The impact of the ECB’s monetary policy measures taken in response to the COVID-19 crisis

Published as part of the ECB Economic Bulletin, Issue 5/2020.

Since March 2020 the severity of the economic and financial implications stemming from the coronavirus (COVID-19) crisis has become increasingly apparent. The ECB has responded with a decisive policy package that is designed to be targeted and proportionate to the unprecedented scale of the crisis as well as temporary, as the emergency and its aftermath are expected to be reabsorbed over time. These measures have supported liquidity and funding conditions in the euro area economy, averted the most adverse feedback loops between the real economy and financial markets, and shored up confidence. They are also expected to significantly contribute to ensuring that inflation in the euro area moves towards levels that are below, but close, to 2% in a sustained manner.

The impact of policy measures on financial conditions

This box examines the impact of the ECB’s response to the crisis, concentrating on asset purchases and the targeted longer-term refinancing operations (TLTRO III). The ECB’s monetary policy response has focused on addressing three key issues: (i) market stabilisation, which is a precondition for avoiding fragmentation and safeguarding the monetary policy transmission mechanism across the euro area; (ii) providing ample central bank liquidity to support credit provision to the real economy; and (iii) ensuring that the overall stance is sufficiently accommodative.[1]

As the severity of the pandemic crisis emerged, investors rebalanced their portfolios, thereby causing liquidity in several securities markets to dry up and increasing the demand for safe assets. The sharp decline in stock and bond market indices, combined with the increase in market-based financing costs for firms, contributed to a marked tightening of financial conditions between mid-February and mid-March 2020. In this environment, there was a very tangible risk of adverse liquidity spirals and an overshooting of asset price corrections in many markets, which would endanger financial stability and impede the transmission of monetary policy.

In a monetary union, increased risk perception can lead to flight-to-safety dynamics in the form of reallocations across sovereign bond markets. As sovereign yields are often the benchmark in pricing assets and setting lending rates, non-fundamental volatility in sovereign spreads impairs the transmission of monetary policy across the euro area.

The announcement of the pandemic emergency purchase programme (PEPP) in March, with its inherent flexibility, has acted as a powerful market-stabilising force. Policy measures aimed at releasing the balance sheet constraints of the private sector are particularly effective in periods of heightened market stress. In this vein, the announcement of the PEPP halted the tightening in financial conditions which had prevailed. The crucial transmission of changes in the overnight index swap (OIS) rates to the euro area GDP-weighted sovereign yield curve, which up to March 2020 had been closely linked and then became increasingly impeded by the COVID-19 crisis, was restored (see Chart A). In fact, following the PEPP announcement, the decline in fragmentation and the associated fall in the GDP-weighted sovereign yield were significant.

Chart A

Drivers of euro area and US sovereign yields

(percentage points) Source: ECB calculations.

Note: “10-year US Treasury” stands for “10-year US Treasury yield”.

At the same time, the provision of ample central bank liquidity to help support the credit flow to the real economy has also been central to the ECB’s monetary policy response to the COVID-19 crisis. This is particularly relevant in the euro area, where banks play a key role in financial intermediation. The provision of central bank liquidity comes in the form of targeted and non-targeted programmes. With respect to the former, the recalibration of TLTRO III in April 2020 included a considerably more favourable interest rate on TLTRO III operations during the period from June 2020 to June 2021. This followed the March 2020 decision to increase the maximum amount that counterparties are entitled to borrow in TLTRO III operations.[2] In line with this, banks indicated in the April 2020 euro area bank lending survey that TLTRO III is having a net easing impact on the terms and conditions offered to borrowers, and a positive net impact on their lending volumes, particularly their expected lending volumes over the next six months. The changes to the terms of TLTRO III were followed by a large expansion in the central bank funding of banks. In the June 2020 operation of TLTRO III, banks bid for a total of €1,308 billion in TLTRO funds, which is the largest amount allotted to date under any single lending operation. In relation to non-targeted programmes, the ECB announced, in March 2020, additional longer-term refinancing operations (LTROs) to provide immediate liquidity support to the euro area financial system and, in April 2020, a series of non-targeted pandemic emergency longer-term refinancing operations (PELTROs). The PELTROs serve as a backstop by helping to ensure sufficient liquidity and smooth money market conditions in response to the crisis.[3]

Once market stabilisation and maintaining credit provision to the real economy were attained, and the ramifications of the pandemic crisis on the baseline macroeconomic outlook became clearer, the PEPP recalibration in June 2020 was able to further ease the general monetary policy stance. In line with the PEPP’s dual role of rekindling the initial stages of the transmission of monetary policy and easing the general monetary policy stance, and in response to the pandemic-related downward revision to inflation over the projection horizon, the recalibration of the PEPP in June 2020 has further eased the general monetary policy stance to make it commensurate to the outlook for medium-term inflation. By extracting the duration risk held by investors through its purchases, the ECB reinforces the impact of its negative interest rate policy and forward guidance on rates by pushing down the medium and long end of the yield curve.[4]

Taken together, the PEPP decisions from March and June 2020 as well as the scaling-up of the asset purchase programme (APP) decided in March 2020 are estimated to have reduced the euro area GDP-weighted ten-year sovereign yield by almost 45 basis points.[5] However, such estimates are likely to be on the conservative side as they are based on estimates of the elasticities of sovereign yields to purchases derived from the public sector purchase programme (PSPP). Evidence from event studies, which examine the financial market reaction to the PEPP announcements, suggests a higher PEPP elasticity compared with the PSPP elasticity, thereby indicating some possible underestimation of the yield impact. The higher elasticity might reflect the flexibility embedded in the PEPP’s design, which makes it an effective tool in an environment of market stress as it can temporarily allocate purchases to those market segments where such purchases are most needed.[6] Therefore, in the absence of the PEPP, sovereign yields could have escalated to even higher levels.

The macroeconomic impact

By counteracting the tightening of financial conditions that confronted the euro area economy in the face of the COVID-19 crisis, the ECB’s policy measures have been providing crucial support to the real economy and, ultimately, to price stability. This support operates across two broad dimensions: (i) underpinning the medium-term growth and inflation outlook, and (ii) removing tail risks around the baseline scenario.

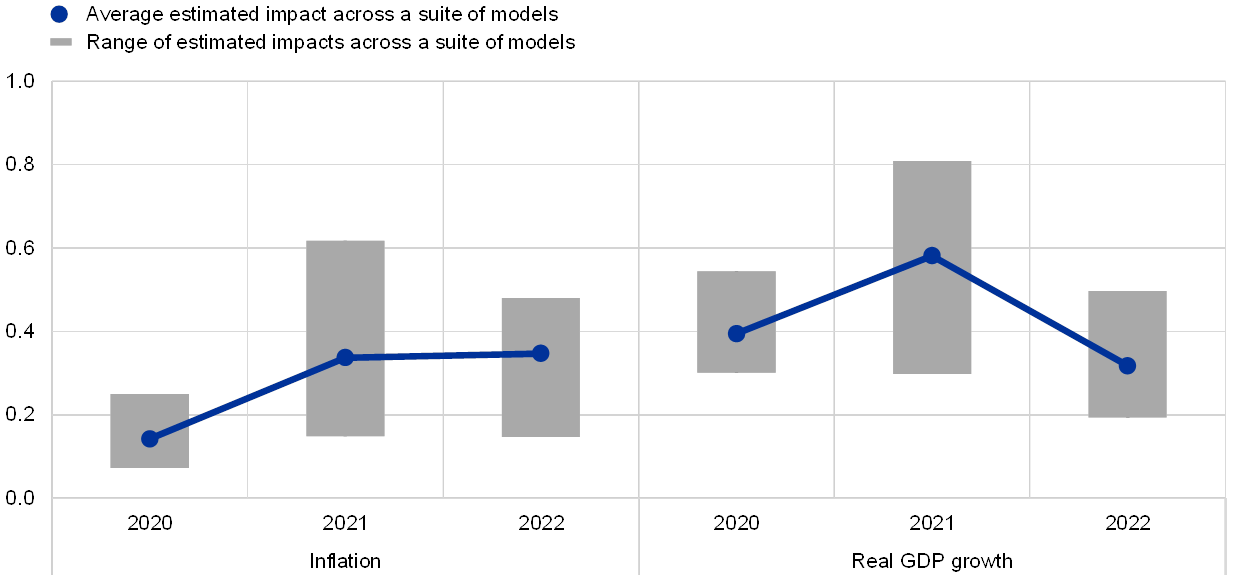

In terms of underpinning the medium-term growth and inflation outlook, ECB staff estimate that, taken together, the PEPP, the scaling-up of the APP and the recent TLTRO III recalibration will add around 1.3 percentage points cumulatively to euro area real GDP growth over the projection horizon, and contribute around 0.8 percentage points cumulatively to the annual inflation rate over the same time horizon (see Chart B). At the same time, while monetary policy typically acts with a transmission lag, the positive impact on consumer and business confidence created by acting swiftly and decisively during a crisis should not be overlooked and can accelerate and support the transmission of monetary policy to growth and inflation.

Chart B

Estimated impact of the ECB’s decisions since March 2020 (PEPP, scaling-up of the APP and TLTRO recalibrations) on the central tendency of inflation and economic activity

Source: ECB calculations.

Note: The estimated impact across a suite of models refers to the average across a set of models used by the Eurosystem for policy simulations, a BVAR model (see Rostagno, M., Altavilla, C., Carboni, G., Lemke, W., Motto, R., Saint-Guilhem, A. and Yiangou, J., “A tale of two decades: the ECB’s monetary policy at 20”, Working Paper Series, No 2346, ECB, Frankfurt am Main, December 2019), the NAWM-II model and the ECB-BASE model.

These estimates do not fully capture the benefits gained from avoiding feedback loops between the real economy and financial markets that may emerge in an economic crisis such as that caused by COVID-19, in which the main contribution of monetary policy is to remove tail risks around the baseline macroeconomic outlook. Econometric evidence points to the existence of large non-linearities in the macroeconomic reaction to shocks to financial conditions. In other words, the impact of a given change in financial conditions depends on the state of the economy. This means that under acute financial market stress, the presence of financial frictions and balance sheet constraints implies severe non-linearities that may translate into much larger contractionary effects brought on by a tightening of financial conditions. Given the severity of the shock associated with the COVID-19 crisis, a tightening of financial conditions in the current environment would be expected to have an impact several times larger than the one captured by the average elasticities employed in Chart B to quantify the impact of the policy. Therefore, monetary policy measures aimed at counteracting such deterioration in financial conditions would deliver a stronger contribution to price stability than is captured by standard elasticities derived from the more normal conditions underpinning the above quantification.

Overall, the ECB’s measures have been an effective and efficient response to the COVID-19 crisis, and they are proportionate under current conditions in the pursuit of the ECB’s price stability mandate. The effectiveness of the ECB’s measures is clearly evident in the improving financing conditions for the overall economy, and the deployment of a combination of asset purchases and TLTROs reflects the fact that they are efficient tools under the current circumstances. Additionally, they are proportionate to the severe risks to the ECB’s mandate, with the net impact of the COVID-19 crisis on the medium-term inflation outlook expected to be disinflationary to a considerable degree. While the ECB continually monitors the side effects of its policies, the case for monetary easing through the PEPP has been overwhelming given that the ECB’s price stability objective would have been subject to further downside risks in the absence of such measures.

- For further analysis, see Lane, P.R.: (i) “Pandemic central banking: the monetary stance, market stabilisation and liquidity”, speech at the Institute for Monetary and Financial Stability Policy Webinar, 19 May 2020; (ii) “The ECB’s monetary policy response to the pandemic: liquidity, stabilisation and supporting the recovery”, speech at the Financial Center Breakfast Webinar, organised by Frankfurt Main Finance, 24 June 2020; (iii) “Expanding the pandemic emergency purchase programme”, The ECB Blog, European Central Bank, 5 June 2020; and (iv) “The monetary response to the pandemic emergency”, The ECB Blog, European Central Bank, 1 May 2020. See also Schnabel, I.: (i) “The ECB’s monetary policy during the coronavirus crisis – necessary, suitable and proportionate”, speech at the Petersberger Sommerdialog, 27 June 2020; and (ii) “The ECB’s policy in the COVID-19 crisis – a medium-term perspective”, speech at the online seminar hosted by the Florence School of Banking & Finance, 10 June 2020.

- In particular, the interest rate on TLTRO III operations during the period from June 2020 to June 2021 is 50 basis points below the average interest rate on the Eurosystem’s main refinancing operations prevailing over the same period. For counterparties whose eligible net lending reaches the lending performance threshold, the interest rate over the period from June 2020 to June 2021 can be as low as 50 basis points below the average deposit facility rate prevailing over the same period. The borrowing allowance is 50% of the stock of eligible loans.

- The PELTROs consist of seven refinancing operations commencing on 20 May 2020 and maturing in a staggered sequence between July and September 2021. They are carried out as fixed rate tender procedures with full allotment, with an interest rate that is 25 basis points below the average rate on the main refinancing operations prevailing over the life of each PELTRO.

- For a more extensive discussion of duration risk, see Lane, P.R., “The yield curve and monetary policy”, speech at the Public Lecture for the Centre for Finance and the Department of Economics, University College London, 25 November 2019.

- The assessment considers the €750 billion overall envelope of the PEPP announced in March, the increase of the envelope by €600 billion announced in June, and the additional €120 billion temporary envelope under the APP until the end of 2020 announced in March.

- That asset purchases have a larger impact during market distress is consistent with the theoretical insights proposed in Vayanos, D. and Vila, J., “A preferred-habitat model of the term structure of interest rates”, NBER Working Paper, No 15487, 2009. At the same time, higher market distress can lead to market segmentation and impede portfolio rebalancing, as is found to be the case with the LSAP1 in the United States (see: Krishnamurthy, A. and Vissing-Jorgensen, A., “The Effects of Quantitative Easing on Long-term Interest Rates”, Brookings Papers on Economic Activity, 2011, pp. 215-265; Krishnamurthy, A. and Vissing-Jorgensen, A., “The Ins and Outs of LSAPs”, mimeo, Federal Reserve Bank of Kansas City, 2013; and D’Amico, S. and King, T.B., “Flow and Stock Effects of Large-Scale Treasury Purchases: Evidence on the Importance of Local Supply”, Journal of Financial Economics, Vol. 108, No 2, 2013, pp. 425-448). In Altavilla, C., Carboni, G. and Motto, R., “Asset purchase programmes and financial markets: lessons from the euro area”, ECB Working Paper, No 1864, 2015, the authors assess the ECB’s APP, which took place during a period of lower market distress, and find that local supply channels play a more limited role when compared with duration and credit risk channels.