentage changes; non-seasonally adjusted data)

Sources: Eurostat and ECB calculations.Notes: Historical month-on-month increases are shown only as of 2017 due to the break in the series resulting from the ECOICOP-5 changeover. The weights of the headline HICP items are shown in parentheses. At the time this box was finalised, a detailed breakdown of price changes for unprocessed and processed food items was not available for June.

Strong month-on-month changes in food prices can have many different causes. Usually, these changes are due to the seasonal nature of supply (in particular for unprocessed food) and the sensitivity of food prices (both processed and unprocessed) to local and global hygiene (animal disease) or weather-related shocks. Changes in indirect taxes can also sometimes have noticeable effects. However, the April 2020 surge was extraordinary and likely reflected upward pressures related to the specific circumstances of the COVID-19 pandemic. These circumstances include the fact that, during the lockdown period, households prepared more meals at home and thus diverted some demand for food away from restaurants and catering services and towards home consumption. Stockpiling in anticipation of lockdown restrictions may have been another reason why household demand for food was stronger than usual, although this argument applies only for processed food products that can be stored. Stronger-than-usual demand and the impact of stockpiling is evident in the surge in retail sales volumes for food in March, when the annual rate of change for the euro area jumped to a historical high of 9.1%, preceding the April price surge. In April, the annual growth rate in retail sales volumes slowed to 2.0%, before increasing again to 4.9% in May.

Developments in April 2020 most likely reflected strong increases in demand combined with supply-side effects related to the lockdown and containment measures. For instance, the surge in prices, especially for vegetables, likely reflected supply difficulties due to harvesting and transportation delays. Such delays may have increased the relative supply of (often more expensive) local products. More generally, producers and retailers faced cost increases due to mandatory hygiene measures and the repackaging of bulk volumes usually sold to businesses into smaller volumes for households. Repackaging takes time and thus may also have exacerbated the temporary supply shortage. It is also possible that consumers expressed a stronger preference for packaged fresh food (likely more expensive than unpackaged products) due to the fear of contracting the virus through direct contact with a product.[4] In addition, and especially for processed food products, in a number of cases the price increases recorded in the HICP may have also reflected the cancellation of promotional activities rather than outright price increases.

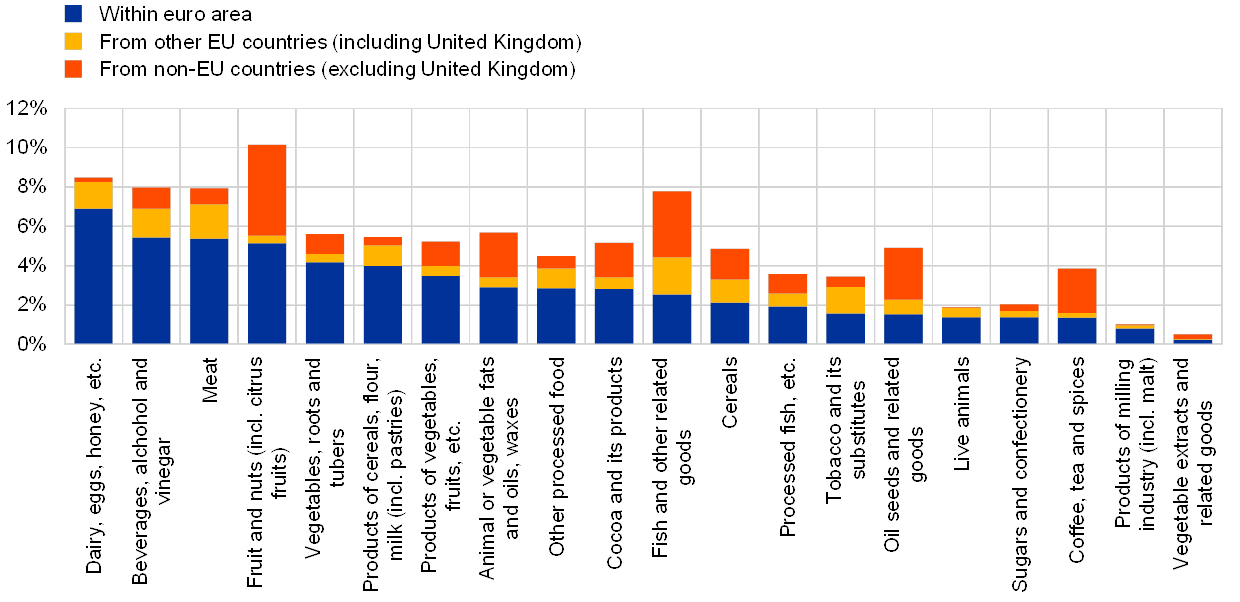

The potential supply-side impacts can be assessed by looking at the cost and input structures of food production. Food production in the euro area is characterised by strong supply linkages within the sector. According to the euro area input-output table, the main input for the manufacturing output of the food sector is domestic processed and unprocessed food products (approximately 40% of all inputs). For example, food is needed to feed animals and flour is needed to make bread. Food products imported from outside the euro area only make up a small share of the food sector’s total production costs (around 5%).[5] At the same time, around 10% of the processed food products, beverages and tobacco products consumed by households are imported directly from countries outside the euro area, and the corresponding share for fresh food (including fish products) is higher, at around 20%.[6] Overall, this suggests that the disruption of supply chains within the euro area, including distribution networks, that has been observed during the COVID-19 pandemic may have had important implications for the food supply and, therefore, prices.

Supply chains within the euro area are very important. Those involving the other EU countries and countries outside the EU, while generally less important, may still be important for specific products. Detailed sectoral data for euro area imports do not provide the breakdown of food imports used for domestic production and food imports delivered directly to shops for household consumption. Nevertheless, data on total food imports can provide some information on which food products are potentially more sensitive to supply chain disruptions. Eurostat trade data for 2019 show that around 40% of food imports from outside the euro area were from the other EU countries (including the United Kingdom). However, there is also substantial trade in food products within the euro area. For many product groups, such as dairy, beverages, meat and vegetables, imports from euro area countries significantly exceed imports from both the rest of the EU and from countries outside the EU (see Chart B). The particularly strong price increases for vegetables in April could thus reflect the bottlenecks in production and shipping from the south to the north of Europe. In May price increases for vegetables somewhat normalised, suggesting that the bottlenecks in southern Europe may have eased. This easing should also have softened price pressures for fresh fruit, but these prices continued to increase at a somewhat higher pace in May 2020 than in the same month in previous years. Given the sizeable imports of fresh fruit, not only from the euro area but also from countries outside the EU, these higher price increases in May could partly reflect the disruption to global supply chains in countries outside the EU as a result of the COVID-19 pandemic.

Composition and direction of euro area food imports in 2019

(percentages of total euro area imports of food products)

Sources: Eurostat and ECB calculations.

Overall, the food price increases in April were unusually strong and reflected an unprecedented combination of demand and supply influences. However, the HICP for food in May and June signalled signs of normalisation in price changes as lockdowns eased and activity resumed. There may still be some upside price pressures in the near term due to potential shortages of seasonal workers or increased hygiene costs for businesses. In the medium term, however, if the increase in unemployment is long-lasting there could be some downside pressures, especially for processed food, due to constrained household incomes.

- [1]In some countries the HICP for food in April was also less reliably compiled than usual as a large share of missing prices had to be inferred. For instance, in the French HICP for food in April, price changes were imputed (i.e. replaced), for example by referring to scanner data, for small shops, outdoor markets and shops whose prices were not available online. More generally, to impute prices that could not be collected, online prices were used if available and product replacement was more frequent than usual.

- [2]The changeover to a more granular HICP classification (ECOICOP-5) in January 2019 affected the split between processed and unprocessed food as of January 2017. As a result, the relative share of processed food in total food increased from around 60% to 75%, making it inappropriate to compare monthly changes with the years prior to 2017. For more information, see the box entitled “New features in the Harmonised Index of Consumer Prices: analytical groups, scanner data and web-scraping”, Economic Bulletin, Issue 2, ECB, 2019.

- [3]Price increases for meat products (both processed and unprocessed) since the middle of 2019 have been somewhat higher than over the preceding few years, partly due to strong demand from China, whose own supply of pork has decreased due to African swine fever. As a result, the EU, which is the world’s largest exporter of pork products, saw these exports increase.

- [4]While the general rule when compiling the HICP is to maintain fixed outlet and product types, the collection difficulties due to COVID-19 lockdowns implied a less stable structure of outlets and products, as a result of imputations that were necessary when some prices could not be collected.

- [5]These estimates are based on the euro area input-output table for 2018 provided by Eurostat.

- [6]Based on input-output tables, “fresh food and fish imports” comprises agriculture and hunting products and related services, as well as fish, other fishing products, aquaculture products and support services for fishing. This product classification is not fully consistent with the HICP unprocessed food item.