- RESEARCH BULLETIN NO. 92

- 24 FEBRUARY 2022

Monetary and macroprudential policies: trade-offs and interactions

There are always trade-offs to weigh up when taking monetary and macroprudential policy actions. The choice is between supporting the economy by ensuring a smooth supply of credit at favourable conditions, on the one hand, and containing financial stability risks, on the other hand. There are also significant spillovers between the two policies since they are both implemented and transmitted through the financial system. Monetary and macroprudential authorities need to take these interactions into account when deciding on interventions. Indeed, there are clear advantages of accounting for financial stability considerations when taking monetary policy decisions and limiting the constraints on the practical implementation of macroprudential policy.

Macroprudential policy trade-offs

The objective of macroprudential policy is to reduce the likelihood of systemic financial events, by limiting the build-up of financial stability risks and increasing the resilience of the financial sector. There is now ample evidence that macroprudential policies can indeed be effective in containing financial stability risks (see, for example, Ampudia et al., 2021). But in evaluating macroprudential policy effectiveness, relatively little emphasis is put on the potential costs required to lower the risks and therefore on the potential net benefits.

Recent research carried out within the European Central Bank (ECB) Research Task Force on monetary policy, macroprudential policy and financial stability sheds some light on the trade-offs involved in the implementation of macroprudential measures between reducing systemic risk and supporting economic growth. The purpose of this article is to highlight the main takeaways from the Research Task Force.

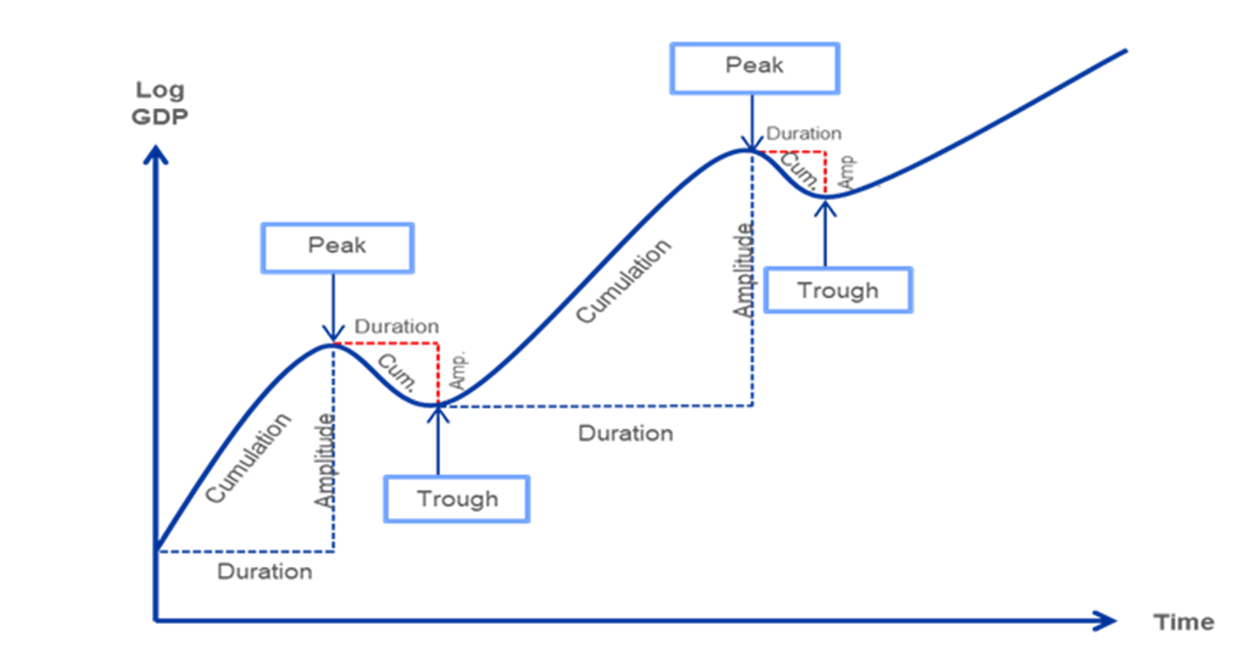

Gadea Rivas, Laeven and Peréz-Quirós (2020) show that there is a trade-off between the pace of credit growth and the level of risk associated with it. Economies experience recurrent expansions and recessions (see Chart 1). Credit growth affects both the length of expansions (duration) and the amplitude (severity) of recessions.[2] Rapid credit growth tends to be followed by deeper recessions, but it also has a direct positive impact on the duration of expansions and therefore on economic growth. One of the findings of the paper is that there is an optimal (intermediate) level of credit growth that can balance the positive and negative effects on economic growth. Hence, macroprudential policies should be used appropriately to manage the balance between deeper recessions and longer-term benefits for economic growth.

Chart 1

Macroprudential policy and the business cycle

Source: Gadea Rivas, Laeven, and Peréz-Quirós (2020).

Note: The figure illustrates the typical evolution of the economy over two expansions and two recessions.

In a similar vein, Chavleishvili et al. (2021) develop a macro-financial stress test framework which can be used to assess when the net effect of macroprudential interventions is beneficial. It takes into account interactions and non-linear effects between financial vulnerabilities, financial stress and GDP growth.

The evidence obtained strongly supports the need to correctly calibrate macroprudential instruments to ensure a sensible balance between the short-term costs of macroprudential policies and their long-term benefits.

Monetary policy trade-offs

Monetary policy measures also involve important trade-offs between supporting the intermediation capacity of banks, therefore ensuring a smooth transmission of monetary policy, on the one hand, and possibly increasing their vulnerabilities, on the other hand. The monetary policy stance affects banks’ risk-taking, with accommodative monetary policy generally inducing more risk-taking in financial markets (see Albertazzi et al., 2020, for a review of the evidence for the euro area). Recent evidence on this relationship suggests that unconventional monetary policy instruments, like asset purchases and negative interest rates, can have non-negligible side effects on financial stability.

Low interest rates generally encourage bank risk-taking, with negative rates having an even stronger effect, which is more pronounced for banks that rely more heavily on deposit funding (see, for example, Ampudia and Van den Heuvel, 2018; Bubeck, Maddaloni and Peydró, 2020; Heider, Saidi and Schepens, 2019; and Heider and Leonello, 2021). Recent empirical evidence in Mendicino et al. (2022) shows that the pass-through of central bank policy rate cuts to interest rates on corporate loans is weaker for banks with an initial low level of deposit rates. This is consistent with the evidence in Bittner et al. (2022) of a weaker pass-through to banks’ funding costs and stronger risk-taking incentives when interest rates on bank deposits are at low levels.

In recent years central banks have provided large amounts of liquidity to the banking sector. Central bank liquidity with longer maturities had a beneficial effect on bank lending, because it reduced the funding uncertainty faced by banks (see, for example, Jasova, Mendicino and Supera, 2021). At the same time, however, Jasova et al. (2022) show that a significant share of the collateral that banks used to obtain central bank liquidity was securities issued by other banks. This increased bank interconnectedness and systemic risk in the banking sector.[3]

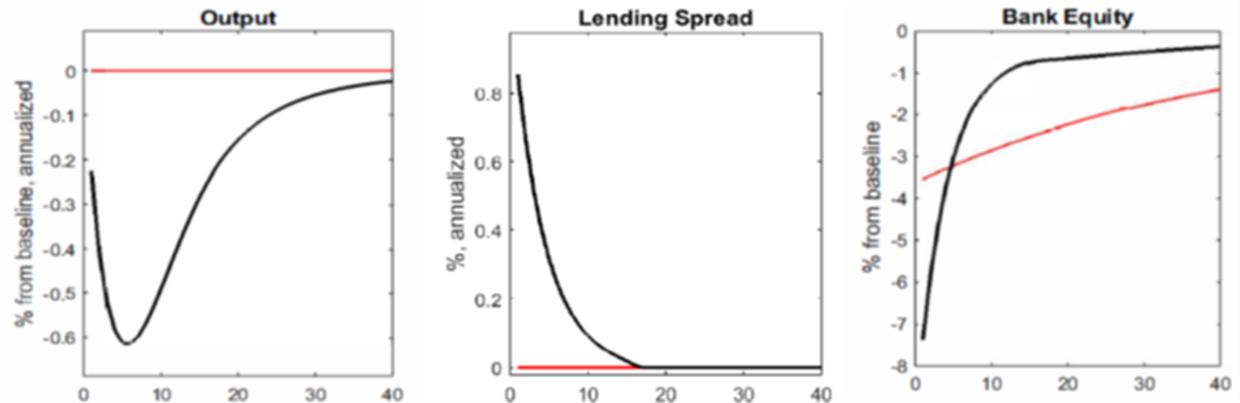

Central bank asset purchases can also have important consequences for bank vulnerability. Karadi and Nakov (2021) argue that asset purchases are effective in stabilising bank lending and economic output in response to financial shocks. At the same time, however, they tend to reduce bank profitability and thereby lengthen the time needed for banks to recapitalise (see Chart 2). Therefore, the exit from asset purchase programmes should ideally be gradual.

Chart 2

Central bank asset purchases in response to a financial shock

Source: Karadi and Nakov (2021).

Note: The chart displays the response to a financial shock with no asset purchase policy (black line) and with an optimal asset purchase policy (red line). Bank equity is measured at market value.

The interaction between monetary policy and macroprudential policy

Generally, the instruments of monetary policy and macroprudential policy both operate through the financial system. Therefore, there are potentially large interactions between the two policies (see Martin, Mendicino and Van der Ghote, 2021, for a review of the literature). For instance, Van der Ghote (2021) argues that (conventional) monetary policy interventions and macroprudential policy interventions can both help to safeguard financial stability. However, macroprudential policy is more targeted and therefore should be the first line of defence against the build-up of systemic financial vulnerabilities.

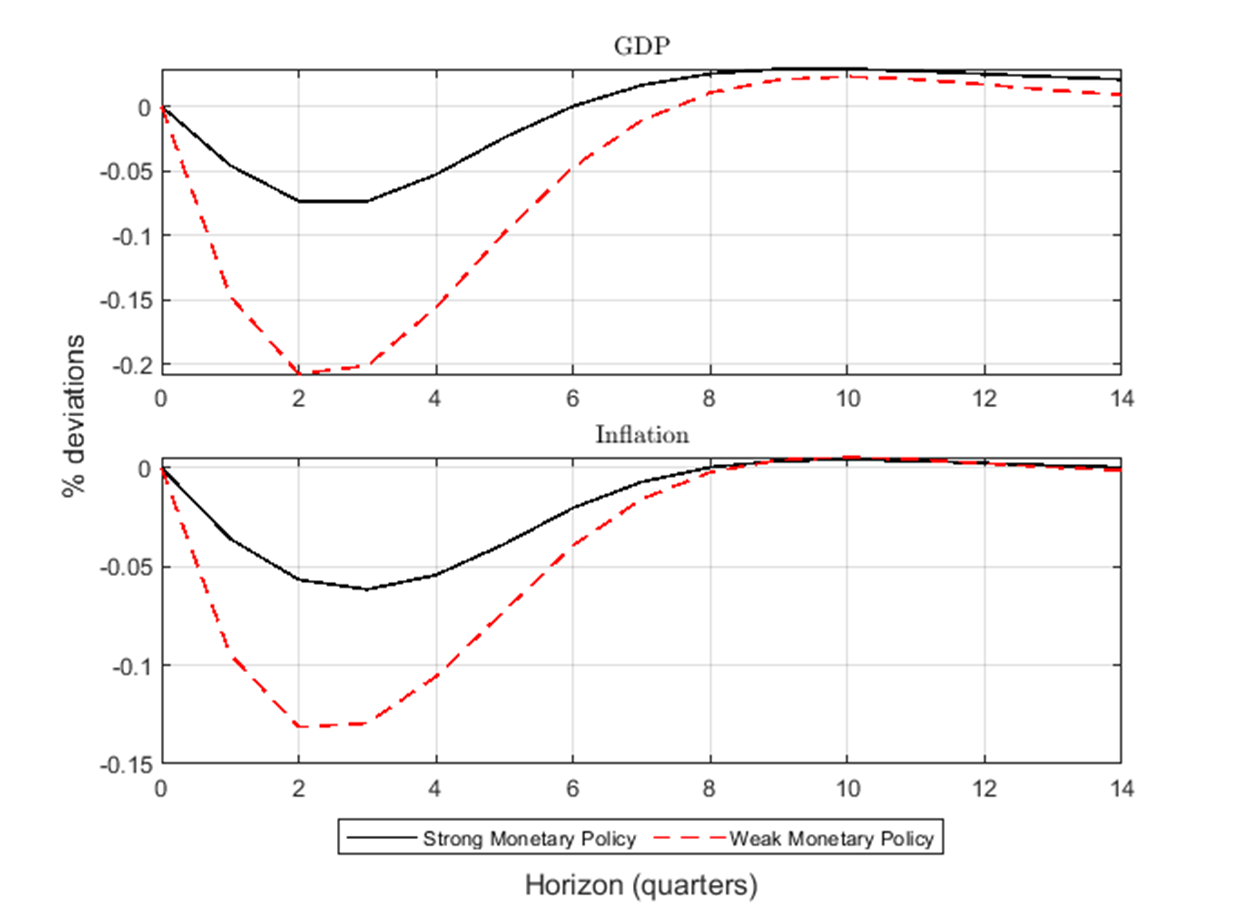

Monetary policy has an impact on the effectiveness of macroprudential policy. Mendicino et al. (2020) argue that, while higher capital requirements improve the stability of the banking sector and are therefore beneficial for the economy in the long run, they can constrain credit provision and limit economic expansion in the short run. In this situation, the degree of monetary policy accommodation is key to smooth the negative effects of tighter macroprudential policy (see Chart 3). When the monetary policy stance is accommodative, capital requirements can be tightened more with limited short-run costs for the economy. On the other hand, if accommodation is somehow constrained, for example because of an effective lower bound on the level of interest rates (i.e. a point at which it is not feasible to cut rates further), the short-run costs of tighter macroprudential policies may be large.[4]

Chart 3

The interaction of monetary policy and macroprudential policy

Source: Mendicino et al. (2020).

Notes: The graph displays the effects of a 1 percentage point increase in banks’ capital buffers over time. Accommodative monetary policy is shown by the black solid line, a constrained monetary policy is shown by the red dashed line.

Macroprudential policy can also have an impact on the transmission of monetary policy. In low interest rate environments, by containing systemic risk in financial markets, macroprudential policy also boosts the natural interest rate – the interest rate that supports the economy at full employment while keeping inflation constant – and hence helps mitigate the intensity of “liquidity traps” which arise when cash holdings are preferred to debt holdings (see Van der Ghote, 2020). In addition, bank leverage and risk exposure have an impact on the sensitivity of banks to monetary policy shocks. When their leverage is higher and their assets are riskier, banks’ net worth is more sensitive to monetary policy shocks. Conversely, higher capital requirements and a more resilient banking system dampen the transmission of monetary policy (see, for example, Cozzi et al., 2020).

The interaction of monetary policy and macroprudential policy also affects bank lending, resulting in strong complementarity between the two policies (see Altavilla, Laeven and Peydró, 2020). The effects of monetary policy easing on bank lending and risk-taking are greater when macroprudential policy is accommodative and are particularly strong for less capitalised banks.

Overall, monetary and macroprudential policies cannot be considered in isolation, as their transmission channels give rise to significant spillovers. The degree of monetary policy accommodation has an effect on the short-term impact of macroprudential policy and therefore on the macroprudential policy space. At the same time, there is evidence of complementarity of policies in response to a monetary policy easing.

Macroprudential policy should be the first line of defence against the build-up of systemic financial vulnerabilities (see, for example, Van der Ghote, 2021). In practice, however, the activation of macroprudential measures – notably (possibly) unpopular borrower-based measures – may encounter obstacles and implementation lags. These measures are also geographically restricted – implemented at the national level – and target a subsample of financial intermediaries. This highlights the importance of reducing limits on the practical implementation of macroprudential policy.

Conclusion

Recent research developed within the ECB Research Task Force on monetary policy, macroprudential policy and financial stability shows that monetary and macroprudential authorities must take account of important trade-offs and interactions when deciding on policy actions. Substantial progress has been made on developing practical frameworks of analysis to assess the costs and benefits of macroprudential and monetary policy interventions. At the same time, measuring excessiveness in risk-taking remains challenging. New state-of-the-art empirical and conceptual frameworks need to be developed to assess in a timely manner whether risk-taking is becoming excessive and leading to the build-up of systemic risk.

Another aspect for future consideration is the redistribution channels of the two policies. It would be useful to assess the different impact of these policies on borrowers and savers to provide further insights into the costs and benefits of interventions that target specific sectors or groups of economic agents. This would require new frameworks of analysis to be used to identify the most important differences in the transmission of policies across economic agents, as well as the implications of such redistribution channels.

References

Albertazzi, U., Barbiero, F., Marqués-Ibáñez, D., Popov, A., d’Acri, C. R. and Vlassopoulos, T. (2020), “Monetary policy and bank stability: the analytical toolbox reviewed”, Working Paper Series, No 2377, ECB.

Altavilla, C., Laeven, L. and Peydró, J.-L. (2020), “Monetary and macroprudential policy complementarities: evidence from European credit registers”, Working Paper Series, No 2504, ECB.

Ampudia, M. and Van der Heuvel, S. (2018), “Monetary policy and bank equity values in a time of low interest rates”, Working Paper Series, No 2199, ECB.

Ampudia, M., Duca, M. L., Farkas, M., Peréz-Quirós, G., Pirovano, M., Rünstler, G. and Tereanu, E. (2021), “On the effectiveness of macroprudential policy”, Working Paper Series, No 2559, ECB.

Bittner, C., Bonfim, D., Heider, F., Saidi, F., Schepens, G. and Soares, C. (2022), “The augmented bank balance-sheet channel of monetary policy”, ECB, mimeo.

Bubeck, J., Maddaloni, A. and Peydró, J.-L. (2020), “Negative monetary policy rates and systemic banks’ risk-taking: evidence from the euro area securities register”, Journal of Money, Credit and Banking, Vol. 52(S1), pp. 197-231.

Chavleishvili, S., Engle, R. F., Fahr, S., Kremer, M., Manganelli, S. and Schwaab, B. (2021), “The risk management approach to macro-prudential policy”, Working Paper Series, No 2565, ECB.

Corradin, S., Eisenschmidt, J., Hoerova, M., Linzert, T., Schepens, G. and Sigaux, J.-D. (2020), “Money markets, central bank balance sheet and regulation”, Working Paper Series, No 2483, ECB.

Cozzi, G., Darracq Pariès, M., Karadi, P., Körner, J., Kok, C., Mazelis, F., Nikolov, K., Rancoita, E., Van der Ghote, A. and Weber, J. (2020), “Macroprudential policy measures: macroeconomic impact and interaction with monetary policy”, Working Paper Series, No 2376, ECB.

Gadea Rivas, D. M., Laeven, L. and Peréz-Quirós, G. (2020), “Growth-and-risk trade-off”, Working Paper Series, No 2397, ECB.

Heider, F. and Leonello, A. (2021), “Monetary policy in a low-rate environment: Reversal rate and risk taking”, Working Paper Series, No 2593, ECB.

Heider, F., Saidi, F. and Schepens, G. (2019), “Life below zero: bank lending under negative policy rates”, The Review of Financial Studies, Vol. 32(10), pp. 3728-3761.

Jasova, M., Mendicino, C. and Supera, D. (2021), “Policy uncertainty, lender of last resort and the real economy”, Journal of Monetary Economics, Vol. 118, pp. 381-398.

Jasova, M., Laeven, L, Mendicino, C., Peydró, J.-L. and Supera, D. (2022), “Systemic risk and monetary policy: the haircut gap channel of the lender of last resort”, Working Paper Series, ECB, forthcoming.

Karadi, P. and Nakov, A. (2021), “Effectiveness and addictiveness of quantitative easing”, Journal of Monetary Economics, Vol. 117, pp. 1096-1117.

Martin, A., Mendicino, C. and Van der Ghote, A. (2021), “Interaction between monetary and macroprudential policies”, Working Paper Series, No 2527, ECB.

Mendicino, C., Nikolov, K., Suarez, J. and Supera, D. (2020), “Bank capital in the short and in the long run”, Journal of Monetary Economics, Vol. 115, pp. 64-79.

Mendicino, C., Puglisi, F. and Supera, D. (2022), “Beyond zero: are policy rate cuts still expansionary?”, Working Paper Series, ECB, forthcoming.

Van der Ghote, A. (2020), “Benefits of macro-prudential policy in low interest rate environments”, Working Paper Series, No 2498, ECB.

Van der Ghote, A. (2021) “Interactions and Coordination between Monetary and Macroprudential Policies”, American Economic Journal: Macroeconomics, Vol. 13(1), pp. 1-34.

- The article was written by Luc Laeven (Director General, Directorate General Research, European Central Bank), Angela Maddaloni (Head of Section, Directorate General Research, European Central Bank) and Caterina Mendicino (Senior Lead Economist, Directorate General Research, European Central Bank). This article summarises some of the key analytical findings and policy implications that have emerged from research by ECB staff conducted as part of the ECB Research Task Force (RTF) on monetary policy, macroprudential policy and financial stability. The views expressed here are those of the authors and do not necessarily represent the views of the European Central Bank and the Eurosystem.

- The amplitude and duration define the size of the cumulation which represents the total gain in wealth associated with the expansion/recession.

- Evidence in Corradin et al. (2020) suggests that ECB asset purchases have also affected money market conditions in the euro area.

- Cozzi et al. (2020) explore the interaction of bank capital requirements with monetary policy using a variety of macro-financial models developed at the ECB for policy analysis.