Could monetary policy have helped prevent the financial crisis?

Speech by Lorenzo Bini Smaghi, Member of the Executive Board of the ECBWorkshop on “Monetary policy: Recent experience and future directions”Bank of Canada, Toronto 9 April 2010

Introduction [1]

There is a broad consensus that the financial crisis has been caused by several factors, such as: failures in financial regulation and supervision; structural changes in the financial sector, including the increased importance of the shadow banking system and securitisation; and global macro-economic imbalances. These factors, together with widespread financial market integration, which in turn creates greater scope for contagion, have been particularly relevant even in countries where credit growth was relatively contained and real estate did not experience a boom.

There is much less consensus on whether monetary policy could have helped prevent the financial crisis, or, more provocatively, on whether errant monetary policy caused the financial crisis. These are uncomfortable questions for central bankers – but ones we cannot avoid. Only by confronting such challenges honestly can we hope to understand the crisis, and thereby guard against its repetition.

Some take the view that monetary policy played, at most, only a marginal role. In this account, failures of financial regulation and supervision – rather than of monetary policy – lay at the heart of the crisis. [2] Yet an influential body of opinion takes an opposing line, claiming that an overly accommodative monetary policy – at the global level, and perhaps especially in the United States – was among the key causes of the crisis. [3] Its advocates argue that short-term interest rates were kept “too low for too long” following the bursting of the dot-com bubble at the turn of the century, and led to the economic imbalances that ultimately threatened the financial and macroeconomic stability of the world economy.

The truth probably lies somewhere between these two extremes. No doubt financial regulation and supervision were weak. No doubt price stability is necessary but insufficient per se to achieve financial stability. Yet there is also no doubt that a monetary policy which turns out to be too lax to achieve price stability is likely to be responsible for fuelling excessive credit growth and thereby creating the potential for financial instability. There is substantial literature explaining this relationship, on which I will not elaborate further. [4]

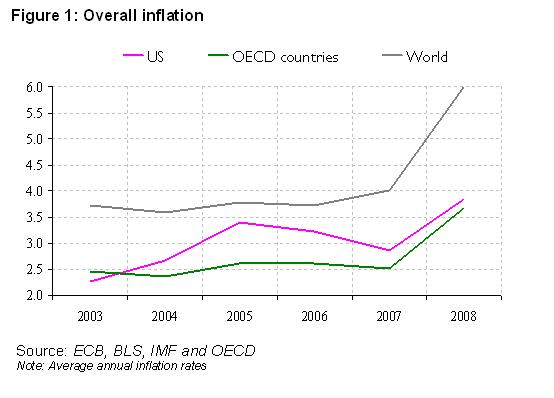

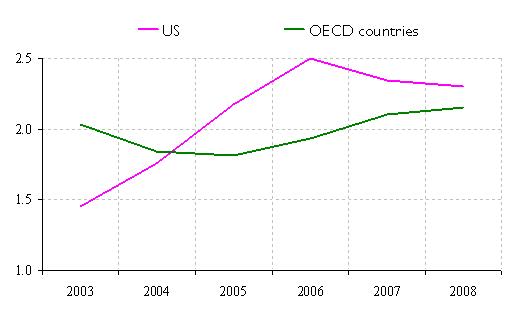

Upside threats to price stability were certainly emerging prior to the crisis, on the back of surging commodity prices and strong global growth. Let’s not forget, for example, that US headline inflation increased from 2.3% on average in 2003 to 3.2% in 2006 and 3.8% in 2008 (See figure 1). Core inflation increased from 1.5% in 2003 to 2.5% in 2006 and 2.3% in 2008 (See fig. 2). Euro area annual inflation reached 3.3% on average in 2008. [5] To contain these upside risks to price stability, a case can be made that interest rates should have been higher than was the case before the crisis.

Central to a honest self-evaluation of the role played by monetary policy is our adoption of a “real-time” perspective. The benefits of hindsight are enormous – but also potentially misleading. If we had known ahead of time that Lehman Brothers would fail in September 2008, we would no doubt have taken different policy decisions in the preceding months. But such considerations are not a meaningful guide to future policy. By their nature, economic “shocks” cannot be foreseen.

Taking these aspects into account, it would be a mistake to think that the way monetary policy was conducted did not play any role in the outbreak of the financial crisis. Monetary policy can actually be considered one of the factors that, in some countries, contributed to the crisis, at least to the extent that it was too accommodative to maintain price stability. The overly loose global monetary policy may have weakened the anchoring of price stability and at the same time unleashed a wave of euphoria and excessive risk-taking in the financial sector.

It would be a waste if this financial crisis did not give us the opportunity to think deeply about the framework for monetary policy-making – the objective of policy; the models underpinning our analysis; and the indicators on which we focus when taking policy decisions. Even if excessively loose monetary policy is only partly to blame for the financial crisis, a case can be made that it fuelled the accumulation of financial imbalances that underlay the crisis. This prompts us to ask: what were the flaws in the decision-making that resulted in – according to some observers – policy errors? And, more importantly, how can we correct these flaws – and avoid any repetition – in the future?

Since the seminal contribution of Theil, [6] policy-making has been characterised as a “control problem”. Such a characterisation embodies three elements: clearly defining the policy objectives; articulating a model of the economy by which policy instrument settings and economic shocks are mapped into outcomes; and defining the information structure facing policy-makers. This last element determines the extent to which they can identify shocks and structural changes in real time.

Using this approach as an organising framework, we can re-phrase our question: if central banks made mistakes in the run-up to the financial crisis, was this because they had the wrong objectives? Or used the wrong model? Or misread the conjunctural situation? Or were the errors a result of the combination of these three factors?

1. The objective of monetary policy

A large body of academic literature, stemming from the insights of Friedman and Phelps, provides the theoretical basis for establishing price stability as the objective of monetary policy. Such an approach found overwhelming empirical support in our experience of the Great Inflation during the 1970s. It has reached its apogee in the modern benchmark macroeconomic model, which articulates – on a state-of-the-art, micro-founded basis – the welfare costs of deviations from price stability. [7]

Such thinking had an important bearing on the design of the institutional framework for Monetary Union in Europe. The ECB has been assigned the primary objective of maintaining price stability in the euro area, establishing a clear hierarchy of goals with price stability at the fore. The clarity of this objective bolsters the credibility of the single monetary policy: it supports the institutional independence of the ECB and helps to stabilise private longer-term inflation expectations at levels consistent with price stability.

At some other central banks, monetary policy has been given a dual mandate, with objectives such as economic activity, employment, financing conditions or financial stability in addition to the goal of price stability. I do not want to give the impression that we are indifferent to such concerns at the ECB: on the contrary, I will discuss in a moment how we can help to attain them. But monetary policy should not be over-burdened with additional objectives. It is too blunt an instrument to be effective in achieving all the goals I have just listed.

For example, a central bank with a dual mandate to maintain price stability and support employment faces a particular dilemma in the context of a so-called “jobless recovery.” Its ability to act in a timely manner to contain emerging inflationary risks may be curtailed by its obligation to support employment. Moreover, since labour market developments are lagging indicators of the cycle, a central bank assigned an explicit employment objective may systematically tighten monetary policy later and more cautiously than necessary to maintain price stability. Such behaviour could impart an “inflation bias” to the economy.

These factors run counter to recent proposals to assign monetary policy additional financial stability objectives. [8] Rather, maintaining price stability over the medium term – an important addendum, to which I will return – is the appropriate objective of monetary policy. Given its neutrality over the longer run, monetary policy’s ability to pursue other objectives at that horizon is heavily circumscribed. And by maintaining price stability, monetary policy creates an environment conducive to financial stability, economic growth and employment creation.

If price stability is the appropriate objective of monetary policy, how should it be quantified? At the ECB, we have defined price stability as annual consumer price inflation of “below, but close to, 2%”. Whether explicit or implicit, similar targets have been established by central banks throughout the world.

Recently, proposals have been made to raise inflation objectives substantially – more than doubling them in the euro area case. [9] Frankly, these proposals are foolhardy. Any shift in inflation objectives at times of economic stress invites the charge of opportunism: if you are willing to raise inflation objectives from 2% to 4%, then why not 6% or 10%? Such thinking puts at risk the hard-won credibility of the existing monetary policy frameworks. To the extent such shifts are motivated on public finance grounds, they suggest that monetary policy is subordinate to fiscal concerns. And concerns about deflation risks should be addressed by refining the conduct of monetary policy, rather than redefining its objective.

In particular, it is crucial that the objective of price stability is pursued symmetrically. Of course, asymmetries may exist in the structure of the economy. Examples include: any lower bound on nominal interest rates; and an aversion to falls in nominal wages. These need to be taken into account in policy making. But this does not imply that monetary policy should demonstrate greater aversion to deflation rather than inflation (or vice versa) An excessive and asymmetric fear of deflation explains in part why interest rates may have been kept “too low for too long” prior to the financial crisis. Pursuing price stability in a symmetric manner would guard against the danger of repeating this mistake.

To sum up, I believe that the recent financial crisis has not challenged the principle according to which the goal of monetary policy should be price stability. In practice, this is recognised by most leading central banks. At the ECB, we are fortunate that the primacy of price stability has been made explicit.

With this in mind, it is difficult to attribute any pre-crisis “policy error” to the pursuit of the wrong monetary policy objective. Nonetheless, we are already witnessing the emergence of siren calls to change the objective – in particular, for monetary policy to target a higher steady-state inflation rate, difficult to reconcile with price stability. These calls must be resisted.

Emphasising the primacy of price stability objective over the medium term does not imply central bankers should be, in the words of Mervyn King, “inflation nutters”. [10] Using Theil’s framework to characterise the monetary policy problem also helps to clarify its dynamic nature. Recognising the long and variable lags in the transmission of monetary policy and the inevitability of short-term shocks to price dynamics, policy-makers need to adopt a medium-term orientation in their decisions. Attempts to fine-tune price developments on a short-term basis are doomed to failure. Such attempts are likely to impart an excessive activism to policy-making, such that interest rate decisions add volatility to the economy rather than stabilise it.

In adopting an appropriate medium-term orientation, monetary policy-makers are accorded an extra “degree of freedom” in setting the policy stance. There can be several paths of interest rates consistent with the maintenance of price stability over the longer run. At least in principle, the choice of a specific path can be used to support broader purposes, without prejudicing the outlook for price stability over the medium term. This has been recognised by the so-called flexible inflation targeting literature. [11] This framework explicitly foresees the use of monetary policy to smooth developments in economic activity over the business cycle, while anchoring longer-term inflation expectations at levels consistent with price stability.

In principle, the flexibility accorded to policy-makers by the medium-term orientation of monetary policy could be used in other directions, such as to contain financial imbalances or limit asset price volatility. The feasibility and desirability of such alternative approaches rests crucially on how monetary policy actions are perceived to be transmitted to the economy in general, and the price level in particular – in other words, on the perception of the structure of the economy and the monetary policy transmission mechanism.

2. The monetary policy transmission mechanism

The desirability of flexible inflation targeting was established using the canonical New Keynesian model. In its simplest version, welfare is maximised by fully stabilising inflation at its target level, a policy which simultaneously delivers a zero output gap. [12] This so-called “divine coincidence” [13] implies that policy-makers who care only about stabilising inflation will deliver an efficient path of economic activity. And, symmetrically, policy-makers who focus solely on keeping output at an (appropriately defined) potential level will deliver low and stable inflation rates. A relatively simple Taylor-like monetary policy rule could achieve these desirable outcomes. In this benign world, traditional monetary policy trade-offs appear to have disappeared!

It is widely recognised that even modest deviations from the simplest version of the canonical model introduce caveats to these very strong conclusions. But the underlying message of these models remains: a policy aimed at stabilising inflation and the output gap at a horizon around two years ahead is both desirable on welfare grounds and consistent with price stability over the medium term.

Given our experience over the past few years, these strong conclusions are now rightly treated with scepticism. With the benefit of hindsight, it is apparent they served to breed complacency among both policy-makers and market participants, resulting in over-confidence in the ability of macro policies to stabilise the economy. Such complacency contributed to both poor policy choices and destabilising private sector behaviour. Such decisions may help to explain the emergence of financial crises in recent years.

Critiques of the benchmark New Keynesian model are legion. [14] I will not repeat them here. Suffice to note that an important weakness of these models was the absence of a financial sector. As a consequence, the financial intermediaries, financial frictions and asset price bubbles and corrections that have played a key role in the events of the past three years were neglected.

To illustrate, imagine a scenario where inflation falls because of a positive supply shock, such as a reduction in manufacturing import prices from Emerging market economies. An inflation-targeting central bank would decrease its policy rates to boost inflation back towards its target level, simultaneously raising output closer to its new (temporarily higher) potential level. In this scenario, financial market participants would experience both stronger economic growth and lower interest rates, all in an environment of benign price developments. The question arises of whether such circumstances can prompt financial market participants to assume a euphoric state: to take on more risk; to expand balance sheets more rapidly; to increase leverage; and to bid up asset prices. Such developments – by construction neglected in the benchmark model lacking a financial sector – may have a macroeconomic impact and, ultimately, undesirable consequences for both financial and price stability.

Why should low interest rates in these circumstances induce such euphoria in the financial sector? And what implications can it have for credit conditions and the transmission of monetary policy?

Recent experience suggests that the monetary policy stance may affect the confidence – and thus the risk-taking behaviour – of financial institutions, in particular of banks. [15] Since bank loans are illiquid assets, liquidation is costly. When liquidity is tight, banks curtail their accumulation of illiquid assets, notably by constraining credit supply. However, if the central bank stands ready to lower interest rates when the financial system needs liquidity, financial institutions may be induced to accumulate illiquid and riskier assets on their balance sheets, given the implicit insurance provided by monetary policy. [16] Low policy interest rates may also promote a “search for yield,” as investors seek to maintain their nominal rate of return at historical levels, even as short risk-free rates decline. As interest rates fall, intermediaries take on greater risk so as to meet this demand for returns.

Similar institutions will adopt a similar risk-taking strategy. Herding will emerge. Risk management behaviour will become more correlated across financial intermediaries. Risk will rise not only at the individual bank level, but also across the system as a whole. [17]

Moreover, since the financial sector is now exposed to greater liquidity risk as a result of such behaviour, central banks are more likely to be called upon to intervene in the future. And the magnitude of such interventions will need to increase if they are to be effective. A “ratcheting-up” of risk within the banking sector can occur over time, creating increasing vulnerability. [18]

Low interest rates also encourage a higher level of leverage. Because financial intermediaries – whether banks, broker-dealers, shadow banks, or hedge funds – finance themselves with short-term liabilities, central bank decisions on the level of short-term rate affect their marginal price of leverage. As a result, the behaviour of financial intermediaries – which, by their nature, have high levels of leverage – can be strongly influenced by even small changes in short-term rates. [19] Low levels of interest rates encourage higher levels of leverage and, as a result, an accumulation of additional risk on bank balance sheets.

Through all these channels, a prolonged period of low short-term interest rates can support the accumulation of risks and financial imbalances on the balance sheets of both financial intermediaries and the private sector. These imbalances render the economy vulnerable to financial crises: if confidence evaporates, lenders call in loans, balance sheets contract and a painful readjustment is required, with adverse implications for financial stability and the real economy. In particular, the build-up of leverage within the financial sector may unwind abruptly, leading to a tightening of overall financing conditions. [20]

Such thinking sheds light on recent developments in the run-up to the financial crisis. Viewing the impact of globalisation on goods prices as the manifestation of a positive supply shock, we can map this abstract scenario into our experience of the past decade. At the global level, the incorporation of emerging markets into the world economy weighed down on price developments (especially of manufactured goods). In response to the resulting benign inflation developments, the prevailing inflation targeting orthodoxy led to the adoption of an accommodative monetary policy stance. In retrospect, such accommodation was probably inappropriate, at least to the extent that it supported the financial imbalances and asset price bubbles that underlay the recent financial crisis. Failure to take into account financial factors and channels of transmission led to a mis-calibration of the monetary policy response to the impact of globalisation.

A simplistic account of the financial sector may have had other, adverse implications for the conduct of monetary policy in recent years. Within the canonical New Keynesian model, financial markets are “perfect.” On the basis of arbitrage considerations, long-term interest rates and other yields and asset returns all derive from the expected path of short-term interest rates determined by the central bank.

Such a construct suggests that monetary policy-makers can steer long-term rates closely by simply making pre-commitments about the future path of short rates. No doubt there is an element of truth in this characterisation. But the conditionality of such pre-commitments on the state of the economy may prove hard to communicate. Financial intermediaries may interpret pre-announced paths as a liquidity guarantee, promoting the excessive risk-taking behaviour I have discussed. Such behaviour may then limit the future flexibility of monetary policy-makers to react promptly to changed circumstances.

All in all, such pre-commitments are not useful and, may even be damaging. Effective central bank communication should allow market participants to understand the decision-making framework. But a pre-commitment to a future path of short-term rates is best avoided. It limits the flexibility of policy-makers – operating within a transparent, rules-based framework – to take decisions as conditions evolve. Looking back over recent years, it seems likely that the adoption of such pre-commitments by some central banks led them to tighten policy too late and too slowly, thus helping to maintain the overly loose monetary stance that fuelled financial imbalances.

3. Assessing economic conditions

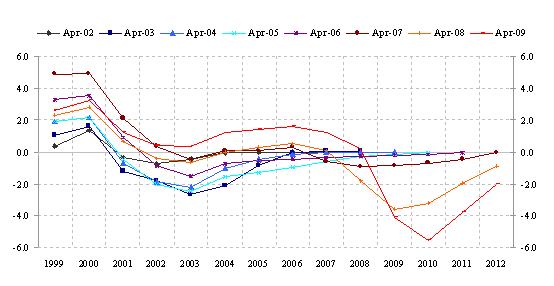

Even with the most sophisticated models of the economy, policy-makers are still heavily reliant on an accurate assessment of the conjunctural situation. Yet the usual business cycle indicators are subject to a variety of measurement errors. As has been demonstrated extensively in the literature, the empirical proxies used to capture the output gap are subject to constant revision. [21] Clearly, policy-makers who rely exclusively on such assessments of the cyclical position can be seriously misguided in their real-time conjunctural assessment. To the extent that these indicators are central to the implementation of flexible inflation targeting, over-reliance on them may have led to an over-activist and at times inappropriate monetary policy stance. In particular, policy makers might also have formed an overly benign assessment of the situation prevailing in 2002-2004 if they relied excessively on output gap measures, as these measures were based on overly optimistic assumptions about potential growth. For instance, in early 2003 the IMF estimated the US output gap for that same year to be slightly above 2%. In early 2006 the estimate was revised down by 1 percentage point and one year later by another 1 percentage point. With the benefit of hindsight it turned out that in 2003 the output gap was basically nil (See figure 3). [22]

Such considerations plague other composite indicators derived from the literature, such as the natural real interest rate.

Understanding current inflation developments can also prove challenging. Headline inflation rates may be volatile in the short term, reflecting the impact of temporary relative price shocks. [23] Monetary policy-makers need to look through such noise. But conventional measures of so-called “core inflation” can themselves be misleading. For example, measures that exclude energy prices can offer a false impression of the underlying dynamics of inflation if energy prices are trending upwards.

Clearly, policy-makers with a mistaken view of the conjunctural situation are liable to make policy mistakes. In a stylised Taylor-rule setting, errors in assessing inflation or the output gap will lead to flawed guidance on interest rate decisions. Such considerations may have led to overly accommodative monetary policy prior to the financial crisis.

To give one example, I have already discussed how the forces of globalisation at the turn of the century weighed on the prices of manufactured goods. This was an important factor underpinning the benign outlook for inflation. Yet the rapid growth of emerging market economies had other implications for global price developments. Notably, commodity prices in general – and that of oil in particular – rose rapidly in the face of strong demand from China as well as from Brazil, Russia and India. Policy-makers who focused on measures of core inflation that excluded energy prices neglected the latter effect. They may have formed an overly benign impression of the consequences of globalisation for price developments, and adopted an overly loose monetary policy as a result.

Thus far, my discussion of the conjunctural assessment has focused on indicators motivated by the benchmark New Keynesian framework. But we need to include the financial sector. What indicators were missed by central banks prior to the crisis due to the neglect of financial factors? What additional indicators should be embodied in the conjunctural assessment?

Monetary and credit aggregates can – and did – have a role to play. At least in part, the ECB’s oft-maligned monetary analysis was vindicated by the crisis. If central banks had taken the signals coming from strong monetary and credit growth in mid-decade more seriously, monetary policy decisions might have been better calibrated to contain the financial imbalances that ultimately led to the financial crisis.

But recent events have also revealed weaknesses in traditional monetary indicators. Experience points to a need to deepen and broaden such analyses to take better account of the fundamental changes observed in the financial sector over recent decades. New aggregates and indicators need to be developed. [24] Work at the ECB is proceeding in this direction.

In particular, the financial crisis revealed weakness in central banks’ understanding of financial fragilities and their implications for the real economy and, ultimately, price developments. To be concrete: while demonstrating concern at the rapid pace of credit growth, in retrospect we did not understand well enough the accumulation of leverage in the economy, in general – and in the financial system, in particular. And we took too benign a view of the accelerating securitisation and credit risk transfer processes. Rather than distributing risks to those best able to bear them, with the benefit of hindsight, incentive problems in these processes led to a concentration of liquidity and credit risk.

In short, central banks had a poor understanding of the complex interconnections among financial intermediaries and with the real economy, both domestically and internationally. Systemic risk, contagion and herding behaviour were neglected. Addressing these weaknesses in existing policy frameworks is at the heart of the ongoing development of so-called macro-prudential policy.

To sum up, the main weakness of monetary policy frameworks prior to the financial crisis was their neglect of financial factors in the evolution of the economy and policy transmission. We need to refine our policy frameworks to take account of such channels.

4. Monetary policy and macro-prudential policy

Taking the role of the financial sector in monetary policy transmission more seriously reveals the macroeconomic consequences of microeconomic behaviour: the impact on inflation, growth and financial stability of the behaviour of financial institutions. As a result, a revised framework has important implications for both the conduct of monetary policy and for policies aimed at maintaining financial stability.

Viewing recent experience through this lens demonstrates that the achievement of financial stability relies on more than traditional micro-prudential supervision of individual financial institutions. Clearly, policy needs to take into account the impact of such externalities in order to develop a framework supporting the stability of the financial system as a whole, rather than the individual institutions which constitute it.

By the same token, the preceding analysis demonstrates that taking appropriate monetary policy decisions relies on an understanding of the behaviour of financial intermediaries and, in turn, on financial structure and innovation.

From a policy perspective, the impact of monetary policy on the behaviour of the financial sector suggests that short-term interest rates are a potentially powerful tool to influence the evolution of systemic risk, and thus to support financial stability. However, as I discussed at the outset, monetary policy should not be overburdened with additional objectives. The primacy of the price stability objective must be retained.

The well-known Tinbergen principle makes clear that a single instrument (short-term interest rates) is insufficient to achieve two goals simultaneously. [25] In such a context, additional policy instruments are required. This is where macro-prudential policy tools come into play. While the analytic basis and calibration of instruments such as pro-cyclical capital requirements or leverage ratios require further elaboration, the hope is that such measures can contain the accumulation of financial imbalances and vulnerabilities without recourse to changes in short-term interest rates.

Monetary policy and macro-prudential policy: two policy instruments and two policy objectives. At least in principle, the Tinbergen problem is resolved.

But practicalities stand in the way. As I said earlier, it is immediately apparent that monetary policy and macro-prudential policy will interact in a variety of potentially complex ways, throwing up new challenges for policy-making. Of course, what is required is the “right combination” of prudential policies and monetary policy – a combination that simultaneously achieves both price stability and financial stability. How is this combination best achieved?

We can draw some important lessons from our assessment of the interaction between monetary and fiscal policy in the past. Attempts to develop an optimal “macroeconomic policy mix” are superficially attractive, but have typically foundered in practice. As the responsibilities of different policy-makers become blurred, their incentive to act appropriately is diluted and ultimately the overall coherence of the policy stance is lost.

The institutional framework for monetary policy in the euro area reflects these concerns. The single monetary policy is independent and has been assigned an unambiguous objective of price stability. The ECB is accountable for the achievement of this objective. All this is understood by other policy-makers. By acting in a transparent way consistent with its mandate, the ECB creates an environment of price stability within which other authorities can take decisions under their responsibility in order to achieve their own objectives. Clarity of responsibility, independence of action and accountability for decisions in an environment of open and frank exchange of information among policy authorities produces the best results.

These principles can be readily applied to the relationship between monetary policy and macro-prudential policies. Of course, monetary policy decisions can have implications for financial stability. And the degree of freedom accorded by the medium-term orientation of monetary policy can be used to contain excessive risk-taking by banks. In this sense, monetary policy can support financial stability objectives without prejudice to its primary objective of price stability.

But this does not imply that monetary policy should be held jointly accountable for maintaining financial stability, still less that it be assigned an additional financial stability objective. Such measures would only serve to obscure the accountability of monetary policy-makers for price stability and dilute the accountability of those authorities responsible for financial stability. All this leads me to re-iterate my earlier conclusion: the primary objective of monetary policy must remain price stability.

By contrast, the institutional structure for prudential supervision and regulation at the European level remains at an embryonic stage, especially on the macro-prudential side. The prospective creation of a European Systemic Risk Board will partly fill this lacuna.

For the reasons I have discussed, financial supervision and regulation clearly cannot be conducted without reference to the monetary policy stance. But, both in finalising the institutional framework and in the conduct of these policies in the future, the principles I have articulated must be respected. We need to ensure that macro-prudential policy is formulated both independently and transparently, guaranteeing a rich flow of information among the relevant authorities, including monetary policy-makers, while at the same time avoiding any blurring of responsibilities, objectives and accountability.

Concluding remarks

In conclusion, what are the main lessons from recent experience that we should seek to incorporate in any revision to the framework for monetary policy-making?

First and foremost, monetary policy should have remained more closely focused on the maintenance of price stability over the medium term. This implies that this objective must be defined clearly and pursued symmetrically. Monetary policy should not be burdened with additional objectives, which it is ill-equipped to pursue.

The institutional independence of the central bank is essential to building the credibility required to pursue price stability in a consistent and coherent manner. Dual mandates for monetary policy place this independence at risk. Independence accords central banks the necessary flexibility to deal with a rapidly changing world without putting their credibility at risk.

Second, monetary policy should have been less geared to fine-tuning the economy, in particular to trying to reduce the output gaps which ex post turn out to be very different from their real-time measurement. The long and variable lags in monetary policy transmission mean that a medium-term orientation for monetary policy must be maintained. Temporary deviations from a precise inflation objective are inevitable – monetary policy-makers must focus on containing persistent trends in inflation. Distinguishing between temporary and more persistent shocks to inflation is therefore crucial. Experience has shown that paying attention to specific measures of “core inflation” may mislead monetary policy. An overly mechanical view of such indicators can lead to an underestimation of the strength of inflationary pressures at the global level.

Third, policy decisions should have been based on better models of monetary policy transmission. Monetary and financial factors have been too easily dismissed, especially by inflation targeting regimes. Placing greater weight on monetary and credit indicators should allow interest rate decisions to be better calibrated to achieve the appropriate medium-term objectives of monetary policy.

Can central banks learn from experience? They can if they are able to recognise what went wrong, rather than sweeping the hard questions under the carpet, and if they are able to adapt their analytical and decision-making framework. Suggesting that monetary policy had nothing to do with the crisis will not help, and might encourage us to make the same mistakes in the future. The reaction to the crisis has however shown that central banks learn fast and can take decisive action to protect the economy. Their response is in stark contrast to how they reacted to the Great Depression. On that occasion, monetary policy-makers were largely responsible for causing the crisis, for deepening it and for preventing a quick recovery.

We can be more optimistic this time around.

Figure 2: Overall inflation excluding food and energy

Source: ECB, BLS and OECD

Note: Average annual inflation rates

Figure 3

Spring vintages (2002-2009) of US output gap estimates by the IMF (WEO)

Source: IMF (WEO) data

Note: Output gaps are defined as the percentage deviation of actual output from potential output.

-

[1]I wish to thank José Luis Peydró-Alcalde and Huw Pill for their contribution to preparing the speech. I remain sole responsible for the opinions.

-

[2]See: B. Bernanke (2010), “Monetary policy and the housing bubble,” speech at the 2010 AEA meetings http://www.federalreserve.gov/newsevents/speech/bernanke20100103a.htm.

-

[3]For a response to Bernanke (2010), see: J. Taylor (2010), “The Fed and the crisis: A reply to Ben Bernanke,” Wall Street Journal (11 January).

-

[4]See, inter alia: C. Borio and H. Zhu (2008), “Capital regulation, risk-taking and monetary policy: A missing link in the transmission mechanism?” BIS working paper no. 268; G. Jiménez, S.R.G. Ongena, J-L. Peydro and J. Saurina Salas (2010), “Credit supply: Identifying balance sheet channels with loan applications and granted loans,” CEPR discussion paper no. 7655; Y. Altumbas, L. Gambacorta and D. Marques (2010), “Does monetary policy affect bank risk-taking?” ECB working paper no. 1166; and A. Maddaloni and J-L. Peydró (2009), “Bank risk-taking, securitisation, supervision and low interest rates: Evidence from lending standards,” ECB working paper, forthcoming.

-

[5]On the basis of the harmonised index of consumer prices (HICP).

-

[6]See H. Theil (1964). Optimal decisions for government and industry, Amsterdam: North Holland.

-

[7]See: M. Goodfriend and R. King (1997), “ The new neoclassical synthesis and the role of monetary policy,” NBER Macroeconomics Annual 12, pp. 231-296; and J.J. Rotemberg and M. Woodford (1999), “ Interest rate rules in an estimated sticky price model,” in ed. J.B. Taylor Monetary policy rules, Chicago University Press, pp. 57-126.

-

[8]See: e.g. S.S. Roach (2010). “The post-crisis fix: Regulatory or monetary policy remedies?” paper presented at the Reserve Bank of India’s First International Research Conference (February); P. De Grauwe and D. Gros (2009), “A new two-pillar strategy for the ECB,” CEPS policy brief no.191.

-

[9]See: O. Blanchard, G. Dell’Ariccia and P. Mauro (2010). “Rethinking macroeconomic policy,” IMF staff position note no. 10/03 http://www.imf.org/external/pubs/ft/spn/2010/spn1003.pdf.

-

[10]See M.A. King (1997), “Changes in UK monetary policy: Rules and discretion in practice.” Journal of Monetary Economics 39, pp. 81–97.

-

[11]See L.E.O. Svennson (1998), “Inflation targeting in an open economy: Strict or flexible inflation targeting?” Victoria Economic Commentaries 15(1).

-

[12]At least when the output gap is defined in a “model-consistent” manner, i.e. as deviations of output from the level it would achieve in the absence of nominal rigidities.

-

[13]See: O. Blanchard and J. Galí (2007). “Real wage rigidities and the New Keynesian model,” Journal of Money, Credit and Banking 39(s1), pp. 35-65.

-

[14]Prominent examples include, inter alia: P. Krugman (2009), “How did economists get it so wrong?” New York Times (2 September); and W.H. Buiter (2009), “The unfortunate uselessness of most ‘state-of-the-art’ academic monetary economics,” Financial Times (3 March).

-

[15]See: C.E.V. Borio and H. Zhu (2008), “Capital regulation, risk-taking and monetary policy: A missing link in the transmission mechanism?” BIS working paper no. 268.

-

[16]See: Y. Altumbas, L. Gambacorta and D. Marques (2010), “Does monetary policy affect bank risk-taking?” ECB working paper no. 1166; G. Jiménez, S.R.G. Ongena, J-L. Peydro and J. Saurina Salas (2010), “Credit supply: Identifying balance sheet channels with loan applications and granted loans,” CEPR discussion paper no. 7655; and A. Maddaloni and J-L. Peydró (2009), “Bank risk-taking, securitisation, supervision and low interest rates: Evidence from lending standards,” ECB working paper, forthcoming.

-

[17]See: E. Fahri and J. Tirole (2009), “Leverage and the central banker's put,” American Economic Review 99(2), pp. 589-93.

-

[18]See: D.W. Diamond and R.G. Rajan (2009), “ Illiquidity and interest rate policy,” NBER working paper no. 15197.

-

[19] See: T. Adrian and H.S. Shin (2009), “Financial intermediaries and monetary economics,” Handbook of Monetary Economics, forthcoming ; R.G. Rajan (2005), “ Has financial development made the world riskier? ” Proceedings of the FRB Kansas City Jackson Hole symposium ‘The Greenspan years: Lessons for the future’; and F. Allen and D. Gale (2007), Understanding financial crises, Oxford University Press.

-

[20]See: G.B. Gorton and A. Metrick (2009), “Securitized banking and the run on repo,” Yale ICF working paper no. 09-14.

-

[21]See: A. Orphanides and S. van Norden (2002), “The unreliability of output gap estimates in real time,” Review of Economics and Statistics 84(4), pp. 569-583; and A. Orphanides and S. van Norden (2005), “The reliability of inflation forecasts based on output gap estimates in real time,” Journal of Money, Credit and Banking 37(3), pp. 583-601.

-

[22] L. Bini Smaghi (2009), “Monetary Policy and Asset Prices”, Freiburg University, 14 October 2009.

-

[23]Such as seasonal movements in food prices.

-

[24]See T. Adrian and H.S. Shin (2009), “Prices and quantities in the monetary policy transmission mechanism,” International Journal of Central Banking 5(4), pp. 131-142.

-

[25]See: J. Tinbergen (1952), On the theory of economic policy, Amsterdam, North-Holland.

Ευρωπαϊκή Κεντρική Τράπεζα

Γενική Διεύθυνση Επικοινωνίας

- Sonnemannstrasse 20

- 60314 Frankfurt am Main, Germany

- +49 69 1344 7455

- media@ecb.europa.eu

Η αναπαραγωγή επιτρέπεται εφόσον γίνεται αναφορά στην πηγή.

Εκπρόσωποι Τύπου