Policy expectation errors during the recent tightening cycle – insights from the ECB’s Survey of Monetary Analysts

Published as part of the ECB Economic Bulletin, Issue 1/2024.

Information from the Survey of Monetary Analysts (SMA) on respondents’ expectations about the future evolution of the ECB’s monetary policy measures can provide insights into the source of expectation errors during the recent tightening cycle. Since July 2022 the Governing Council has raised the key ECB interest rates by a total of 450 basis points in response to the extraordinary surge in inflation. After a protracted period of policy rates close to the effective lower bound, financial markets and analysts expected an interest rate path that was much flatter than the one ultimately realised. Accordingly, policy expectation errors have been large and have only recently started to diminish. SMA data can help to determine whether these errors are due to a misperception of the ECB’s reaction function or to miscalculations about the macroeconomic environment.[1]

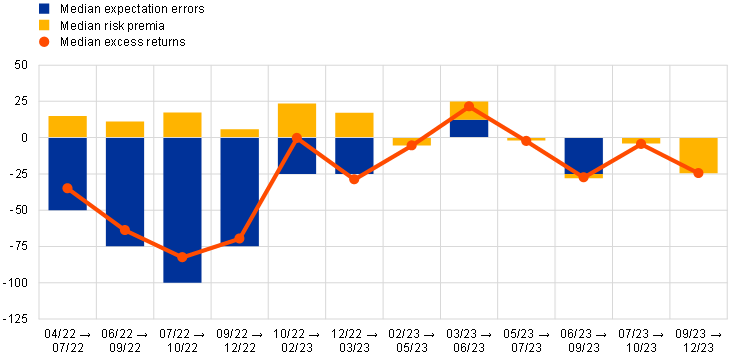

Since spring 2022 financial markets and analysts have predicted the Governing Council’s immediate policy rate decisions relatively accurately but made substantial errors in their predictions three Governing Council meetings ahead. Using individual SMA expectations, ex post excess returns, measured as the difference between the euro short-term rate (€STR) forward curve and the realised deposit facility rate (DFR), can be decomposed into two components:[2] (i) risk premia, approximated by the difference between the €STR forward curve and the SMA DFR expectations, and (ii) expectation errors, namely the difference between the SMA DFR expectations and the realised DFR.[3] The resulting decomposition (Chart A) shows that, during the sample period, both financial markets and SMA respondents underestimated the pace of the interest rate hiking cycle. In the very short term (one Governing Council meeting ahead), monetary policy expectations predicted the interest rate decisions accurately in most cases. However, over a longer horizon (three Governing Council meetings ahead) there was a sharp increase in policy expectation errors. Specifically, SMA respondents consistently underpredicted the path of policy rates during 2022, by up to 1 percentage point.

Chart A

SMA-based expectation errors and risk premia three Governing Council meetings ahead

(basis points)

Sources: SMA and ECB calculations.

Notes: SMA expectations are used to decompose ex post excess returns (measured as the difference between €STR forward rates and the realised deposit facility rate into risk premia (approximated by the difference between the €STR forward rates and SMA DFR expectations) and expectation errors (the difference between the SMA DFR expectations and the realised DFR)

For instance, "three meetings ahead” implies that, at the SMA cut-off date ahead of the July 2022 Governing Council meeting, expectations for the October 2022 Governing Council decision are considered. The sample period spans from April 2022 to December 2023. The latest observations are for 14 December 2023.

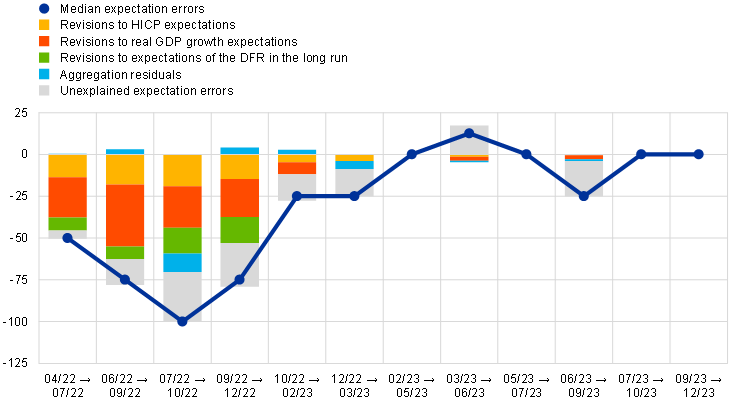

The uncertain macroeconomic environment, as reflected in large revisions to inflation and output expectations, has played a major role in shaping the policy expectation errors.[4] Econometric evidence suggests that a considerable share of the underprediction of the policy rate path three Governing Council meetings ahead is associated with revisions to expectations for macroeconomic developments (Chart B). Specifically, revisions to macroeconomic expectations, measured here by revisions to SMA expectations of year-on-year HICP inflation and quarter-on-quarter real GDP growth four quarters ahead, are strongly linked to the policy expectation errors. Similarly, upward revisions to expectations for the DFR in the long run can help explain those errors. Hence, the underprediction of policy tightening correlates with respondents consistently revising their inflation expectations upwards and their real GDP growth expectations downwards, reflecting an economic environment dominated by supply-side shocks causing inflation and output to move in opposite directions. Such correlation patterns cannot be interpreted as a perceived structural policy reaction function, owing to the episodic nature of the short sample being investigated. Nevertheless, they suggest that developments in macroeconomic expectations are a key factor in explaining the policy expectation errors.

Chart B

Decomposition of expectation errors three Governing Council meetings ahead

(basis points)

Sources: SMA and ECB calculations.

Notes: Expectation errors are decomposed at the individual level via a pooled ordinary least squares (OLS) regression with revisions to (i) HICP inflation expectations four quarters ahead, (ii) real GDP growth expectations four quarters ahead, and (iii) expectations for the DFR in the long run as regressors. The chart shows the median contributions from these three components. Aggregation residuals are the differences between the regression’s fitted values and the sum of the median of these three components. Unexplained expectation errors are the differences between the observed expectation errors and the fitted values. The coefficients are estimated based on the sample of individual SMA expectations from April 2022 to September 2023. The latest observations are for 14 December 2023.

This analysis suggests that SMA respondents perceived a broadly consistent policy reaction to macroeconomic developments when forming expectations for monetary policy. Since the start of the increases in the key ECB interest rates, both excess yield returns and errors in predicting the path of the DFR have been predominantly negative, as financial markets and analysts have underestimated the pace and size of the hikes. The rise in expectation errors has been mostly related to changes in macroeconomic expectations, suggesting that analysts perceived a broadly consistent policy reaction to economic developments, but have had difficulty predicting those developments.

For further details on the SMA, see Brand, C. and Hutchinson, J., “The ECB Survey of Monetary Analysts: an introduction”, Economic Bulletin, Issue 8, ECB, 2021.

The €STR forward curve is adjusted by adding individual SMA expectations for the spread between the DFR and the €STR.

For comparable decompositions of excess returns, see Schmeling, M., Schrimpf, A. and Steffensen, S.A.M., “Monetary policy expectation errors”, Journal of Financial Economics, Vol. 146, No 3, December 2022, pp. 841-858; and Cieslak, A., “Short-Rate Expectations and Unexpected Returns in Treasury Bonds”, The Review of Financial Studies, Vol. 31, No 9, September 2018, pp. 3265-3306.

For a similar analysis, but with calibrated coefficients, see Bernardini, M. and Lin, A., “Out of the ELB: expected ECB policy rates and the Taylor Rule”, Occasional Papers, No 815, Banca d’Italia, October 2023.