Eurosystem balance sheet

The annual consolidated balance sheet of the Eurosystem comprises the assets and liabilities of euro area national central banks (NCBs) and the ECB held at year-end vis-à-vis third parties.

Claims and liabilities between Eurosystem central banks (intra-Eurosystem claims and liabilities) are netted and are therefore not visible.

The content and format of the Eurosystem’s annual consolidated balance sheet are set out in Annexes IV and VII to Guideline (EU) 2016/2249 of the European Central Bank of 3 November 2016 on the legal framework for accounting and financial reporting in the European System of Central Banks (ECB/2016/34).

Financial developments in 2022

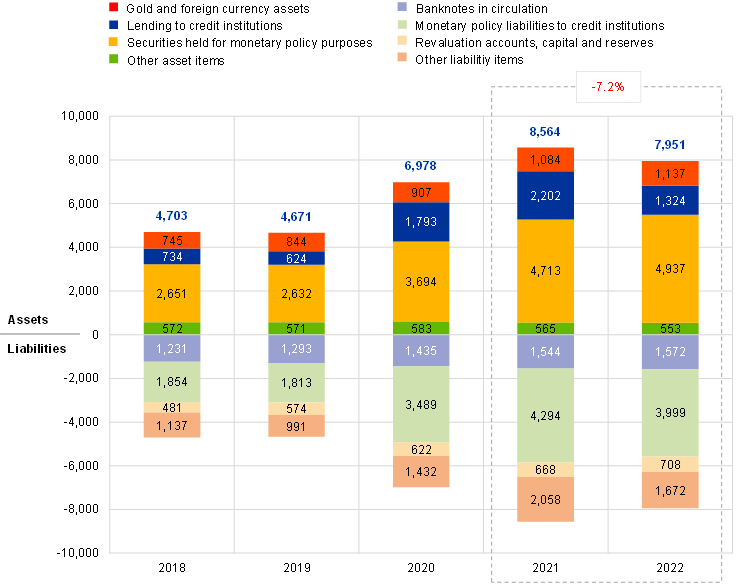

In 2022 the Eurosystem’s balance sheet total decreased by €613.3 billion to €7,951 billion (-7.2%), mainly because of the decrease in Eurosystem refinancing operations, in particular due to the maturing of and early repayments under the third series of targeted longer-term refinancing operations (TLTRO III).

Chart 1 presents the main components of the Eurosystem’s balance sheet from 2018 to 2022. Net purchases of securities under the asset purchase programme (APP)[1] ceased in December 2018 and resumed in November 2019, as a result of which the size of the Eurosystem’s balance sheet decreased slightly in 2019. The increase in the size of the balance sheet in 2020 and 2021 can mainly be attributed to the monetary policy measures taken to soften the impact of the coronavirus (COVID-19) pandemic: the pandemic emergency purchase programme (PEPP)[2], more favourable conditions for TLTRO III operations and the continuation of net purchases under the APP. The decrease in the size of the balance sheet in 2022 was mainly due to the maturing of and early repayments under TLTRO III operations, which were only partially offset by the increase in securities held under the APP and PEPP as a result of net purchases during the year[3].

Chart 1

Eurosystem balance sheet by component, 2018-22

(EUR billions)

Source: Eurosystem.

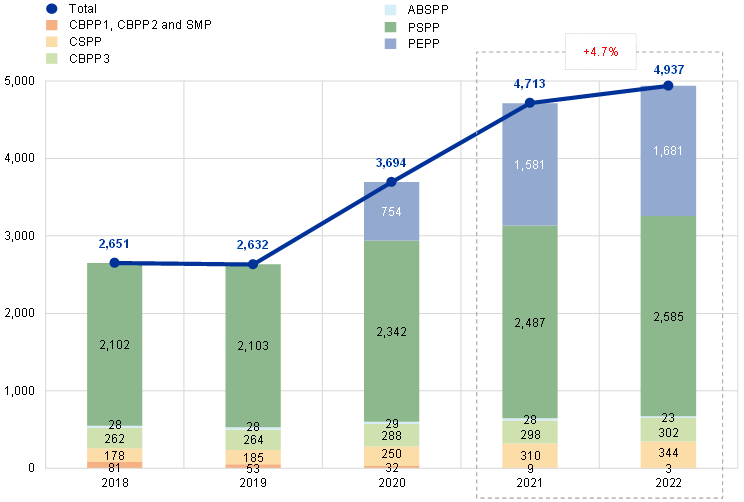

Euro-denominated securities held for monetary policy purposes (asset item 7.1) constituted 62.1% of the Eurosystem’s total assets as at the end of 2022. Under this balance sheet item, the Eurosystem holds securities acquired under the APP, the PEPP and the terminated Securities Markets Programme (SMP). All remaining securities held under the first two covered bond purchase programmes (CBPP1 and CBPP2) matured during 2022.

In 2022 securities held by the Eurosystem for monetary policy purposes increased by €223.8 billion to €4,937.2 billion (Chart 2), with PEPP purchases accounting for 44.7% (or €100 billion) of this increase. Securities holdings under the APP increased by €130.3 billion to €3,253.7 billion. Securities held under the SMP and under CBPP1 and CBPP2 declined by €3.7 billion and €2.8 billion respectively owing to redemptions.

Chart 2

Securities held for monetary policy purposes, 2018-22

(EUR billions)

Source: Eurosystem.

Impairment tests of securities held for monetary policy purposes are conducted on an annual basis and approved by the Governing Council. As a result of the impairment tests conducted at the end of 2022, the Eurosystem has not recorded any impairment losses on the securities held in its monetary policy portfolios.

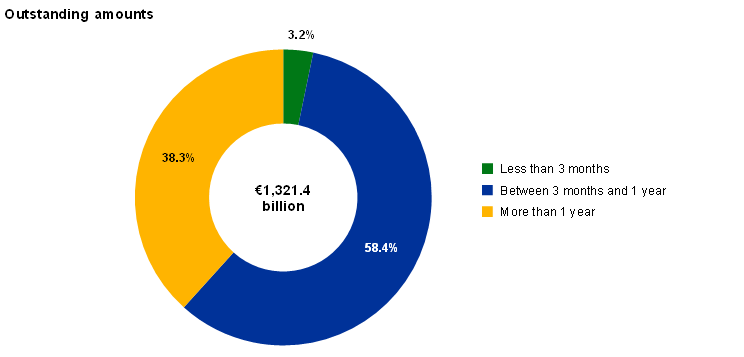

Lending to credit institutions (asset item 5)[4] decreased by €877.5 billion to €1,324.3 billion. The decrease is almost entirely attributable to the maturing of and early repayments under TLTRO III operations (€880.4 billion), while repayments under pandemic emergency longer-term refinancing operations (PELTROs) amounted to €2.3 billion. Allotments under the three-month longer-term refinancing operations increased by €2.6 billion. Chart 3 shows the maturity breakdown of outstanding longer-term refinancing operations (asset item 5.2) as at 31 December 2022.

Chart 3

Residual maturity of outstanding longer-term refinancing operations

Source: Eurosystem.

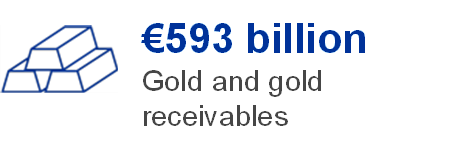

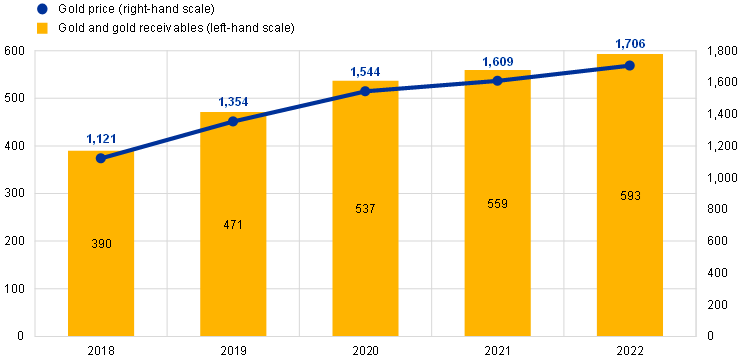

In 2022 the value of the Eurosystem’s gold and gold receivables (asset item 1) increased by €33.5 billion to €592.9 billion (Chart 4), primarily reflecting the rise in the market price of gold in euro terms. This increase also led to an equivalent increase in the Eurosystem’s gold revaluation accounts.

Chart 4

Gold holdings and gold prices, 2018-22

(left-hand scale: EUR billions; right-hand scale: euro per fine ounce of gold)

Source: Eurosystem.

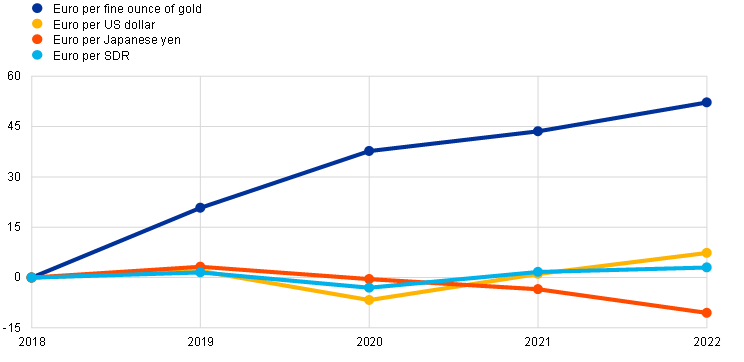

The net position of the Eurosystem in foreign currency (asset items 2 and 3 minus liability items 7, 8 and 9) rose by €17 billion in euro terms to €346.1 billion. The increase was mainly the result of customer and portfolio transactions, which accounted for €14.6 billion. The remaining increase of €2.4 billion was due to the effect of the revaluation of assets and liabilities denominated in foreign currency. The Eurosystem’s foreign currency holdings comprise mainly US dollars, special drawing rights (SDRs) and Japanese yen.

In line with the Eurosystem’s harmonised accounting rules, gold, foreign exchange and financial instruments (other than securities classified as held-to-maturity, non-marketable securities and securities held for monetary policy purposes) are revalued at market rates and prices. The gold price and the principal exchange rates used for the revaluation of year-end balances and those of the previous year-end were as follows:

Chart 5 below shows the gold price and main foreign currency rate movements against the euro during the period from 2018 to 2022.

Chart 5

Main foreign exchange rates and gold price, 2018-22

(percentage changes vis-à-vis 2018, year-end data)

Source: Eurosystem.

In 2022 banknotes in circulation[5] (liability item 1) increased by €27.6 billion to €1,572 billion, an increase of 1.8% compared with 2021.

Base money, which in addition to banknotes in circulation includes current accounts (liability item 2.1) and the deposit facility (liability item 2.2), decreased by €266.4 billion to €5,569.8 billion in 2022. This was mainly due to the smaller size of outstanding Eurosystem refinancing operations and the discontinuation of net purchases of monetary policy securities. The large shift of funds from current accounts (liability item 2.1) to the deposit facility (liability item 2.2) was primarily due to the reallocation of credit institutions’ excess liquidity to this facility following the rise of the deposit facility rate above 0% as of 14 September 2022.

Liabilities to other euro area residents denominated in euro (liability item 5) fell by €192.5 billion to €564.6 billion as a result of a decrease in deposits of government and other euro area residents, including financial institutions not subject to minimum reserve requirements.

Liabilities to non-euro area residents denominated in euro (liability item 6) declined by €169.2 billion to €540.7 billion, mainly due to a reduction in deposits of financial institutions, in particular under the Eurosystem reserve management services (ERMS)[6].

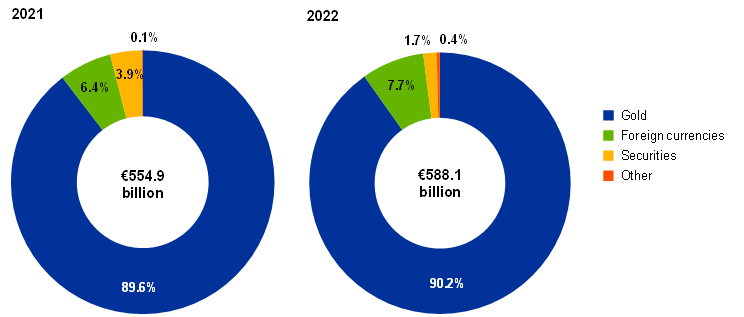

Revaluation accounts (liability item 11) increased by €33.2 billion to €588.1 billion in 2022, primarily reflecting a rise in the revaluation accounts for gold and foreign currencies (Chart 6).

Chart 6

Breakdown of revaluation accounts, 2021-22

Source: Eurosystem.

Capital and reserves (liability item 12) increased by €7.2 billion to €120.2 billion in 2022. Some Eurosystem central banks maintain provisions (part of liability item 10) for risks that have not materialised.[7] These provisions stood at €115.6 billion at the end of 2022, compared with €115.9 billion at the end of 2021.

The APP consists of the third covered bond purchase programme (CBPP3), the asset-backed securities purchase programme (ABSPP), the public sector purchase programme (PSPP) and the corporate sector purchase programme (CSPP). Further details can be found on the ECB’s website under Asset purchase programmes.

The PEPP is a temporary asset purchase programme of private and public sector securities initiated in March 2020 to counter the serious risks to the monetary policy transmission mechanism and the outlook for the euro area posed by the pandemic. Further details can be found on the ECB’s website under Pandemic emergency purchase programme.

The Governing Council decided to discontinue net asset purchases under the PEPP and APP as of the end of March 2022 and 1 July 2022 respectively.

More information about lending can be found on the ECB’s website under Open market operations.

Information on the development of banknotes in circulation since 2002, broken down by denomination, can be found on the ECB’s website under Banknotes and coins circulation.

More information on the ERMS can be found on the ECB’s website under Eurosystem reserve management services.

The creation of these provisions is subject to the legal frameworks of the individual central banks. Provisions related to Eurosystem monetary policy operations are not included.