The euro’s global role in a changing world: a monetary policy perspective

Speech by Benoît Cœuré, Member of the Executive Board of the ECB, at the Council on Foreign Relations, New York City, 15 February 2019

This year marks the 20th anniversary of the euro’s creation, an event which has triggered much reflection on the single currency’s successes and challenges.[1]

Most of this commentary has, rightly, focused on the economic track record of the euro area. The main aim of monetary union was, after all, to maximise the benefits of the EU’s internal market and thereby shift Europe onto a higher growth trajectory.[2]

I will not discuss these benefits today. Instead I will merely say that, since day one, many commenters, including here in the United States, have predicted the imminent demise of the euro. However, the truth is that, today, three out of four people in the euro area support the euro – the broadest support since its creation.[3] One should never underestimate the resilience and strength of Europe’s monetary union project.

Today I would like to focus on a different aspect, however: the external dimension of the euro – that is, its international role. For some Europeans, external factors have always formed part of the case for the single currency. A currency with a global standing would not just be a symbol of European unity on the world stage, it would also be a tool to project global influence.

Following this line of thought, it is no coincidence that the final push towards monetary union took place against the backdrop of the confrontational foreign economic policies of the 1980s.[4]

Yet by the time the euro was launched in 1999, this protective aspect of the single currency had rather disappeared from view. The turn of the century was the age of “the end of history”, when conflicts between great powers were seen as a relic of the past, replaced by a widespread liberal order. The notion that countries should view their currencies as tools of foreign economic policy became unfashionable.

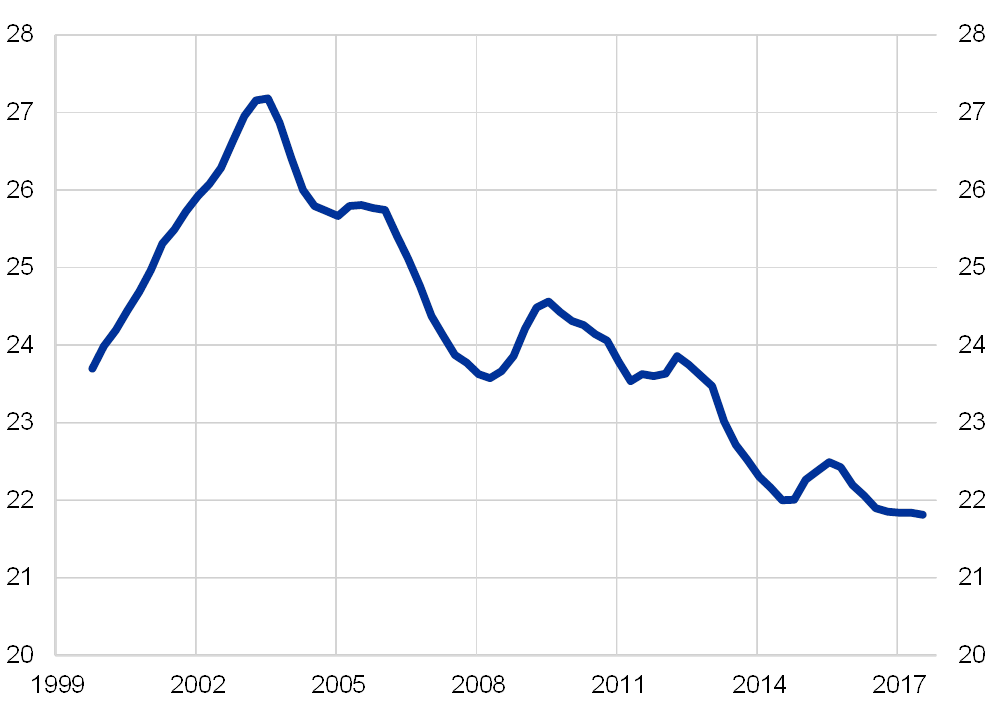

As a result, few politicians in Europe took note that, after quickly establishing itself as a global currency, the euro gradually lost international standing from the mid-2000s onwards. You can see this on my first slide, which shows a composite index measuring the euro’s international role. Today, it stands at an historic low.

The euro’s international role has declined since the mid-2000s

Index of the euro’s international role

(percentages; four-quarter moving averages)

Sources: BIS, IMF, CLS, Ilzetzki, Reinhart and Rogoff (2017) and ECB calculations.Notes: Arithmetic average of the shares of the euro at constant exchange rates in stocks of international bonds, cross-border loans, cross-border deposits, foreign exchange settlements, global foreign exchange reserves and exchange rate regimes. Data on the share of the euro in global trade invoicing were not available; those on foreign exchange settlements are at market exchange rates. The latest data are for the fourth quarter of 2017.

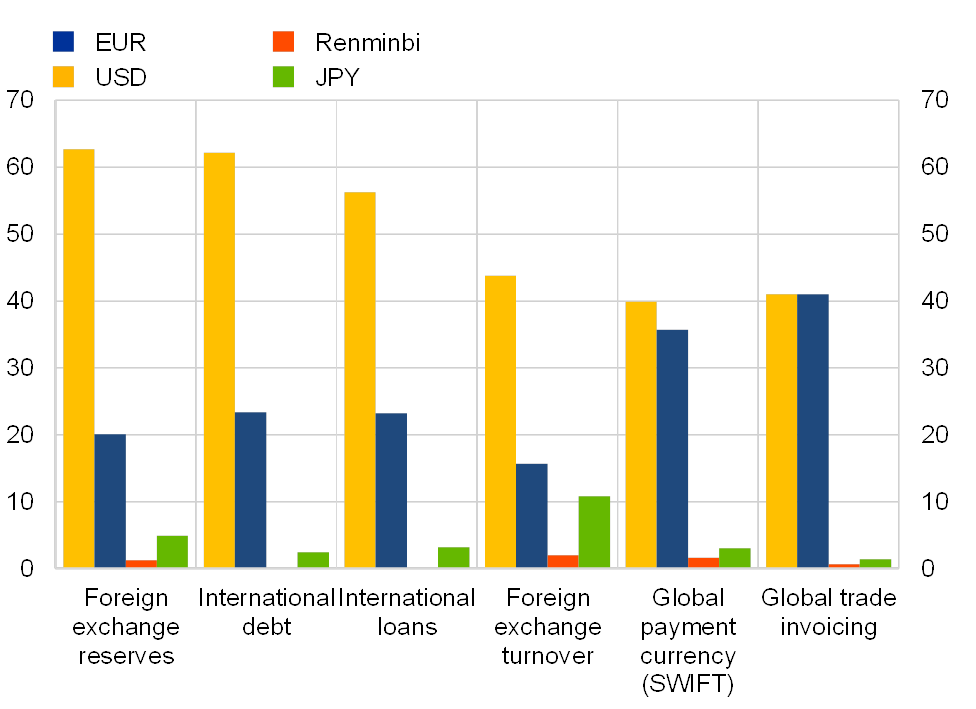

While the euro is the second most used currency by most measures, it often lags behind the dollar by a wide margin.[5] You can see this on Slide 2, which shows the shares of major currencies in selected measures of international currency use.

The euro is the world’s second global currency

Snapshot of the international monetary system

(percentages)

Sources: BIS, IMF, SWIFT, Gopinath (2016) and ECB calculations.Note: Data as at the fourth quarter of 2017 or latest available.

European policymakers have woken up to these developments. There have been a series of calls in recent months for the euro to assume a stronger international role.[6]

The main reason that I see for these calls relates to the growing perception of a shift in global governance, from leadership built on trust and common identities – what the ancient Greeks called hegemonia – to leadership based on arkhe, hard power where policies and doctrines are imposed on others.[7]

In such an environment, being the issuer of a global reserve currency confers international monetary power, in particular the capacity to “weaponise” access to the financial and payments systems.[8] As has been clear on a number of recent occasions, the prospect of being shut out of major financial systems makes fines or economic sanctions markedly more threatening.

This shift in global governance, in turn, has contributed to the belief that the EU may be more exposed to the risk that the monetary power of others is not used in its best interests, or is even used against it.[9]

These risks are not new, of course. As Tommaso Padoa-Schioppa once noted, the demise of the gold standard shifted monetary management away from international constraints and towards domestic priorities. In Padoa-Schioppa’s words, this is when “monetary nationalism took over”.[10]

The novelty of our situation today is that these concerns extend well beyond advanced economies. Other nations are now seeking to raise the international profile of their currencies. The renminbi, for example, was included in 2016 in the International Monetary Fund’s special drawing rights (SDR) basket alongside the US dollar, euro, yen and pound sterling. China recently also launched its first oil futures contract denominated in renminbi – the so-called petroyuan – in an apparent bid to strengthen the hold of the renminbi in global energy markets.

There are certainly high barriers to other currencies displacing the dollar in the international financial and commodity system.[11] Yet multi-polar currency systems existed in the not-so-distant past. Before World War One, the pound sterling, the Deutsche Mark and the French franc all vied for global supremacy as reserve currencies.[12] And the interwar period was characterised by a sterling-dollar duopoly. So, if history is any guide, a multi-polar system could well become a reality once again.[13]

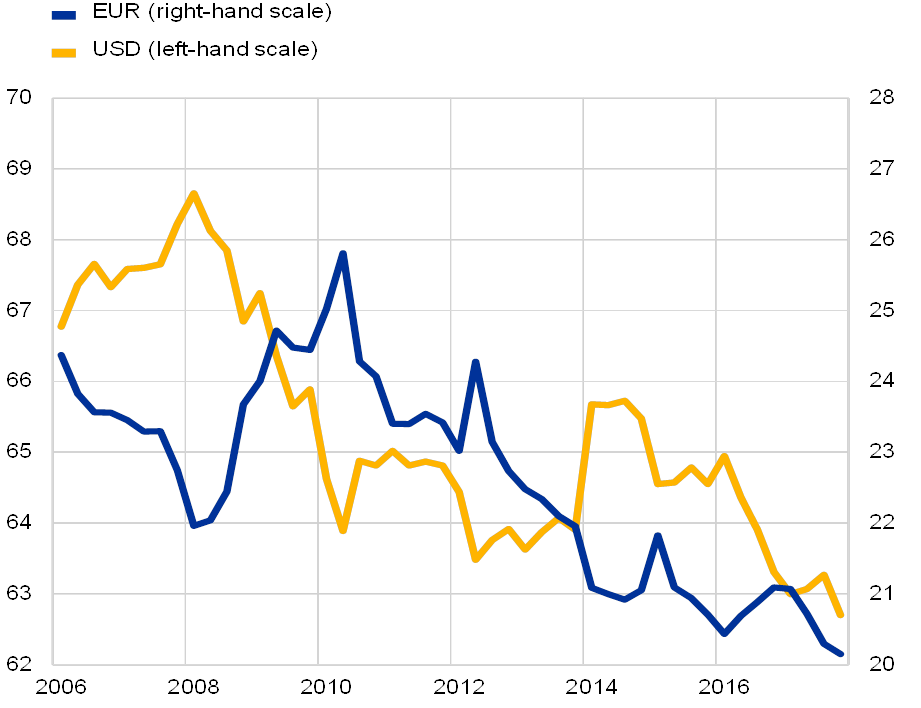

In fact – and you can see this on Slide 3 – some shifts are already taking place. Both the euro and the dollar have lost similar ground as international reserve currencies since the global financial crisis.[14] It remains to be seen whether this is a short-lived development or the beginning of a larger trend.

The euro and the US dollar have lost ground as international reserve currencies

Share of the euro and the US dollar in global foreign exchange reserves

(percentages)

Sources: IMF and ECB calculations.Notes: Data adjusted for exchange rate valuation effects. The latest observations are for the fourth quarter of 2017

So how are we as central bankers affected by these developments?

The ECB, of course, does not take a view on foreign policy questions. It is not for us to decide on Europe’s role in the world, or on which countries outside Europe choose to use the euro and which do not. We continue to see the global role of the euro as being primarily a market-led process.

That said, we are not indifferent to the current debate in Europe, for two major reasons.

First, we see an alignment between the policies that will strengthen the euro’s global role and the policies that are needed to make the euro area more robust. We support efforts to improve the design of Economic and Monetary Union (EMU), and these efforts will also, indirectly, foster a stronger international role for the euro.

Second, a stronger global role for the euro may have tangible consequences for the conduct of monetary policy.

In my remarks this morning, I would like to explain these two points in more detail.

Policies supporting the euro’s international role

The decline of the euro’s international role is, on the face of it, puzzling. The euro area displays two of the fundamental elements that economists deem essential in fostering a currency’s international use.

The first element is that it is the currency of a large economy that is comparable in economic size to that of the United States.[15] The second is that it is issued by the world’s largest trading bloc.[16] These two elements featured prominently in the discussions that took place 20 years ago as to whether the euro could match the international standing of the dollar.[17]

Secular factors unrelated to the euro area – such as the parallel rise of the renminbi – have certainly played a role in stalling the euro’s progress. But what is also clear is that establishing an international currency is not just a matter of economic size.

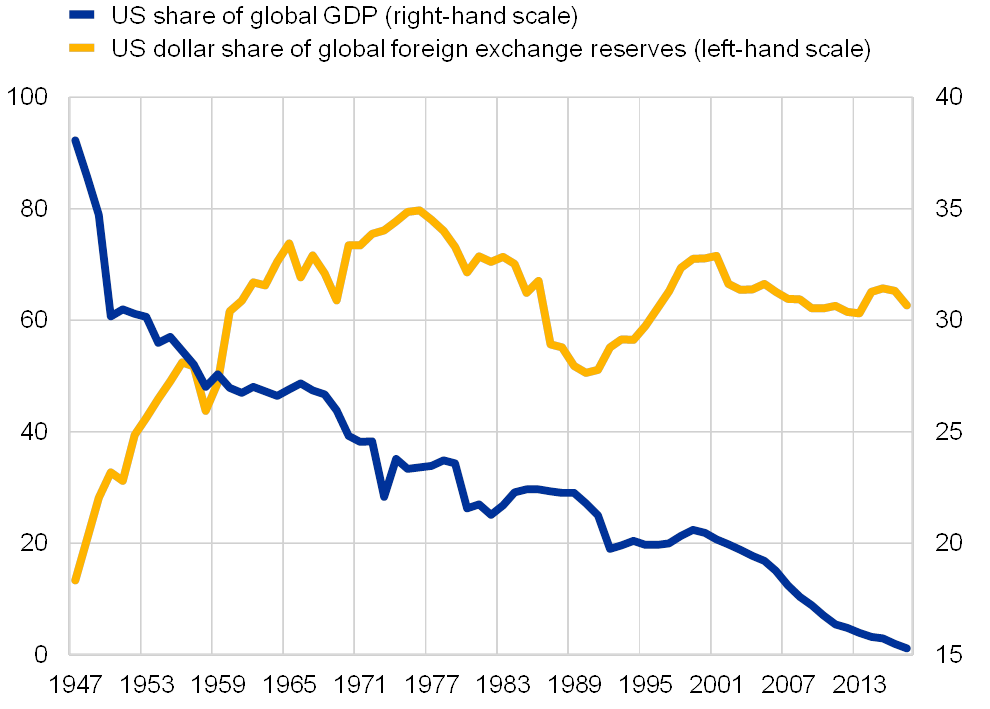

You can see this clearly on Slide 4. The United States accounts for a much smaller share of the global economy today than it did after World War II, and yet the US dollar is still, by far, the leading global reserve currency, now like then.

Economic size is not the only factor determining global currency use

Importance of the US and the US dollar in the global economy

(percentages)

Sources: Maddison project, IMF WEO and Eichengreen, Mehl and Chitu (2016).Note: Share of the US in global GDP in PPP terms. The last observation is for 2017.

This suggests that factors specific to the euro area are likely to have prevented the euro from rising more forcefully as an international currency. I see these factors as closely related to three broad shortcomings in the institutional design of the EU and EMU:

- First – the ability to provide stability both domestically and internationally.

- Second – the limited depth and liquidity of euro area financial markets.

- And third – Europe not speaking with one voice on international matters, including national security.

An international currency must be stable

Take stability first. Empirical research confirms that, next to size and openness, stability is a key determinant of international currency use. But stability means different things to international investors, who hold the currency as a store of value, and international borrowers, who use it as a financing vehicle.

For borrowers, broadly speaking, stability derives primarily from central banks’ monetary policy frameworks. Research finds that the currencies that become dominant in international financing are the ones whose central bank actively pursues an inflation stabilisation policy that protects borrowers’ real debt burdens.[18]

To deliver this stability, central bank independence is crucial. That aspect was highlighted in 2011 by the US Treasury Secretary, Timothy Geithner, in the context of the renminbi becoming part of the IMF’s SDR basket.[19]

For investors, stability mainly comes from a currency’s ability to act as a safe haven in times of global financial stress.[20] This is what some have coined the “exorbitant duty” of international currency status, which offsets the “exorbitant privilege” in crisis times, since it leads to negative wealth effects for the currency issuer.[21]

Theoretical work suggests that investors are more likely to perceive sovereign debt as safe if the fundamentals of the issuer are strong relative to other possible issuers, but not necessarily strong on an absolute basis.[22] This may explain, for example, why investors did not rebalance away from US Treasuries throughout the global financial crisis, despite the stark deterioration in the United States’ fiscal position.

For currency unions, however, absolute fundamentals arguably matter more. The reason is that, in the absence of a common consolidated balance sheet, sovereign debt exhibits a higher degree of credit risk than it does in economies that can pursue their own monetary policy. Public debt can therefore behave like private debt when risk aversion rises.[23]

This fact was not unknown. The idea of the euro was always that a credible set of fiscal rules would ensure that national sovereign debt would be safe. But the euro area debt crisis exposed flaws in the design of our monetary union.

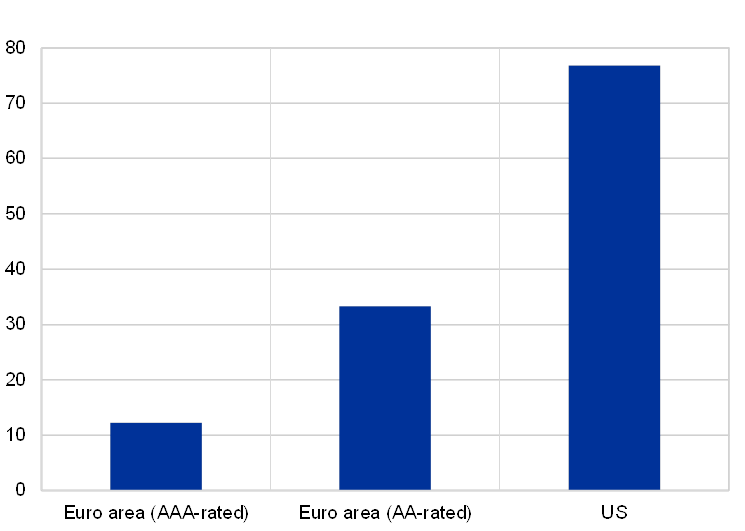

With the crisis, the number of AAA-rated euro area sovereigns fell from eight to three. Today, AAA-rated euro area sovereign debt amounts to just 10% of GDP. In the United States it is more than 70%. You can see this on Slide 5.

The supply of euro area safe assets has declined and is small relative to the US

Outstanding amount of AAA-rated debt securities issued by euro area central governments

(EUR billions)

Sources: OECD Government Statistics and ECB staff calculations.Notes: Outstanding amounts at market value. The blue bars in the chart report debt securities issued that are rated AAA/Aaa both by Standard and Poor’s and Moody’s (local currency long-term debt rating). Totals for 2007 includes Austria, Finland, France, Germany, Ireland, Luxembourg, the Netherlands and Spain. Totals for 2018 include Germany, Luxembourg and the Netherlands.

Debt securities issued by central governments

(2018; as percent of GDP)

Sources: OECD Government Statistics, IMF WEO and ECB staff calculations.Notes: Outstanding amounts at market value for the euro area; publicly held Treasury securities outstanding for the US. See the preceding footnote for definitions of the rating universe.

But Europe has learnt its lesson. Considerable efforts have been made in recent years to improve the euro area governance framework, and work is still ongoing. We now have a single supervisor for large banks, a single framework for resolving failing institutions, a single fund to finance those resolution activities and, soon, a single backstop for that fund.

We have also established the European Stability Mechanism, which provides a safety net for sovereigns threatened with losing market access, provided that they implement sound economic policies.

But for the euro to act as a true, effective hedge in times of stress, and therefore to attain and maintain international status, we need to further strengthen the fiscal dimension of EMU.

Sound fiscal and structural policies are needed to provide international investors with what they need most: a large and elastic supply of safe assets. The fact that the supply of euro-denominated safe assets can shrink at precisely the time when demand for such assets is rising has not been lost on investors. It is likely a dominant factor keeping the euro from having a stronger international role.

We know that the journey towards a true European safe asset, one that does not vanish on rainy days, will be long and full of perils. While progressing towards this objective, we should thus also focus our efforts on “upgrading” the credit quality of outstanding liabilities, which can only be achieved if governments make public debt more sustainable by committing to credible fiscal rules.

The need for deeper and more liquid capital markets

The second, and related, shortcoming of EMU is the segmentation of its capital markets.

Deep and liquid financial markets are fundamental to a currency’s ability to attain international status. They reduce transaction costs, making the currency more attractive for international financing and settlement, and – as more liquid markets mitigate rollover risk – they are perceived as safer by investors.[24]

This is not just theory. Recent research shows that capital market depth was critical in helping the US dollar to catch up with, and then overtake, the pound sterling in the first half of the last century. Financial deepening was by far the most important contributor to the increase in the share of dollar-denominated international bonds issued between 1918 and 1932. Its impact dwarfed that of economic size or credibility.[25]

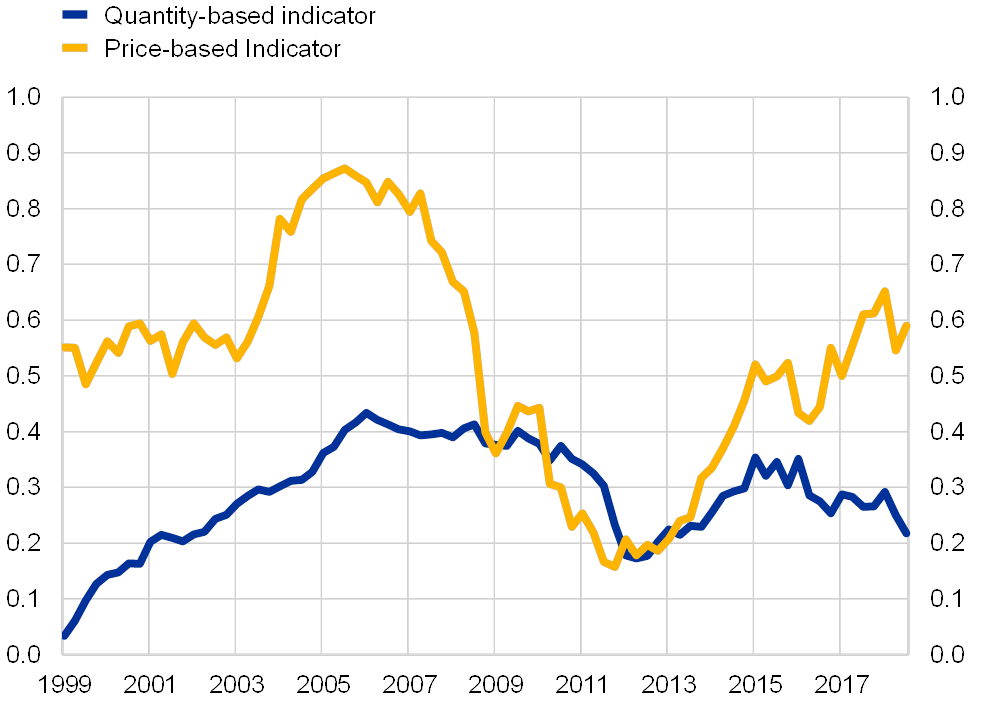

European capital markets appeared to be becoming more integrated, and hence deeper, prior to 2008. But this impression was based more on price convergence than on real cross-border integration. You can see this clearly on Slide 6, which shows composite indicators of euro area financial integration produced by the ECB. The quantity-based indicator remains at about half of its pre-crisis peak, and at very low levels in absolute terms.[26]

Financial fragmentation has weighed on the euro’s global standing

Financial integration in the euro area

(indices)

Source: ECB.Notes: The price-based composite indicator aggregates ten indicators covering the period from the first quarter of 1995 to the fourth quarter of 2017, while the quantity-based composite indicator aggregates five indicators available from the first quarter of 1999 to the third quarter of 2017. The indicators are bounded between zero (full fragmentation) and one (full integration). Increases in the indicators signal greater financial integration. For a detailed description of the indicators and their input data, see ECB (2018), Financial integration in Europe, Frankfurt am main. The latest data are for the third quarter of 2018.

Cyclical factors and the “doom loop” between euro area banks and sovereigns have certainly aggravated market segmentation. But the underlying reasons for it are structural. Capital markets in Europe are still fragmented along national lines, since various legal and institutional barriers hinder the creation of a single pool of liquidity.

This is precisely why policymakers have now put their weight behind the capital markets union (CMU) project. But progress remains too slow. We at the ECB see CMU as a key priority for the next European Commission and Parliament. [27]

The ECB has been complementing these efforts by upgrading its payment system infrastructure, which contributes to market integration and, in turn, to the depth and liquidity of euro area securities markets. Recent initiatives include the successful launch of our securities settlement platform TARGET2-Securities, a new platform for instant payments and the upgrade of our large-value transactions TARGET system. In time, these systems may offer international market participants easier access to our currency.[28]

International currencies carry a security premium

The third and final factor that is likely to have held back the international role of the euro relates to the EU’s ability to speak with one voice on international affairs.

I will venture very warily into what is certainly not central bankers’ territory. But empirical evidence supports the view that the US dollar benefits from a substantial security premium. Nations that depend on the US security umbrella hold a disproportionate share of their foreign reserves in dollars.

Global geopolitical outreach matters for international currency status

Predicted share of the US dollar in the foreign exchange reserves of selected countries

(percentages)

Source: Eichengreen, B., A. Mehl and L. Chiţu (2019).Note: The figures show the predicted shares of the US dollar in the foreign reserve holdings of five countries which depend on the US security umbrella. Predicted shares are computed under two scenarios: (i) using estimates from a model restricted to standard economic determinants of international currency choice (shown as yellow bars); and (ii) using estimates from a model expanded to include the effect on international currency choice of the countries’ NATO membership (shown as red bars). Actual US dollar shares are shown as blue bars. The actual dollar shares are based on publicly available estimates for the year 1987 (Korea), 2004 (Germany), 2006 (Japan), 2007 (Saudi Arabia) and 2016 (Taiwan); see Eichengreen et al. (2019) for further details on the sources for the data.

You can see this on Slide 7: a model restricted to economic factors – the yellow bars – under-predicts, by a wide margin, the dollar reserves of countries dependent on the United States for their security. A model including their NATO membership – the red bars – comes much closer to the actual shares. By one estimate, military alliances boost the share of a currency in the partner country’s foreign reserve holdings by about 30 percentage points.[29]

This is not a new phenomenon. During the late 19th century, a growing share of Deutsche Marks in Austria-Hungary’s reserves went hand in hand with the Triple Alliance, i.e. the secret agreement between Germany, Austria-Hungary and Italy signed in 1882 and renewed periodically until World War I. The increasing importance of French francs in Russia’s reserves in the years after the Franco-Russian alliance of 1894 reflected similar security patterns.[30]

Of course, this aspect of a currency’s international status extends beyond EMU. But it has a clear implication for policymakers. Europe already exerts global leadership in regulatory, competition and trade domains.[31] European initiatives to foster cooperation on security and defence, to speak with one voice on international affairs, and, in short, to further assert global leadership, might also help promote the euro’s global outreach.

The monetary policy consequences of a greater international role for the euro

Now, one important aspect that is often overlooked in the debate about strengthening the international role of the euro is what it would mean for the ECB’s monetary policy. This is what I would now like to discuss.

As I see it, the monetary policy relevance of an international currency has probably increased over time, on account of both the evolution of the international monetary system itself and the way central banks implement monetary policy today, in particular at the zero-lower bound.

More specifically, I see three broad implications for the conduct and transmission of our monetary policy, all of which we would need to understand and take into account when defining the appropriate stance for the euro area.

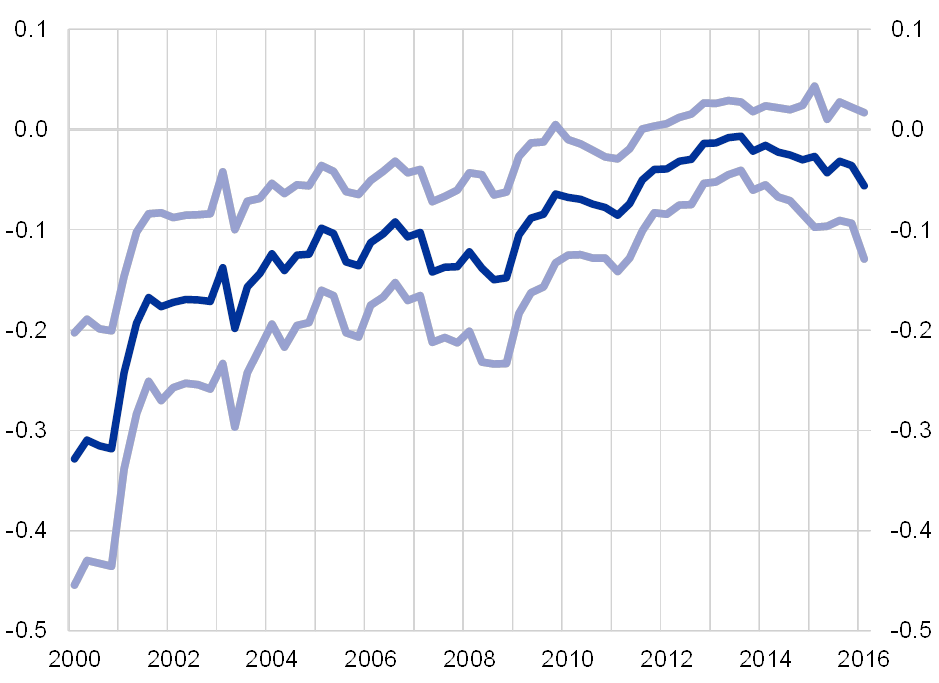

First is the effect on exchange rate pass-through.

This is in part mechanical: the more the domestic currency is used for trade invoicing, the less the pass-through to import prices in the face of fluctuations in the exchange rate. This holds not only over the short run, when prices are sticky, but also over the long run when they are adjusted by producers.[32]

The tight correlation between domestic currency invoicing and exchange rate pass-through is evident in the euro area.[33] As you can see on the left-hand chart of Slide 8, euro area countries with a greater share of imports invoiced in euro – those on the south-east corner of the chart – are more insulated from fluctuations in the euro exchange rate and have lower pass-through to import prices.

International currency status lowers exchange rate pass-through

Exchange rate pass-through to import prices vs. euro invoicing across euro area countries

Source: The international role of the euro, ECB, July 2015.Notes: Long-run exchange rate pass-through is estimated using a standard log-linear regression model of the quarterly log change in import price unit values on the quarterly changes of the standard broad measure of the NEER-38 of the euro, a quarterly effective measure of inflation in production costs of the euro area’s major trading partners and the quarterly log change in industrial production (excluding construction). The estimation sample spans the time period from the first quarter of 2000 to the last quarter of 2014. The share of euro invoicing reported on the x-axis is the average over the sample period. The black line is a fitted regression line.

Exchange rate pass-through to euro area import prices in response to a monetary policy shock

(percent)

Source: ECB calculations based on Casas et al. (2017).Note: The figure plots the impulse response of import prices to a negative 25 basis point cut in the short-term interest rate leading to 1% depreciation in the exchange rate under local currency (euro) pricing and dominant currency (dollar) pricing obtained in a calibrated small open-economy model.

The degree of pass-through, in turn, has a strong influence on the transmission of shocks, which has differing implications for monetary policy.

On the one hand, lower pass-through means that import prices are better shielded from exogenous exchange rate shocks, and monetary policy can focus more on domestic sources of inflationary pressures.[34]

As of today, more than 90% of US imports are invoiced in US dollars. By comparison, less than 50% of extra-euro area imports are invoiced in euro. If this share were to increase to, say, 70%, the sensitivity of import prices to exchange rate movements would decline by around one-third.

On the other hand, the effect of domestic monetary policy on import prices is more limited when pass-through is low. You can see this on the right-hand chart, which plots simulations from a calibrated model of the exchange rate pass-through. Clearly, increased local currency pricing would, in principle, attenuate an important lever of monetary policy.[35]

But it is also true that, in the euro area, exchange rate pass-through has already notably declined over the past two decades, mainly due to the declining share of commodity imports and the increasing role of global value chains.[36] You can see this on Slide 9. Today, the pass-through to final consumer price inflation may be less than a third of what it was at the beginning of the century.[37]

There has been a marked decline in exchange rate pass-through over time

Exchange rate pass-through to HICP inflation

(percent)

Sources: Eurostat and ECB staff calculations.Notes: The chart shows the cumulated impulse response (dark blue line) of HICP inflation to a 1% appreciation in the NEER after three years over time and the respective 95% confidence bands (light blue lines). The cumulated impulse response is based on the updated estimation of Hahn (2003) over a 20-year rolling window from the first quarter of 1980 to the first quarter of 2016. Each point on the dark blue line refers to the end point of each 20-year rolling sample, with the first sample referring to the period from the second quarter of 1981 to the first quarter of 2000 and the last sample to the period from the second quarter of 1996 to the first quarter of 2016.

The second way in which an international currency is relevant for monetary policy is its effect on interest rates.

In principle, international currency issuers enjoy greater monetary autonomy. Central banks in small open economies, for example, are typically more heavily exposed to foreign spillovers in setting interest rates than those presiding over an internationally dominant currency.

But international currencies are not isolated from foreign spillovers. Greater external demand for euro area securities, for instance, can increase the influence of foreign factors on domestic monetary and financial conditions.[38]

For example, in periods of global stress, investors rush to the safety and liquidity of dollar-denominated securities, thereby compressing term premia. These effects, however, are typically temporary and policymakers can hence afford to look through such volatility.[39]

Other effects may prove more durable, however. The past experience of the Federal Reserve highlights these challenges. It is well documented that the large demand for US securities by foreign central banks in the run-up to the financial crisis contributed to the decline in longer-term US interest rates, thereby in part offsetting the parallel tightening efforts by the Federal Open Market Committee.[40]

In other words, the effects of such purchases by foreign central banks do not fundamentally differ from those of domestic central banks which purchase assets as part of their efforts to stimulate the economy – quantitative easing.[41]

It is not that these effects are completely absent in the euro area today. As the second most important reserve currency, demand from foreign central banks can also be expected to have affected euro area financing conditions.[42]

But there is a difference, and it is due to a distinctive feature of the euro area which I have already highlighted: the lack of a single safe asset. We have seen foreign demand driving a wedge between sovereign bond yields in the euro area. Specifically, foreign central banks currently hold more than 40% of their euro reserves in German government bonds, well above Germany’s share of total outstanding euro-denominated sovereign bonds, which is around 15%.[43]

The implication is that efforts to improve the stability of our currency union could be expected to lead to a more even distribution of reserve demand effects across the euro area. This, by itself, would benefit the transmission of our monetary policy.

The final monetary policy implication of a stronger international role for the euro is that spillovers and spillbacks through international trade and finance would probably be larger.

There are two broad channels to consider here.

The first is that the increased use of the euro as an international funding currency would amplify the so-called international risk-taking channel of monetary policy, which operates through international bank leverage.[44] As you can see on my last slide, the risk-taking channel is strong for the United States.

International currency status increases monetary policy spillovers

Strong link between US dollar movements and international dollar lending

(%)

Sources: BIS and ECB staff calculations.Notes: Growth in US dollar lending refers to quarterly changes in cross-border loans and deposits in US dollars of BIS reporting banks; NEER stands for nominal effective exchange rate (positive changes indicate a dollar appreciation). The sample period is Q1/2002-Q3/2015 as in Avdjiev, Koch and Shin (2017). The black line is a fitted regression line.

When monetary policy eases, the US dollar depreciates, and international lending in dollars grows because emerging market borrowers’ balance sheets look stronger in dollar terms, which encourages lenders to provide them with dollar-denominated credit.

Second, if the euro were used more for trade among third countries, a depreciation of the euro would make all euro-denominated exports cheaper, from euro area and non-euro area firms alike. This would cause an increase in global trade with potentially positive spillbacks.[45] And since the euro area is more open to trade than the United States, the spillbacks to it could even be larger than those to the United States.

The flipside is that central banks in smaller economies, not least in emerging market economies, could turn more frequently to the ECB for currency swap lines when the tide turns – i.e. if and when monetary policy is tightened and the availability of international liquidity in euro dries up.

The ECB would then be called on to increase its activities as an international lender of last resort. Any extension of the global network of currency swap lines would, however, have to be based on sound monetary arguments. Central banks are mindful of global financial stability, but they always act in full discretion and within domestic mandates.

Conclusion

It is time for me to conclude.

The decline in the euro’s international role in recent years is primarily a symptom of the initial fault lines in Economic and Monetary Union. There is thus a close alignment between the policies that will strengthen the euro’s global role and the policies that are needed to make the euro area more robust. The ECB continues to see the global role of the euro as being primarily a market-led process. Nevertheless, we support efforts to overcome the shortcomings in the design of our monetary union, and these efforts will also, indirectly, foster a stronger international role for the euro.

At the same time, a stronger global role for the euro may have tangible consequences for the conduct of monetary policy, all of which we would need to understand and take into account when designing the common monetary policy for the euro area. But provided the right economic policies are adopted, a stronger global role of the euro could help facilitate the transmission of monetary policy across euro area financial markets and reduce perilous fragmentation.

Thank you.

- [1]I would like to thank J. Gräb, A. Mehl and J. Yiangou for their contributions to this speech. I remain solely responsible for all opinions contained herein.

- [2]See, for example, Draghi, M. (2018), “Europe and the euro 20 years on”, speech at Laurea Honoris Causa in Economics by University of Sant’Anna, Pisa, 15 December.

- [3]See European Commission (2018), “Eurobarometer: Support for the euro steady at all-time high levels”, 20 November.

- [4]See Henning, R. (1998), “Systemic Conflict and Regional Monetary Integration: The Case of Europe”, International Organization, Vol. 52, No 3, pp. 537-573.

- [5]In 2008, some economists expected the euro to overtake the US dollar as an international reserve currency by around 2020. See, for example, Chinn, M. and Frenkel, J. (2008), “Why the euro will rival the dollar”, International Finance, Vol. 11(1), pp. 49-73.

- [6]See Juncker, J.C. (2018), “The Hour of European Sovereignty”, State of the Union Address 2018; European Commission (2018), “Towards a stronger international role of the euro”, European Commission contribution to the European Council and the Euro Summit, 5 December; and European Council (2018), “Statement of the Euro Summit”, 14 December.

- [7]See Cœuré, B. (2018), “Asserting Europe’s leadership”, panel remarks at Les rencontres économiques d’Aix-en-Provence, 8 July.

- [8]See, for example, Tooze, A. and Odendahl, C. (2018), “Can the euro rival the dollar?”, CER Insight, Centre for European Reform, 4 December.

- [9]See, for example, European Commission (2018), ibid.

- [10]“In the last century [the] history [of monetary orders] was marked by a fundamental shift in relations between money and the two entities to which it had been anchored from time immemorial: a commodity (mainly gold) and the ‘sovereign’ or, to put it another way, intrinsic value and political power. Over the decades, the commodity anchor was relaxed while the political anchor was correspondingly strengthened.” See Padoa-Schioppa, T. (2010), “The Ghost of Bancor: The Economic Crisis and the Global Monetary Disorder”, Triffin Lecture, Louvain-la-Neuve, 25 February.

- [11] Increasing returns and network effects are important determinants of international currency status and support the continued use of incumbent currencies. Small initial differences accumulate over time, resulting in the disproportionate and persistent use of one currency. Early discussions of these effects include: Krugman, P. (1984), “The International Role of the Dollar: Theory and Prospect,” in Bilson, J. and Marston, R. (eds.), Exchange Rate Theory and Practice, Chicago: University of Chicago Press, pp. 261-278; and Rey, H. (2001), “International Trade and Currency Exchange,” The Review of Economic Studies, Vol. 68, No 2, pp. 443-464. In line with this, it is conventionally believed that it took between 30 and 70 years for the US dollar to dethrone the pound sterling as the leading international currency once the United States surpassed the United Kingdom as the leading global economic powerhouse and trading nation (see Triffin, R. (1960), Gold and the Dollar Crisis: The Future of Convertibility, New Haven: Yale University Press). But more recent scholarly work suggests that this change occurred faster than conventionally assumed because the increasing returns of networks may not be as strong as commonly posited (see, for example, Chiţu, L., Eichengreen, B. and Mehl, A. (2014), “When did the dollar overtake sterling as the leading international currency? Evidence from the bond markets,” Journal of Development Economics, Vol. 111, pp. 225-245).

- [12]See Eichengreen, B., Mehl, A. and Chiţu, L. (2017), How Global Currencies Work: Past, Present and Future, Princeton University Press.

- [13]On the prospects for a multi-polar monetary system, see also Bénassy-Quéré, A. and Cœuré, B. (2010), “Le rôle international de l’euro : chronique d’une décennie”, Revue d’économie politique, Vol. 120, pp. 355-377.

- [14]Official reserve managers, including the ECB, have diversified a small part of their portfolios towards non-traditional currencies, with the shares of the Chinese renminbi, Australian dollar, Canadian dollar and other non-traditional units trebling to about 7% of global foreign exchange reserves.

- [15]In purchasing power parity terms, the United States accounts for about 15% of world GDP, compared with 11% for the euro area. Economic size is an important determinant of international currency use in random matching models considering currency choice as a double-coincidence-of-wants problem (see Matsuyama, K., Kiyotaki, N. and Matsui, A. (1993), “Toward a Theory of International Currency,” The Review of Economic Studies, Vol. 60, No 2, pp. 283-307).

- [16]The United States accounts for about 11% of global trade, compared with 14% for the euro area.

- [17]See, for example, Bergsten, F. (1997), “The Dollar and the Euro,” Foreign Affairs, Vol. 76, pp. 83-95.

- [18]This is the essence of the international Fisher debt-deflation channel which works through the effects of monetary policy on the exchange rate and inflation risk premia (see Eren, E. and Malamud, S. (2018), “Dominant Currency Debt”, CEPR Discussion Paper, No 13391).

- [19]“We believe that currencies of large economies heavily used in international trade and financial transactions should become part of the SDR basket, and that to achieve this objective, the concerned countries should have flexible exchange rate systems, independent central banks, and permit the free movement of capital flows.” See Geithner, T. (2011), Statement at the High-level Seminar on the International Monetary System, Nanjing, 31 March.

- [20]Certain academics have created models to show that currency depreciations make holding a unit unattractive and discourage its international use insofar as it will not be perceived as a reliable store of value. For example, see: Devereux, M. and Shi, S. (2013), “Vehicle Currency,” International Economic Review, Vol. 54(1), pp. 97-133.

- [21]See Gourinchas, P.-O., Govillot, N. and Rey, H. (2011), “Exorbitant Privilege and Exorbitant Duty”, Working Paper Series, University of California, Berkeley. See also Caballero, R., Farhi, E. and Gourinchas, P.-O. (2015), “Global Imbalances and Currency Wars at the ZLB,” NBER Working Paper, No 21670.

- [22]See He, Z., Krishnamurthy, A. and Milbradt, K. (2019), “A Model of Safe Asset Determination,” American Economic Review, forthcoming.

- [23]See Cœuré, B. (2016), “Sovereign debt in the euro area: too safe or too risky?”, keynote address at Harvard University’s Minda de Gunzburg Center for European Studies, 3 November.

- [24]The dynamic interaction between debt liquidity and safety is non-trivial, however, as shown in He et al. (2019), op. cit. If global demand for safe assets is high, large debts can enhance safety because they offer greater liquidity and so reduce rollover risk. Conversely, if demand for safe assets is low, large debt may increase rollover risk.

- [25]Chiţu, L., Eichengreen, B. and Mehl, A. (2014), op. cit.

- [26]The price-based composite indicator is about 30% below.

- [27]See Building a Capital Markets Union – Eurosystem contribution to the European Commission’s GreenPaper, 21 May 2015.

- [28]The new platform for instant payments launched by the ECB in November 2018 might offer an alternative to credit cards for payments online. The reform of the large-value transactions TARGET system would make it technically possible to establish direct links with comparable systems worldwide. In turn, this would enable settlement of foreign exchange transactions and offer an alternative to other systems.

- [29]See Eichengreen, B., Mehl, A. and Chiţu, L., “Mars or Mercury? The Geopolitics of International Currency Choice”, Economic Policy, forthcoming.

- [30]Ibid.

- [31]Europe already exerts global leadership in the regulatory domain. The obligation for companies to respect EU standards when exporting products to the Single Market, combined with the size of this market, means that the EU tends to influence standards elsewhere – the so-called Brussels effect. The EU is the top trading partner for no fewer than 80 countries.

- [32]See Gopinath, G., Itskhoki, O. and Rigobon, R. (2010), “Currency Choice and Exchange Rate Pass-Through”, American Economic Review, Vol. 100, No 1, pp. 304-336.

- [33]For further details, see ECB (2015), “The international role of the euro”, Frankfurt am Main, July.

- [34]Price increases in local currency by exporters will, of course, still be transmitted to domestic consumer prices.

- [35]The estimates are taken from Casas, C., Diez, F., Gopinath, G. and Gourinchas, P.-O. (2017), “Dominant Currency Paradigm: A New Model for Small Open Economies”, IMF Working Papers, No 17/264.

- [36]See Cœuré, B. (2017), “The transmission of the ECB’s monetary policy in standard and non-standard times”, speech at the workshop “Monetary policy in non-standard times”, Frankfurt am Main, 11 September. It is ultimately the source of exchange rate movements that is likely to determine the degree, and at times even the direction, of pass-through to consumer prices. For the role of import shares, see Campa, J. and Goldberg, L. (2005), “Exchange Rate Pass-Through into Import Prices”, The Review of Economics and Statistics, Vol. 87(4), pp. 679-690.

- [37]See European Central Bank (2016), “Exchange rate pass-through into euro area inflation”, Economic Bulletin, July.

- [38]Concerns about foreign influences on domestic monetary policy are of course not new. As early as the 1970s, the Deutsche Bundesbank was expressing misgivings about the rapid internationalisation of the Deutsche Mark, fearing that it could lead to heightened “hot money” flows that would, in turn, make monetary aggregates more volatile and difficult to interpret.

- [39]And to the extent that such flight-to-safety flows affect the exchange rate, the aforementioned reduced pass-through to import prices that international currencies imply also mitigate more direct effects on domestic prices.

- [40]See Bernanke, B. (2005), “The Global Saving Glut and the U.S. Current Account Deficit”, speech at the Homer Jones Lecture, St. Louis, Missouri, 14 April. On the impact and transmission channel of foreign official purchases on US Treasury yields in the mid-2000s, see also: Kaminska, I. and Zinna, G. (2014), “Official Demand for U.S. Debt; Implications for U.S. Real Interest Rates”, IMF Working Papers, No 14/66; and Krishnamurthy, A. and Vissing-Jorgensen, A. (2012), “The Aggregate Demand for Treasury Debt”, Journal of Political Economy, Vol. 120, No 2, pp. 233-267.

- [41]See, for instance, Warnock, F. and Warnock, V. (2009), “International capital flows and U.S. interest rates”, Journal of International Money and Finance, Vol. 28(6), pp. 903-919; and Beltran, D., Kretchmer, M., Marquez, J. and Thomas, C. (2013), “Foreign holdings of U.S. Treasuries and U.S. Treasury yields”, Journal of International Money and Finance, Vol. 32(C), pp. 1120-1143.

- [42]See Cœuré, B. (2018), “The persistence and signalling power of central bank asset purchase programmes”, speech at the 2018 US Monetary Policy Forum, New York City, 23 February.

- [43]See IMF Coordinated Portfolio Investment Survey (2018).

- [44]Bruno and Shin (2015) argue that looser US monetary policy encourages global banks to leverage more in dollars (on the supply side) and emerging markets to borrow more in dollars (on the demand side). The latter reflects the fact that the ensuing dollar depreciation flatters emerging markets’ balance sheets, hence appearing less risky. See Bruno, V. and Shin, H. S. (2015), “Capital flows and the risk-taking channel of monetary policy”, Journal of Monetary Economics, Vol. 71(C), pp. 119-132. Miranda-Agrippino and Rey (2015) find evidence of large financial spillovers from the hegemon to the rest of the world. US monetary policy explains an important share of the variance of returns of risky assets around the world. See Miranda-Agrippino, S. and Rey, H. (2015), “US Monetary Policy and the Global Financial Cycle”, NBER Working Paper, No 21722.

- [45]See Boz, E., Gopinath, G. and Plagborg-Møller, M. (2017), “Global Trade and the Dollar”, NBER Working Paper No 23988.

Europeiska centralbanken

Generaldirektorat Kommunikation och språktjänster

- Sonnemannstrasse 20

- 60314 Frankfurt am Main, Tyskland

- +49 69 1344 7455

- media@ecb.europa.eu

Texten får återges om källan anges.

Kontakt för media