The scarring effects of past crises on the global economy

Published as part of the ECB Economic Bulletin, Issue 8/2020.

The coronavirus (COVID-19) pandemic is an unparalleled shock to the global economy. First, the shock is multilayered, with the public health emergency compounded by an induced supply shock (i.e. following the adoption of stringent lockdown measures) and a demand shock as a consequence of increased unemployment and heightened uncertainty. Second, it has triggered a multifaceted and sizeable policy response, which has alleviated the adverse effects on economic activity but could exacerbate existing imbalances in the global economy and raise concerns about public and private debt overhangs and future deleveraging needs. Finally, certain sectors have been hit particularly hard by the lockdown measures and behavioural changes on the part of consumers, which are likely to remain in place at least until an effective medical solution has been implemented.

Given the complex nature of the COVID-19 shock, the implications for the long-term growth potential of the global economy must be considered. This box reviews past crises and the transmission channels through which potential output is affected.[1] The analysis is subject to high uncertainty, because potential output is an unobserved variable. Furthermore, the COVID-19 crisis is in many respects unique, and therefore past crises may not be reliable indicators of the lasting effects it may have on the global economy, not least because its length, one of the key parameters for assessing potential scarring effects, remains unknown.

The traditional view that business cycle fluctuations do not influence long-term growth has been disputed in the economic literature. For example, the existence of labour market hysteresis effects (i.e. a persistent effect of shocks on unemployment) is a phenomenon that has been widely examined and discussed.[2] Furthermore, recent literature contributions, motivated by the sluggish recovery after the global financial crisis, have shown that recessions cause persistent or “scarring” effects on the level of GDP,[3] as cyclical events affect the supply side of the economy through several channels, thereby shaping the long-term trend.

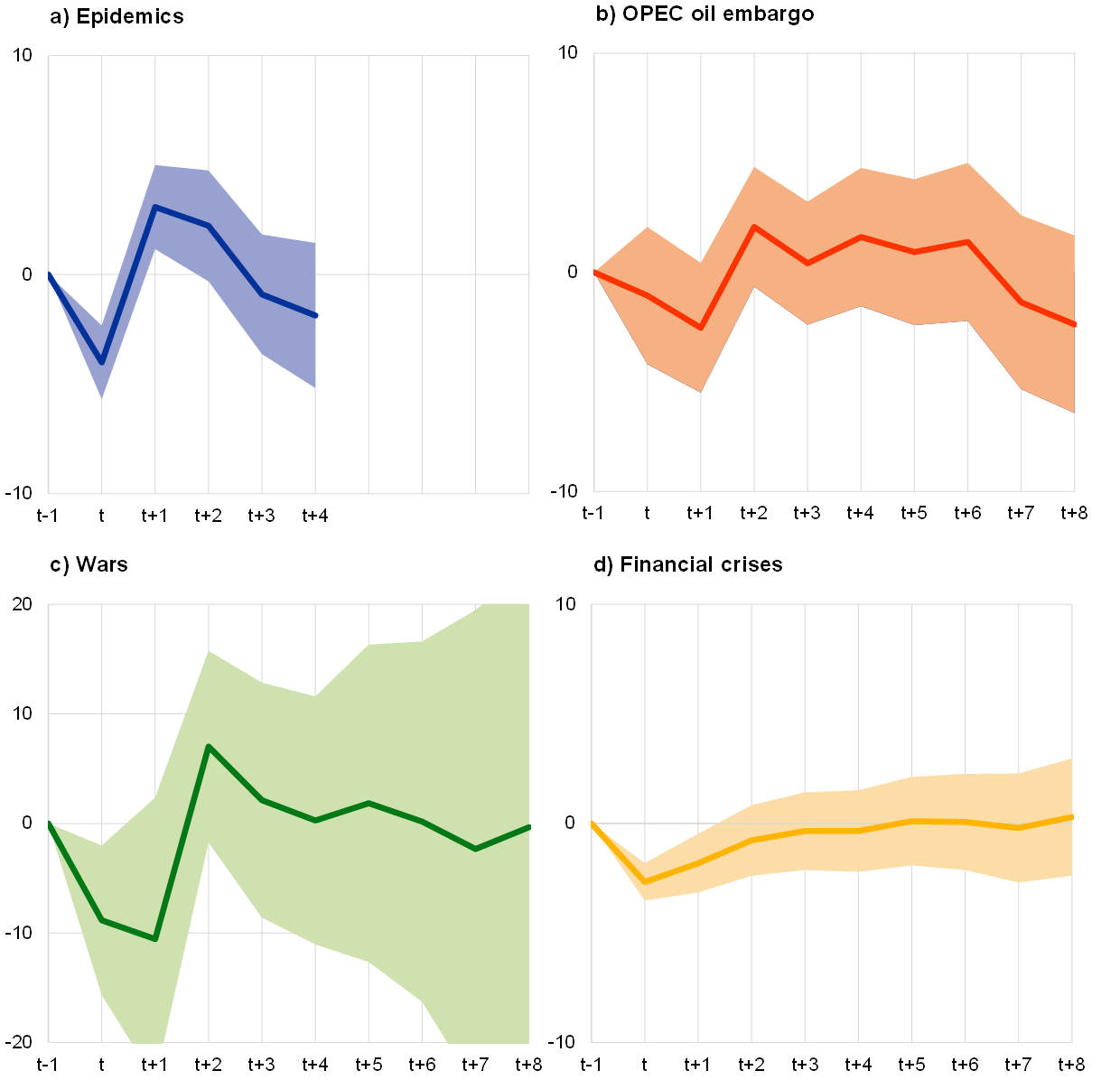

Assessing the scarring effects of past crises does provide some indication as to how the COVID-19 shock may affect potential output.[4] A local projections analysis of past epidemics suggests that the initial impact on the level of potential output is relatively short-lived, tending to dissipate two years after the end of the epidemic (see Chart A, upper left panel). [5] However, it should be noted that the past epidemics considered in the analysis were mostly localised events which are not comparable to a major global pandemic.[6] Thus, the impact of two additional exogenous types of crisis on potential output is assessed, namely the 1973-74 oil embargo imposed by the Organization of the Petroleum Exporting Countries (OPEC), which can be regarded as an exogenous negative supply shock for the targeted countries,[7] and the effect of major wars[8]. Results suggest that the oil embargo only had a negative effect on potential output in the first year after the shock (upper right panel). In turn, the results for major wars (lower left panel) suggest that following a severe initial impact, post-war economic recoveries tend to be steep with no longer-lasting scarring effects (i.e. beyond four years). However, the very wide confidence intervals point to sizeable heterogeneity in the long-term impact of wars.

Chart A

Scarring effects of past epidemics and other crises on potential output levels

(indices)

Sources: ECB calculations based on Penn World Tables and Laeven and Valencia (see footnote 4).

Note: The continuous lines indicate the impact of the respective event in year t on the level of potential output up to the period t+8, i.e. eight years after the end of the event, and the shaded areas depict the 95% confidence interval. The impact on potential output is estimated with a local projections approach, based on a global panel that includes all events simultaneously, four lags of potential output growth to control for endogeneity, and country-fixed effects. As most of the epidemics considered in the analysis are relatively recent, the sample only allows their impact to be calculated until four years after the end of the epidemic. Potential output is defined as the level of output that is consistent with the productive capacity of an economy.

In contrast, financial crises are associated with a very persistent downward shift in potential output. The results for past financial crises (as examples of endogenous crises, i.e. those triggered by the accumulation of economic imbalances) suggest a loss of around 5% even after eight years, in line with the recent literature discussed above. This is supported by the fact that, for recessions caused by financial crises, no overshooting in growth rates can be observed after the end of the recession, pointing to long-lasting scarring effects on the level of potential output (see Chart B). This is different from the exogenous crises (i.e. epidemics, the OPEC embargo and wars), where the initial contraction is followed by above-normal growth rates, bringing the economy’s potential output back to its long-term trend path.

Chart B

Impact of past epidemics and other crises on potential output growth

(percentage growth rates)

Sources: ECB calculations based on Penn World Tables and Laeven and Valencia (see footnote 4).

Note: The continuous lines indicate the impact of the respective event in year t on the growth rate of potential output up to the period t+8, i.e. eight years after the end of the event, and the shaded areas depict the 95% confidence interval. The impact on potential output is estimated with a local projections approach, based on a global panel that includes all events simultaneously, four lags of potential output growth to control for endogeneity, and country-fixed effects. As most of the epidemics considered in the analysis are relatively recent, the sample only allows their impact to be calculated until four years after the end of the epidemic. Potential output is defined as the level of output that is consistent with the productive capacity of an economy.

Evidence shows that in recessions following financial crises, the impact of the crisis was particularly persistent for the capital stock.[9] It is useful to assess the impact of past financial crises on the individual components of potential output. All three supply-side components of the production function are initially affected by a financial crisis (see Chart C). While the negative impact on total factor productivity and labour input starts to subside after approximately three years, there are adverse and persistent effects on the capital stock, which is the main source of the long-term scarring effects of financial crises.

COVID-19 could negatively affect the capital stock, as was observed in past financial crises. Capital depreciation is likely to have increased as a result of COVID-19, especially in capital-intensive sectors hit by the crisis such as the airline industry, where parts of the capital stock could become obsolete, as well as in other sectors that are struggling as a result of the demand shock. Furthermore, post-crisis public finance consolidation needs combined with difficult economic prospects for companies may contribute to a period of protracted under-investment.[10]

Chart C

Impact of financial crises on supply-side components of potential output

(cumulative growth rates)

Sources: ECB calculations based on Penn World Tables and Laeven and Valencia (see footnote 4).

Notes: The bars indicate the impact of financial crises on the respective supply-side components after the number of years shown since the end of the crisis. The error bars represent a 95% confidence interval. The impact on potential output is estimated using a local projections approach, based on a global panel that includes all events simultaneously, four lags of potential output growth to control for endogeneity, and country-fixed effects. Potential output is defined as the level of output that is consistent with the productive capacity of an economy.

As the COVID-19 shock has above all hit labour-intensive sectors, the initial impact on labour supply could be stronger compared with past financial crises. With the exception of transport, the sectors most affected by the COVID-19 containment measures (i.e. retail trade, accommodation and food services, entertainment and recreation) tend to be more labour than capital-intensive (see Chart D). At the same time, even sectors not targeted by the lockdown measures may have been hit indirectly through reduced sales of intermediate goods to affected sectors.[11] Whether those employment losses will become more permanent will depend on the speed of the reallocation of workers across sectors and firms. Pandemic-related labour market consequences, such as a reduction in the labour force due to an increase in the number of discouraged workers or more limited global migration flows to advanced economies, might lead to a sustained contraction in the labour force. This contraction, combined with the impact on the accumulation of human capital from widespread school closures, could exacerbate the loss in labour supply.[12] At the same time, it should be recognised that the losses depend on the policy response and the success of labour market policies in mitigating these effects.[13]

Chart D

Sectoral losses as a result of the COVID-19 containment measures and capital/labour intensity ratio

(x-axis: fixed capital stock per employee; y-axis: percentage estimated losses in value added)

Sources: ECB calculations and the EU KLEMS database.

Notes: Sectoral losses as a result of the COVID-19 lockdown measures are based on an ECB staff assessment for a sample of globally systemic countries and calculated as an unweighted average. The capital/labour intensity ratio is calculated as the fixed capital stock (in 2017) divided by the labour input (in number of employees in 2017) for each sector, based on the unweighted average of a sample of 19 countries.

Finally, while the COVID-19 crisis could also have a negative impact on productivity, the push towards digital technologies might be positive in the longer term. The COVID-19 crisis could affect total factor productivity in several ways. First, the impact of COVID-19 could temporarily lock resources in unproductive sectors, with the reallocation of productive resources towards fast-growing industries likely to take time.[14] In addition, innovation could be impaired through lower spending on research and development, both in the public sector on account of consolidation needs and in the private sector owing to elevated uncertainty. Furthermore, reshoring of global value chains in the aftermath of the COVID-19 crisis could hamper innovation and knowledge spillovers across countries. At the same time, the increased use of digital technologies spurred by the COVID-19 crisis has the potential to accelerate the digital transformation of the global economy and therefore contribute positively to total factor productivity.[15]

- See also the article entitled “The impact of COVID-19 on potential output in the euro area”, Economic Bulletin, Issue 7, ECB, 2020.

- See for example Blanchard, O.J. and Summers, L.H., “Hysteresis and the European Unemployment Problem”, NBER Working Papers, No 1950, National Bureau of Economic Research, 1986.

- See for example Cerra, V., Fatás, A. and Saxena, S.C., “Hysteresis and Business Cycles”, CEPR Discussion Papers, No DP14531, 2020; Jordà, O., Schularick, M. and Taylor, A.M., “Disasters Everywhere: The Costs of Business Cycles Reconsidered”, Federal Reserve Bank of San Francisco Working Papers, No 2020-11, 2020; and Bluedorn, J. and Leigh, D., “Is the Cycle the Trend? Evidence from the Views of International Forecasters”, IMF Working Papers, No 18/163, 2018.

- The following results are based on local projections from a panel data model covering 117 countries from 1970 to 2017. The independent variables represent cumulative potential output growth in each year. Regressors include autoregressive terms of four lags, dummies for the respective events as well as country-fixed effects. Data sources are the Penn World Tables for potential output and its respective sub-components, and Laeven, L. and Valencia, F., “Systemic Banking Crises Revisited”, IMF Working Papers, No 18/206, 2018, for financial crises.

- Past epidemics include SARS (2003), swine flu (2009-10), MERS (2013), the Ebola virus (2014-15) and the Zika virus (2016). Countries are treated as affected if they registered at least ten cases.

- See also Jordà, Ò., Singh, S.R. and Taylor, A.M., “Longer-Run Economic Consequences of Pandemics”, Federal Reserve Bank of San Francisco Working Papers, No 2020-09, 2020, who find significant long-lasting macroeconomic consequences from 15 major pandemics since the 14th century.

- The estimation sample includes the following countries targeted by the OPEC oil embargo: Canada, Japan, the Netherlands, Portugal, South Africa, the United Kingdom and the United States. While the OPEC oil embargo had only a short-lived effect on the embargoed countries compared with the countries not subject to the embargo, the permanent rise in oil prices due to the oil price shocks in the 1970s, particularly the second oil price shock, may have had a more permanent effect on global potential output. See also the article entitled “The impact of COVID-19 on potential output in the euro area”, Economic Bulletin, Issue 7, ECB, 2020.

- The following wars are included in the sample: the Lebanese Civil War (1975-90), the Gulf War in Iraq (1990-91), the Yugoslav Wars (1991-99), the Sierra Leone Civil War (1991-2002), the Second Congo War (1999-2003), the Iraq War (2003-11), the Syrian Civil War (2011-present) and the Iraq Civil War (2014-17).

- In line with the short-lived impact on potential growth discussed above, the impact of epidemics, the OPEC embargo and wars on the individual components of the supply side is either short-lived or not significant at all and is therefore not discussed further here. The only exception is the adverse impact of epidemics on labour supply (including human capital), which intensifies over time. The results for epidemics are broadly similar to the results of recent research by the World Bank. See Dieppe, A. (ed.), “Global Productivity: Trends, Drivers, and Policies”, World Bank, 2020.

- In the first half of 2020 global investment (excluding the euro area) dropped by around 11%, which is more than after the global financial crisis: between the third quarter of 2008 and the first quarter of 2009, global investment decreased by a cumulative 8%. According to OECD projections, global investment will still be 4% lower in the fourth quarter of 2021 than in the fourth quarter of 2019 (the numbers are based on an unweighted average of Australia, Canada, Japan, Korea, the United Kingdom and the United States). See “OECD Economic Outlook No 107 - Single-hit scenario - Edition 2020/1”, OECD Economic Outlook: Statistics and Projections (database), OECD, 2020.

- See Laeven, L., “Pandemics, Intermediate Goods, and Corporate Valuation”, CEPR Discussion Papers, No DP15022, 2020.

- See Burgess, S. and Sievertsen, H.H., “Schools, skills, and learning: The impact of COVID-19 on education”, VoxEU, 2020, which argues that “even a relatively short period of missed school will have consequences for skill growth”.

- See the box entitled “A preliminary assessment of the impact of the COVID-19 pandemic on the euro area labour market”, Economic Bulletin, Issue 5, ECB, 2020.

- Once this has taken place, however, aggregate productivity might benefit from such a reallocation of resources towards more productive sectors. Additionally, the COVID-19 shock might have a stronger impact on low-productivity firms, which could in principle have a positive effect on aggregate productivity. See Box 2 in the article entitled “The impact of COVID-19 on potential output in the euro area”, Economic Bulletin, Issue 7, ECB, 2020.

- In fact, in a recent survey of leading companies in the euro area, more remote working and an acceleration of digitalisation were the most frequently cited long-term supply-side effects of the pandemic (see the box entitled “The long-term effects of the pandemic: insights from a survey of leading companies” in this issue of the Economic Bulletin).