Macroeconomic impact of financial policy measures and synergies with other policy responses

Published as part of Financial Stability Review, May 2020.

As authorities have sought to soften the impact of the coronavirus pandemic, a key concern has been the potential for the banking sector to ration credit and amplify the economic cost. Euro area real GDP could decrease substantially in 2020. For example, it could be 9 percentage points lower than expected before the pandemic shock, with a rebound in 2021 as confinement policies are reversed (see Chart A).[1]

This initial economic shock could be amplified by the procyclical nature of financial intermediation. In this box, the financial sector’s amplification role is viewed through the lens of a dynamic stochastic general equilibrium model featuring a capital-constrained banking sector.[2] The model is used to assess the impact of financial policy responses aimed at mitigating procyclical effects currently, taking into account interactions with fiscal and monetary policy actions.[3]

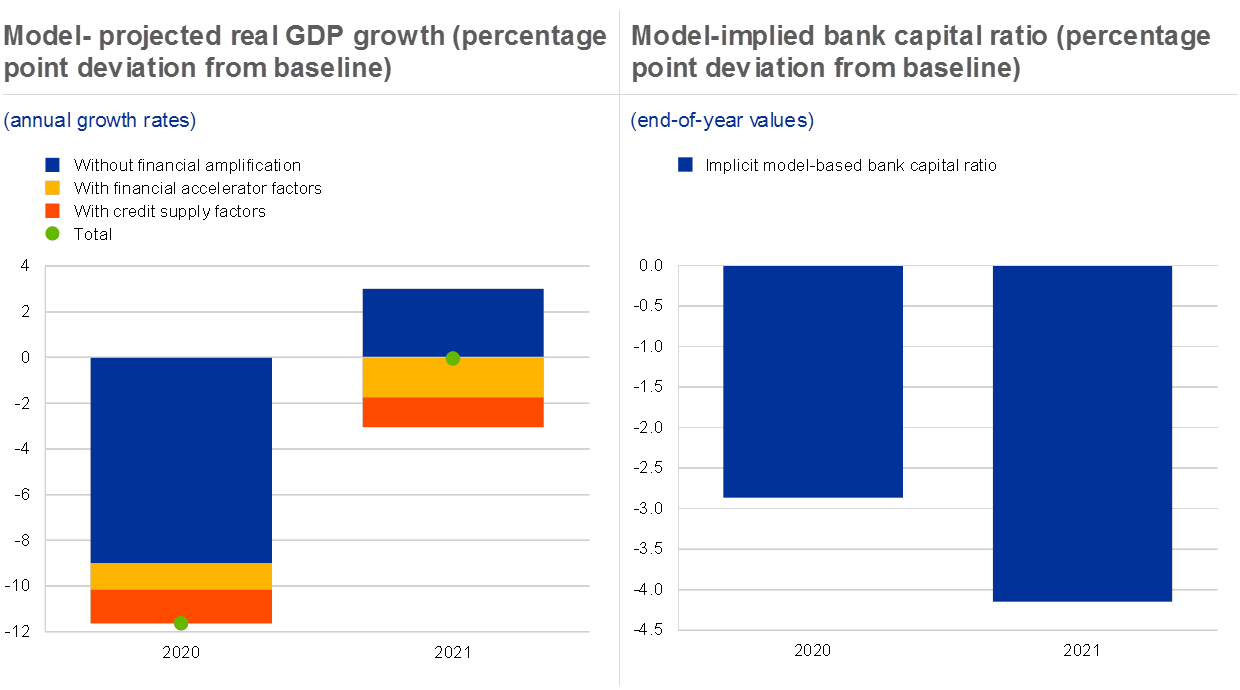

Procyclical financial intermediation effects could amplify the impact of the pandemic on the economy. Non-financial firms and households are now expected to face lower cash and income flows as well as lower collateral values. This could increase the cost of credit and reduce loan demand. According to the model estimates, such financial accelerator effects[4] would subtract another percentage point of GDP in 2020 and increase the size of the recession by an additional 2 percentage points of GDP in 2021 (see Chart A, left panel). Financial accelerator effects in turn imply an increase in loan impairments and rising risk weights, reducing capital ratios and, therefore, banks’ loss-absorption capacity. Within the model, the implicit bank capital ratio would decline by 4 percentage points below its baseline level over two years (see Chart A, right panel).[5] As banks get closer to regulatory constraints, they are anticipated to constrain lending, either by raising lending margins or through outright quantity constraints (see Chart A, left panel).[6] Overall, credit supply effects reduce GDP growth by more than 1 percentage point in 2020-21 on average over two years.

Without policy interventions, the financial sector is likely to induce procyclical effects of the coronavirus pandemic shock

Sources: DKR model, ECB and ECB calculations.Notes: The simulations are conducted assuming unchanged monetary, fiscal and prudential policies. The impact on the bank capital ratio displayed in the right panel is consistent with the magnitude of the financial accelerator effects shown in the left panel.

This impact would be even greater without the large increase in bank capital levels following the 2008 financial crisis which has boosted euro area banks’ loss-absorption capacity. Overall, euro area significant institutions’ Common Equity Tier 1 (CET1) ratio stood at 14.7% on average at the end of 2019. This corresponded to a distance to the minimum capital requirements (i.e. Pillar 1 and Pillar 2 requirements) of around 8% of risk-weighted assets (RWAs) and close to 5% of the combined buffer requirement (CBR; including the capital conservation buffer).

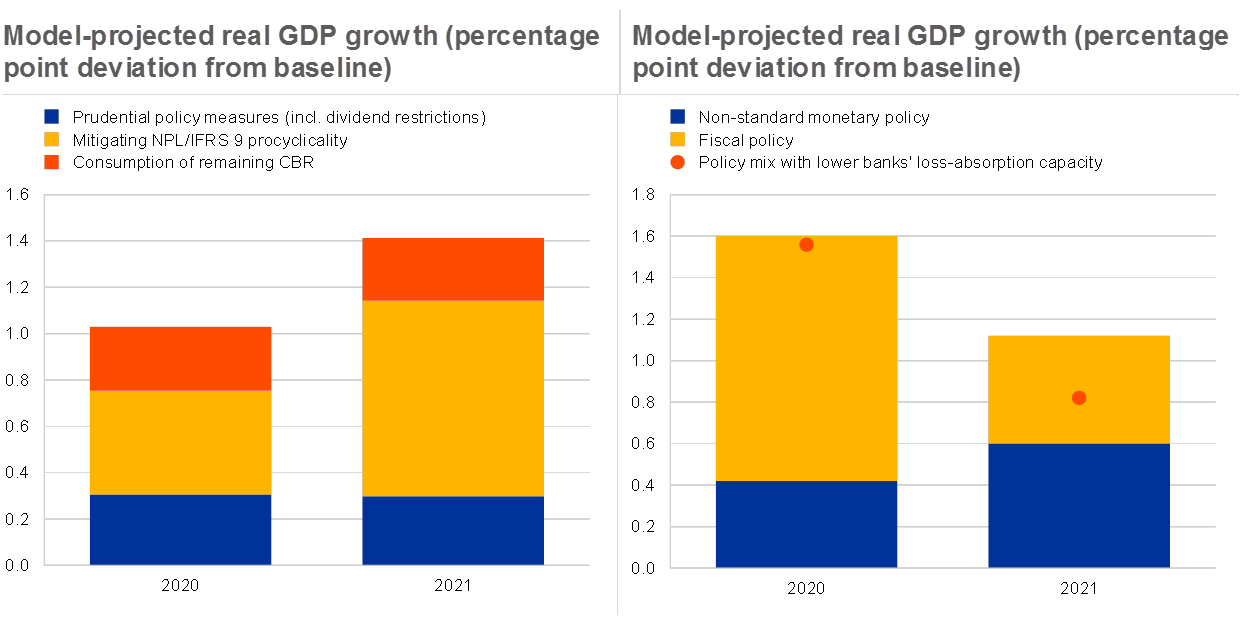

Capital built up over recent years has allowed authorities to now be able to relax constraints and provide room for banks to avoid undue procyclicality. A combination of supervisory capital relief measures and credit risk treatment measures, including the announced releases or reductions of macroprudential buffers and restrictions on dividends, amount to around €170 billion (or almost 2.0% of RWAs).[7] Furthermore, making it easier for banks to consume the remaining CBR could overall amount up to around €330 billion (about 3.5% of RWAs).[8] In addition, supervisors have recommended the use of more flexibility in the application of the IFRS 9 accounting rules with the aim of avoiding procyclical effects on banks’ regulatory capital, which under the macroeconomic scenario shown in Chart A could reduce the CET1 ratio depletion by about 1.5 percentage points in 2020 and 1.8 percentage points in 2021.[9]

The financial policy relief measures would help attenuate the economic impact of the pandemic by reducing procyclicality. Combining the effects of the announced prudential capital relief measures, the measures to retain capital through dividend restrictions and the relaxation of IFRS 9 accounting rules, model-based simulations suggest that the offsetting prudential actions, reducing the likelihood and magnitude of a credit crunch, could restore 1.9 percentage points to real GDP over the two-year horizon, and up to 2.4 percentage points if banks were allowed to draw down the remaining CBR (see Chart B, left panel). An important caveat, however, is that in order to safeguard their credit ratings and funding costs banks may be reluctant to consume their remaining buffers. If so, this would tend to lower the macroeconomic impact of the measures.

Prudential measures relaxing bank capital requirements should help mitigate procyclicality, but monetary policy and in particular fiscal measures are needed to tackle the cyclical downturn

Sources: DKR model, ECB and ECB calculations.Notes: The simulations are conducted assuming the path of the monetary policy interest rate remains at the baseline. The illustrative macroeconomic simulation of ECB non-standard monetary policy measures in the right panel corresponds to central bank asset purchases of €870 billion; this reflects the additional temporary envelope of €120 billion for 2020 assigned to the asset purchase programme (decided on 12 March) and a purchase envelope of €750 billion assigned to the pandemic emergency purchase programme (decided on 18 March). Other non-standard measures enacted prior or in response to the pandemic emergency are not taken into account. The illustrative fiscal policy response in the right panel abstracts from the effect of automatic stabilisers and off-budget items such as State guarantees on loans. The policy mix simulation with lower bank loss-absorption capacity in the right panel evaluates the same fiscal and non-standard monetary policy measures, but assumes tighter bank capital constraints so that banks would resist any temporary decline in net interest income through less accommodative lending policies.

Fiscal and monetary policy measures are the first line of defence against the economic fallout from the coronavirus outbreak. Timely fiscal easing supports households’ and firms’ incomes, while central bank asset purchase and liquidity operations ease financing conditions for all economic agents. For example, the impact of a debt-financed fiscal impulse of 3 percentage points[10] and central bank asset purchases amounting to €870 billion, taking the total purchases to over €1 trillion,[11] could, according to this model, support real GDP by 2.7 percentage points over the two-year horizon (see Chart B, right panel). Note that this fiscal policy response neither includes the effects of automatic stabilisers, nor off-budget measures, such as the various State guarantee schemes and equity injections.

Prudential policy can in parallel reinforce the transmission of fiscal and monetary actions. Without the relief measures described above, banks’ ability or willingness to absorb losses without constraining credit would be significantly lower. With tighter bank capital constraints, the same fiscal and non-standard monetary measures would yield a smaller expansionary effect, notably in 2021 as banks would react to the downward pressures on their net interest income stemming from the central bank asset purchases (see Chart B, right panel).

- [1]This is within the range of alternative scenarios presented in the box entitled “Alternative scenarios for the impact of the COVID-19 pandemic on economic activity in the euro area”, Economic Bulletin, Issue 3, ECB, 2020. In the model-based simulations, the scenario considered here is based on a combination of demand and supply shocks which in the absence of real-financial amplification effects produces a GDP path corresponding to the estimates within the range of these alternative scenarios.

- [2]The DKR model of Darracq et al. (2011) is employed; see Darracq Pariès, M., Kok, C. and Rodriguez Palenzuela, D., “Macroeconomic propagation under different regulatory regimes: Evidence from a DSGE model for the euro area”, International Journal of Central Banking, Vol. 7, December 2011. See also Cozzi, G., Darracq Pariès, M., Karadi, P., Körner, J., Kok, C., Mazelis, F., Nikolov, K., Rancoita, E., Van der Ghote, A. and Weber, J., “Macroprudential policy measures: macroeconomic impact and interaction with monetary policy”, Working Paper Series, No 2376, ECB, February 2020.

- [3]The analysis presented in this box does not account for the macroeconomic costs of unwinding the fiscal, monetary and prudential policy measures later.

- [4]See Bernanke, B., Gertler, M. and Gilchrist, S., “The financial accelerator in a quantitative business cycle framework”, Handbook of Macroeconomics, 1999.

- [5]The model-implied capital gap should not be confused with bank-level stress-test calculations, but is in line with credit losses and net interest income projections using ECB top-down stress-test models.

- [6]Within the confines of the model, impairments of bank assets and bank funding constraints generate substantial capital shortfalls, to which banks react by tightening lending conditions.

- [7]See “ECB Banking Supervision provides further flexibility to banks in reaction to coronavirus”, ECB Banking Supervision, press release, 20 March 2020.

- [8]This figure does not take into account the leverage ratio which comes into force in the EU in June 2021.

- [9]These numbers include: (i) the additional provisions under IFRS 9 with respect to IAS 39 in stress with respect to normal times; and (ii) the estimated impact on provisions of including flexibility in the classification of the exposures potentially falling under debt restructuring (e.g. public moratoria schemes). It is assumed that the implemented policies would be able to absorb the full procyclical impact of IFRS 9. IFRS 9 adds back to the CET1 ratio, but would not increase the loss-absorption capacity. Thus, the increase in the loss-absorption capacity would be less than the reduction in capital depletion.

- [10]The fiscal measures are illustrative of part of the government responses to the pandemic emergency; see the “Report on the comprehensive economic policy response to the COVID-19 pandemic”, Eurogroup, 9 April 2020. In the model, it is assumed that the fiscal measures consist of government consumption and transfers to liquidity-constrained households and firms, and are sustained over two years.

- [11]This package is indicative of part of the ECB’s response to the pandemic emergency, namely the asset purchases announced by the ECB since the 12 March 2020 Governing Council meeting (other interventions related to liquidity operations or collateral easing measures are not considered in the simulation). To simulate the impact of non-standard measures, the DKR model has been augmented with relevant frictions as in Darracq Pariès, M., Körner, J. and Papadopoulou, N., “Empowering central bank asset purchases: The role of financial policies”, Working Paper Series, No 2237, ECB, February 2019.