Maintaining price stability with unconventional monetary policy measures

Speech by Peter Praet, Member of the Executive Board of the ECB, at the SUERF Conference, New York, 11 October 2017

*The text of this speech is broadly the same as my remarks at the MMF Monetary and Financial Policy Conference, in London, on 2 October 2017*

The euro area continues to experience a solid, broad-based and resilient recovery. Deflationary risks have disappeared and some measures of underlying inflation have ticked up over recent months. But overall inflation developments, despite the solid growth, have remained subdued.

Accordingly, while we remain confident that inflation developments will eventually return to levels below, but close to, 2%, our medium-term objective, the evidence still shows insufficient progress towards a sustained adjustment in the path of inflation towards those levels. Such “sustained adjustment” is the principal contingency that has guided and will be guiding the introduction and withdrawal of our asset purchase programme (APP) and, indirectly, of all the main components of our present policy.

In my remarks today, I would like to outline the central role monetary policy plays in underpinning this recovery and to discuss the main mechanisms by which our measures have impacted on the economy. I will start from a brief overview of the monetary policy toolkit that the Governing Council has adopted over the last years, and I will sketch out the elements that are most relevant for the Governing Council’s deliberations about the calibration of our policy measures. I will then highlight the key channels by which this toolkit transmits to financial conditions. Finally, I will focus on the impact channels of the APP, which plays a central role among the policy instruments.

The ECB’s monetary policy toolkit

Over the last three years, the Governing Council has had to take bold measures to maintain price stability. The context in which we launched this package of measures, in June 2014, was one in which a sustained period of disinflation could have morphed into one of outright deflation. The Governing Council had to move beyond its conventional policy instruments and instead deploy a set of unconventional tools that were tailored to the specific challenges of that time. The first challenge related to the effective lower bound on interest rates. The leeway to cut policy-controlled short-term interest rates was insufficient to provide the degree of accommodation that was necessary to support the economy and fight off the threats to our objective. The second challenge related to a dysfunctional monetary transmission. Bank intermediation was significantly impaired, which had caused the transmission of policy stimulus to the broader economy to be too slow and uncertain.

The unconventional tools were designed to act both on the quasi-risk-free yield curve and on bank lending margins. By “yield curve” I mean the term structure that we observe in the money market for overnight indexed interest rate swaps (OIS), as well as the curves in the markets for the national sovereign debts, which traditionally constitute an important benchmark for pricing credit to the entire economy. Due to this benchmark function, the level and shape of the yield curve are crucial determinants of prices of a whole range of longer-term financial assets, including those most closely tied to economic activity, such as bank lending rates, corporate bonds and mortgages. Our policy to influence intermediate and long-term yields has been instrumental in bringing the whole structure of credit conditions for households and companies to the accommodative levels necessary to arrest disinflation and strengthen the recovery.

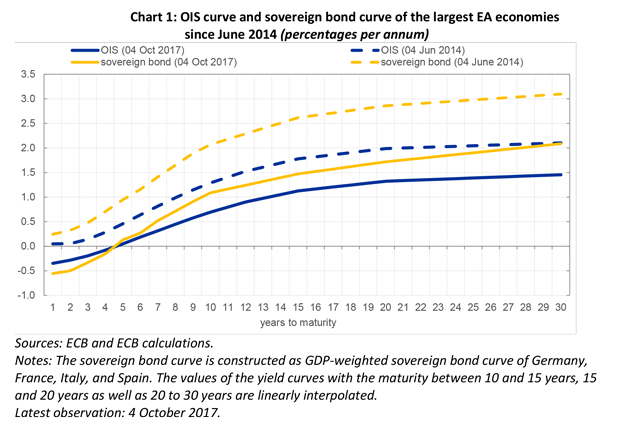

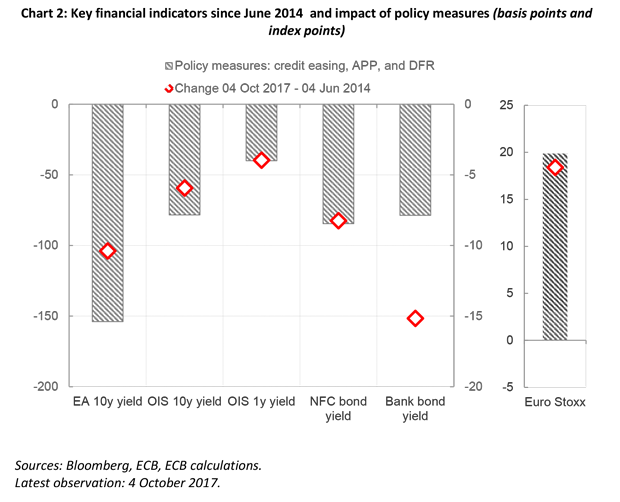

By now, the OIS curve at maturities of ten years and above is more than half a percentage point below the levels observed before the initiation of our measures in June 2014 (Chart 1). For sovereign yields, the drop over this period was even more pronounced, amounting to around one percentage point for maturities at or above ten years. While financial market developments over this time period were also impacted by a host of other factors that go beyond ECB monetary policy, empirical analysis indeed ascribes the bulk of the decline in longer-term yields to our measures.[1] Moreover, it indicates that the monetary impulse has transmitted not only to money-market and sovereign yield curves, but also to an array of other market segments, including financial and non-financial corporate bonds, as well as equity markets (Chart 2).

As a complement to the impact of our measures on yield curves, our targeted longer-term refinancing operations (“TLTROs”) were specifically designed to compress bank lending rates – a key intermediate objective of the policy toolkit, given the important role that bank credit plays in financing the euro area economy. Through a number of mechanisms, the TLTROs have successfully bid down the level of bank lending rates on loans to households and companies, while preserving banks’ overall margins.[2]

For instance, the cost of borrowing for non-financial corporations, at the euro area average, are now more than one percentage point lower than before the first TLTROs were adopted in June 2014 (Chart 3). What is more, the introduction of the TLTROs was followed by a steep intra-euro area convergence in bank lending rates. That is: countries in which the economic recovery had previously been lagging behind the euro area average benefitted from particularly strong declines in bank lending rates.

This toolkit has formed the backbone of ECB monetary policy for almost three years, which initiated a pronounced expansion of our balance sheet (Chart 4). At the same time, the package had to be adjusted at times in response to the evolving situation. In particular, such adjustments became necessary to counteract the sequence of external shocks that, between summer 2015 and summer 2016, have created headwinds for the euro area economy, thereby slowing down the firming of its recovery.

Moreover, in March 2016, the Governing Council also reactivated the TLTROs to prevent the market turmoil that prevailed at the start of 2016 from undermining the progress that had previously materialised with regard to bank intermediation. As bank lending conditions normalised subsequently at a relatively quick pace, the planned TLTROs were let to run their course. While credit drawn by banks under this facility will be outstanding for the next three to four years, the facility itself is not an active instrument today.

As a consequence, while all the instruments – including indeed the credit extended to banks under the previous TLTROs – interact to determine the stance prevailing today, the main source of easing at present comes from the interaction between the APP, the moderately negative short-term interest rate and the forward guidance on both these policy tools.

Our forward guidance clarifies the relationship between our two main instruments. It sets the conditionality that governs them and the sequencing of their phasing out. It also provides information about their expected life. With the last DFR reduction in March 2016, the APP became the margin along which the Governing Council can still ease policy to a meaningful degree if needed. Keeping policy rates at their present level for the entire life of the APP is an enabling condition for the purchases to exert their full impact. This is why we have coordinated the guidance about our key interest rates and our asset purchases very carefully and, since March 2016, we have consistently communicated that our key policy rates are expected “to remain at their present levels for an extended period of time, and well past the horizon of our net asset purchases.”

The appropriate calibration of this set of instruments is of course always a highly complex exercise and requires a broad range of analytical inputs and policy judgement. It works backward: from a desired medium term inflation outlook – one which is most consistent with the objective and with its numerical clarification that the Governing Council announced in May 2003 – to the broad financing conditions that can support that outlook, to the calibration of the Governing Council’s instruments that can foster those financing conditions. Concretely, these exercises start from the Governing Council’s assessment of the prospects for inflation to return to levels that are close to 2% by a meaningful time frame and with a reasonable degree of confidence. If the prospects for achieving that desired outcome are too weak, the Governing Council will form a view on the degree of accommodation that is necessary to make that outcome less uncertain. Working backwards, this exercise is designed to promote the level and shape of the yield curve that, according to past regularities, can be expected to deliver the requisite amount of stimulus, taking into account the endogenous adjustment of the whole spectrum of market conditions – including bank lending rates, corporate bonds, mortgages, as well as the foreign exchange rate – to the yield curve.

But the decision process is never mechanical. All along, the Governing Council combines the indications coming from models and past empirical regularities with its own judgement. In engaging in this layer of judgemental deliberations, our intent is to come to a firm assessment of the balance between the likely efficacy of our measures and their potential costs in term of financial distortions.

How do our main policy instruments work?

Ensuring an appropriate interest rate environment throughout the yield curve is instrumental in fostering the financing conditions that are most conducive to our objective. A central bank can seek to influence the level and shape of the yield curve by acting on two components of the long-term interest rates: the expectations component and the term premium. The expectations component reflects market expectations of the future path of the policy-controlled short-term interest rates. All else equal, a path that is lower and shallower tends to produce a lower level of long-term yields and a flatter curve. The term premium reflects the excess return that an investor demands as a compensation for holding a bond with a long, say ten-year, residual maturity relative to rolling over a short-term bill for ten years. Locking themselves into a long-dated fixed income investment for a period of time is not equivalent to rolling over a short-term investment for the same period, because holding a long-dated bond exposes the investor to the risk that interest rates may increase unexpectedly during the holding period. An unexpected increase in interest rates causes a loss on the portfolio. So, the term premium – the excess return – is typically positive: it compensates investors for taking on such interest rate (or duration) risk.

How does the interplay between the APP and our short-term interest rate policy enter this simple logic? Suppose the level and shape of the yield curve prevailing at a given point in time is judged to be inconsistent with a set of financing conditions that are sufficiently accommodative to foster a return of inflation to levels below, but close to, 2% over the medium term. How could the two main instruments of current policy be deployed to change this state of affairs in an environment in which the short-term interest rate cannot be lowered meaningfully?

Simplifying a great deal, one could say that the forward guidance on short-term interest rates – our stated expectation that the ECB’s key interest rates will remain “at their present levels for an extended period of time” – should be calibrated in a way to anchor the short-to-medium maturities of the yield curve – those portions most sensitive to short-term interest rate expectations and, therefore, to forward guidance – around levels that are sufficiently steady and low. In this respect, a mildly negative DFR has proved to be particularly powerful in controlling and anchoring these maturities, which are key to pricing bank credit in the euro area. The notion that zero was not the effective lower bound has exerted additional flattening pressure on the short-to-intermediate maturities of the yield curve, those to which banks tend to index loans with adjustable interest rates. This has amplified the reach-out potential of the stimulus relative to a situation in which our policy rates had been reduced to levels no lower than zero.[3] Consistent with this mechanism, the OIS forward curve underwent a striking downward shift and flattening, once we launched our monetary policy package in mid-2014, especially in the short-to-medium segment of the curve, which is arguably most indicative of investors’ short-term rate expectations (Chart 5).

The APP applies further pressure on longer-term interest rates along the curve, mainly by compressing the term premium. This is supported, for instance, by decompositions of long-term interest rates based on term-structure models indicating that the downward impact in the run-up to and around the announcement of APP mainly reflected a compression of term premia (Chart 6). How does the APP influence the term premium? The APP extracts duration risk from the market. Markets see duration risk as a potential source of portfolio losses, so they want to hedge against it, and the compensation for hedging is precisely what we call the term premium. If this premium is high, it makes long-term borrowing more expensive than short-term borrowing. If, at times of disinflation and weak growth, long-term borrowing is to be made more affordable so as to promote investment and durable consumption, then the central bank can try to absorb part of the duration risk that otherwise would have to be held by private investors. This can be done by purchasing long-dated bonds, as the ECB did under its APP. With less long-dated bonds to hold in the aggregate, private investors have more balance sheet capacity to hedge against the amount of duration risk that remains in the market, and more risk-bearing power to re-deploy funds to other investments, including the financing of productive capital. As a consequence, the desired compensation for hedging decreases, which drives down the term premium and the whole yield curve. This same mechanism spurs propagation. Duration extraction is the catalyst for the portfolio rebalancing channel, which is the chief mechanism by which easing through quantitative interventions propagates through the entire economy.

In practice, distinguishing between the effects of the APP and of forward guidance on the two components of long-term interest rates is less straightforward. The credibility of promises to follow a certain course of action for setting the policy rates in the future is almost certainly enhanced by the asset purchase programmes today, as these purchases are a concrete demonstration of a desire to provide additional stimulus. In other words, there is a signalling channel inherent in asset purchases, which reinforces the credibility of the forward guidance on policy rates via the expectations channel. Conversely, forward guidance may affect the term premium component of longer-term yields by reducing the uncertainty about the future path of short-term interest rates and thereby reducing duration risk in the market. Accordingly, the net stimulus provided by asset purchases depends in part on expectations of how policymakers will adjust short-term interest rates in the future.

But these additional complexities do not alter, and in fact reinforce, the key insight – namely that the different policy tools must be seen as mutually complementary elements of a package. The sequencing between policy tools, as we have described it in our forward guidance since March 2016, with rates expected “to remain at their present levels for an extended period of time, and well past the horizon of our net asset purchases”, is motivated by this insight.

For example: letting the expectations component of longer-term yields float upwards while, at the same time, engaging in asset purchases would be an inefficient conduct of policy. The compression of yields through the asset purchases would be directly countered by an upward drift in the expectations component. By contrast, the established sequencing helps anchor the expectations component and thereby allows the APP to exert its full effect.

Calibrating APP

While fostering the appropriate interest rate environment is a critical intermediate condition enabling the transmission of our policies, in the end we do not directly control the yield curve. We can influence the yield curve only indirectly, through forward guidance and, notably, via modulating the size and intensity of our asset purchases. This process is mediated and to some extent difficult to forecast: we change our instruments and let markets determine the asset price implications of our actions. But, importantly, this process preserves the ability of markets to express views about the creditworthiness of the financial assets that are to be priced. Indeed the last year has demonstrated that, despite the ECB’s forward guidance on short-term interest rates and its continuing presence in the market as a large investor, market prices have tended to reflect investors’ evolving views about the prospective standing of sovereign issuers’ credit.

With this in mind, let me turn now to the challenge of calibrating the size and duration of purchases that can deliver that yield constellation and, indirectly, the set of financing conditions consistent with our objective. For this, we rely on the current theory and empirics of quantitative interventions by central banks. The theory available today stipulates that it is primarily by announcing that the central bank will withdraw a certain stock of long-term bonds at a certain horizon, and thus a share of duration risk that otherwise would have to be borne by the market, that an asset purchase programme can impact on the term premium and on the yield curve in general.

It is important to emphasise that it is the amount of duration that we extract relative to the amount of duration that otherwise would be in the market that produces the impact. In this respect, keeping the size of the APP portfolio constant at a certain nominal level does not necessarily safeguard a given amount of accommodation. By keeping the portfolio of assets acquired under the APP constant in nominal terms, it is difficult to prevent the ageing of the portfolio, i.e. its gradual loss of duration as the securities held in the portfolio mature. Although re-investments of the proceeds from principal payments of the maturing securities can, to a certain extent, offset this endogenous decay of the average portfolio duration – by replacing short-term expiring securities with the purchase of longer-term securities – this substitution effect is generally not strong enough to maintain the average maturity of the portfolio relative to that of the market portfolio at a level consistent with a desired yield curve. In addition, of course, the amount of duration that is supplied to the market by public and private issuers is not constant and indeed typically trends up. Thus, keeping the central bank portfolio steady at a certain nominal level means that, in relative terms, the fraction of duration risk that is withdrawn from the market tends to fall. As time passes, the endogenous loss of duration in the central bank portfolio is bound to exert increasing upward pressure on the term premium.

When the Governing Council will eventually judge that a sustained adjustment is likely to be completed within a medium term horizon with a sufficiently high degree of confidence, this endogenous process will act as a self-correction mechanism. In those conditions, the higher expected returns on business investment will make borrowing conditions still attractive even as nominal borrowing costs will tend to rise. From today’s point of view, we are still some distance away from a sustained adjustment. As we concluded at our last monetary policy meeting, a very substantial degree of monetary accommodation is still needed for underlying inflation pressures to gradually build up and support headline inflation developments in the medium term.

Before drawing to a close, let me address one additional issue related to the calibration of the APP, namely the horizon for executing the purchases.

We have traditionally communicated our (re-)calibrations of the APP in terms of two parameters: the pace of monthly purchases and an intentional end date, which is however always conditional on a sustained adjustment. The two parameters have facilitated market participants’ calculus of the extra stimulus implied by each of our successive rounds of (re-)calibrations: by multiplying pace by the horizon, markets have been able to identify the size of the portfolio which is relevant for pricing the term premium. What we have seen is that, if confronted with a higher monthly pace in exchange for a shorter intentional horizon or, conversely, a lower pace in exchange for a longer intentional horizon, the reaction in the markets has been varying through time. In more tense market conditions, a higher purchase pace in the near term is generally seen as having a higher easing potential. Probably, in conditions in which uncertainty is high, frontloading the accumulation of a given stock of purchases more forcefully signals the central bank’s commitment to inject the degree of accommodation necessary to support the recovery. By contrast, in more normal market conditions, the market’s capacity to engage in intertemporal arbitrage improves. Consequently, investors may become “more patient”, or, in other words, better able to evaluate the stimulus that can be expected to come from a purchase plan that is to be executed over a more extended time interval.

Conclusion

While the euro area recovery remains solid, broad-based and resilient, the economy has yet to make sufficient progress towards a sustained adjustment in the path of inflation to levels that are consistent with the Governing Council’s aim. To support such sustained adjustment, the ECB has resorted to a package of complementary policy measures and recalibrated this package at various occasions in line with the evolving macroeconomic conditions, most notably the outlook for price stability, and the state of monetary policy transmission. In the next few weeks, the Governing Council will again assess how all these factors can be expected to influence the monetary policy stance and will re-calibrate its instruments accordingly, with a view to delivering the monetary policy impulse that is still necessary to secure a sustained adjustment in the path of inflation in a way that is consistent with our monetary policy aim.

[1] See ECB Economic Bulletin, Issue 2 / 2017 – Box 3: Impact of the ECB’s non-standard measures on financing conditions: taking stock of recent evidence.

[2] For additional detail, see my remarks at the Belgian Financial Forum colloquium on “The low interest rate environment”, in Brussels, on 4 May 2017.

[3] For further detail on this mechanism, see my speeches at The ECB and Its Watchers XVIII Conference in Frankfurt am Main, on 6 April 2017; as well as my remarks at the Fixed Income Market Colloquium in Rome on 4 July 2017.

Ευρωπαϊκή Κεντρική Τράπεζα

Γενική Διεύθυνση Επικοινωνίας

- Sonnemannstrasse 20

- 60314 Frankfurt am Main, Germany

- +49 69 1344 7455

- media@ecb.europa.eu

Η αναπαραγωγή επιτρέπεται εφόσον γίνεται αναφορά στην πηγή.

Εκπρόσωποι Τύπου