A revised weighting scheme for the international environment projections

Published as part of the ECB Economic Bulletin, Issue 7/2020.

The September 2020 ECB staff macroeconomic projections used a revised weighting scheme for the euro area’s trading partners.[1] The country weights are important for calculating foreign demand and the export prices of competitors. Both of these are used as conditioning assumptions in the macroeconomic projections for the euro area and for euro area countries.[2] This revision follows a recent enhancement of the method employed to calculate euro effective exchange rate indices. The latter was done to take account of the development of international trade linkages and, in particular, the growing importance of international trade in services.[3] This box discusses the impact of the revised weighting scheme on euro area foreign demand and export prices of competitors. It also touches upon updated weights used to calculate global aggregates for the purpose of the international environment projections prepared by ECB staff.

Two key conceptual changes were implemented in the calculation of country weights this year. First, data on trade in services were used in addition to data on trade in goods. Second, the number of euro area trading partners was increased from 30 to 42, while the remaining countries are consolidated in five regional aggregates. These changes increased the coverage of the euro area’s foreign demand by individual country data from 85% to 92%.

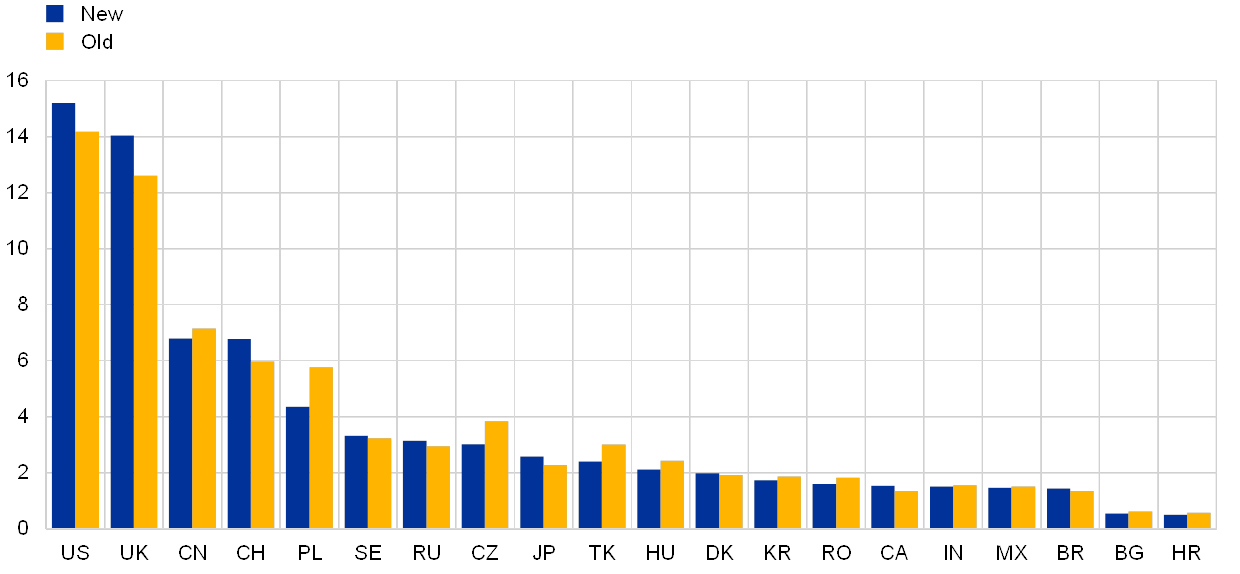

The inclusion of trade in services for the purposes of calculating the country weights reshuffled the weights of the euro area’s key trading partners. More specifically, the share of the United States and the United Kingdom has increased further so that together they account for 29.2% of the euro area’s foreign demand (see Chart A). Also, Switzerland now accounts for a similar share of euro area foreign demand to China, which by contrast has seen a slight decline in its weight compared to previous values. The weights have fallen for a number of countries, including Poland, the Czech Republic and Turkey, which are important euro area trading partners, but where bilateral trade in goods is greater than trade in services.

Chart A

Country weights in euro area foreign demand

(percentages)

Source: ECB calculations.

Note: The reported country weights for 20 important trading partners are used to calculate euro area foreign demand in the ECB/Eurosystem staff macroeconomic projections.

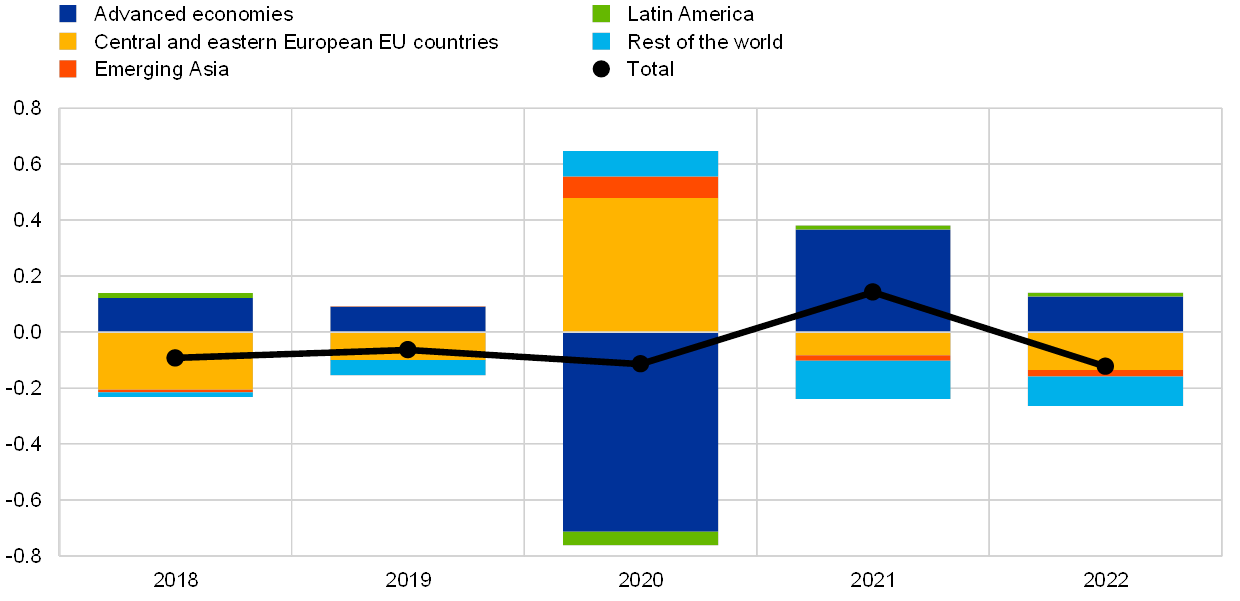

The impact of the revised weights on euro area foreign demand projections was relatively modest. Zooming in on the contribution of selected country groups, a higher weight for advanced economies (excluding the euro area) accentuated the role of the projected decline in imports in this group of countries for this year, which in turn weighed on euro area foreign demand (see Chart B). For 2021, the contribution of advanced economies turned positive. The negative impact from advanced economies in 2020 was largely due to the higher weight of the United Kingdom, where imports are projected to decline sharply this year, while contributions of non-euro area EU countries in central and eastern Europe moved in the opposite direction to advanced economies.

Chart B

Revisions to euro area foreign demand implied by changes in weights

(percentage points)

Source: ECB calculations.

Notes: Contributions to effective revisions of annual percentage growth. The weights of the five aggregates in euro area foreign demand are advanced economies 48.2%, emerging Asia 16.2%, Latin America 5%, central and eastern European EU countries 12.1% and rest of the world 18.5%. Before the update, the weights were 44.0%, 16.5%, 4.7%, 15.0% and 19.7% respectively. The figures refer to historical data and the September 2020 ECB staff projections.

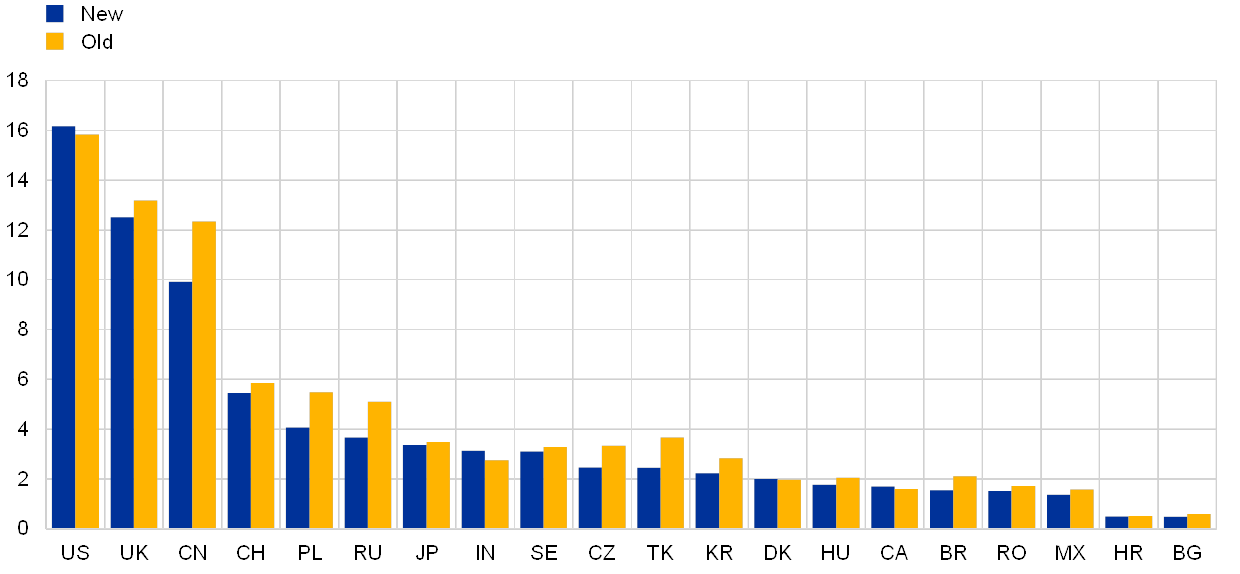

Furthermore, the impact of revised export weights on the export prices of euro area competitors was relatively contained. The weights used to compute this indicator are double-weighted to account for the national competitors in both the importing country and the other, non-euro area, exporting countries. As Chart C shows, the weights for China, the United Kingdom and a number of non-euro area EU countries in central and eastern Europe declined markedly. For this year, the revised weights imply an annual growth rate for the export prices of euro area competitors that is 0.3 percentage points lower, as implemented in the September 2020 ECB staff projections, while for the outer years of the projection horizon, revisions are marginal.

Chart C

Country weights of export prices of euro area competitors

(percentages)

Source: ECB calculations.

Notes: The reported country weights for 20 important trading partners are used to calculate the export prices of euro area competitors in the ECB/Eurosystem staff macroeconomic projections. The export weights of euro area competitors are double-weighted to account for third-market effects.

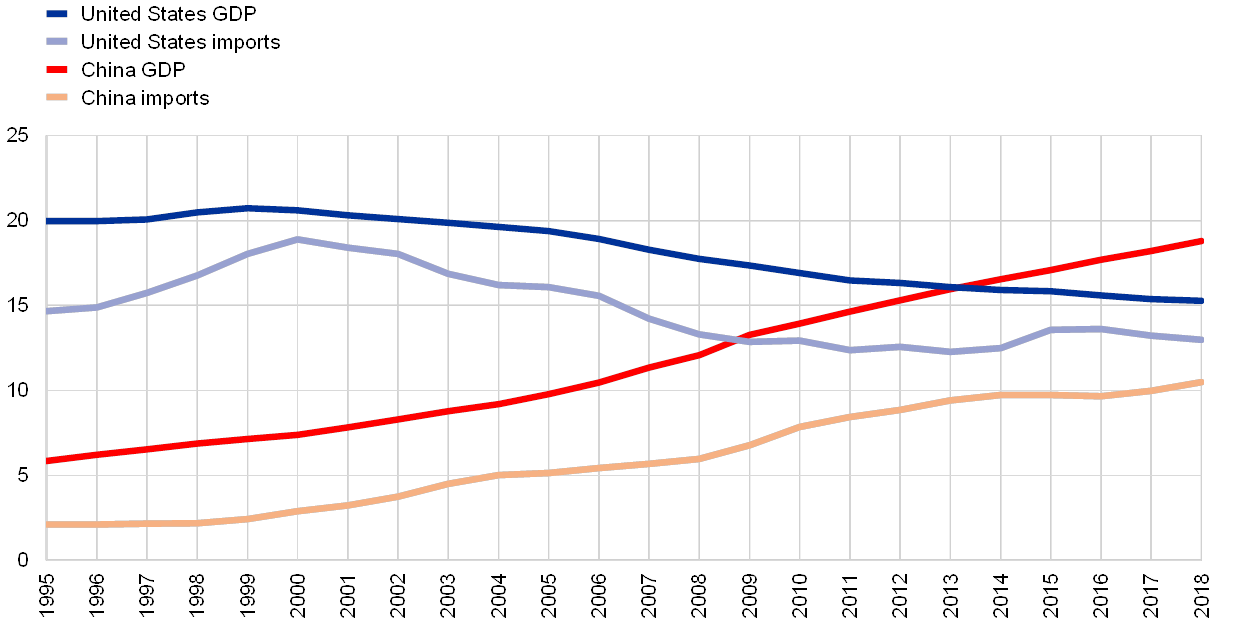

The global aggregates for GDP reported for the ECB staff international environment projections use a different set of weights, which were also updated. This update, based on GDP measures in purchasing power parity (PPP), further increased the shares of China in the global economy.[4] It now commands 21.2% in world real GDP (excluding the euro area), up from 20.7% the year before. China is also the top exporter (with a 14.5% weight in world exports excluding the euro area), while the United States remains the most important importer in the world economy (17% of world imports excluding the euro area).

Taking a longer term perspective, the development of shares of world output and trade over the last two decades shows the steady rise in the global economic weight of China and the downward trend of the United States.[5] In PPP terms, which accounts for differences in price levels between countries, China overtook the United States as the world’s largest economy in 2014 (see Chart D).[6] Import shares show a similar picture. While in 1999 there was an 18 percentage point gap between the two economies in favour of the United States, by 2018 this had narrowed to around 5 percentage points. While the decline of the United States’ weight in output and imports followed a similar trajectory, in the case of China, import shares have grown at a slower pace than its GDP weight. Assuming past (linear) trends continue, by 2022 Chinese import volumes would surpass those of the United States, while the wedge in GDP weights would rise further to around 7 percentage points.

Chart D

Long-term trends in world GDP and import shares

(percentages)

Sources: IMF World Economic Outlook and ECB calculations.

Note: The chart reports the shares of the United States and China in world GDP (in PPP terms) and import volumes.

- See Box 2, “The international environment”, ECB staff macroeconomic projections for the euro area, September 2020.

- For further details on the calculation of these assumptions and the methodology used to construct the weights, see Hubrich, K. and Karlsson, T., “Trade consistency in the context of the Eurosystem projection exercises an overview”, Occasional Paper Series, No 108, ECB, March 2010.

- For further details, see the box entitled “The ECB’s enhanced effective exchange rate measures”, Economic Bulletin, Issue 6, ECB, 2020.

- In contrast to market exchange rates, PPP measures are not directly observable. PPP weights, however, are less subject to short-term swings in foreign exchange markets and they are more appropriate for comparing non-traded goods and services and analysing welfare.

The global aggregates for GDP reported for the international environment are computed using PPP weights from the April 2020 IMF World Economic Outlook. For further details and the latest IMF update of world GDP weights, see Box 1.1 “Revised World Economic Outlook Purchasing-Power-Parity Weights”, World Economic Outlook, IMF, October 2020. - For comparison, the shares of the euro area in world GDP have also declined, from 17.7% in 1999 to 11.5% in 2018.

- This is not the case when considering GDP at market exchange rates, where the latest world shares of the United States and China are 24% and 15% respectively.