- 9 OCTOBER 2025 · RESEARCH BULLETIN NO. 135

Details matter – how loan pricing affects monetary policy transmission in the euro area

Merely classifying loans as fixed-rate or floating-rate[2] fails to fully capture their distinct sensitivity to changes in ECB policy rates. We analysed the maturity of the relevant risk-free rates used to price new loans to see if it affected their short-term interest rate sensitivity – which it did. In countries where new loans were priced using shorter-term risk-free rates, interest rates increased more sharply during the ECB’s monetary tightening, regardless of the loan’s own maturity. This effect was not purely mechanical. Banks partly offset this rise by lowering the premia they charged. By looking beyond headline classifications, we gain a more nuanced understanding of how variations in lending practices drive cross-country differences in monetary policy pass-through.

Beyond fixed and floating

Although the euro area has a single currency and a common monetary policy, lending practices differ between euro area countries in several ways that shape the pass-through of monetary policy. In Vilerts et al. (2025), we study a less explored difference: the maturity of the relevant overnight interest rate swap (OIS) at the time of issuance of new loans. We use data from AnaCredit, a comprehensive euro area-wide loan-level database, covering about seven million new loans issued by banks to non-financial corporations (NFCs) in 2022-23.[3] This timeframe encompasses the series of post-pandemic rate hikes.

Our preliminary analysis reveals that structural factors, such as loan type, firm size or loan maturity, explain only a small portion of the lending rate differences across euro area countries. This suggests that other loan characteristics may play a more significant role.[4] In our study, we break the interest rate on individual loans down into a “relevant risk-free rate” and a “premium” – the residual compensating banks for risk. The relevant risk-free rate is that of the OIS. For fixed-rate loans the maturity of the relevant OIS is that equal to the maturity of the loan, while for floating-rate loans it is the maturity corresponding to the loan’s reference rate at origination.[5] For example, the relevant risk-free rate for a five-year fixed-rate loan is the five-year OIS rate on the issuance date. In contrast, for a five-year floating-rate loan benchmarked against a three-month EURIBOR and adjusted every three months, the relevant risk-free rate would be the three-month OIS rate. The premium is then calculated as the difference between the lending rate and the relevant risk-free rate.

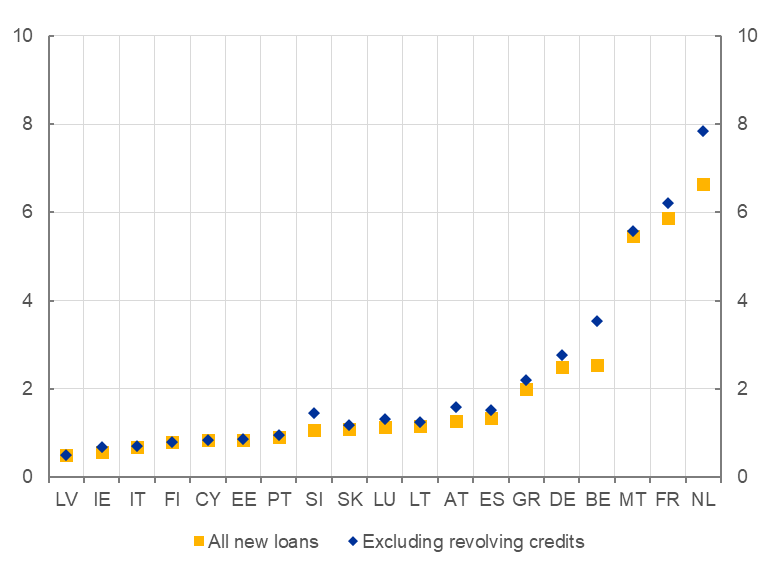

We find striking cross-country variation (Chart 1) in the maturity of the relevant risk-free rates: in countries such as Latvia and Ireland maturities are very short – around six months on average. Meanwhile in other countries, such as the Netherlands, Malta and France, they often exceed five years on average.

Chart 1

Cross-country heterogeneity in the maturity of the relevant risk-free rate

(years)

Source: Vilerts et al. (2025).

Note: The figure shows the weighted average maturity of the relevant risk-free rate for the newly issued loans of NFCs in euro area countries, 2022-23.

Loan characteristics key for pass-through

These structural differences mean that monetary policy transmits with varying strength and speed across the euro area, depending on which segment of the risk-free yield curve dominates local lending. Two key questions emerge. First, to what extent can the cross-country variation in the rise of average interest rates on new loans between early 2022 and late 2023 be explained by differences in the evolution of the risk-free rates used to price NFC loans? And, second, how does the maturity of the relevant risk-free rate affect the pass-through of monetary policy rate changes to interest rates on new loans?

“Before and after” analysis of lending rates

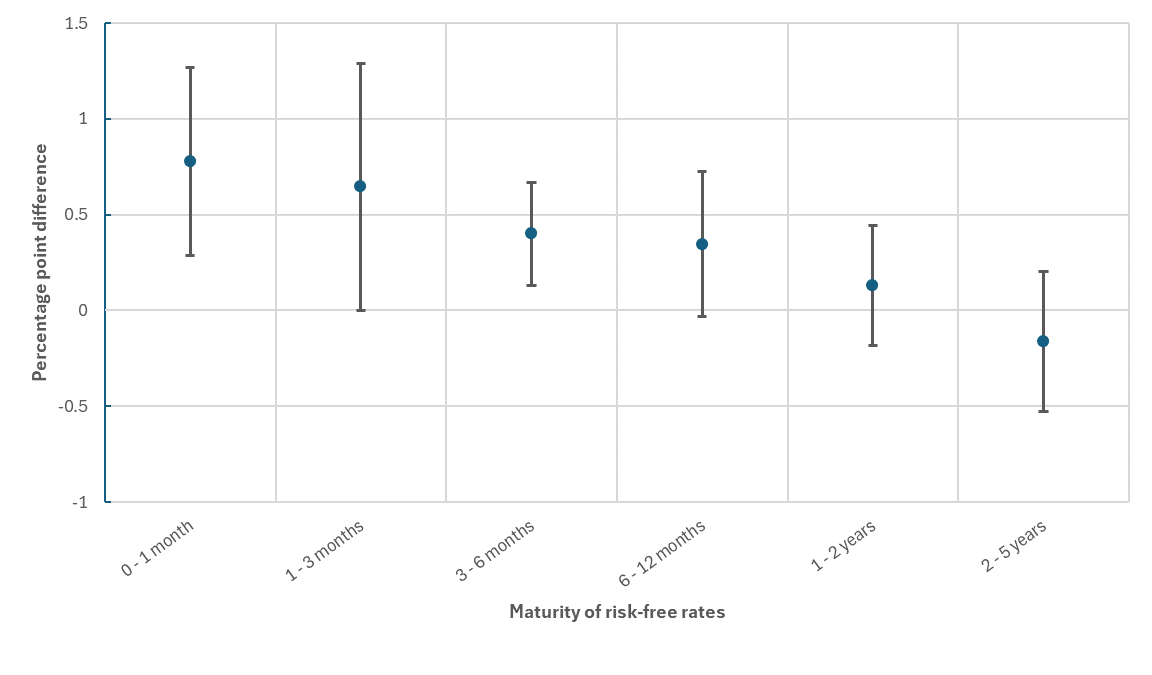

To address the first question, we employ a time-difference approach to analysing changes in interest rate levels. In particular, we compare interest rates – as well as adjustments in the relevant risk-free rates and shifts in the premium – on loans issued in two periods bracketing the 2022-23 tightening cycle.[6] They are the first quarter of 2022, before the first hike in July 2022, and the fourth quarter of 2023, after the final hike in September 2023. We find that most of the rise in interest rates on new loans during the post-pandemic tightening was driven by increases in the relevant risk-free rate (Chart 2).

Chart 2

“Before and after” analysis of lending rates

(conditional change between the first quarter of 2022 and the last quarter of 2023, percentage points)

Source: Vilerts et al. (2025).

Notes: The figure shows conditional changes in lending rates (from the first quarter of 2022 to the fourth quarter of 2023) with 95% confidence bands, breaking them down into the contributions from relevant risk-free rates and the premium.

Three key observations emerge from the analysis. First, the pass-through of changes in the relevant risk-free rates to changes in lending rates exhibits notable cross-country variation. Some 11 countries experienced an increase in relevant risk-free rates exceeding 4 percentage points, with Latvia and Estonia experiencing the highest increases at 4.37-4.41 percentage points. In contrast, the Netherlands and Malta saw risk-free rates rise by only 2.85 percentage points. Second, the distinction between fixed and floating-rate loans does not always provide a clear explanation for the observed patterns. For the relevant risk-free rates the change was particularly pronounced in countries like Latvia and Ireland, where floating-rate loans with short fixation periods are more prevalent. Similarly, a strong contribution of relevant risk-free rates was observed in Italy, despite its higher reliance on fixed-rate loans which tend to have shorter maturities. Third, a large increase in the relevant risk-free rates does not necessarily result in the largest increase in lending rates. In several countries, the rise in relevant risk-free rates was offset by a decline in the premium, which moderated the overall increase in lending rates.

Pass-through of monetary policy rates to lending rates

We then turn our attention to loans issued near ECB Governing Council meetings and use a stacked time-difference regression (following Bredl, 2024)[7] instead of a simple before-and-after comparison. Specifically, we examine how the pass-through of monetary policy rate changes varies across loans priced off different maturities of relevant risk-free rates, now using the full set of actual changes in the policy rate, instrumented by high-frequency surprises (Altavilla et al. 2019). As shown in Chart 3, the pass-through from monetary policy rates to lending rates strengthens as the maturity of the relevant risk-free rates shortens.

However, applying this approach to the components of interest rates shows that this mechanical pass-through is not the only factor at play, as we see adjustments in premia smoothing differences in pass-through across loan categories. We find that premia increased less for loans linked to shorter maturity risk-free rates, which partially offsets the differences in the aggregate pass-through to lending rates.

Chart 3

Stronger pass-through at shorter maturities

Source: Vilerts et al. (2025).

Notes: The figure shows the effect of a 1 percentage point increase in the deposit facility rate on lending rates for loans issued within the 6 weeks before or the 7-12 weeks after an ECB Governing Council meeting relative to loans for which the relevant risk-free rates have maturities over five years.

There are several possible explanations for this pattern. On the lender side, repricing of loans can at times outpace the pass-through to funding costs, improving net interest income and creating scope to lower premia on new loans – especially for those priced off short-term reference rates. On the borrower side, tighter policy can alter the composition of lending and firms may substitute borrowing across maturities and rate types. Overall, the evidence points to systematic smoothing effects: premia adjustments dampen differences in loan rate changes. This suggests that the variation reflects pricing within the bank rather than shifts in the banks doing the lending.

Loan pricing design matters for monetary policy

Our results point to several important implications for monetary policy. First, loan pricing design matters for monetary policy transmission. Markets where lending is tied to shorter maturities exhibit stronger and faster transmission. Second, loan premia also adjust independently of exogenous factors. When short-term rates move sharply, banks reprice loan premia over the relevant risk-free rate in ways that smooth differences across loans priced off different maturities. Recognising this interaction helps explain cross-country differences during tightening episodes and anticipate how the composition and pricing of new credit respond to policy.

References

Altavilla, C., Brugnolini, L., Gürkaynak, R.S., Motto, R. and Ragusa, G. (2019), “Measuring euro area monetary policy”, Journal of Monetary Economics, Vol. 108, Issue C, pp. 162-179.

Bredl, S. (2024), Regional loan market structure, bank lending rates and monetary transmission.

Vilerts, K., Anyfantaki, S., Beņkovskis, K., Bredl, S., Giovannini, M., Horky, F.M., Kunzmann, V., Lalinsky, T., Lampousis, A., Lukmanova, E., Petroulakis, F. and Zutis, K. (2025), “Details Matter: Loan Pricing and Transmission of Monetary Policy in the Euro Area”, Working Papers, No 3078, ECB.

This article was written by Kārlis Vilerts (Latvijas Banka), Sofia Anyfantaki (Directorate General Research, European Central Bank), Konstantīns Beņkovskis (Latvijas Banka), Sebastian Bredl (Deutsche Bundesbank), Massimo Giovannini (Bank of Malta), Florian Matthias Horky (Národná banka Slovenska), Vanessa Kunzmann (Central Bank of Ireland), Tibor Lalinsky (European Central Bank and Národná banka Slovenska), Athanasios Lampousis (Bank of Greece), Elizaveta Lukmanova (Central Bank of Ireland), Filippos Petroulakis (Bank of Greece) and Klāvs Zutis (Latvijas Banka). The authors gratefully acknowledge the comments of Alexander Popov and Zoë Sprokel. The underlying study has benefited greatly from comments received from Refet Gürkaynak, Vasso Ioannidou, Òscar Jordà and Carlo Altavilla. That study is part of the Challenges for Monetary Policy in a Changing World (ChaMP) Research Network, and the authors extend their gratitude to the leadership team of the ChaMP Network – Philipp Hartmann, Diana Bonfim, and Margherita Bottero. The views expressed here are those of the authors and do not necessarily represent the views of the European Central Bank or the Eurosystem.

A loan is considered to be a fixed-rate loan if it has an interest rate that remains constant over the entire duration of the loan. By contrast, a loan is treated as a floating-rate one if it has an interest rate that adjusts over time, typically linked to a defined reference interest rate (e.g. the EURIBOR or LIBOR).

We consider the 19-country composition of the euro area valid in 2022: Belgium, Germany, Estonia, Ireland, Greece, Spain, France, Italy, Cyprus, Latvia, Lithuania, Luxembourg, Malta, the Netherlands, Austria, Portugal, Slovenia, Slovakia and Finland. Croatia adopted the euro on 1 January 2023 so AnaCredit data for Croatia are only available as from 2023. We impose several restrictions when selecting the sample for our analysis. We limit our sample to credit lines, revolving credit and other loans, as these categories encompass the majority of lending activity across all euro area countries.

Specifically, to account for cross-country differences in loan portfolio structure in terms of loan types, firm size classes and maturities, we calculate the conditional mean interest rates and show that this adjustment has a minimal effect on cross-country variation.

In AnaCredit, the reference rate used for the calculation of the actual interest rate is formed by combining the reference rate value with the maturity value. The following reference rate values are used: EURIBOR, USD LIBOR, GBP LIBOR, EUR LIBOR, JPY LIBOR, CHF LIBOR, MIBOR, other single reference rates, other multiple reference rates. The following maturity values are used: overnight, one week, two weeks, three weeks, one month, two months, three months, four months, five months, six months, seven months, eight months, nine months, ten months, eleven months and twelve months.

We include an extensive set of loan-level controls and a rich set of fixed effects. However, the results should not be interpreted as causal or used to directly quantify the pass-through of monetary policy rates to lending rates in the euro area countries. This is because the policy rate changes between the first quarter of 2022 and the fourth quarter of 2023 were neither exogenous nor entirely unexpected. The “before and after” comparison offers valuable insights into cross-country differences in lending rate responses over the longer term, as the expectations regarding monetary policy changes were likely shared by agents across all countries within the monetary union.

In total, there were 15 ECB Governing Council meetings in 2022-23. Eight meetings were held in 2022, on 3 February, 10 March, 14 April, 9 June, 21 July, 8 September, 27 October and 15 December. Seven meetings were held in 2023, on 2 February, 16 March, 4 May, 15 June, 27 July, 14 September and 26 October.