Published as part of the ECB Economic Bulletin, Issue 8/2022.

This box explores how financing gaps faced by euro area firms and these firms’ expectations about the future availability of finance relate to current and future macroeconomic outcomes. The ongoing monetary policy normalisation is gradually tightening financing conditions and influencing the supply of external finance as part of the standard transmission of monetary policy. A key question is the impact of changes in financing conditions and access to finance on firm-specific and aggregate growth. The Survey on the Access to Finance of Enterprises (SAFE) provides detailed information about the financing conditions for euro area firms. The SAFE has been conducted biannually since 2009 and surveys around ten thousand firms across the euro area. This box analyses the link between macroeconomic developments and two key indicators in the SAFE: the change in the external financing gap, defined as the difference between the change in demand for and the change in the availability of external financing, and the change in firms’ expectations about the availability of bank loans.[1]

At the current juncture, euro area firms report a widening of their financing gaps and expect a decline in the future availability of bank loans (Chart A). Since the inception of the SAFE in 2009, there has generally been an inverse relation between changes in the financing gap and expectations about the future availability of bank loans. Moreover, an expansion of euro area activity (i.e. positive real GDP growth rates) has usually coincided with declining financing gaps for firms, as well as greater optimism on the part of firms about the future availability of bank loans. The evolution of these indicators has in the past been influenced by the euro area business cycle as well as by the ECB’s monetary policy. During the 2011-2013 sovereign debt crisis the financing gaps of euro area firms increased markedly, indicating the difficulties faced by firms in covering their external financing needs. Subsequently, supported by monetary policy easing by the ECB, financing gaps gradually decreased and expectations about the availability of bank loans improved. After the outbreak of the coronavirus (COVID-19) pandemic in 2020, financing conditions deteriorated sharply but were again stabilised by monetary policy and public sector support. The deterioration was therefore only temporary. Most recently, against the backdrop of weakening economic growth, rising inflation and monetary policy normalisation, firms have started to signal widening financing gaps and expect a reduced availability of bank loans for the period from October 2022 to March 2023.

Chart A

Changes in the financing gap, expected availability of bank loans and financing obstacles as reported by euro area enterprises and development of euro area real GDP growth

(weighted net balances of external financing gap, net percentage changes in the expected availability of finance, annualised percentage changes)

Sources: ECB and European Commission Survey on the Access to Finance of Enterprises (SAFE) and Eurostat.

Notes: The financing gap indicator combines both financing needs and the availability of bank loans at firm level. For each of the five financing instruments, the indicator of the perceived change in the financing gap takes a value of 1 (-1) if the need increases (decreases) and availability decreases (increases). If enterprises perceive only a one-sided increase (decrease) in the financing gap, the variable is assigned a value of 0.5 (-0.5). A positive value for the indicator points to an increase in the financing gap. Values are multiplied by 100 to obtain weighted net balances in percentages. The first vertical grey line denotes the announcement of the Outright Monetary Transactions; the second vertical grey line denotes the start of the first series of targeted longer-term refinancing operations (TLTRO I) and the negative interest rate policy; the third vertical grey line denotes the start of TLTRO II and the corporate sector purchase programme; the fourth one denotes the start of the pandemic emergency purchase programme and TLTRO III; and the last vertical grey vertical line denotes the rise of the three key ECB interest rates by 50 basis points and approval of the Transmission Protection Instrument (TPI) in July 2022.

However, despite the recent increases in the cost of borrowing, euro area firms were still not particularly concerned about access to finance (Chart A). In the latest survey round, the percentage of firms reporting obstacles to obtaining bank loans remained broadly unchanged compared to previous survey rounds, mainly supported by banks’ unchanged willingness to provide credit.[2]

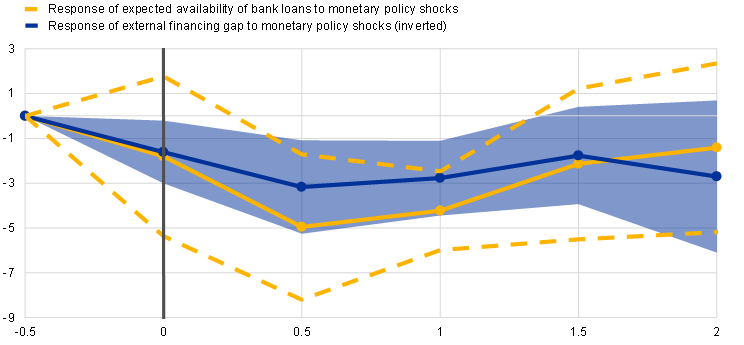

A tightening of monetary policy increases firms’ financing gaps and lowers their expectations about the future availability of bank loans (Chart B). An econometric exercise allows for a more quantitative assessment of the transmission of monetary policy to firms’ financing conditions. This is done using local projections[3], which estimate the response of firms’ financing gaps and their expectations about the future availability of bank loans (measured at the aggregate level by net balances across firms) to identified monetary policy shocks[4]. Monetary policy shocks are measured here by the target factor of Altavilla et al. (2019), which captures surprises in interest rates at the short end of the yield curve around ECB monetary policy announcements.[5] Chart B shows that monetary policy shocks have a significant effect on firms’ financing gaps and expectations about the future availability of bank loans within a two-year horizon. Specifically, a monetary policy shock of one standard deviation, which is equivalent to a 4 basis point shock to the one-month OIS rate, is estimated to increase the average firm’s financing gap by around 3 percentage points over six months.[6] In comparison, the standard deviation of the change in the financing gap has been 7% since 2009. The same shock results in a 5-percentage-point drop in the net share of firms expecting an increase in the availability of bank loans. The effects are persistent until up to two years after the shock, indicating how monetary policy affects financing conditions of firms through the supply of credit. These findings confirm those of previous studies that funding expectations play an important role in the bank lending channel of monetary policy.[7] Once actual credit conditions change, the interplay between changes in the availability and demand for bank loans is affected as well.

Chart B

Response of firms’ financing gaps and expectations of the future availability of bank loans to an identified monetary policy shock

(horizontal axis: years after shock, vertical axis: percentage point changes relative to period before the shock)

Sources: ECB and European Commission Survey on the Access to Finance of Enterprises (SAFE), Altavilla et al. (2019), ECB calculations.

Notes: Response of firms’ financing gaps and the net percentage of firms reporting an expected increase in the availability of bank loans over the next six months after a one-standard-deviation monetary policy shock. The shock used is the target factor from Altavilla et al. (2019), capturing monetary policy surprises in the very short end of the OIS curve in and around ECB monetary policy announcements. The effect of the monetary policy shocks on SAFE variables are estimated using local projections (Jorda, 2005). The shaded and dotted areas are 95% confidence bands based on Newey-West.

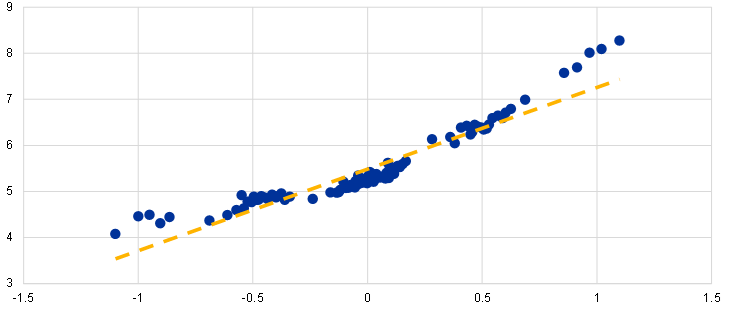

When financing gaps increase, firms tend to be more concerned about future access to finance, suggesting that changes in financing gaps matter for firms’ growth prospects (Chart C). To assess whether changing financing conditions affect the real economy, a natural test is to analyse their effect on business sentiment. The SAFE measures business sentiment by asking firms to indicate to what extent they are concerned about access to finance.[8] Overall, firms have not considered access to finance to be their main concern in recent years, likely due to the extended period of monetary accommodation.[9] However, this might change as monetary policy is being normalised. Firm-level data is used to study the relationship between financing gaps and firms’ concerns about access to finance. Chart C shows the correlation between the financing gaps and levels of concern regarding access to finance. This is done by grouping firms’ replies since 2009 into bins according to their rating of access to finance as a concern, after having removed common variation within countries and time periods and computing the bin-specific average level of concern about finance. The positive correlation indicates that firms with large financing gaps perceive access to finance as a more pressing concern. Financing gaps therefore appear relevant to firms’ overall sentiment and may plausibly affect their future growth prospects.

Chart C

Relationship between concerns about access to finance and financing gaps at the firm level

(horizontal axis: residualised change in external financing gap, vertical axis: residualised degree of concern)

Sources: ECB and European Commission Survey on the Access to Finance of Enterprises (SAFE), ECB calculations.

Notes: Binned scatterplot of the financing gap for bank loans against the degree to which firms are concerned about access to finance, conditional on country-by-time fixed effects.

Financing gaps and expectations about the availability of bank loans are related to current and future real GDP growth. Although firms’ availability of external financing affects their business sentiment, it is important to investigate how they are related to macroeconomic outcomes. The average evolution of euro area GDP growth following net changes in financing gaps and expectations from the SAFE as measures of changes in financing conditions is estimated using local projections.[10] Although the estimates cannot be considered causal effects, they provide an indication of average future developments after a given change in the SAFE measures. Chart D shows that after a 1 percentage point increase in the financing gap indicator or a decrease in the balance of expectations about the future availability of bank loans, real GDP in the euro area declines on average by about 0.2% more in the subsequent year relative to no change in these financing indicators, with some modest further effect during the subsequent year. These effects are estimated conditional on current and lagged GDP growth, thereby using the informational content contained in SAFE above and beyond currently observable developments in the business cycle. The estimated effects are persistent, especially when considering changes in firms’ expectations about the availability of finance. This suggests that forward-looking variables, a unique feature of the SAFE, contain useful information for understanding the future development of the euro area economy.

Chart D

Average evolution of euro area real GDP after a deterioration in financing conditions or in the expected availability of bank loans, relative to no deterioration

(horizontal axis: years after shock, vertical axis: cumulated growth in percent relative to period before the shock)

Sources: ECB and European Commission Survey on the Access to Finance of Enterprises (SAFE), ECB calculations.

Notes: Average evolution of euro area real GDP growth in cumulated terms after changes in firms’ financing gaps and the net percentage of firms reporting an expected increase in the availability of bank loans. The local projections (Jorda, 2005) include current and past GDP growth as control variables. The shaded and dotted areas are 95% confidence bands based on Newey-West.

Bank loans are the most widely used source of external finance for euro area firms.

The financing obstacles indicator is the sum of the percentages of firms reporting the rejection of loan applications, loan applications for which only a partial amount was granted, and loan applications which resulted in an offer that was declined by the firms because the borrowing costs were too high, as well as the percentage of firms that did not apply for a loan for fear of rejection. See Survey on the Access to Finance of Enterprises in the euro area – October 2021 to March 2022, ECB, June 2022.

See Jorda, Oscar, “Estimation and inference of impulse responses by local projections,” American Economic Review, Vol. 95, No 1, March 2005, pp. 161–182.

The local projection is executed by performing a sequence of regressions specified by for , where are changes in the financing gap or expectations about finance, respectively, based on SAFE in wave . The coefficients reflect the impulse-response function of the financing gap or expectations of future bank loan availability to an identified monetary policy shock .

The shock is suitable in this context, as non-financial corporations typically rely on bank funding with interest rates fixed for less than one year. In our sample, the target factor ranges from -8.6 to 10.4 basis points. See Altavilla, C., Brugnolini, L., Gurkaynak, R. S., Motto, R., and Ragusa, G., “Measuring euro area monetary policy”, Journal of Monetary Economics, Vol. 108, December 2019, pp. 162–179.

To put this into perspective, the largest monetary policy shock to the one-month OIS is around 10 basis points over the sample considered.

See Ferrando, A., Popov., A. and Udell, G., “Unconventional monetary policy, funding expectations and firm decisions”, European Economic Review, Vol. 149, October 2022.

Firms provide an answer on a scale of 1 (not at all important) to 10 (extremely important) regarding finance, as well as a selection of other problems. The derived indicator is normally used to detect the relative importance of financing with respect to other problems affecting firms, such as increasing costs of production or labour or difficulties finding customers.

See Survey on the Access to Finance of Enterprises in the euro area – October 2021 to March 2022, ECB, June 2022.

For a related exercise assessing how information from the Bank Lending Survey relates to future lending volumes, please see the box entitled “What information does the euro area bank lending survey provide on future loan developments?”, Economic Bulletin, Issue 8, ECB, 2022.