Niet beschikbaar in het Nederlands

Production of the ECB’s financial statements

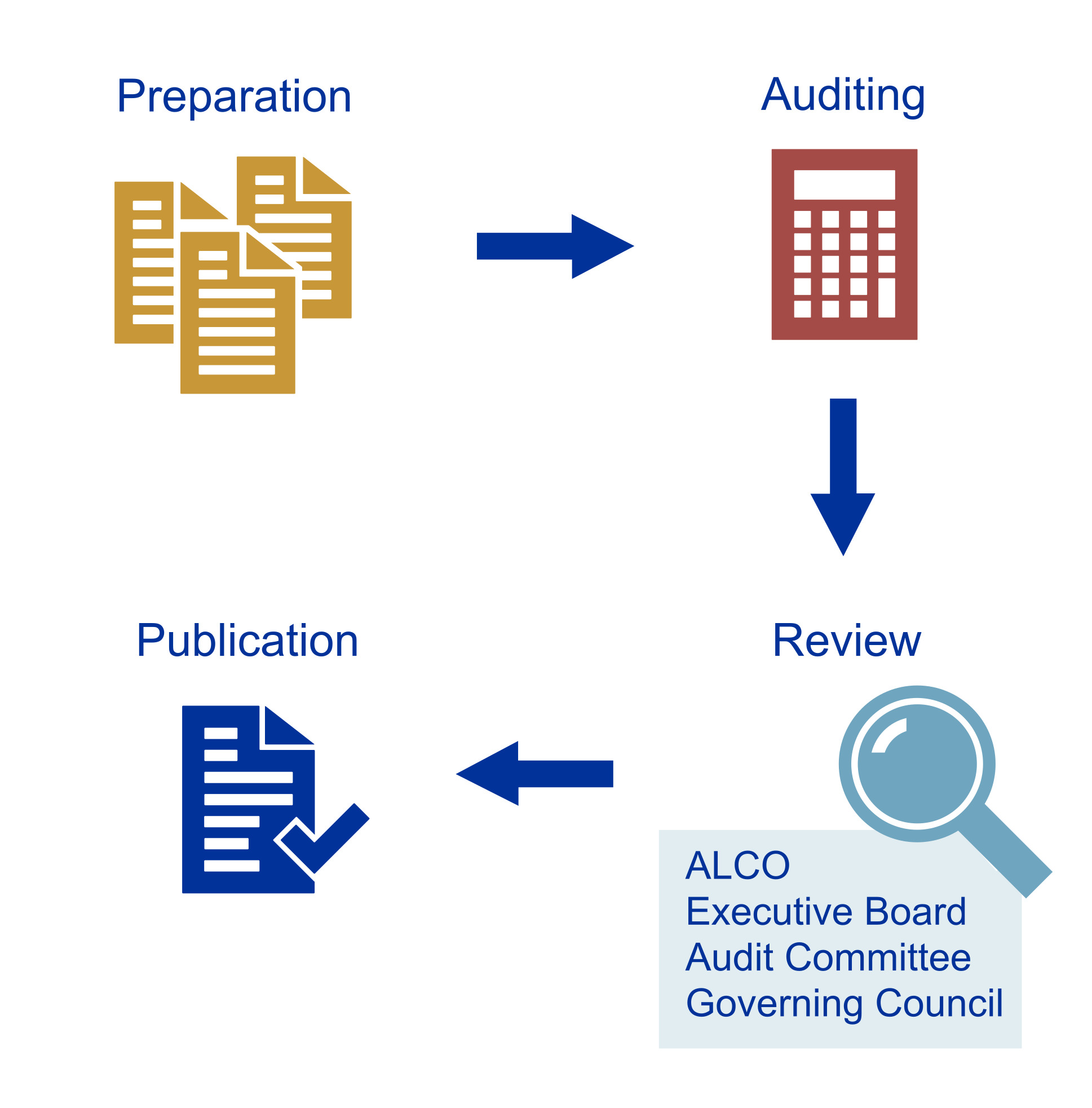

There are several steps to publishing our financial statements.

Preparation

The Directorate Finance is responsible for preparing the financial statements in cooperation with other teams at the ECB.

Auditing

Our financial statements are audited by an independent external auditor. The auditor is recommended by the Governing Council and approved by the EU Council.[1] Its responsibility is to express an opinion as to whether the financial statements give a true and fair view of the financial position of the ECB and of the results of its operations, in accordance with the accounting policies established by the Governing Council. The auditor examines our books and accounts, evaluates the adequacy of internal controls applied to the preparation and presentation of the financial statements, and assesses the appropriateness of the accounting policies used. The financial reporting processes and our financial statements may also be subject to internal audit.

Review

The ECB’s Assets and Liabilities Committee (ALCO) – composed of representatives from various departments at the ECB – systematically monitors and assesses all factors that may have an impact on our financial statements. The committee reviews our financial statements before they are submitted to the Executive Board for endorsement. And, after Executive Board authorisation, the financial statements, independent auditor’s report and all other relevant documentation are submitted to the Audit Committee.[2] Among other things, the Audit Committee supports the Governing Council in its responsibilities concerning the integrity of financial information and the oversight of internal controls.

In this context, the Audit Committee assesses the overall adequacy and effectiveness of the processes underlying the establishment of our financial statements and the overall adequacy of the associated disclosures.

The committee also reviews any significant accounting or financial reporting issues that could have an impact on our financial statements.

Publication

Once the Governing Council approves the financial statements, management report and note on the profit distribution/allocation of losses in February, we publish our Annual Accounts in full.

- To reinforce public assurance as to the independence of the ECB’s external auditors, we apply the principle of audit rotation, which means that we change our auditor after a set period of time.

- The Audit Committee is composed of up to six members: the Vice-President of the ECB, two senior governors of euro area national central banks and up to three external members chosen from among high-ranking officials with experience in central banking. For more information, see the Audit Committee mandate and the corporate governance page on our website.