Economic Bulletin Issue 5, 2022

Update on economic, financial and monetary developments

Summary

At its meeting on 21 July 2022, in line with its strong commitment to its price stability mandate, the Governing Council took further key steps to make sure inflation returns to its 2% target over the medium term. The Governing Council decided to raise the three key ECB interest rates by 50 basis points and approved the Transmission Protection Instrument (TPI).

The Governing Council judged that it was appropriate to take a larger first step on its policy rate normalisation path than signalled at its previous meeting. This decision was based on the Governing Council’s updated assessment of inflation risks and the reinforced support provided by the TPI for the effective transmission of monetary policy. It will support the return of inflation to the Governing Council’s medium-term target by strengthening the anchoring of inflation expectations and by ensuring that demand conditions adjust to deliver its inflation target in the medium term.

At the Governing Council’s upcoming meetings, further normalisation of interest rates will be appropriate. The frontloading of the exit from negative interest rates to the July meeting allows the Governing Council to make a transition to a meeting-by-meeting approach to interest rate decisions. The Governing Council’s future policy rate path will continue to be data-dependent and will help to deliver on its 2% inflation target over the medium term. In the context of its policy normalisation, the Governing Council will evaluate options for remunerating excess liquidity holdings.

The Governing Council assessed that the establishment of the TPI was necessary to support the effective transmission of monetary policy. In particular, as the Governing Council continues normalising monetary policy, the TPI will ensure that the monetary policy stance is transmitted smoothly across all euro area countries. The singleness of the Governing Council’s monetary policy is a precondition for the ECB to be able to deliver on its price stability mandate.

The TPI will be an addition to the Governing Council’s toolkit and can be activated to counter unwarranted, disorderly market dynamics that pose a serious threat to the transmission of monetary policy across the euro area. The scale of TPI purchases would depend on the severity of the risks facing policy transmission. Purchases are not restricted ex ante. By safeguarding the transmission mechanism, the TPI will allow the Governing Council to more effectively deliver on its price stability mandate.

In any event, the flexibility in reinvestments of redemptions coming due in the pandemic emergency purchase programme (PEPP) portfolio remains the first line of defence to counter risks to the transmission mechanism related to the pandemic.

Economic activity

Economic activity has decelerated in key advanced economies since the last Governing Council meeting in June. In the United States, consumer spending in May surprised significantly to the downside, while there continue to be solid employment gains. Downside risks to the US outlook have increased overall. Activity data for the United Kingdom surprised to the downside, and consumer confidence fell to a record low. Growth in China is recovering after the country emerged from the most recent wave of the pandemic, but remains weak. Meanwhile, inflation in key advanced economies continues to rise, with elevated month-on-month gains, and is increasingly spreading to the service sector. Since the June Governing Council meeting, oil prices have fallen by around 14% as higher risks of an economic slowdown outweigh supply disruptions. Gas prices have increased sharply in Europe owing to reduced supply from Russia, implying an aggravation of the energy shock despite the fall in oil prices.

Euro area economic activity is slowing. Russia’s unjustified aggression towards Ukraine is an ongoing drag on growth. The impact of high inflation on purchasing power, continuous supply constraints and higher uncertainty are having a dampening effect on the economy. Firms continue to face higher costs and disruptions in their supply chains, although there are tentative signs that some of the supply bottlenecks are easing. Taken together, these factors are significantly clouding the outlook for the second half of 2022 and beyond.

At the same time, economic activity continues to benefit from the reopening of the economy, a strong labour market and fiscal policy support. In particular, the full reopening of the economy is supporting spending in the services sector. As people start to travel again, tourism is expected to help the economy in the third quarter of this year. Consumption is being supported by the savings that households built up during the pandemic and by a strong labour market.

Fiscal policy is helping to cushion the impact of the war in Ukraine for those bearing the brunt of higher energy prices. Temporary and targeted measures should be tailored so as to limit the risk of fuelling inflationary pressures. Fiscal policies in all countries should aim at preserving debt sustainability, as well as raising the growth potential in a sustainable manner to enhance the recovery.

Inflation

Inflation increased further to 8.6% in June. Surging energy prices were again the most important component of overall inflation. Market-based indicators suggest that global energy prices will stay high in the near term. Food inflation also rose further, standing at 8.9% in June, in part reflecting the importance of Ukraine and Russia as producers of agricultural goods.

Persistent supply bottlenecks for industrial goods and recovering demand, especially in the services sector, are also contributing to the current high rates of inflation. Price pressures are spreading across more and more sectors, in part owing to the indirect impact of high energy costs across the whole economy. Accordingly, most measures of underlying inflation have risen further.

The Governing Council expects inflation to remain undesirably high for some time, owing to continued pressures from energy and food prices and pipeline pressures in the pricing chain. Higher inflationary pressures are also stemming from the depreciation of the euro exchange rate. But looking further ahead, in the absence of new disruptions, energy costs should stabilise and supply bottlenecks should ease, which, together with the ongoing policy normalisation, should support the return of inflation to the Governing Council’s target.

The labour market remains strong. Unemployment fell to a historical low of 6.6% in May. Job vacancies across many sectors show that there is robust demand for labour. Wage growth, also according to forward-looking indicators, has continued to increase gradually over the last few months, but still remains contained overall. Over time, the strengthening of the economy and some catch-up effects should support faster growth in wages. Most measures of longer-term inflation expectations currently stand at around 2%, although recent above-target revisions to some indicators warrant continued monitoring.

Risk assessment

A prolongation of the war in Ukraine remains a source of significant downside risk to growth, especially if energy supplies from Russia were to be disrupted to such an extent that it led to rationing for firms and households. The war may also further dampen confidence and aggravate supply-side constraints, while energy and food costs could remain persistently higher than expected. A faster deceleration in global growth would also pose a risk to the euro area outlook.

The risks to the inflation outlook continue to be on the upside and have intensified, particularly in the short term. The risks to the medium-term inflation outlook include a durable worsening of the production capacity of the economy, persistently high energy and food prices, inflation expectations rising above the Governing Council’s target and higher than anticipated wage rises. However, if demand were to weaken over the medium term, it would lower pressures on prices.

Financial and monetary conditions

Market interest rates have been volatile as a result of the pronounced economic and geopolitical uncertainty. Bank funding costs have risen in recent months, which has increasingly fed into higher bank lending rates, in particular for households. While the volume of bank lending to households remains strong, it is expected to decline in view of lower demand. Lending to firms has also been robust as high production costs, inventory building and lower reliance on market funding have created a continued need for credit from banks. At the same time, demand for loans to finance investment has declined. Money growth has continued to moderate owing to lower liquid savings and lower Eurosystem asset purchases.

The most recent euro area bank lending survey reports that credit standards tightened for all loan categories in the second quarter of the year, as banks are becoming more concerned about the risks faced by their customers in the current uncertain environment. Banks expect to continue tightening their credit standards in the third quarter.

Conclusion

Summing up, inflation continues to be undesirably high and is expected to remain above the Governing Council’s target for some time. The latest data indicate a slowdown in growth, clouding the outlook for the second half of 2022 and beyond. At the same time, this slowdown is being cushioned by a number of supportive factors.

At its meeting on 21 July 2022, the Governing Council decided to raise the key ECB interest rates and approved the TPI. At its upcoming meetings, further normalisation of interest rates will be appropriate. The future policy rate path will continue to be data-dependent and will help the Governing Council deliver on its 2% inflation target over the medium term.

The Governing Council stands ready to adjust all of its instruments within its mandate to ensure that inflation stabilises at its 2% target over the medium term. The new TPI will safeguard the smooth transmission of the monetary policy stance throughout the euro area as the Governing Council keeps adjusting the stance to address high inflation.

Monetary policy decisions

The Governing Council decided to raise the three key ECB interest rates by 50 basis points. Accordingly, the interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will be increased to 0.50%, 0.75% and 0.00% respectively, with effect from 27 July 2022.

At the Governing Council’s upcoming meetings, further normalisation of interest rates will be appropriate. The frontloading of the exit from negative interest rates allows the Governing Council to make a transition to a meeting-by-meeting approach to interest rate decisions. The Governing Council’s future policy rate path will continue to be data-dependent and will help to deliver on its 2% inflation target over the medium term.

The Governing Council approved the TPI. The Governing Council assessed that the establishment of the TPI was necessary to support the effective transmission of monetary policy.[1] In particular, as the Governing Council continues normalising monetary policy, the TPI will ensure that the monetary policy stance is transmitted smoothly across all euro area countries. The singleness of the Governing Council’s monetary policy is a precondition for the ECB to be able to deliver on its price stability mandate.

Subject to fulfilling established criteria, the Eurosystem will be able to make secondary market purchases of securities issued in jurisdictions experiencing a deterioration in financing conditions not warranted by country-specific fundamentals, to counter risks to the transmission mechanism to the extent necessary. The scale of TPI purchases would depend on the severity of the risks facing monetary policy transmission. Purchases are not restricted ex ante.

The Governing Council intends to continue reinvesting, in full, the principal payments from maturing securities purchased under the asset purchase programme (APP) for an extended period of time past the date when it starts raising the key ECB interest rates and, in any case, for as long as necessary to maintain ample liquidity conditions and an appropriate monetary policy stance.

As concerns the PEPP, the Governing Council intends to reinvest the principal payments from maturing securities purchased under the programme until at least the end of 2024. In any case, the future roll-off of the PEPP portfolio will be managed to avoid interference with the appropriate monetary policy stance.

Redemptions coming due in the PEPP portfolio are being reinvested flexibly, with a view to countering risks to the transmission mechanism related to the pandemic. PEPP reinvestment flexibility will continue to be the first line of defence to counter risks to the transmission mechanism related to the pandemic.

The Governing Council will continue to monitor bank funding conditions and ensure that the maturing of operations under the third series of targeted longer-term refinancing operations (TLTRO III) does not hamper the smooth transmission of its monetary policy. The Governing Council will also regularly assess how targeted lending operations are contributing to its monetary policy stance.

The Governing Council stands ready to adjust all of its instruments within its mandate to ensure that inflation stabilises at its 2% target over the medium term. The Governing Council’s new TPI will safeguard the smooth transmission of its monetary policy stance throughout the euro area.

1 External environment

Economic activity has slowed in key advanced economies since the last Governing Council meeting in June. In the United States, consumer spending in May surprised significantly to the downside, while there continues to be solid employment gains. Downside risks to the US outlook have increased overall. Activity data for the United Kingdom surprised to the downside, and consumer confidence fell to a record low. Growth in China is recovering after the country emerged from the most recent coronavirus (COVID-19) wave, but remains weak. Meanwhile, inflation in key advanced economies continues to rise, with elevated month-on-month gains, and is increasingly spreading to the service sector. Since the June Governing Council meeting oil prices have fallen by around 14% as higher risks of an economic slowdown outweigh supply disruptions. Gas prices have increased sharply in Europe, implying an aggravation of the energy shock, despite the decrease in oil prices.

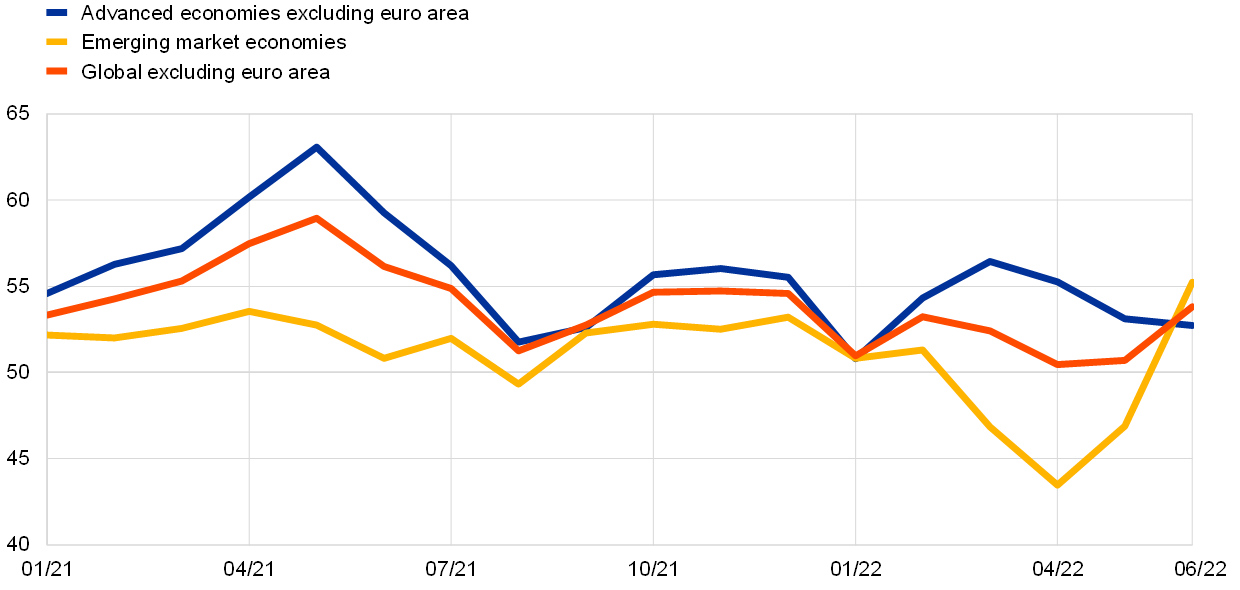

Recent data on global economic activity point to moderating growth amid high inflation and a normalisation in monetary policy around the world. The composite output Purchasing Manager’s Index (PMI) for advanced economies (excluding the euro area) declined between April and June, reflecting weaknesses in the United States and the United Kingdom in particular. By contrast, emerging market activity improved significantly in June, primarily owing to the surge in activity in China (see Chart 1). The strong improvement in China in June followed positive developments in the pandemic and the associated lifting of many containment measures in May. The global activity tracker, based on high-frequency indicators, and June PMI data both point to somewhat weakening activity, especially in advanced economies. While some of the uncertainty related to the war in Ukraine is slowly fading, inflation is weighing on real disposable incomes and aggregate demand. Although the easing of pandemic-related containment measures is set to support growth in Asia, global activity is expected to further moderate in the coming months. Central banks in both advanced and emerging economies are progressively normalising their monetary policy stance in response to surging inflation.

Chart 1

Composite output PMI

(diffusion indices)

Sources: IHS Markit, Haver Analytics and ECB calculations.

Note: The latest observations are for June 2022.

Global supply chain disruptions have eased further. In most economies PMI suppliers’ delivery times in June returned to close to levels seen prior to the war in Ukraine, after worsening in April and May. The PMI for supply shortages also improved at the global level, and global price pressures softened. Moreover, recent high-frequency activity data for the port of Shanghai indicate that supply strains in the shipping sector are easing in China. Further improvements in global production networks are expected as pandemic-related containment measures are lifted and the impact of the war in Ukraine on supply chains wanes. Looking ahead, the decline in the June PMI for input prices together with the easing of supply disruptions may signal somewhat lower inflationary pressures from the supply side. However, war-related disruptions to the supply of essential foods (such as wheat and maize) and fertilisers persist and are affecting already-vulnerable emerging market economies, particularly in Africa and the Middle East.

Global trade has contracted again owing to the Russia-Ukraine war and pandemic containment measures in China. In April, global (excluding the euro area) merchandise trade contracted for a third consecutive month and has fallen by 1.9% since January 2022. The ECB trade tracker and the June PMI for new export orders remain in contractionary territory despite some improvement. However, global merchandise trade is still expected to grow moderately in 2022 and 2023.

Global inflationary pressures are broadening to services. Annual headline CPI (consumer price index) inflation across OECD countries increased to 9.6% in May (from 9.2% in April), driven by energy and food inflation and, to a lesser extent, core inflation (Chart 2). Inflation is broadening to services in a number of key advanced economies on the back of higher input costs and the rotation of demand from goods back to services.

Chart 2

OECD consumer price inflation

(year-on-year percentage changes; percentage point contributions)

Sources: OECD, Haver Analytics and ECB calculations.

Note: The latest observations are for May 2022.

Oil prices have declined by 14% since the Governing Council meeting in June as markets started to factor in a slowdown in real economic activity. Oil prices were supported by the gradual reopening of the Chinese economy and the ongoing constraints on supply, but this was offset by weaker economic growth prospects. These factors also affected other commodity prices. Both metal and food prices are lower than before the Russian invasion of Ukraine. The recent progress made on establishing a safe corridor for Ukrainian grain shipments has led to a drop in wheat and maize prices since the last Governing Council meeting. Gas prices increased steeply (+119%) following supply shortfalls. After a period of declining gas prices in Europe amid sharp increases in gas inventories, prices recently surged again in response to the reduction in gas flows from Russia to Germany.

In the United States, economic growth momentum slowed sharply in the second quarter. Consumer spending for May was considerably lower than expected and was revised down for April. Also, the Michigan Consumer Sentiment index fell in June to the lowest level since records began in the 1950s. Moreover, the housing market shows signs of slowing, with housing starts surprising to the downside for May. By contrast, the labour market remains tight, and consumers continue to hold excess savings that could support spending going forward. Overall, downside risks to the growth outlook have risen amid increased uncertainty. On the nominal side, annual CPI headline inflation rose to 8.6% in May and 9.1% in June, above market expectations. In month-on-month terms, headline CPI increased to 1.0% in May and 1.3% in June, standing at historically elevated rates. On the risk of recession, a Wall Street Journal survey of economists from late June indicated a 44% probability of a recession in the next 12 months.

In China, the lifting of COVID-19 containment measures led to a rebound in economic activity in June, but underlying growth remains weak and downside risks elevated. With COVID-19 cases falling sharply in early June, containment measures were further eased. As a result, mobility indicators moved closer to normal levels. Monthly hard activity data partially recovered in May and are expected to further improve in June, given that the composite output PMI surged sharply to above pre-pandemic levels in June. Looking ahead additional fiscal support measures have been announced that are likely to boost infrastructure spending in the third quarter. However, GDP growth this year is expected to remain significantly below the official growth target of 5.5% for 2022, hampered in part by a persistently weak housing sector.

In Japan, annual CPI inflation remains above the target rate set by the Bank of Japan. The jump in the inflation rate in April reflected a dissipation of strong negative base effects related to mobile phone charges. Headline inflation in May remained unchanged at 2.5%, sustained by high energy and food prices, while core inflation increased only marginally. The June Tankan survey signalled that firms may be gradually passing on higher input costs to final prices. Despite increasing market pressure, the Bank of Japan maintained its yield curve control policy. The rate of divergence with other major central banks increased depreciation pressures on the yen, which reached levels not seen since the aftermath of the 1997 Asian financial crisis. Nevertheless, the Bank of Japan has not signalled a change in its monetary policy stance.

In the United Kingdom, growth momentum is further decelerating amid deteriorating business sentiment and rising inflation that is weighing on consumer demand. Monthly GDP surprised to the downside in April. Retail sales also declined and consumer confidence fell to a record low. Annual headline CPI inflation rose to 9.1% in May, while inflationary pressures have increasingly spread to the service sector. Real wages declined sharply, and short-term indicators point towards a deterioration in business sentiment. UK GDP is likely to have contracted in the second quarter.

In Russia, recent data continue to signal deteriorating economic conditions. The impact of the war on the Russian economy is beginning to broaden. In May industrial production and retail sales continued to decline, while car production almost came to a complete halt. However, GDP data for the first quarter and current account data for the second quarter may point to the collapse in 2022 being less severe than previously expected. Headline inflation declined to 16% in mid-June (from 18% in April and 17% in May), mainly driven by the appreciation of the rouble and declining consumer demand. On 10 June the Bank of Russia cut its policy rate for the fourth time to 9.5% (down from 11.0% in May). This was a return to the level set before the February emergency rate increase to 20% following Russia’s invasion of Ukraine and the ensuing sanctions.

2 Economic activity

Following a growth rate of 0.5% in the first quarter of 2022, driven by positive net trade and inventory contributions, euro area real GDP growth in the second quarter is expected to have been driven by the reopening of the economy. The reopening has bolstered a recovery in consumption of contact-intensive services and dynamic activity in the tourism sector, which are also likely to support growth in the third quarter. At the same time, persistent headwinds such as the continuing Russia-Ukraine war, high inflation, supply chain disruptions and tightening financing conditions continue to weigh on growth.[2] Elevated uncertainty, commodity price pressures – partly owing to the reduced gas supply from Russia – and tightening financing conditions are expected to dampen consumer and capital spending in the coming quarters. Moreover, a further reduction in gas supplies from Russia, with the prospect of gas rationing in the autumn and winter months, could weaken economic activity significantly and lead to further increases in energy prices. However, the impact of further energy disruptions could be mitigated by the resilient labour market, high levels of accumulated savings and additional targeted fiscal measures.

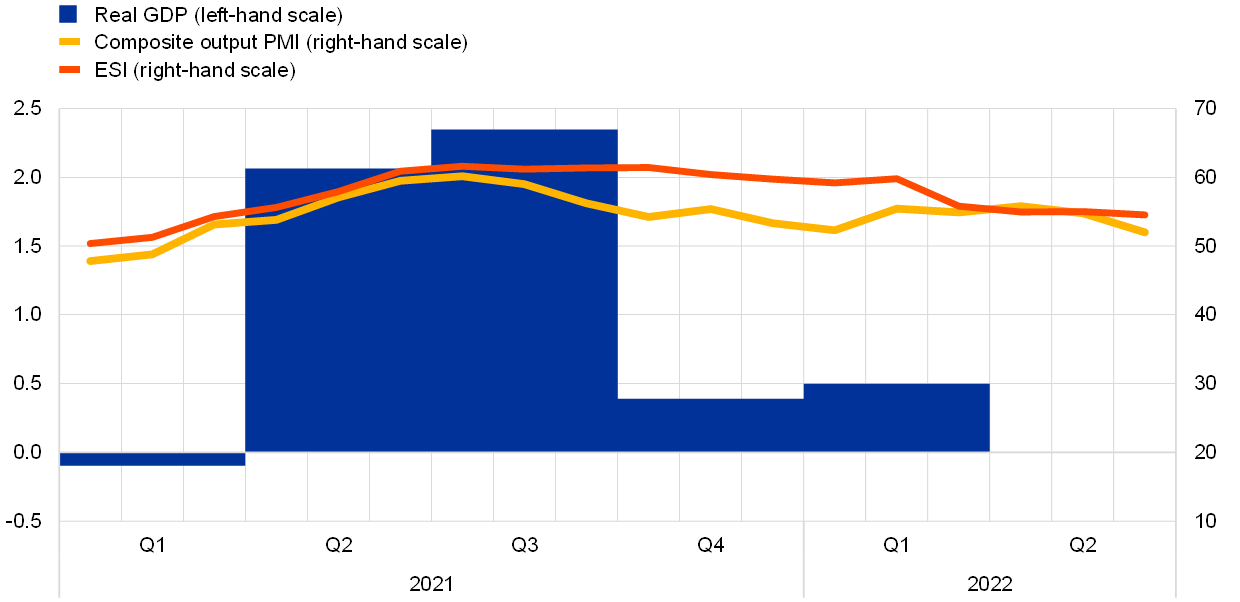

Real GDP growth in the second quarter of 2022 is expected to have been supported by the reopening of the economy and strong activity in the tourism sector, despite the war in Ukraine, high inflation, tightening financing conditions and persistent uncertainty. Euro area real GDP grew by 0.5% quarter on quarter in the first quarter of 2022, driven by positive net trade and inventory contributions, while domestic demand contracted. Excluding Ireland, euro area GDP rose by 0.3% quarter on quarter. For the second quarter of 2022, the favourable impact on euro area activity from the lifting of pandemic-related restrictions seems to have more than offset the persistent headwinds to consumption and investment spending. Incoming data support these observations. In the first two months of the second quarter, industrial production (excluding construction) was slightly below its level in the first quarter, in line with a negligible contribution to growth from the manufacturing sector. The euro area composite output Purchasing Managers’ Index (PMI) averaged 54.2 in the second quarter, only marginally below the level in the first quarter (Chart 3). In June, the manufacturing output PMI indicated a contraction for the first time since June 2020, dropping below 50 (Chart 4, panel a). This signalled a weakening in activity in the manufacturing sector, particularly owing to the acute supply chain disruptions, high commodity prices as a result of Russia’s invasion of Ukraine, and the rise in overall uncertainty. Moreover, the PMI for new manufacturing orders continued to decline in June, while the PMI suppliers’ delivery times showed that, although supply bottlenecks remained tight in June, they did ease somewhat. By contrast, activity in the services sector recovered in the second quarter of 2022 and is estimated to strengthen further in the third quarter. Services production in April was 2.4% above its level in the first quarter of the year, reflecting a rotation in demand from goods to services with the reopening of the economy. In the second quarter, the PMI for services activity averaged 55.6, improving slightly compared with the average for the first quarter, despite experiencing a moderation in June (Chart 4, panel b). The European Commission’s Economic Sentiment Indicator (ESI) declined slightly in June, signalling a slowdown in growth in the second quarter (Chart 3). While business confidence improved somewhat for industry and services, it deteriorated for the retail and construction sectors. Reflecting persisting concerns about high inflation amid elevated uncertainty and acute supply chain disruptions, consumer confidence declined further in July to a level below the one recorded at the start of the COVID-19 crisis in April 2020.[3]

Chart 3

Euro area real GDP, composite output PMI and ESI

(left-hand scale: quarter-on-quarter percentage changes; right-hand scale: diffusion index)

Sources: Eurostat, European Commission, Standard & Poor’s Global Ratings and ECB calculations.

Notes: The two lines indicate monthly developments; the bars show quarterly data. The European Commission’s Economic Sentiment Indicator (ESI) has been standardised and rescaled to have the same mean and standard deviation as the Purchasing Managers’ Index (PMI). The latest observations are for the first quarter of 2022 for real GDP and June 2022 for the PMI and the ESI.

Economic activity should benefit from the recovery in consumption in contact-intensive services, but headwinds could persist. The demand for contact-intensive services is being driven by the reopening of the economy, which is benefiting the tourism sector, but higher energy prices and elevated uncertainty are dampening consumer and business sentiment. The ECB’s contacts in the non-financial sector expect the current headwinds to be countered to some extent by the reopening of the economy, spurring activity in contact-intensive services, particularly in tourism. However, corporate contacts, especially in the retail sector, remain concerned about future developments in demand, particularly after the summer (Box 5). While risks are markedly high for the growth outlook in the autumn and winter months, especially in a scenario with further cuts in energy supplies, there are positive factors that continue to support the economy. The resilient labour market, savings accumulated during the pandemic and fiscal measures should help to cushion the impact of higher inflation on income and consumption. Progress in the implementation of the Next Generation EU (NGEU) programme is also expected to bolster the economic recovery.

Chart 4

Manufacturing and services

(left-hand scale: diffusion index; right-hand scale: index, February 2020 = 100)

Sources: Standard & Poor’s Global Ratings, Eurostat and ECB calculations.

Note: The latest observations are for May 2022 for industrial production, June 2022 for the PMIs and April 2022 for services production.

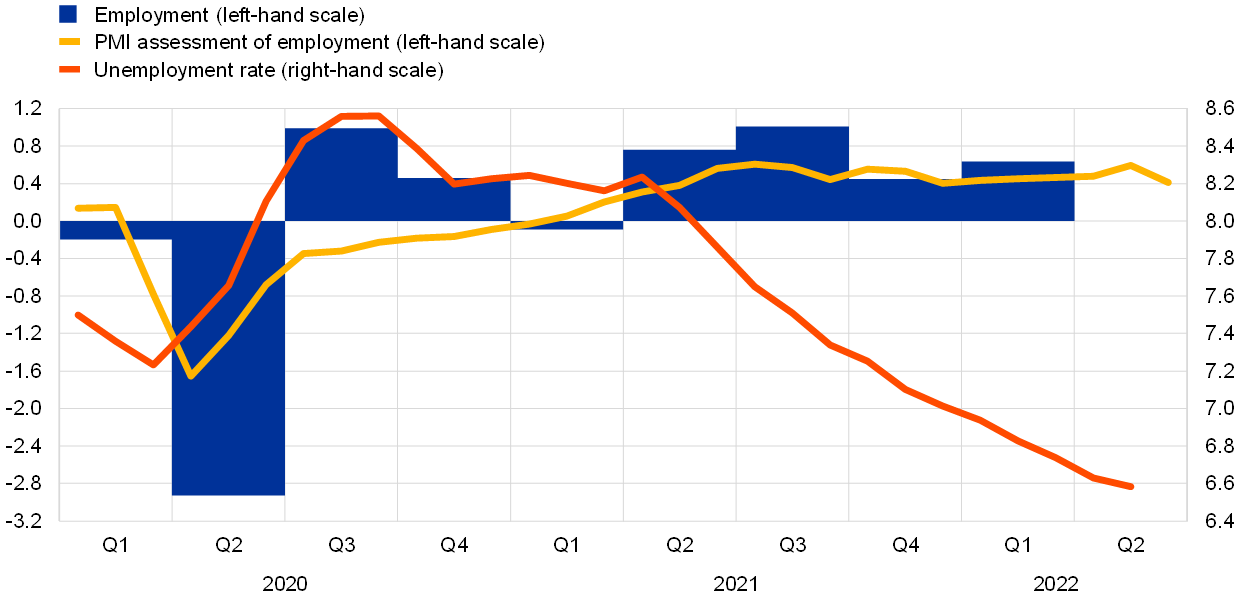

The labour market in the euro area continues to improve despite the economic impact of the war in Ukraine. The unemployment rate stood at 6.6% in May 2022, slightly lower than in April and around 0.8 percentage points lower than the pre-pandemic level observed in February 2020 (Chart 5). This is the lowest level recorded since the euro area came into existence, albeit with continuing, though progressively lower, recourse to job retention schemes. Total employment rose by 0.6%, quarter on quarter, in the first quarter of 2022, after growing by 0.4% in the fourth quarter of 2021. As a result of the economic recovery following the lifting of pandemic-related restrictions, job retention schemes covered 1.1% of the labour force in March 2022, down from around 1.6% in December 2021. This is also mirrored in the total hours worked which, while still below pre-pandemic levels, have increased towards these levels, particularly in the industrial and market services sectors.

Chart 5

Euro area employment, the PMI employment indicator and the unemployment rate

(left-hand scale: quarter-on-quarter percentage changes, diffusion index; right-hand scale: percentages of the labour force)

Sources: Eurostat, Standard & Poor’s Global Ratings and ECB calculations.

Notes: The two lines indicate monthly developments; the bars show quarterly data. The PMI is expressed as a deviation from 50 divided by 10. The latest observations are for the first quarter of 2022 for employment, June 2022 for the PMI and May 2022 for the unemployment rate.

Short-term labour market indicators continue to point to an overall resilient labour market in the euro area. The composite PMI employment indicator for the second quarter of 2022 remaind, overall, at a broadly similar level to that observed in the first quarter, thus suggesting a further growth in employment. However, the drop to 54.1 in June (1.8 points lower than in May) indicates a deceleration in momentum. The PMI employment indicator has now been in expansionary territory since February 2021. Looking at developments across different sectors, the PMI employment indicator continues to point to robust employment growth in services and manufacturing.

Household spending is shifting from goods to services. Private consumption declined by 0.4% in the first quarter of 2022, with demand for both services and goods contracting. Household consumption of goods is likely to have remained weak in the second quarter amid high inflation, elevated uncertainty and persistent bottlenecks in production and distribution networks in the goods sector. This weakness is supported by the recent developments in retail sales, which, over the period April-May 2022, stood at an average of 0.8% below their level in the first quarter. Meanwhile, new car registrations in the second quarter were 3% below their level in the first quarter. Consumer confidence continued to wane during the second quarter and declined further in July, reflecting persisting concerns about high inflation and lower economic and financial expectations, amid elevated uncertainty and acute supply constraints. Demand in the tourism sector, however, continues to recover. As restrictions are being lifted, household spending is shifting from goods back to contact-intensive services, supporting demand in the short term. The European Commission’s business and consumer survey results for June suggested that, despite the lower sentiment, expected demand for accommodation, food and travel services is likely to support growth in private consumption, at least over the summer period.[4] This is also confirmed by the latest evidence from the Consumer Expectations Survey for June, showing that households prioritised spending on holidays, whereas their intentions to buy major physical items (such as cars and household appliances) remained subdued (Chart 6). At the same time, consumption is being partly supported by the large volume of savings accumulated by households during the pandemic and by the continued strength of the labour market, which is helping to sustain labour income overall. The household saving rate marginally increased to 15% of disposable income in the first quarter of 2022, largely reflecting the impact of the COVID-19 restrictions and heightened uncertainty. Looking ahead, it is likely that increased precautionary motives due to the uncertainty caused by Russia’s invasion of Ukraine will be countered by households’ use of savings to cushion, at least partially, the negative effects of the energy shock. However, the asymmetric distribution of the saving capacity across households, rising financial concerns and the related uncertainty might limit the extent to which these savings are able to shield the ongoing recovery in consumption from the recent surge in energy prices (Box 3).

Chart 6

Household purchasing plans for the next 12 months

(percentage of respondents)

Sources: Consumer Expectations Survey and ECB calculations.

Note: The latest observation is for June 2022.

Business investment growth is expected to have been subdued in the second quarter of 2022. Non-construction investment declined by 3.6% quarter on quarter in the first three months of 2022, owing to swings in intellectual property investment in Ireland. Excluding Ireland, euro area investment rose by 1.5% quarter on quarter, driven by growth across the four largest euro area economies, and mostly due to growth in the areas of non-transport machinery and equipment. In the second quarter, industrial production of capital goods partially recovered in May (+2.5% month on month) after a significant decline in March (-3.5%) and a moderate contraction in April (-0.6%). However, it still remains below its average in the first quarter, signalling downside risks to business investment. Survey evidence from June also points to reduced momentum, as a result of persisting supply chain disruptions, elevated uncertainty, high input costs and slowing demand for capital goods. Looking ahead, downside risks are likely to persist in the second half of the year. Rising concerns due to the possibility of gas rationing as a result of the Russia-Ukraine war, paired with tightening funding conditions and weaker final demand, are also likely to reduce demand for business investment. Nevertheless, several factors may support business investment and partly cushion downside pressures: the availability of retained earnings and cash flow for firms; continued stimulus for investment through NGEU disbursements; and the investment opportunities provided by further progress in the economy’s green and digital transitions (Article 1).

Housing investment growth is likely to have moderated in the second quarter of 2022, weighed down by rising uncertainty and weakening demand. After surging in the first quarter of 2022, housing investment momentum is estimated to have moderated substantially in the second quarter. Despite substantial construction activity in the pipeline, indicated by a rising number of building permits in the first three months of the year, building construction output in April and May stood only 0.1% above its level in the first quarter, on average. Survey data also point to moderating activity amid growing headwinds to demand. The European Commission’s indicator of recent trends in construction activity picked up in June, but on average it declined in the second quarter, as a result of less supportive demand and financial conditions, together with persistent, albeit easing, shortages of materials and labour. According to the survey on the access to finance of enterprises, construction companies’ near-term turnover expectations remained strong at the start of the second quarter, but the companies increasingly reported concerns about the cost of materials, finding customers and access to finance. The European Commission’s business and consumer survey confirms a significant decline in housing demand, as households’ near-term intentions to buy or build a house recorded their largest ever single-quarter decline in the second quarter, although they remained above their long-run average. Overall, elevated uncertainty and deteriorating financing conditions may place further downward pressures on the ongoing recovery in housing investment.

Exports of goods grew moderately in April, but the near-term outlook has deteriorated significantly. In April 2022 nominal extra-euro area goods exports moderately expanded, while extra-euro area goods imports increased substantially. The goods trade balance shifted further into deficit, owing to the higher cost of energy imports and subdued export performance. Exports to Russia decreased further in April after halving in March, reflecting the impact of international sanctions. High-frequency data on trade point to some tentative easing of supply bottlenecks in the second quarter of 2022 compared with the previous quarter, although surveys suggest that firms are likely to continue to face disruptions in their cross-border value chains for the foreseeable future. Forward-looking indicators point to a slowdown in exports of both goods and services, reflecting further weaknesses in manufacturing exports and capacity constraints in the tourism sector. The June PMI indicates that export orders in the manufacturing sector fell deeper into contractionary territory, while export orders for services, following a recovery in May, also fell back into contractionary territory. After having gradually strengthened until the spring, tourism indicators showed some signs of weakening in June, although all the indicators (except for flights) remained above pre-pandemic levels.

The risks to the economic outlook continue to be tilted to the downside. While pandemic-related risks remain contained in the near term, the Russia-Ukraine war continues to represent a significant downside risk to growth. In particular, a major threat would be a further disruption in the energy supply to the euro area, which may result in gas rationing for firms and households. The war may also further dampen confidence and aggravate supply-side constraints, while energy and food costs could remain persistently higher than expected.

3 Prices and costs

Inflation increased further to 8.6% in June. Surging energy prices were again the most important component of overall inflation. Food inflation also rose further, in part reflecting the importance of Ukraine and Russia as producers of agricultural goods. Persistent supply bottlenecks for industrial goods and recovering demand, especially in the services sector, are also contributing to the current high rates of inflation. Price pressures are spreading across more and more sectors, in part owing to the indirect impact of high energy costs across the whole economy. Accordingly, most measures of underlying inflation have risen further. Continued pressures from energy and food prices and pipeline pressures in the pricing chain will likely keep inflation high for some time to come. Higher inflationary pressures are also stemming from the depreciation of the euro exchange rate. Looking further ahead, in the absence of new disruptions, energy costs should stabilise and supply bottlenecks should ease, which, together with the ongoing policy normalisation, should support the return of inflation to the ECB’s inflation target.

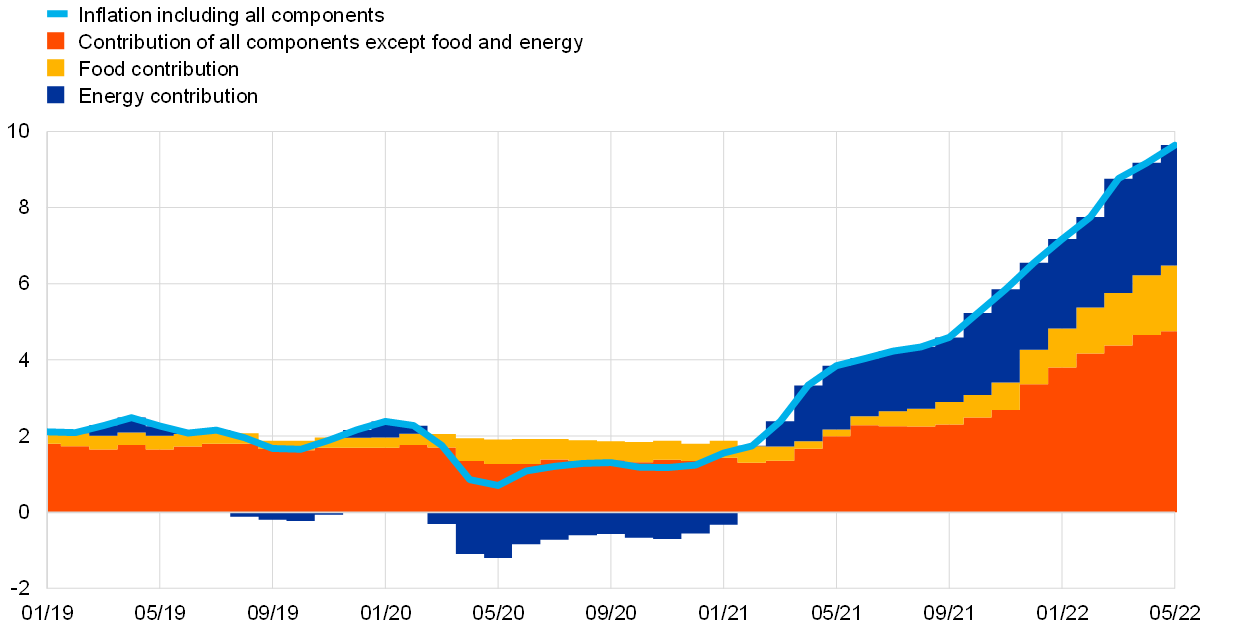

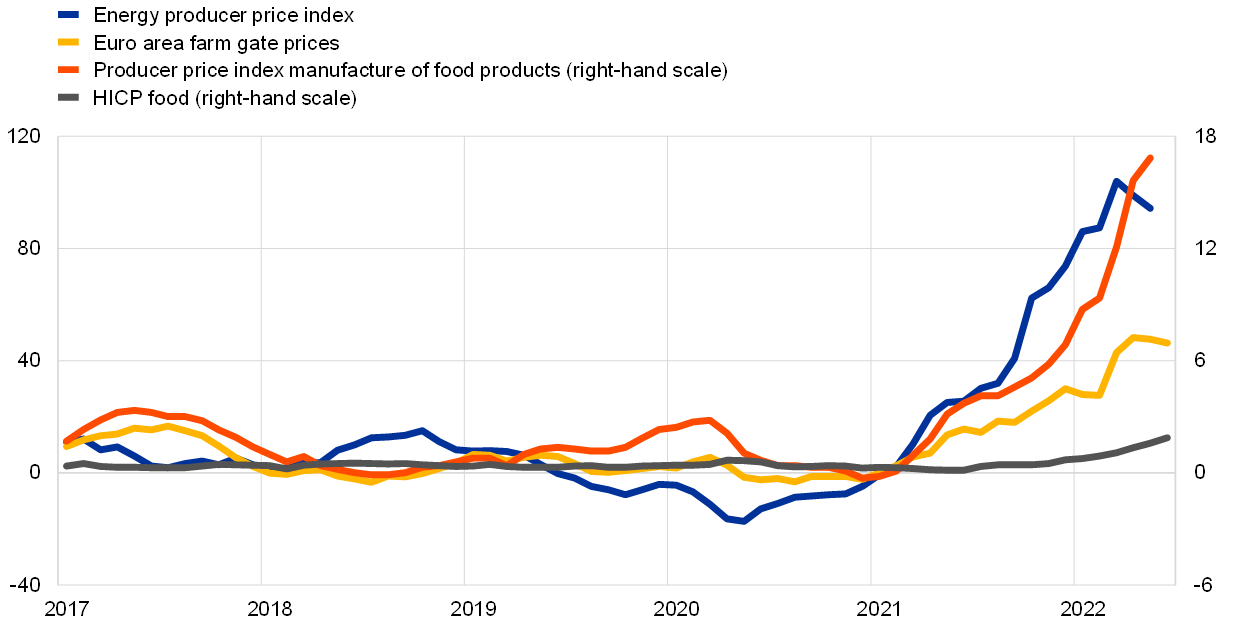

HICP inflation rose to another record high in June. The further increase from 8.1% in May to 8.6% in June was mainly driven by higher food inflation. The annual rate of change in consumer energy prices edged only marginally higher, but at more than 40% it remained exceptionally high and continued to account for around half of overall inflation. Elevated wholesale prices for gas, oil and electricity, as well as high refining and distribution margins for transport fuels (particularly diesel oil), all contributed to high energy inflation. Food inflation rose substantially for both processed and unprocessed food, pushed up by global food commodity prices and higher euro area farm gate prices. The pressures on food prices have been increasingly reflecting higher input costs related to energy and fertilisers (Chart 7).

Chart 7

Energy and food input cost pressure

(annual percentage changes)

Source: Eurostat.

Note: The latest observations are for June 2022 for euro area farm gate prices and for May 2022 for the other data.

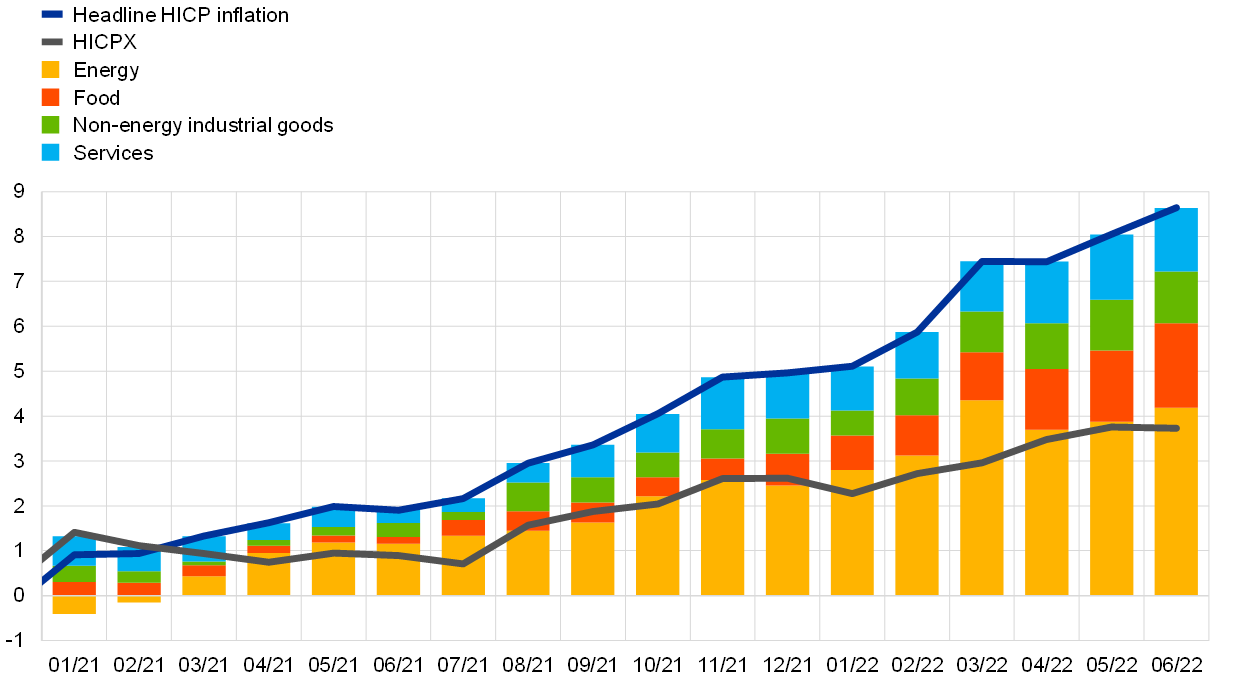

HICP inflation excluding energy and food (HICPX) decreased slightly to 3.7% in June, as the small increase in non-energy industrial goods (NEIG) inflation was more than offset by the moderation in services inflation (Chart 8). Here, too, higher input costs stemming from the surge in energy prices remained a prominent factor. NEIG inflation reached a new high, driven by both durable and non-durable goods. Sizeable month-on-month increases were recorded yet again for the prices of both these components amid global supply disruptions, which had further intensified as a result of the war in Ukraine and indirect effects from high energy costs. Services inflation was the only major component of HICP inflation to decrease, reflecting in part the temporary introduction of the €9 public transport ticket in Germany. Excluding the impact of this measure, services inflation continued its upward dynamic. The main factors driving services inflation are still higher energy costs, which affect transportation in particular; surging food prices, which are an important factor for restaurant services; and reopening effects, which have been particularly evident in items such as accommodation.

Chart 8

Headline inflation and its main components

(annual percentage changes; percentage point contributions)

Sources: Eurostat and ECB calculations.

Note: The latest observations are for June 2022.

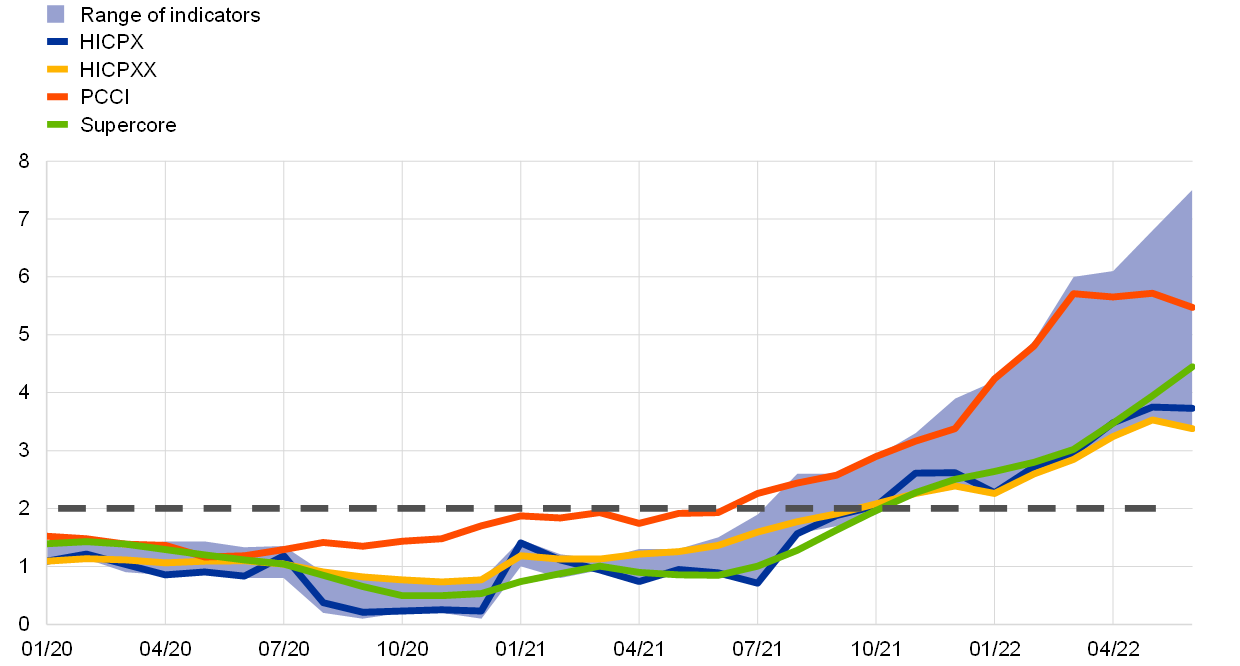

A wide range of measures of underlying inflation surpassed 3.5% in June (Chart 9). Some exclusion-based measures decreased while others continued to increase. While remaining elevated, HICPX inflation declined slightly to 3.7% in June, after 3.8% in May. HICPXX inflation (which excludes travel-related items, clothing and footwear, as well as energy and food) also saw a slight decline, to 3.4%. Meanwhile, the model-based Persistent and Common Component of Inflation (PCCI) edged down to 5.5% in June, and the Supercore indicator, which comprises cyclically sensitive HICP items, rose to 4.5%, from 3.9% in May. It is likely that the decline in some of the underlying inflation measures has been affected by the very strong impact of the €9 public transport ticket in Germany. Finally, the indicator of domestic inflation, which represents price developments of items with lower import content, has surpassed 3%.[5] At the same time, it remains uncertain how persistent the elevated levels of these indicators will be. A large part of the upward push in underlying inflation dynamics can be attributed to indirect effects from the surge in energy and food prices and from exceptional developments in the balance between supply and demand related to the pandemic and the Russian invasion of Ukraine.

The latest available data showed growth in negotiated wages stood at 2.8% in the first quarter of 2022. The increase from a 1.6% growth rate in the previous quarter was largely driven by one-off payments. Regarding measures of actual pay, growth in compensation per hour and growth in compensation per employee stood at 1.2% (after 1.3% in the previous quarter) and 4.5% (up from 3.8% in the previous quarter) respectively. The discrepancy between these two actual wage measures reflects the changes in hours worked per employee in response to developments in activity and the fading impact of job retention schemes. Looking ahead, developments in wages will be a key factor for the future dynamics of underlying inflation.

Chart 9

Indicators of underlying inflation

(annual percentage changes)

Sources: Eurostat and ECB calculations.

Notes: The range of indicators of underlying inflation includes HICP excluding energy, HICP excluding energy and unprocessed food, HICPX (HICP excluding energy and food), HICPXX (HICP excluding energy, food, travel-related items, clothing and footwear), the 10% and 30% trimmed means, and the weighted median. The latest observations are for June 2022.

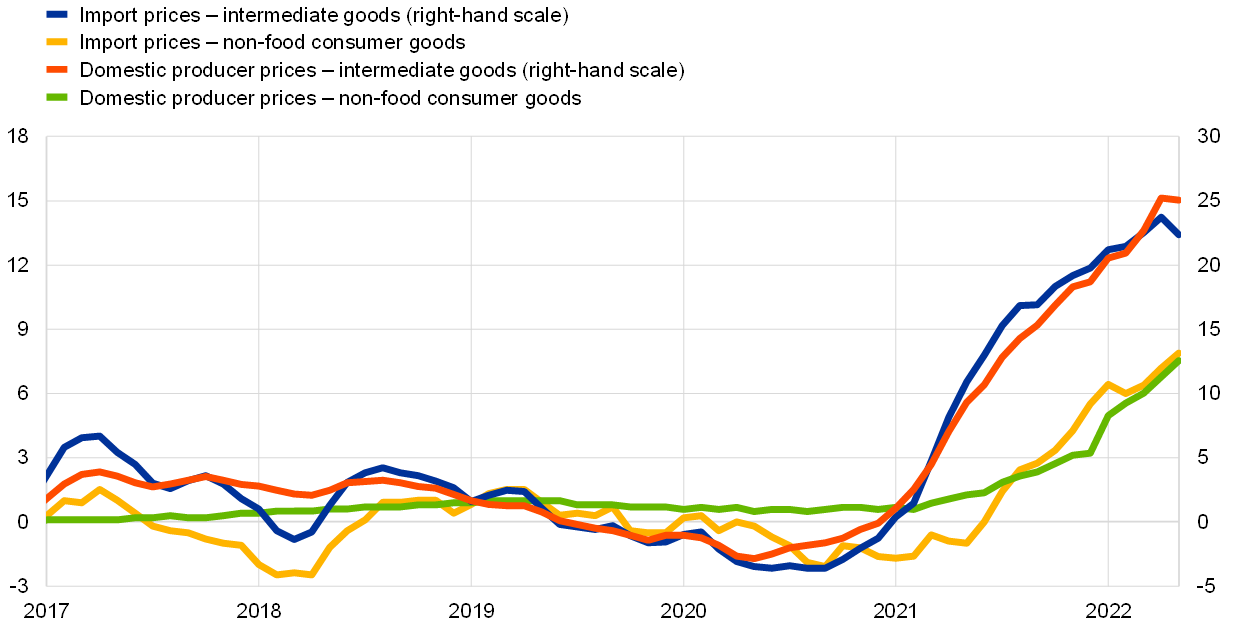

Pipeline pressures on consumer prices for NEIG have continued to build up at all stages of the pricing chain (Chart 10). Cost pressures rose further to new all-time highs on the back of supply chain disruptions, which have intensified again in the wake of the war in Ukraine, and rises in global commodity prices, particularly for energy but also for some metals. At the early stages of the pricing chain for HICP NEIG inflation, the annual growth rate of producer prices for domestic sales of intermediate goods marginally declined to 25.0% in May 2022, down from 25.2% in the previous month. The annual growth rate of import prices for intermediate goods also declined (22.4% in May compared with 23.7% in the previous month). Input cost pressures also featured more prominently at later stages of the pricing chain, with producer price inflation for domestic sales of non-food consumer goods increasing from 6.8% in April to 7.5% in May, which was again exceptionally high compared with the average annual rate of 0.6% over the 2001-19 period. Import price inflation for non-food consumer goods continued to increase as well, reaching 7.9% in May. The difference between import price inflation and domestic producer price inflation is likely attributable to the continued depreciation of the euro. Overall, the developments in import and producer prices for non-food consumer goods imply that pressure on NEIG inflation in the HICP is likely to remain elevated in the near term. This is also reflected in the data on selling-price expectations in the manufacturing sector, which remain elevated despite moderating somewhat over the past 2 months.

Chart 10

Indicators of pipeline pressures

(annual percentage changes)

Sources: Eurostat and ECB calculations.

Note: The latest observations are for May 2022.

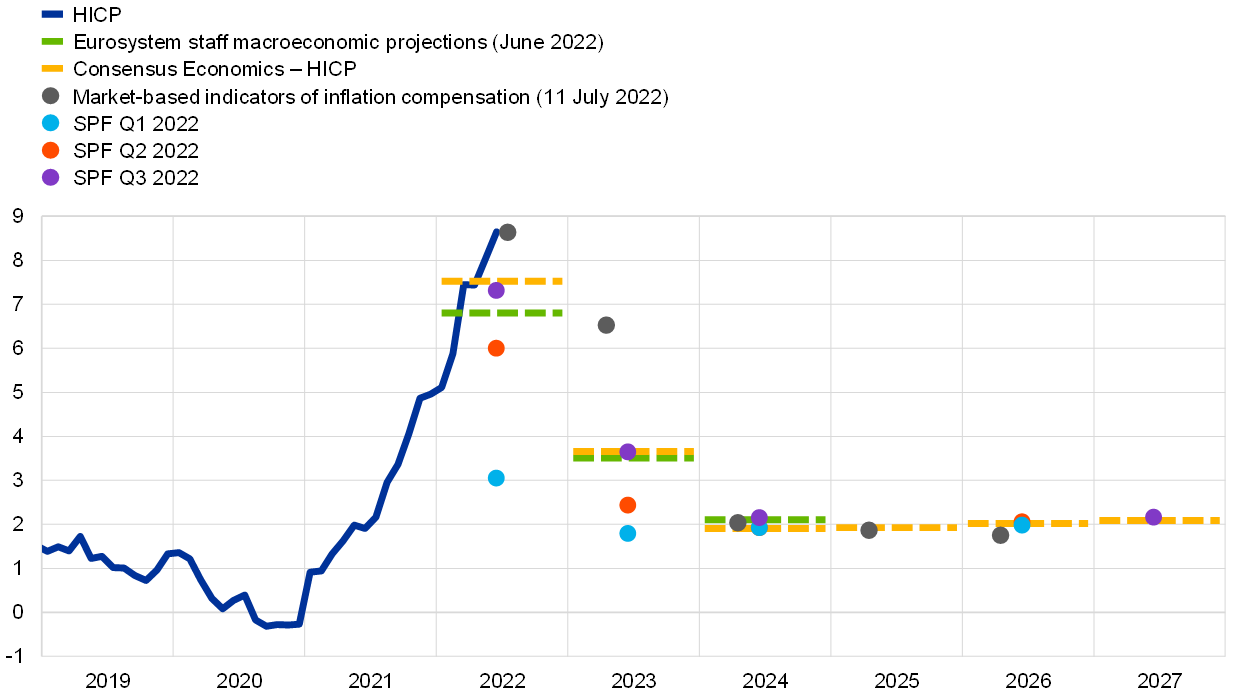

Survey-based measures of longer-term inflation expectations continued to increase gradually, reaching levels around or slightly above 2%, while market-based measures declined considerably following the June Governing Council meeting (Chart 11). According to the ECB’s Survey of Professional Forecasters (SPF) for the third quarter of 2022, longer-term inflation expectations (for 2026) rose further to 2.2%, while those of Consensus Economics stood at 2.1%, up from 1.9% in the previous quarter. At the same time, both the median and the modal expectation in the SPF survey remained at 2.0%. In the latest ECB Survey of Monetary Analysts, long-term inflation expectations remained unchanged at 2.0%. The ECB Consumer Expectations Survey also showed that the longer-term (three years ahead) inflation expectations of households increased in June, after easing slightly in the previous two months. Market-based measures of inflation compensation (based on HICP excluding tobacco) now suggest that inflation may return to levels of around 2% over the course of 2024, rather than in late 2025 as forecast before the meeting. These measures started to decline in the immediate aftermath of the June Governing Council decision and continued to do so in the weeks after the meeting, with signs of a slowdown in growth, together with tighter monetary policy, expected to ease inflationary pressures over the coming years. Longer-term measures of inflation compensation also continued to fall over the review period. The five-year forward inflation-linked swap rate five years ahead declined by 18 basis points to 2.08% on 20 July. Importantly, market-based measures of inflation compensation are not a direct measure of market participants’ actual inflation expectations, since they contain inflation risk premia to compensate for inflation uncertainty. Currently, while much of the repricing in these measures is assessed to reflect lower inflation risk premia, their elevated volatility suggests that the uncertainty around market participants’ inflation outlook remains high.

Chart 11

Survey-based indicators of inflation expectations and market-based indicators of inflation compensation

(annual percentage changes)

Sources: Eurostat, Refinitiv, Consensus Economics, Survey of Professional Forecasters, Eurosystem staff macroeconomic projections for the euro area and ECB calculations.

Notes: The market-based indicators of inflation compensation series is based on the one-year spot inflation rate, the one-year forward rate one year ahead, the one-year forward rate two years ahead, the one-year forward rate three years ahead and the one-year forward rate four years ahead. The latest observations for market-based indicators of inflation compensation are for 11 July 2022. The Survey of Professional Forecasters for the third quarter of 2022 was conducted between 1 and 5 July 2022. The cut-off date for the Consensus Economics forecasts was July 2022. The cut-off date for data included in the Eurosystem staff macroeconomic projections was 24 May 2022.

The risks to the inflation outlook continue to be on the upside and have intensified, particularly in the short term. The risks to the medium-term inflation outlook include a lasting reduction in the production capacity of our economy, persistently high energy and food prices, inflation expectations rising above our target and higher than anticipated wage rises. However, if demand were to weaken over the medium term, it would lower pressures on prices.

4 Financial market developments

Over the review period (9 June to 20 July 2022) financial market developments were dominated by the impact of the ongoing monetary policy tightening in advanced economies and by growing concerns about an imminent global slowdown. The euro short-term rate (€STR) forward curve exhibited high volatility. Long-term sovereign bond yields declined amid lower risk-free rates; sovereign spreads also narrowed, albeit displaying some volatility over the review period. Euro area equity markets recorded sizeable losses, while corporate bond spreads widened, reflecting expectations of tighter monetary policy and increasing likelihood of an economic slowdown. The euro continued to depreciate in trade-weighted terms.

The euro area short-term risk-free rates showed high volatility during the review period, amid elevated uncertainty about the inflation outlook. Over the review period the €STR averaged -58 basis points, while excess liquidity decreased by approximately €180 billion to stand at €4,437 billion, reflecting repayments associated with previous operations in the third series of targeted longer-term refinancing operations (TLTRO III) amounting to €74 billion. At the same time, the overnight index swap (OIS) forward curve based on the benchmark €STR shifted upwards at the beginning of the review period, especially in response to higher than expected US Consumer Price Index in May and the impact of the ongoing monetary policy tightening in several global economies. The initial increase was reversed as market participants’ concerns about an imminent global slowdown took centre stage. Towards the end of the review period the OIS moved upwards again, following a renewed higher than expected increase in the US Consumer Price Index in June. Overall, at the end of the review period the OIS forward curve tentatively priced in cumulative hikes amounting to around 150 basis points by the end of 2022 (up from 138 basis points priced in on 9 June).

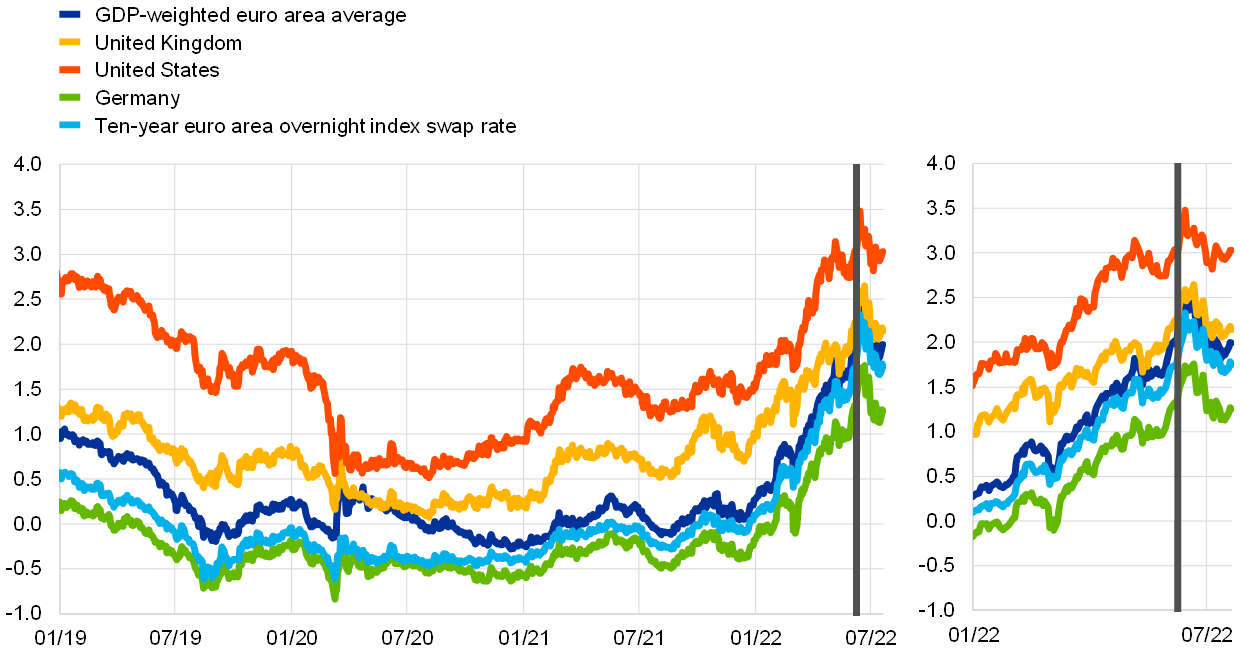

Long-term euro area sovereign bond yields declined amid lower long-term risk-free rates and narrowing sovereign spreads (Chart 12). During the period under review the average GDP-weighted euro area and German ten-year sovereign bond yields decreased by 17 basis points and 18 basis points, to stand at 1.99% and 1.26% respectively. Ten-year US and UK government bond yields also decreased to stand at 3.03% and 2.14% respectively. Euro area long-term risk-free rates declined by around 11 basis points and sovereign spreads over risk-free rates also narrowed, albeit displaying some volatility over the review period. Notably, sovereign spreads fell tangibly following the Governing Council’s announcement on 15 June to apply flexibility in reinvesting redemptions coming due in the PEPP portfolio, with a view to preserving the functioning of the transmission mechanism, and to accelerate the completion of the design of a new anti-fragmentation instrument. Over the last days of the review period euro area sovereign spreads reverted back to higher levels, amid the escalation of the political crisis in Italy. At the country level, the largest decline in spreads was observed for Greece, with the ten-year sovereign spread decreasing by 55 basis points over the review period. Declines in the ten-year sovereign spreads for Spain and France were less pronounced, amounting to 1.5 basis points and 4.5 basis points respectively. While the ten-year sovereign spread for Italy also declined overall by 8 basis points, its volatility increased towards the end of the review period reflecting the political crisis in Italy.

Chart 12

Ten-year sovereign bond yields and the ten-year OIS rate based on the €STR

(percentages per annum)

Sources: Refinitiv and ECB calculations.

Notes: The vertical grey line denotes the start of the review period on 9 June 2022. The latest observations are for 20 July 2022.

Euro area corporate bond spreads widened as downside risks to corporate bond valuations increased. Spreads on euro area investment-grade non-financial corporate bonds increased by 17 basis points to stand at 87 basis points, while spreads on financial corporate bonds increased slightly further, rising by 20 basis points to stand at 113 basis points. Corporate bond markets valuations decreased as well, reflecting investors’ pessimism about the economic outlook. In line with this, model estimates of corporate bond spreads suggest that the increases in corporate bond spreads since the Governing Council’s meeting in June likely reflect increases in default risk and a further deterioration in investors’ risk sentiment.

Euro area equity markets recorded further losses as tightening monetary policy and the deteriorating outlook for global growth weighed on equity prices. Equity prices of euro area banks and non-financial corporations decreased by 12.67% and 2.84% respectively, mainly reflecting a deterioration in risk sentiment and further downgrade in long-term earnings expectations. The larger decrease in bank equity prices likely reflect the fact that many large European corporations are global in nature, while banks are much more sensitive to domestic business cycles. These factors point to a higher likelihood of global economic slowdown perceived by market participants on the back of worse than expected outcomes in the latest economic data releases. Furthermore, this perception is exacerbated in the euro area by concerns about Russian threats of further cuts to gas supplies. In the United States, the decline in equity prices for bank and non-financial corporations was more contained, standing at 3.16% and 1.18% respectively

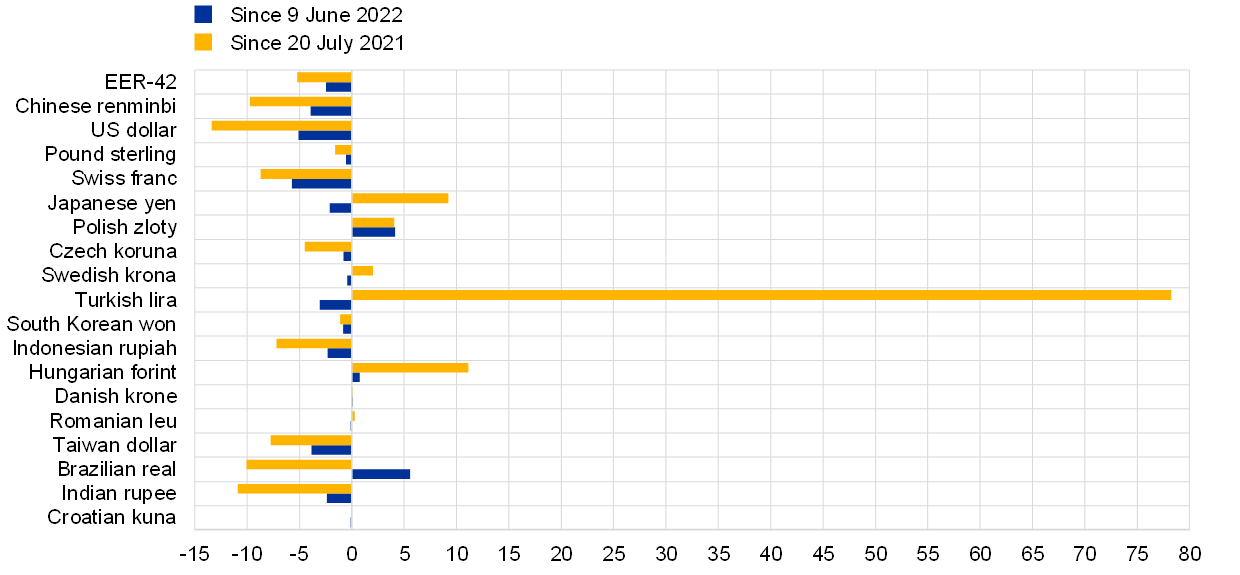

In foreign exchange markets, the euro continued to depreciate in trade-weighted terms, reflecting a weakening against most major currencies (Chart 13). Over the review period the nominal effective exchange rate of the euro, as measured against the currencies of 42 of the euro area’s most important trading partners, weakened by 2.4%. This reflected a depreciation of the euro against the US dollar (by 5.1%) – amid expectations of a faster pace of monetary tightening by the US Federal Reserve System – as well as against the currencies of other major economies, including the Swiss franc (by 5.7%), the Japanese yen (2.1%) and to a lower extent the pound sterling (by 0.6%). The euro also weakened against the currencies of most emerging market economies, including the Chinese renminbi (by 3.9%), but appreciated vis-à-vis the Polish zloty (by 4.1%) and the Hungarian forint (0.8%).

Chart 13

Changes in the exchange rate of the euro vis-à-vis selected currencies

(percentage changes)

Source: ECB.

Notes: EER-42 is the nominal effective exchange rate of the euro against the currencies of 42 of the euro area’s most important trading partners. A positive (negative) change corresponds to an appreciation (depreciation) of the euro. All changes have been calculated using the foreign exchange rates prevailing on 20 July 2022.

5 Financing conditions and credit developments

Bank funding and lending conditions continued to tighten in May, and bank lending rates for firms and households increased further, reflecting the rising trend of market rates. The growth of loans to firms and households nonetheless remained robust. Over the period from 9 June to 20 July the cost of both market-based debt financing and equity for firms increased substantially. The most recent bank lending survey indicates that credit standards on loans to firms and to households for house purchase tightened considerably in the second quarter of 2022, as banks are becoming more concerned about the risks faced by their customers in the current uncertain environment. Money creation normalised further in May amid high energy prices, which compressed disposable income, and lower Eurosystem asset purchases.

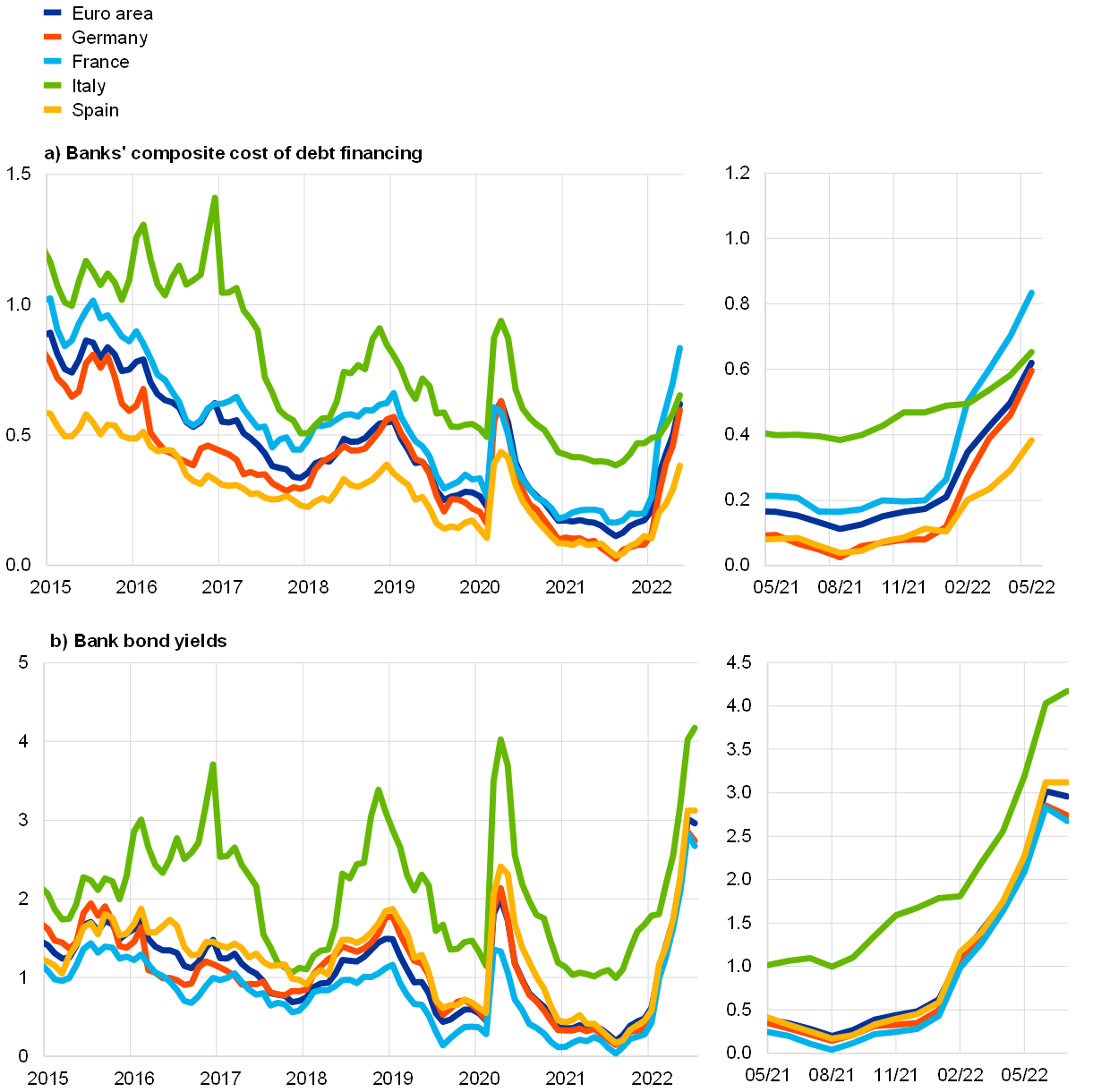

The funding costs of euro area banks continued to increase in May, as market rates rose further. The composite cost of euro area banks’ debt financing in May continued the upward trend that had started in August 2021, and subsequently increased by about 50 basis points (Chart 14, panel a). This was mainly attributable to rising yields on bank bonds (Chart 14, panel b), as rates on deposits, which account for a large share of euro area banks’ funding, have so far remained close to their historical lows. Banks are still able to apply negative rates to a significant share of firms’ and households’ deposits. More recently, bond yields have stabilised as worsening perceptions of the economic outlook have put downward pressure on risk-free rates.

Chart 14

Composite bank funding rates in selected euro area countries

(annual percentages)

Sources: ECB, IHS Markit iBoxx indices and ECB calculations.

Notes: Composite bank funding rates are a weighted average of the composite cost of deposits and unsecured market-based debt financing. The composite cost of deposits is calculated as an average of new business rates on overnight deposits, deposits with an agreed maturity and deposits redeemable at notice, weighted by their respective outstanding amounts. Bank bond yields are monthly averages for senior-tranche bonds. The latest observations are for May 2022 for composite bank funding rates and 20 July 2022 for bank bond yields.

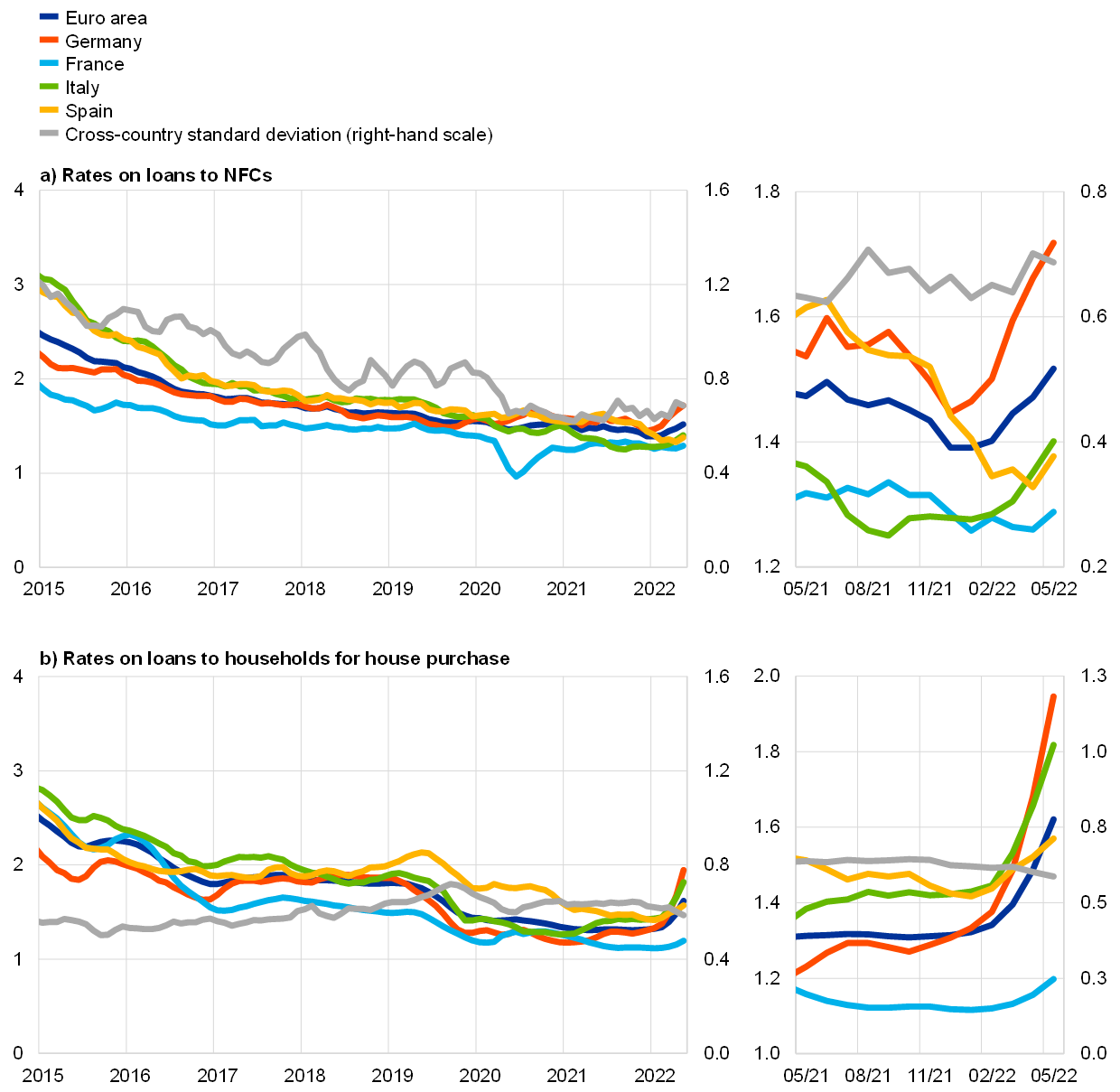

Bank lending rates for firms and households increased further in May, as mortgage rates recorded the largest monthly change in two decades. The sharp increase since the beginning of 2022 in risk-free rates and in euro area government bond yields has pushed up lending rates (Chart 15). In May the composite bank lending rate for loans to households for house purchase continued to accelerate, standing at 1.78% after a monthly increase of 17 basis points and an increase of 14 basis points in April. Bank lending rates for loans to non-financial corporations (NFCs) increased more moderately, by 4 basis points, to 1.55%. The spread between bank lending rates on very small loans and on large loans remained broadly unchanged at pre-pandemic levels, suggesting that bank-based financing conditions for small and medium-sized enterprises have not worsened in relative terms. Moreover, the cross-country dispersion of lending rates to firms and households remained contained (Chart 15, panels a and b). For the coming months, available evidence points to further lending rate increases. This is suggested, for example, by the marked increase recorded by diffusion indices. These indices, which are computed from micro data, measure the net number of banks that are raising lending rates for firms and tend to have leading indicator properties. In addition, banks have continued to tighten their credit standards on loans to firms and households, as indicated by the euro area bank lending survey, which signals a contraction in credit supply in the coming months that may imply higher lending rates.

Chart 15

Composite bank lending rates for NFCs and households in selected countries

(annual percentages, three-month moving averages; standard deviation)

Source: ECB.

Notes: Composite bank lending rates are calculated by aggregating short and long-term rates using a 24-month moving average of new business volumes. The cross-country standard deviation is calculated using a fixed sample of 12 euro area countries. The latest observations are for May 2022.

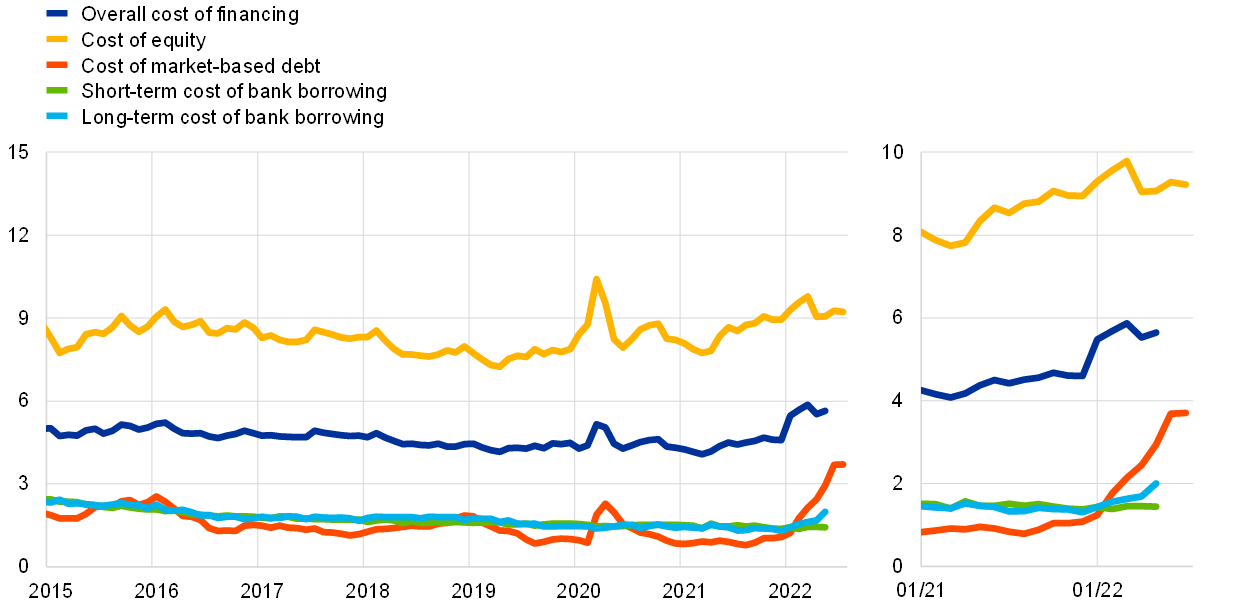

Over the period from 9 June to 20 July 2022 the cost of both market-based debt issuance and equity financing for NFCs increased substantially. Due to lags in the data available for the cost of bank borrowing, the overall cost of financing for NFCs, comprising the cost of bank borrowing, the cost of market-based debt and the cost of equity, can be calculated only up to May 2022, when it increased to 5.7% from 5.5% in April. This was the result of an increase in both the cost of market-based debt and the cost of long-term bank borrowing (Chart 16). The May 2022 data were close to the peak recorded earlier in the year and significantly above the levels seen in the previous two years. In the period since 9 June, both the cost of market-based debt and the cost of equity have continued to increase, by around 50 and 30 basis points respectively. The slight decline in the risk-free rate during this period was more than compensated by a significant increase in corporate bond spreads, especially in the high-yield segment. In the same vein, the increase in the cost of equity is accounted for by an increase in the equity risk premium as the deterioration in the euro area and global economic outlook percolated into market risk perceptions.

Chart 16

Nominal cost of external financing for euro area NFCs, broken down by components

Sources: ECB and ECB estimates, Eurostat, Dealogic, Merrill Lynch, Bloomberg and Thomson Reuters.

Notes: The overall cost of financing for NFCs is calculated as a weighted average of the cost of borrowing from banks, market-based debt and equity, based on their respective outstanding amounts. The latest observations are for 20 July 2022 for the cost of market-based debt (monthly average of daily data), 15 July 2022 for the cost of equity (weekly data) and May 2022 for the cost of borrowing from banks (monthly data).

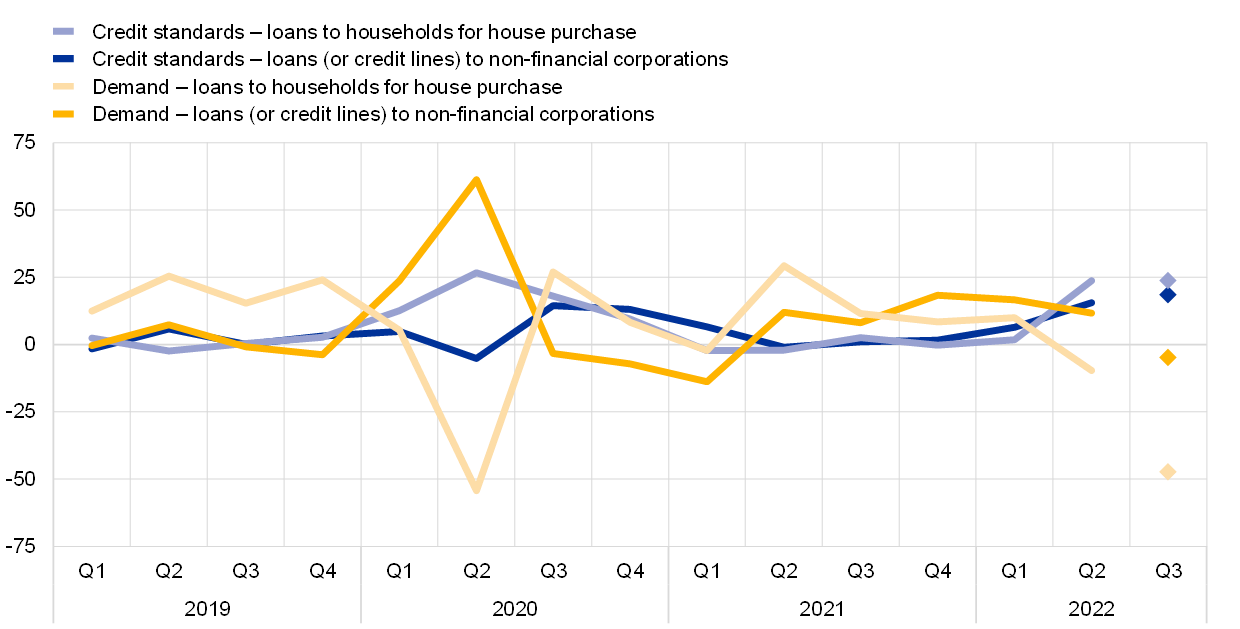

According to the July 2022 euro area bank lending survey, credit standards for loans to firms and for loans to households for house purchase became substantially tighter in the second quarter of 2022 (Chart 17). Against the background of the highly uncertain economic outlook, continuing supply chain disruptions and high energy prices, the main factors underlying the tightening of credit standards were perceptions of increased risk and reduced risk tolerance. With monetary policy becoming less accommodative, euro area banks also reported that their cost of funds and balance sheet constraints had contributed to the tightening of credit standards. The tightening of credit standards for housing loans was considerably stronger than in the previous quarter and above the historical average. For the third quarter of 2022, banks expect a continued tightening of credit standards on loans to firms and loans to households for house purchase.

Chart 17

Changes in credit standards and net demand for loans to NFCs and loans to households for house purchase

(net percentages of banks reporting a tightening of credit standards or an increase in loan demand)

Source: Euro area bank lending survey.

Notes: For survey questions on credit standards, “net percentages” are defined as the difference between the sum of the percentages of banks responding “tightened considerably” and “tightened somewhat” and the sum of the percentages of banks responding “eased somewhat” and “eased considerably”. For survey questions on demand for loans, “net percentages” are defined as the difference between the sum of the percentages of banks responding “increased considerably” and “increased somewhat” and the sum of the percentages of banks responding “decreased somewhat” and “decreased considerably”. The diamonds denote expectations reported by banks in the most recent round of the survey for the following quarter. The latest observations are for the second quarter of 2022.

The demand for housing loans decreased in the second quarter of 2022, while loan demand from firms continued to increase but is expected to fall in the third quarter. Banks reported that firms’ loan demand was supported by the need for working capital financing, against the background of supply chain bottlenecks and rising input costs. By contrast, demand for loans to finance fixed investment made a significant negative contribution to firms’ overall demand for loans, indicating that firms may be postponing their investment in the current uncertain environment. In addition, the reported positive contribution of the general level of interest rates to loan demand was more moderate than in the previous quarter. The decrease in demand for housing loans was reported to stem from lower consumer confidence and the increase in the general level of interest rates. For the third quarter of 2022, banks expect a decrease in firms’ demand for loans and a more pronounced decrease in the demand for housing loans than in the second quarter.

The survey also suggests that banks’ access to wholesale funding has deteriorated. Euro area banks reported that their access to money markets, securitisation and particularly funding via the issuance of debt securities deteriorated in the second quarter of 2022. This reflects the tightening of financial market conditions for banks in the context of the ongoing monetary policy normalisation. By contrast, access to retail funding improved slightly in the second quarter. For the third quarter, banks expect a slight deterioration in access to retail funding and a continued deterioration in access to market-based funding, in particular debt securities funding.

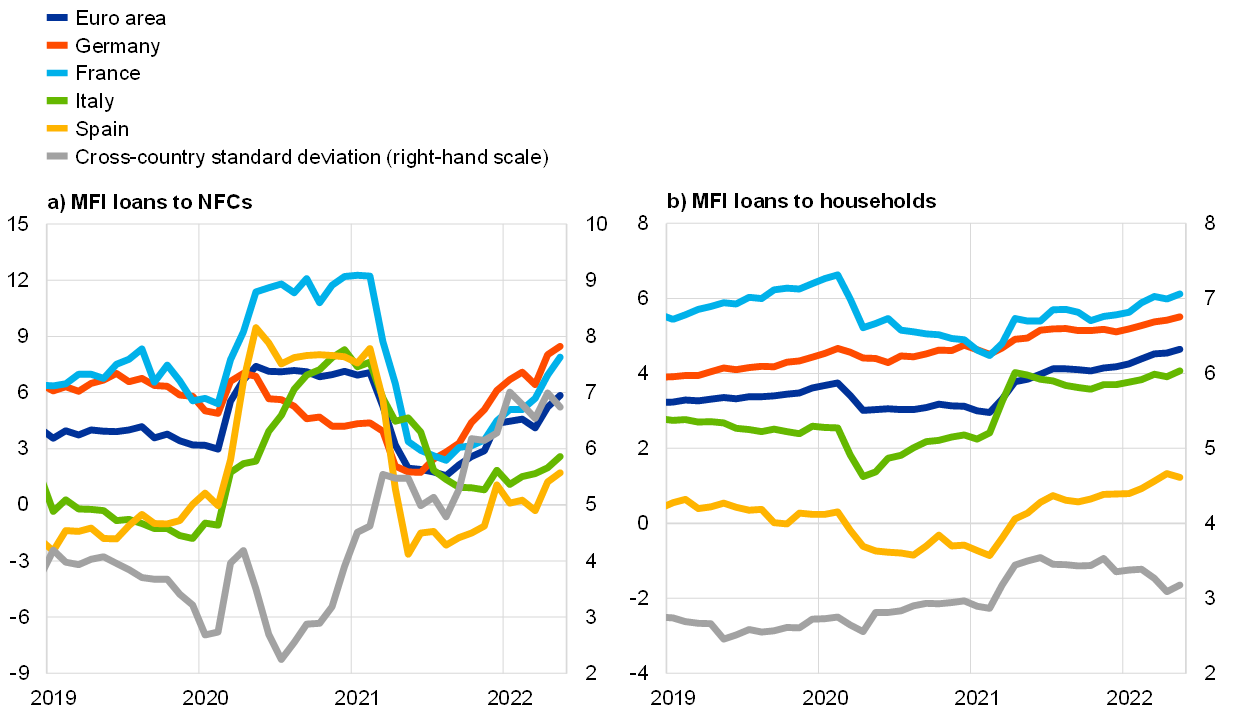

The growth of loans to firms and households has remained robust. The annual growth rate of loans to NFCs accelerated to 5.8% in May, from 5.2% in April and 4.1% in March (Chart 18, panel a). This once again reflected a large base effect, following a month-on-month reduction in loan volumes in both April and May 2021. Shorter-term loans made a large contribution, given the persistence of supply chain bottlenecks and higher input costs, both of which raise firms’ working capital needs. The resilience of loan growth also reflects to some extent a move away from the issuance of debt securities, with market-based funding conditions having tightened more sharply than bank-based funding conditions. The annual growth rate of loans to households remained broadly unchanged at 4.6% in May (Chart 18, panel b), supported by robust lending for house purchase and a recovery in consumer loans as spending opportunities improved with the reopening of the economy. As indicated by the ECB’s Consumer Expectations Survey, this could be also related to households’ expectations of tighter access to credit and higher nominal borrowing costs next year.

Chart 18

MFI loans in selected euro area countries

(annual percentage changes; standard deviation)

Source: ECB.

Notes: Loans from monetary financial institutions (MFIs) are adjusted for loan sales and securitisation; in the case of NFCs, loans are also adjusted for notional cash pooling. The cross-country standard deviation is calculated using a fixed sample of 12 euro area countries. The latest observations are for May 2022.

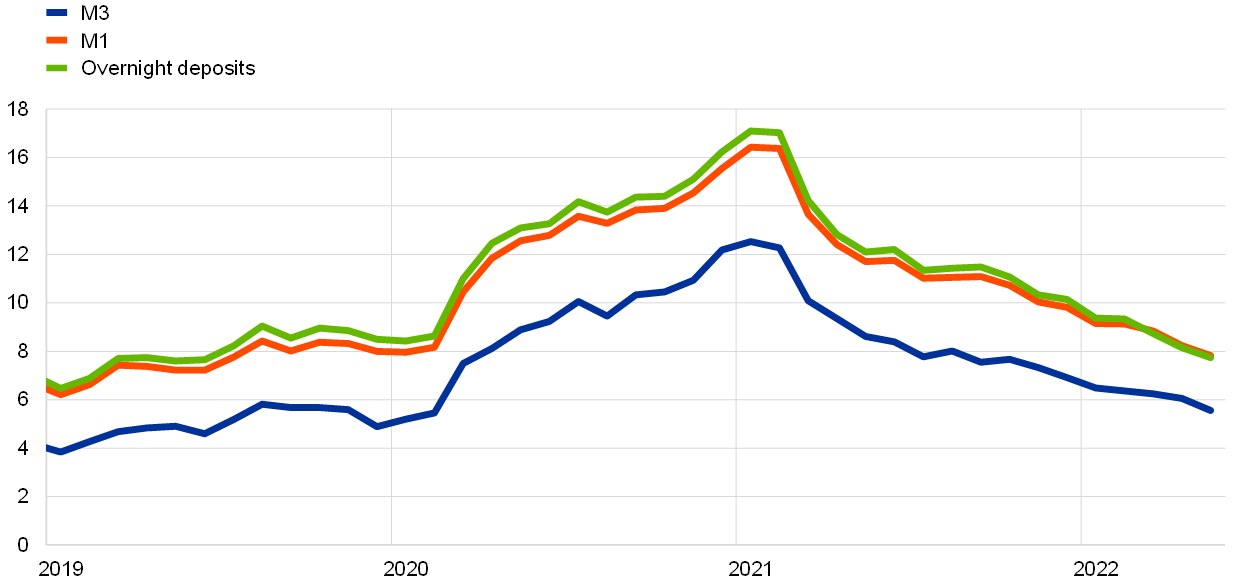

The pace of deposit accumulation continued to moderate in May from the high levels seen during the pandemic (Chart 19). The annual growth rate of overnight deposits decreased to 7.7% in May, from 8.1% in April. The slowdown was observed for the overnight deposits of both firms and households, as higher costs for food and energy have reduced firms’ cash buffers and limited the capacity of households to increase savings.[6] At the same time, high uncertainty related to the war in Ukraine and the deteriorating economic outlook continued to support firms and households’ preference for liquidity. Against this background, inflows into deposits remained sizeable in May, owing to an increase for households. Growth in the deposit holdings of firms and households has varied across countries, reflecting differences in their liquidity needs and national fiscal support measures.

Chart 19

M3, M1 and overnight deposits

(annual growth rate, adjusted for seasonal and calendar effects)

Source: ECB.

Note: The latest observations are for May 2022.

Broad money (M3) growth returned to its long-term average in May. The annual growth rate of M3 continued its downward trend in May, declining to 5.6% from 6.1% in April (Chart 19). This annual rate is in line with the average since 1999, and shorter-term dynamics point to a stronger moderation. On the components side, the main driver of M3 growth continued to be the narrow aggregate M1, largely reflecting developments in overnight deposits. On the counterparts side, credit to the private sector continued to support annual M3 growth, while the positive contribution from the Eurosystem’s purchases of government securities under the asset purchase programme and the pandemic emergency purchase programme decreased further, as these purchases are gradually being phased out. At the same time, the increase in net monetary outflows to the rest of the world dampened money growth, reflecting two main developments. First, the higher energy prices exerted a negative impact on deposit dynamics and the euro area trade balance. Second, the current uncertainty and yield differentials with several countries outside the euro area has made investing in euro area assets less attractive to global investors.

Boxes

1 Trade flows with Russia since the start of its invasion of Ukraine

War-related disruptions to the production and trade of energy and agri-food commodities have raised concerns about global energy and food supply security. Russia is a top exporter of energy commodities and, like Ukraine, also a key global exporter of agricultural commodities. This box first takes stock of recent developments in the trade flows from war-affected areas since the onset of the conflict. Flows of energy and agri-food commodities are tracked using marine freight data and gas flow data, which provide a timelier assessment of recent developments than customs trade data. [7] The box then examines the evolution of Russia’s imports since the start of the war. However, as Russia stopped releasing official customs trade data as of end-February 2022, the box looks at customs data on the exports of a selection of Russia’s trading partners in order to approximate Russia’s imports. Finally, these data are used to provide a preliminary empirical assessment of the effects of sanctions on Russia´s trade flows.

2 Wage share dynamics and second-round effects on inflation after energy price surges in the 1970s and today

This box reviews wage share dynamics and potential second-round effects on inflation at times of energy price increases. In a net energy-importing region, such as the euro area, increasing energy inflation induces a deterioration in the terms of trade (the ratio of export prices to import prices), thereby eroding the income used to remunerate domestic factors of production. The wage share (the share of domestic income allocated to labour) can provide an indication of the ability of workers to resist such real income losses and the potential for second-round effects on prices.[8] This box explores wage share and inflation dynamics in the euro area after the energy price increase observed since the second quarter of 2021. First, the current episode is compared to another well-known episode featuring a large energy price shock, namely the oil embargo imposed by the Organization of the Petroleum Exporting Countries (OPEC) in October 1973. Second, the developments in the euro area are compared with those in the United States. Finally, a model-based analysis evaluates how the transmission of energy price increases to inflation, and in particular the emergence of second-round effects, has changed compared to the 1970s.

3 Household saving during the COVID-19 pandemic and implications for the recovery of consumption

The ECB Consumer Expectations Survey (CES) asked households in 2020 and 2021 about their saving behaviour and the underlying motives. Some special-purpose questions were fielded asking households whether in 2020 they saved or dissaved, by how much and why they did so. The answers to these questions provide information about the drivers of the increase in savings recorded in euro area aggregate data.[9]

4 How higher oil prices could affect euro area potential output

The recent increase in energy prices constitutes a significant supply shock, which could therefore also have an impact on the potential output of the euro area economy. Based on the assumptions used in the June 2022 Eurosystem staff macroeconomic projections, oil prices in US dollars in the period 2022 to 2024 are expected to be around 40% higher than their levels in the pre-COVID period (2017-19).[10] Expressed as a percentage, the increase in oil prices since 2019 is smaller than the 1973 and 1979 shocks (Chart A).[11] In addition, the increase observed between 2003 and 2008 turned out to be of a greater magnitude than the current increase. The nature of the current oil price increase – largely a supply shock linked to supply bottlenecks and to the war in Ukraine – is more comparable to the 1970s shocks than to those of the 2000s, when demand for oil played a major role in the rise in fossil fuel prices.[12] Since the current increase in energy prices, and oil prices in particular, reflects supply-side factors, it could also affect potential output and the output gap, with implications for inflationary pressures. This box describes the channels of impact and uses elasticities estimated on historical data to shed light on the risks to potential output stemming from the current increase in energy prices.

5 Main findings from the ECB’s recent contacts with non-financial companies

This box summarises the results of contacts between ECB staff and representatives of 71 leading non-financial companies operating in the euro area. The exchanges mainly took place between 20 and 29 June 2022.[13]

6 Selling price expectations among euro area enterprises

This box analyses recent information from euro area firms regarding their selling price expectations. Firms are important economic agents when it comes to determining inflation dynamics, since they take many decisions that influence macroeconomic outcomes, from negotiating wages and setting prices to determining how much to invest and how many people to employ. However, information about firms’ pricing practices remains relatively scarce compared with information on other economic agents in both the euro area and many other countries. To help understand pricing practices among euro area corporations, the most recent Survey on the Access to Finance of Enterprises in the euro area (SAFE) introduced additional questions on recent (over the past 12 months) and expected (over the next 12 months) price changes at firm level.[14] It also included questions on the importance of different determinants of such price expectations over the next 12 months. This box reports on the responses and analyses which characteristics of firms are relevant for better understanding those expectations.

7 Euro area fiscal policy response to the war in Ukraine and its macroeconomic impact

This box provides a quantitative assessment of the fiscal policy measures adopted by euro area governments in response to the war in Ukraine and their macroeconomic impact. The discretionary fiscal measures adopted by euro area governments since Russia’s invasion of Ukraine on 24 February 2022 have three main objectives: cushioning the impact of energy price increases, increasing defence capabilities in euro area countries and Ukraine, and addressing the refugee crisis. Some governments have also extended liquidity support in the form of guarantees, although this would, in principle, affect their budget balances only if the guarantees (contingent liabilities) are called on.[15] Moreover, several support initiatives have been adopted at the EU level, including direct help for the Ukrainian government. Against this background, this box focuses on fiscal stimulus measures that have a direct impact on the budget balance of euro area countries. It also provides estimates for the impact of such measures on euro area growth and inflation over the period 2022-24.

Articles

1 The recovery in business investment – drivers, opportunities, challenges and risks