Published as part of the ECB Economic Bulletin, Issue 3/2023.

This box summarises the findings of recent contacts between ECB staff and representatives of 61 leading non-financial companies operating in the euro area. The exchanges took place between 30 March and 13 April 2023.[1]

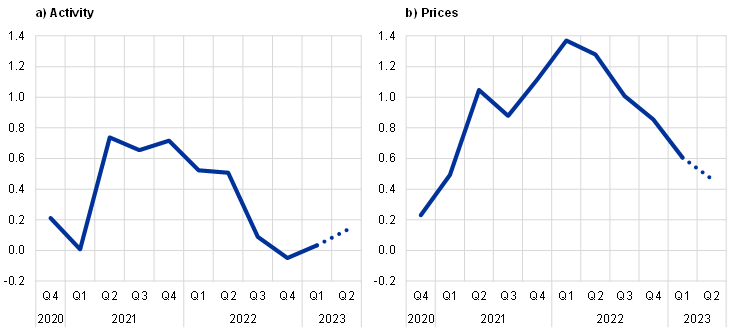

In aggregate terms, these contacts pointed to stagnating or only modestly growing activity in the first quarter, with varied development across sectors. In this respect, developments were, on average, in line with expectations expressed during the previous round of exchanges in January. Most contacts in the consumer goods, retail and construction sectors reported declining activity, but this was offset by reports of growth in the demand for consumer services and the production of capital goods.

Activity in the industrial sector continued to be influenced by forces working in opposing directions. On one hand, high inflation, together with the satiation of consumer demand for certain items during the coronavirus (COVID-19) pandemic, continued to depress demand for many consumer goods. Moreover, since mid-2022 many companies had reportedly been reducing their inventories and this reduction was viewed as still ongoing in some sectors, causing divergent developments in the demand for related intermediate goods. Construction activity was adversely affected by falling demand for residential development, reflecting higher input and financing costs. On the other hand, a relatively rapid easing of past supply disruption facilitated increased production, primarily in the capital goods sector. According to the contacts, supply chains were largely back to normal. Automotive-related production was therefore recovering (albeit still at a low level), while producers of machinery and equipment reported high or increasing production levels to deal with still large order backlogs, especially those serving customers’ investment needs in relation to the transition to net zero. Activity in the agri-food sector was supported by generally inelastic demand, reduced imports and high prices incentivising increased production. In the energy sector, the generation of wind and solar energy had increased in recent months.

Contacts in the services sector reported subdued activity in retail and the transport of goods but strongly growing demand for travel, tourism and IT services. Most retailers, especially those selling non-essential goods, reported contracting activity in line with the downbeat assessment of contacts in the consumer goods industry. This was consistent with reports from contacts in the transport sector, with activity in road haulage and shipping described either as declining or as stabilising at somewhat lower levels than a few quarters ago. By contrast, contacts from across the travel and tourism industry were very upbeat about strongly growing demand for travel services, despite rising prices, both during the winter and Easter and in relation to bookings for the summer season. IT services continued to be another driver of services sector growth, in part benefiting from demand related to environmental, social and governance (ESG) and regulatory requirements.

Current trends in activity were generally expected to persist during the second quarter, while the outlook for later in the year was still subject to elevated uncertainty. Expectations of a further pick-up in activity in the second half of the year were muted in view of mixed signals about global demand and continued uncertainty surrounding energy prices/supply, to which was added some nervousness caused by recent problems with some banks.

Chart A

Summary of views on developments in and the outlook for activity and prices

(averages of ECB staff scores)

Source: ECB.

Notes: The scores reflect the average of scores given by ECB staff in their assessment of what contacts said about quarter-on-quarter developments in activity (sales, production and orders) and prices. Scores range from -2 (significant decrease) to +2 (significant increase). A score of 0 would mean no change. The dotted line refers to expectations for the next quarter.

Developments in – and the near-term outlook for – employment were quite stable overall. Reports of strong employment growth were limited to relatively few sectors, most notably energy (driven by investment in renewables and clean energy infrastructure) and travel (given the ongoing strong recovery of tourism). Reports of lay-offs and anticipated lay-offs were also few in number and mainly in the energy-intensive intermediate goods sectors. Companies that wanted to reduce headcount could generally achieve this through natural churn, although some expected increasing scrutiny of labour costs as the year went on in view of rising wages and moderating price growth. Employment agencies reported somewhat mixed developments, with weak activity in temporary placements but still strong growth in permanent placements. Contacts from a range of industries continued to find recruitment challenging given shortages of various skills, while there were also some reports of activity being hindered and labour costs rising due to high rates of sick leave.

The rate of increase in selling prices was said to be moderating overall, broadly as anticipated at the beginning of the year. To a large extent, this moderation reflected stabilising non-labour input costs and the rebalancing of supply and demand for many goods since last summer. This was, however, partly offset by increasing cost pressure from wages. Contacts in the consumer goods and retail sectors (at least those producing and/or selling non-essential items) saw the pricing environment becoming more difficult amid reduced demand and strong competition. There were, however, a number of sectors in which contacts still pointed to strong selling price increases, at least during the first half of 2023. In the industrial sector, notwithstanding the fact that the prices of energy and many upstream intermediate goods had fallen in recent months, such prices mostly remained at historically high levels. Consequently, the prices of many inputs were still rising as past input cost increases and/or higher wages were passed through. Contacts in the more labour-intensive parts of the business and consumer services sectors anticipated continued strong price growth in view of high wage growth. Pricing in the travel and tourism sectors also continued to benefit from exceptionally strong price-inelastic demand.

Wage expectations were basically unchanged from the previous survey round, and wage growth remained the main cost concern. Taking a simple average of the mid-points of the quantitative indications provided, contacts anticipated growth of around 5% in 2023 (up from levels around 3% in 2022). Many firms also made significant one-off payments to employees in 2022 and/or 2023.

Despite the favourable pricing environment in many sectors recently, contacts pointed to profit margins being quite stable overall, especially if developments in 2022 and expectations for 2023 were considered together. Margins had increased quite significantly in the energy, transport and agri-food sectors in 2022, reflecting the exceptional market developments in these sectors. However, at least for energy and goods transport, this situation was already reversing. In business-oriented sectors (capital goods, intermediate goods, business services), most contacts said that the environment had been favourable for passing through rising costs to prices during 2022, in part due to supply disruption which caused customers to focus more on availability than price. The effect of this price and cost inflation on margins varied depending on how quickly prices could be adjusted given contractual obligations, and the aggregate picture for 2022 and 2023 was one of broadly stable margins. By contrast, in consumer-oriented sectors (consumer goods and services, including retail trade), many contacts said that it had been difficult to fully pass through increased costs to prices, and the aggregate picture was of margins being squeezed, especially in 2022, and, to some extent, this was also expected to continue in 2023.

For further information on the nature and purpose of these contacts, see the article entitled “The ECB’s dialogue with non-financial companies”, Economic Bulletin, Issue 1, ECB, 2021.