Main findings from the ECB’s recent contacts with non-financial companies

Published as part of the ECB Economic Bulletin, Issue 5/2021.

This box summarises the results of contacts between ECB staff and representatives of 63 leading non-financial companies operating in the euro area. The exchanges took place between 28 June and 7 July 2021.[1]

Contacts reported strong growth overall, with activity mainly influenced by supply constraints and the easing of measures to contain the coronavirus (COVID-19) pandemic. The relaxation of measures gave rise to a stepwise and partial recovery in the affected service sectors, which also benefited their suppliers. Meanwhile, demand in the industrial sector continued to increase or remained elevated, but production lagged somewhat owing to persistent supply constraints.

As containment measures eased, services activity was the main driver of growth in the second quarter, although the recovery was still patchy. Contacts in or exposed to the travel and hospitality industries described a stepwise recovery in business during the second quarter, albeit still at very low levels. High street retailers reported strong growth in sales as outlets reopened, but generally still saw business somewhat below pre-pandemic levels.[2] This was especially the case for higher-quality or luxury goods, sales of which typically benefited from international tourism. The gradual reopening of hospitality and entertainment was supporting growth in services such as media and advertising and employment services. Meanwhile, contacts in services that had been largely unaffected or had benefited from the pandemic (such as telecoms, consulting and information services) generally reported strong or steady growth in their activity.

Contacts in the industrial sector reported still buoyant demand, while production was constrained by shortages of materials and components. The most acute shortage continued to be that of semiconductors. This had already significantly affected motor vehicle production but was also increasingly being felt across other parts of industry. Many contacts continued to mention shortages of a range of materials and components as well as delays in receiving inputs owing to transport bottlenecks, especially in container shipping. While these broader shortages mainly affected costs, production was also constrained to some extent. This, in turn, made it difficult to assess the strength of final demand, as customers brought purchases forward in anticipation of higher prices or over-ordered to guarantee supply. Meanwhile, delivery times were in some cases so long that customers were reluctant to place orders. However, there was little sign of any generalised softening of demand.

Looking ahead, contacts anticipated continued strong growth over the summer months. Full order books would sustain activity in the industrial sector through the summer. Contacts in the services sector also anticipated continued growth, as it was assumed that pandemic-related restrictions would ease further. There was, however, still considerable uncertainty about the outlook, especially for autumn and winter, as this would depend on the future evolution of the pandemic and, in particular, of the Delta and other possible COVID-19 variants.

Contacts’ responses suggested an uptick in employment developments and prospects compared with previous survey rounds. Contacts in employment placement services described strong growth in recruitment activity, with the technology and logistics sectors being among the strongest recruiters. Recruitment for hospitality and leisure was recovering but remained at low levels. After a long period in which changing jobs had been difficult, there was substantial demand for career moves, and several contacts referred to a “war for talent”. The increased use of flexible working arrangements widened the pool of available candidates for some jobs, but penalised companies who needed staff to work on-site. As hotels and shops reopened, recruitment was sometimes difficult, as many former employees had moved to sectors less affected by the pandemic.

Contacts in the industrial sector reported significant increases in selling prices, while price developments in the services sector were more subdued. Commodity prices and transport costs, which had risen very strongly over the past few quarters, were increasingly feeding through to industrial prices. Contacts described a very favourable environment for passing higher costs on to customers, who were focused on securing supplies rather than negotiating prices. Some upstream contacts reported increasing margins, while pass-through tended to be less complete further down the value chain. Looking ahead, most contacts in the industrial sector expected relevant commodity prices to plateau or gradually fall but the pass-through to selling prices to continue for some quarters, and most expected some pass-through to final consumer prices. Contacts in the services sector considered the outlook for selling prices to be more stable.

While industrial input prices were sharply higher, the situation would eventually ease, and the wage outlook remained moderate. Most contacts said that capacity investments would gradually rebalance supply and demand in the industrial sector, so even though unusual cost pressures may persist for a few quarters, they would ultimately be transitory. More persistent longer-term cost pressures would instead come from the regulatory and investment costs required for decarbonisation. Some contacts anticipated a pick-up of wage inflation in the next rounds of wage negotiations given the currently higher consumer prices and recovering business profits in their sectors. However, this pick-up was generally expected to be moderate.

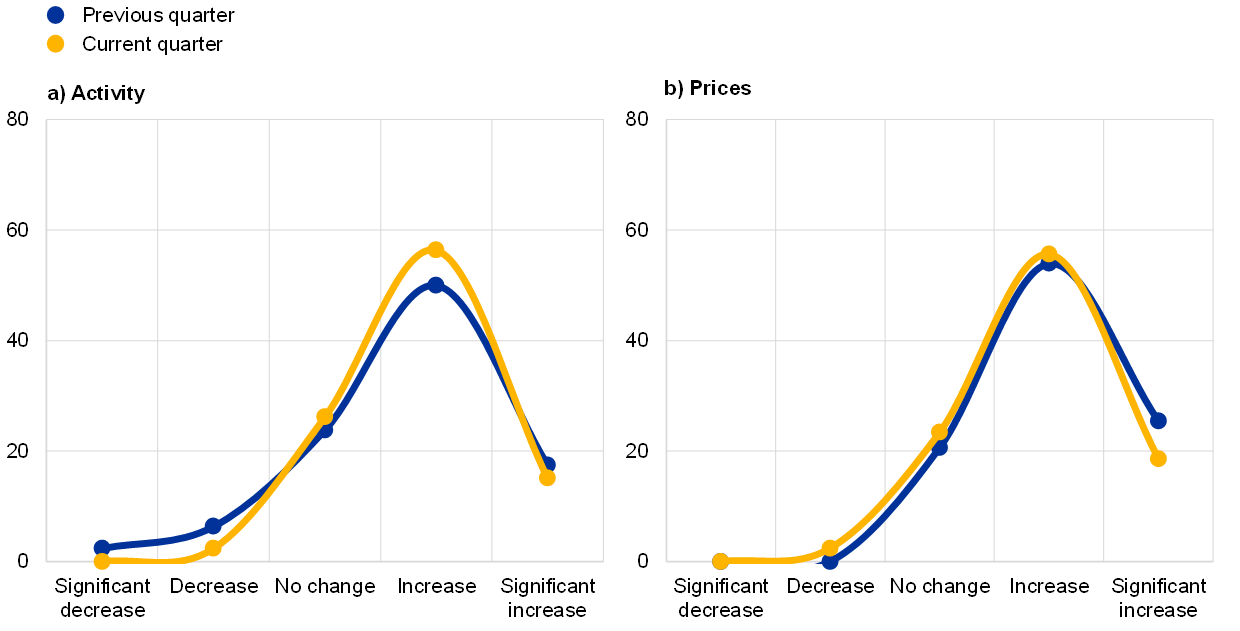

Chart A

Summary of views on developments in and the outlook for activity and prices

(percentage of respondents)

Source: ECB.

Notes: The scores for the previous quarter reflect the ECB staff assessment of what contacts said about developments in activity (sales, production and orders) and prices in the second quarter of 2021. The scores for the current quarter reflect the assessment of what contacts said about the outlook for activity and prices in the third quarter of 2021.

- For further information on the nature and purpose of these contacts, see the article entitled “The ECB’s dialogue with non-financial companies”, Economic Bulletin, Issue 1, ECB, 2021.

- The reopening of outlets led to reported surges in spending, but footfall then tended to settle well below pre-pandemic levels. Therefore, even though customers entering establishments were more likely to spend than before the pandemic, overall sales in shops were still below where they were in 2019.