6 September 2023

By Luis de Guindos

Moving towards carbon neutrality as quickly and boldly as possible is by far the best way to slow down climate change. It may take more effort in the short run, but in the long run it will cost less overall, says ECB Vice-President Luis de Guindos. We need to reach carbon neutrality to avoid existential risks to nature, people and our economies. And we need to start making changes soon. Procrastinating may be easier and less costly today, but means we will pay a higher price tomorrow: the damage to our environment and economies from rising temperatures will be much more severe. In fact, the sooner and faster we complete the necessary green transition, the lower the overall costs and risks. This is one of the main outcomes of our second economy-wide climate stress test. Let me talk you through the findings.

The ECB economy-wide climate stress test is a tool that allows us to measure the future impact of climate risk on companies, households and the financial system. Its top-down modelling ensures a harmonised approach and provides unprecedented coverage of companies and financial institutions in the euro area.[1] It uses granular datasets, particularly data on firms’ geographical location and their greenhouse gas emissions. This allows us to identify firms that are vulnerable to transition and physical risk across sectors and regions. The results of the first ECB economy-wide climate stress test exercise were published in September 2021.[2] The first exercise focused on how physical and transition risks increase the probability of companies defaulting on their debt. It showed that the short-term costs of an early green transition are always more than offset by the long-term benefits of avoiding the physical risks of a “hot house world” in which the green transition does not happen.

This second economy-wide climate stress test exercise builds on the previous one, but also focuses on the timing and ambition of transitioning towards net zero and its financial consequences for companies and households in the context of a changing macroeconomic environment. More specifically, it asks two questions. Given today’s circumstances, what are the costs and risks associated with a transition to net-zero emissions in the short and medium-term? And what impact would the different transition pathways have on the economy and the financial system?

What’s new in our top-down climate stress testing framework

We have upgraded and added several features to our stress testing framework since 2021. First, we have constructed new short-term transition scenarios based on the climate scenarios of the Network for Greening the Financial System.[3] Second, we have developed new climate risk models that account for recent developments in the European energy sector, particularly the increase in energy prices triggered by Russia’s invasion of Ukraine. Third, we have calculated the investment needed to successfully transition towards net-zero emissions in a more granular way.

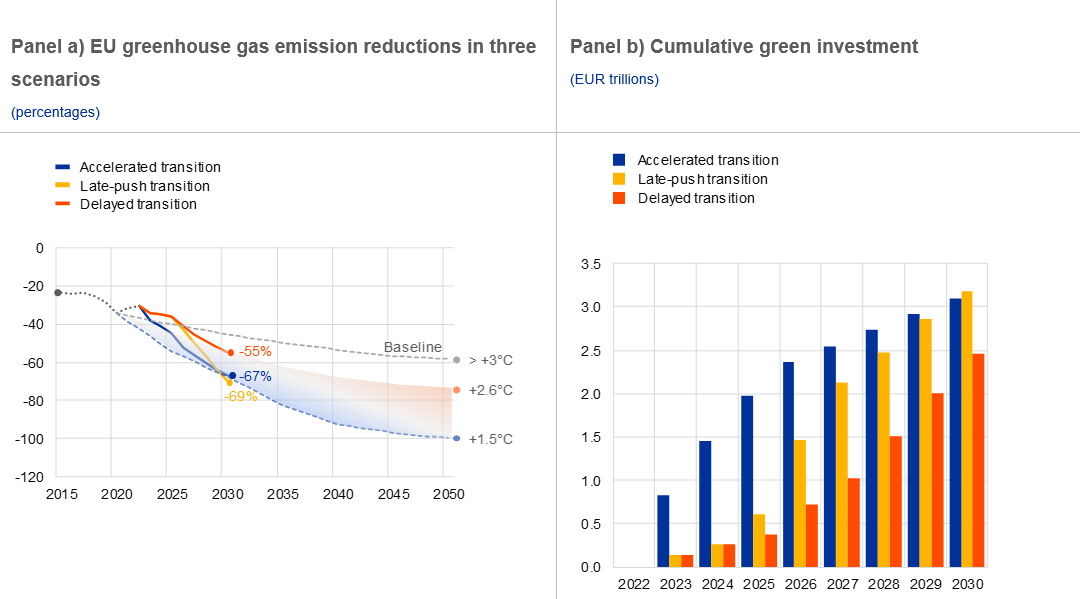

We designed three transition scenarios covering the period until 2030. The “accelerated transition” scenario assumes a jumpstart of the transition with rapid and severe increases in energy prices. Investment in renewable energy sources in the short term leads to a reduction in emissions by 2030. This would be compatible with the long-term temperature targets of the Paris Agreement (+1.5°C increase relative to pre-industrial levels).

In the other two scenarios, current macroeconomic and geopolitical conditions lead to a delay in green transition efforts until the end of 2025. In the “late-push transition” scenario, the green transition starts in 2026 and is intense enough to achieve emission reductions by 2030. The expected results are comparable to those in the accelerated transition, but they come at a higher cost, as the policies needed to achieve them are more ambitious and abrupt. In the “delayed transition” scenario, the transition also starts in 2026 but is more gradual and slower than in the late-push transition. It is therefore not ambitious enough to achieve emission targets in line with the Paris Agreement goals by 2030.

The green transition and potential ways forward

Under the three scenarios, how would greenhouse gas emissions, global temperatures and investment efforts develop? Chart 1, panel a) shows the historical and projected emission pathways compared with a baseline scenario that assumes that nothing will be done beyond currently implemented policies. In the long term the temperature increase in the delayed transition scenario is substantially higher than in the other two scenarios at 2.6°C compared with 1.5°C relative to pre-industrial levels. A delayed transition is therefore expected to lead to much higher physical risk in the long term via more frequent and more intense wildfires and floods than we are already currently experiencing.[4]

The transition towards net zero requires substantial investment in energy-efficient and renewable energy, such as solar and wind energy, as well as in phasing out fossil fuels. Chart 1, panel b) presents the total required investment based on bottom-up estimates for the three scenarios. An accelerated or late-push transition would require companies and households to invest significant funds from the very start of the transition, with green investment adding up to around €3 trillion by 2030. Under the delayed transition, the reduced efforts made until 2030 would result in a smaller increase in the funds needed. However, emission reductions would be lower and accompanied by heightened physical risk in the long term owing to the failure to meet the net-zero target of the Paris Agreement.

Chart 1

Emission pathways and green investment required in the three transition scenarios

Source: ECB calculation based on Orbis, Urgentem, Eurostat, NGFS and International Renewable Energy Agency (IRENA; 2021).

Notes: In panel a), historical aggregated data on emissions are provided by the European Environment Agency and are available until 2020. Quarterly emissions data for 2021 and 2022 are taken from Eurostat and aggregated at yearly frequency to complete the timeseries. Temperature increases refer to the year 2100. Emission pathways until 2050 correspond to the NGFS’s Net Zero 2050 (+1.5°C), the nationally determined contributions (NDC) scenario (+2.6°C) and current policy scenario (>+3°C). In panel b), green investment consists of investment in: i) renewable-based energy, and ii) carbon mitigation activities. Cumulated green investment is based on bottom-up estimates for the 2.9 million European non-financial corporations covered in the climate stress test exercise.

The short and medium-term financial impact of transition risk

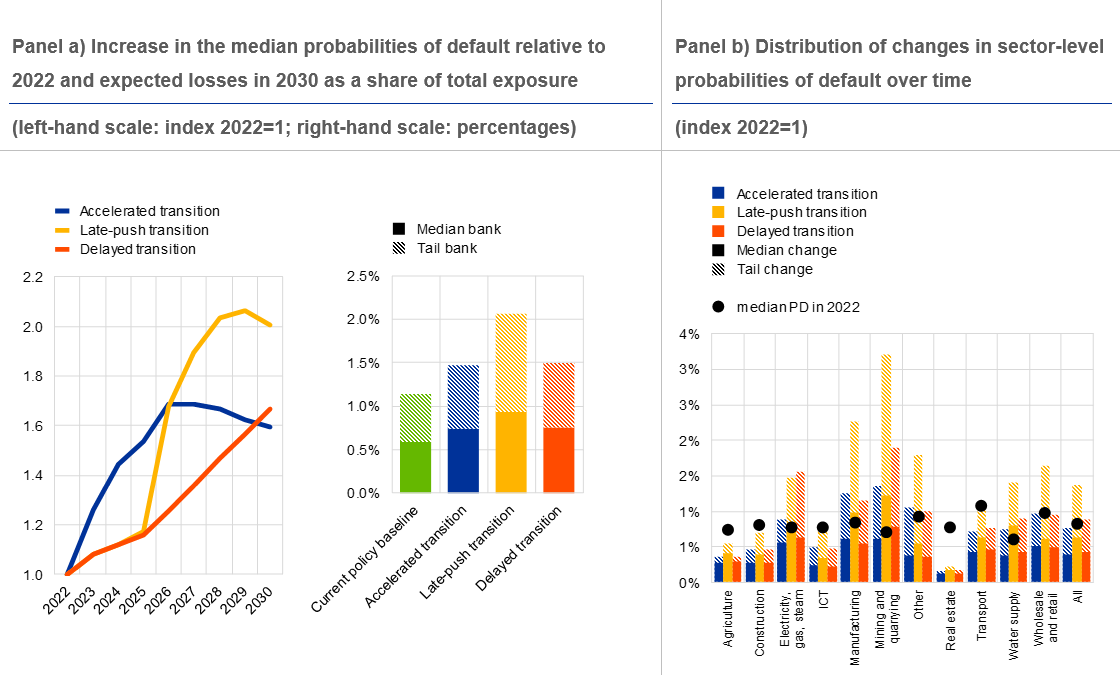

The results of the second exercise show that an accelerated transition scenario would lead to the lowest financial risk and lowest long-term physical risk. In all three scenarios, the probability of default of banks’ loan portfolios increases in the short term owing to transition risk (Chart 2, panel a). The accelerated and delayed transitions would lead to similar risk levels by 2030, but banks’ credit risk is expected to increase further in the delayed transition after 2030 because physical risk will develop more severely in the long term.

A late-push transition would be the most severe in the medium-term because of the higher costs of the green transition and the greater impact on companies’ profitability and debt. Expected losses in 2030 under the late-push transition would be almost double those under a baseline scenario (with no further transition risk). A late-push transition would be particularly detrimental for those banks most vulnerable to transition risk. Such banks could face expected losses of 2% of their loan portfolios[5] compared with losses of only 1% for the median bank.

The impact of the green transition will differ greatly across economic sectors (Chart 2, panel b). Energy-intensive sectors such as mining, manufacturing and electricity will experience the strongest effects on their credit risk because they produce the highest emissions and, as such, will come under the most pressure to reduce their carbon footprint and invest in renewable-based energy sourcing and production (particularly the electricity sector).

Chart 2

Accelerated transition leads to lower credit risk and is aligned with the Paris Agreement goals

Source: ECB calculations based on Orbis, Urgentem, Eurostat, NGFS, International Renewable Energy Agency (IRENA; 2021) and Intergovernmental Panel on Climate Change (2022).

Notes: Panel a) shows the median probabilities of default (PDs) of corporate loan portfolios and total expected losses of significant banks in the euro area. Corporate loan portfolio PDs are calculated as the average borrower-level PD, weighted by their loan size. The baseline scenario comprises NGFS current policies only, with no additional transition risk, and serves as a benchmark scenario. In panel b), tail changes represent percentage point changes in borrower-level PDs for the 75th percentile firm in each sector and scenario. ICT stands for the Information and Communication Technology sector.

Green policy measures to achieve net zero

Financing the transition towards a carbon-neutral economy is one of the most pressing challenges facing Europe today. The results of the new climate stress test exercise show that the earlier the transition happens, the lower the costs and risks for the economy and financial system. The effective and coordinated mobilisation of green finance is more necessary than ever to support the European Union’s efforts to take the lead in the transition towards net zero. Here are some of the policy measures that will help achieve this goal.

- Phasing out fossil fuels – moving away from high emission and polluting energy sources towards renewable-based energy is essential to achieve the Paris Agreement goal of net-zero emissions. Carbon policies, if well-designed, can compress the demand for fossil fuels and stimulate the production of cheaper renewable energy sources, while containing inflationary pressures.[6]

- Filling the green investment gap – firms would greatly benefit from progress towards a capital markets union (CMU), which would help them undertake the massive amounts of green investment required. The CMU would facilitate cross-border access to funds, strengthen risk-sharing, avoid fragmentation and foster integration[7]. There is a need for sustainable finance products, such as green loans and bonds, and funds with environmental, social and governance standards. It is also important to prevent the “greenwashing” of funds.[8]

- Setting up reliable transition plans – companies and financial institutions need to align their business models and operations with transition targets. This requires immediate and long-term planning in the form of credible and transparent transition plans. To further foster the green transition, transition plans compatible with EU policies implementing the Paris Agreement should become legally binding and publicly disclosed.[9]

- Designing prudential climate tools – the green transition is a potential source of systemic risk, as certain regions are more vulnerable to climate risks with potential spillover effects across sectors and to the financial system. We therefore need tools to address such risks, involving both microprudential and macroprudential measures.[10]

Conclusion

The first top-down economy-wide climate stress test showed that the short-term costs of an early green transition are always more than offset by long-term benefits stemming from the reduced physical risks. By including new elements in the original framework and focusing on transition risk over the next eight years, the second climate stress test exercise shows that acting immediately is more effective and comes at a lower cost in terms of financial stability, transition costs and physical risks. Early and strong policy action – designed properly and implemented timely – is required to mobilise funds for green investments and to support Europe’s transition towards a carbon-neutral economy. If we act now, it will be better all round – for nature and our economies. Let’s take the fast-track to Paris before it is too late.

The exercise covers around 2.9 million non-financial corporations and 600 consolidated banks in the euro area. The total exposures concerned amount to around €2.9 trillion.

See De Guindos, L. (2021), “Shining a light on climate risks: the ECB’s economy-wide climate stress test”, The ECB Blog, 18 March. The methodology and results of the first exercise were published in Alogoskoufis, S. et al. (2021), “ECB economy-wide climate stress test – methodology and results”, Occasional Paper Series, No 281, ECB, September. It was subsequently used in the 2022 supervisory climate stress test and the 2022 Eurosystem climate stress test.

Network for Greening the Financial System (2022), “NGFS Climate Scenarios for central banks and supervisors”, Paris, September.

Such temperature increases and the associated physical risk levels are expected on the assumption that, globally, all economies reduce their emissions as specified under the respective NGFS scenario and that the emission pathways for different countries – taken together – would make it possible to achieve the scenario-specific temperature target by the end of the century.

Vulnerable banks are defined as banks with expected losses relative to portfolio size within the 90th percentile of the distribution.

See Panetta, F. (2022), “Greener and cheaper: could the transition away from fossil fuels generate a divine coincidence?”, speech at the Italian Banking Association, Rome, 16 November.

See De Guindos, L. (2020), “Capital markets union: the role of equity markets and sustainable finance”, The ECB Blog, ECB, 3 March and De Guindos, L., Panetta, F. and Schnabel, I. (2020), “Europe needs a fully fledged capital markets union ‒ now more than ever”, The ECB Blog, ECB, 2 September.

See European Commission (2023), “Sustainable Finance: Commission takes further steps to boost investment for a sustainable future”, Brussels, June.

See Elderson, F. (2021), “Overcoming the tragedy of the horizon: requiring banks to translate 2050 targets into milestones”, speech at the Financial Market Authority’s Supervisory Conference, Vienna, 20 October.

See Chaves, M., Grill, M., Parisi, L., Popescu, A. and Rancoita, E. (2021), “A theoretical case for incorporating climate risk into the prudential framework”, Macroprudential Bulletin, ECB, October.