What is behind the decoupling of global activity and trade?

Published as part of the ECB Economic Bulletin, Issue 5/2019.

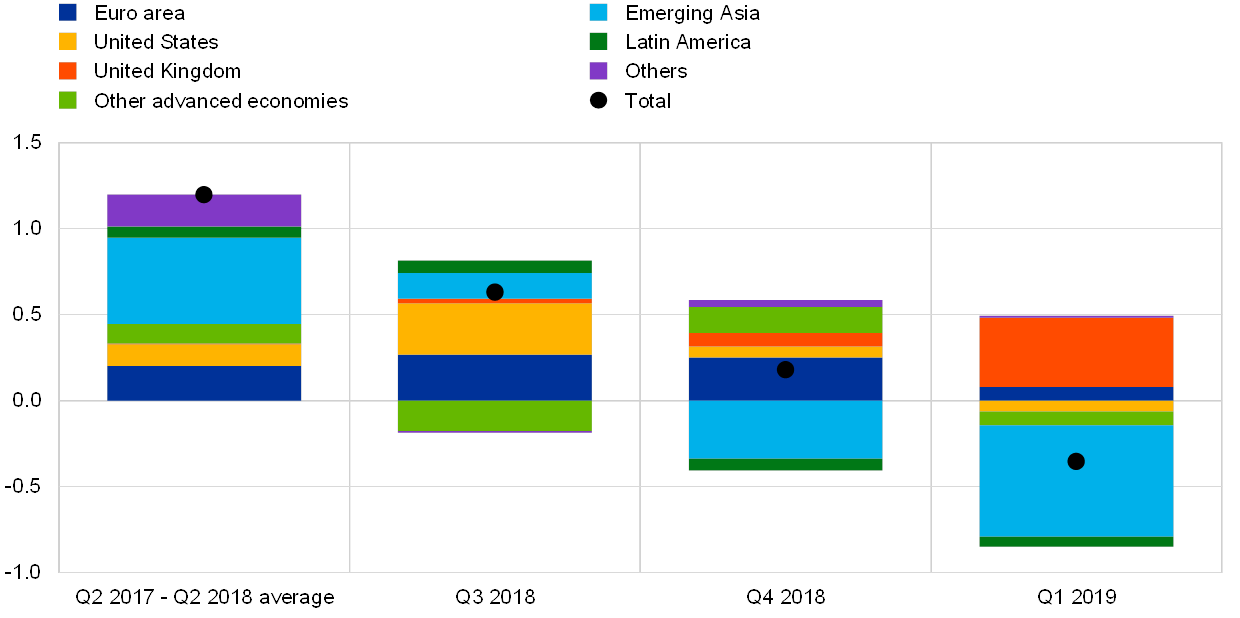

This box looks at the softness in global trade observed since the second half of 2018, focusing in particular on the causes of its decoupling from economic activity. Having already slowed in the third quarter of 2018, world trade contracted at the turn of the year (see Chart A). The deceleration was broad-based across regions. Trade deteriorated particularly sharply in China and in emerging Asia, which had recorded strong increases in 2017, but it also weakened in Latin America, Japan and the United States in the first quarter of 2019 (see Chart B). In contrast, import growth surged in the United Kingdom, probably owing to stock building by UK firms in the face of Brexit-related uncertainty. While global GDP growth has also slowed, the decline was less pronounced than for world trade. Due to significant movements in the most import-intensive categories of expenditure, such as investment and inventories, over the business cycle, trade can be subject to larger swings than activity (see Chart A). For example, world trade remained subdued in the period from the second quarter of 2014 to the third quarter of 2015, while in 2017 it significantly outstripped global activity growth. The decline in trade observed in recent quarters may reflect several factors. These include cyclical and compositional factors, but also influences stemming from rising trade tensions between the United States and China.[1] This box aims to shed light on the reasons behind the recent weakness in global trade and its decoupling from activity.

Chart A

World imports and world GDP

(quarterly percentage changes)

Sources: Haver Analytics and ECB calculations.

Chart B

World imports

(quarterly percentage changes)

Sources: Haver Analytics and ECB calculations.

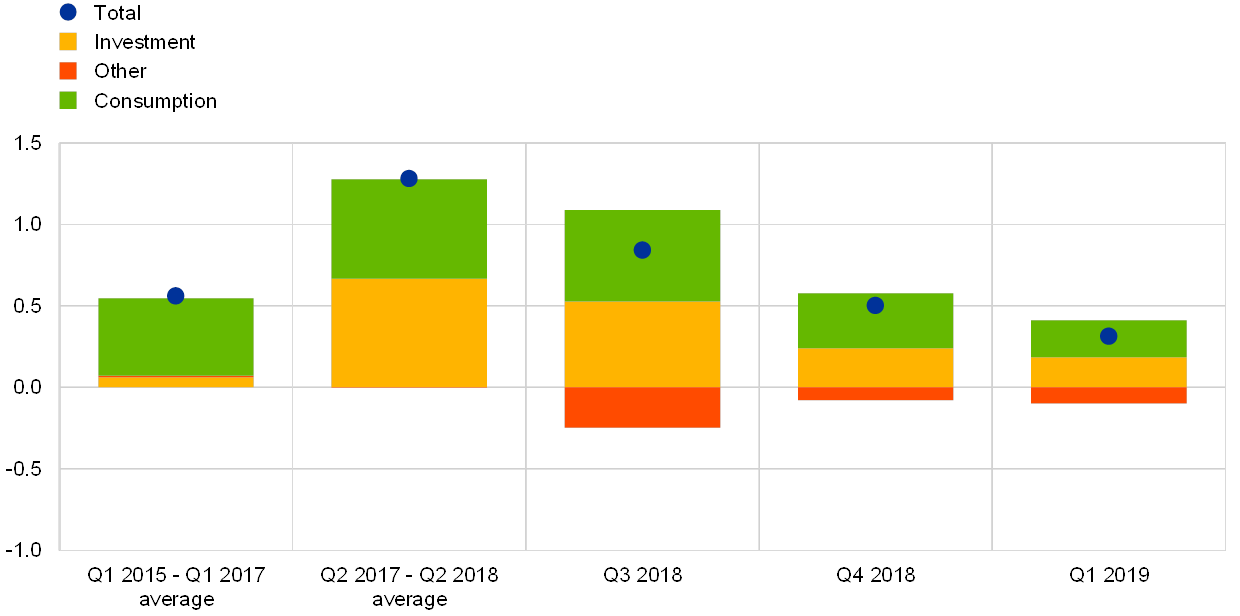

The decoupling of global trade and activity apparent since the second half of 2018 largely reflects a weakening of global investment, although consumption also softened at the turn of the year. Estimates from standard import-demand models suggest that both the previous rise in global trade in 2017 and the most recent slowdown since mid-2018 can be accounted for by large fluctuations in global investment (see Chart C). The recent decline has also occurred on the back of a fall in consumption in some emerging market economies (EMEs).

Chart C

World imports (excluding the euro area)

(average quarterly percentage changes)

Sources: World Input-Output Database (WIOD), Haver Analytics and ECB calculations.

Notes: Aggregation of 17 countries representing approximatively 65% of euro area foreign demand. China is not included in the sample. Due to the smaller sample composition, the aggregate of world trade differs from that shown in Charts A and B. Contributions are obtained from individual countries’ error-correction models. The models relate import volumes to domestic demand components, commodity prices and relative import prices. Following Bussière et al., “Estimating Trade Elasticities: Demand Composition and the Trade Collapse of 2008-2009”, American Economic Journal: Macroeconomics, Vol. 5(3), 2013, measures of import intensity-adjusted demand (IAD) are computed, by weighting the components of domestic demand according to their import content derived from global input-output tables. In order to capture long-term factors, such as shifts in non-price competitiveness or changes in trade openness, non-linear deterministic trends are also included in the long-run relationships. The long-term coefficient of the elasticity of imports to domestic demand is restricted to one. “Other” includes contributions from relative prices, the trend and unexplained factors.

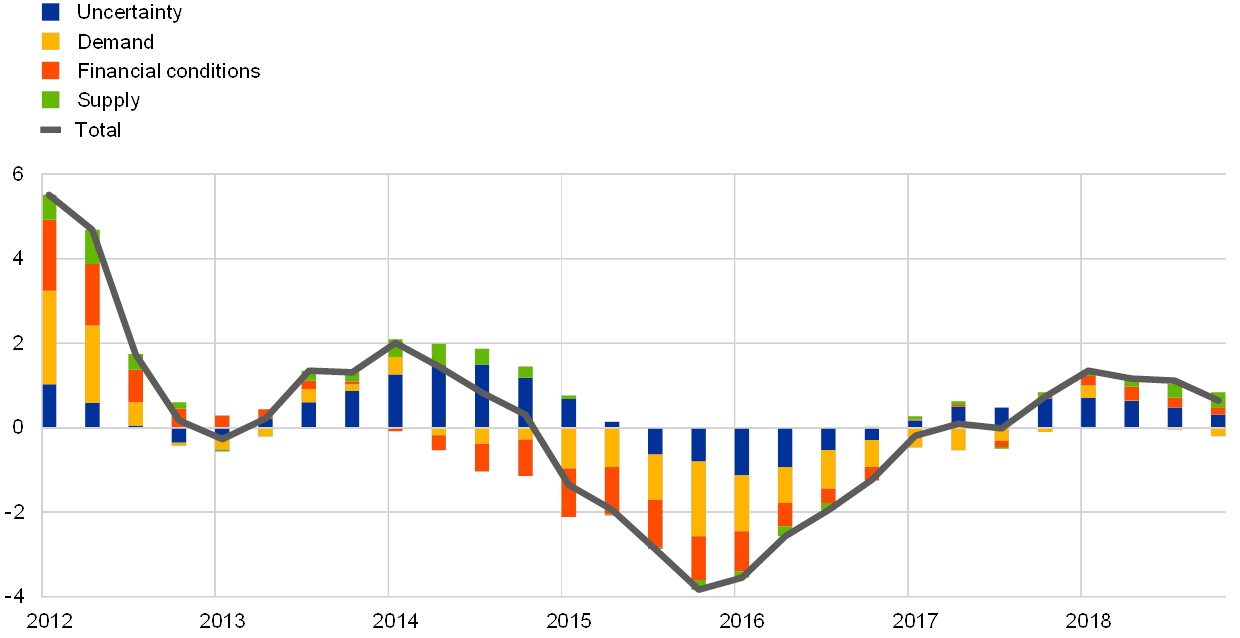

The slowdown in investment is likely to have been accentuated by a number of headwinds weighing on the global economy. In order to shed further light on the drivers of the recent slowdown in investment globally, two Bayesian panel vector autoregressive models are estimated, one for advanced economies (AEs) and one for EMEs. The methodology accounts for cross-country heterogeneity,[2] while the identification, based on sign restrictions, allows four main drivers of investment over time to be identified: uncertainty, financing conditions, demand shocks and supply shocks. The results of the models suggest that heightened uncertainty and tighter financing conditions explain to a large extent the slump in investment in both AEs and EMEs in the second half of 2018 (see Chart D). Weaker EME demand prospects amplified the slowdown.

From an output perspective, the deceleration in global investment has been mirrored by a sharp decline in manufacturing production. Much of the weakness in the global economy in recent quarters has been concentrated in the industrial sector, and within that in manufacturing output. In contrast, growth in the services sector has proved to be more resilient overall, although Purchasing Managers’ Index (PMI) indicators softened in the second quarter of this year. In the second half of 2018, industrial production contracted in Japan, in the euro area and in some Latin American countries. More recently, industrial production has also been slowing in the United States and China. Overall, countries with a larger industrial sector, greater exposure to industrial commodities and/or a heavy reliance on exports in GDP experienced sharper growth slowdowns. The investment and manufacturing cycles tend to be closely intertwined. Production in the manufacturing sector is highly capital-intensive, with capital goods forming a large part of manufacturing output. Therefore, it is not surprising that the slowdown in investment has been mirrored by a sharp decline in manufacturing output globally.

The global manufacturing slowdown was particularly pronounced in the electronics and automotive sectors and was also associated with a strong decline in trade flows in both sectors. As far as the automotive sector is concerned, the weakness at the global level partly reflected temporary factors, such as the bottlenecks in car production following the introduction of the new Worldwide Harmonised Light Vehicle Test Procedure (WLTP). However, medium-term structural trends, such as increasing environmental concerns and policies, may also have played a role. In addition, in China, the tax rebates on car purchases, which helped boost car sales in 2015-17, came to a halt in 2018. The weakness in the electronics cycle might relate to a slowing technological cycle in Asia, following a period of expansion in 2017 related to substantial investment in data centre capacity globally.

Chart D

Decomposition of changes in investment – main drivers

(annual percentage changes, percentage point contributions)

Sources: Haver Analytics and ECB calculations.

Notes: The chart is based on two Bayesian panel vector autoregressive models, one for advanced economies and one for emerging economies. This framework allows for cross-country heterogeneity. The countries included in the estimations are Canada, Japan, the United Kingdom, the United States, China, Turkey, Mexico and Brazil. The following variables are included: uncertainty, measured by the dispersion of growth expectations among professional forecasters; financial conditions indices; expected growth; business investment; and price developments. Structural shock identification is achieved by means of zero and sign restrictions. Global investment is shown in deviation from trend/steady state and is based on an aggregation of country-specific results based on GDP weights.

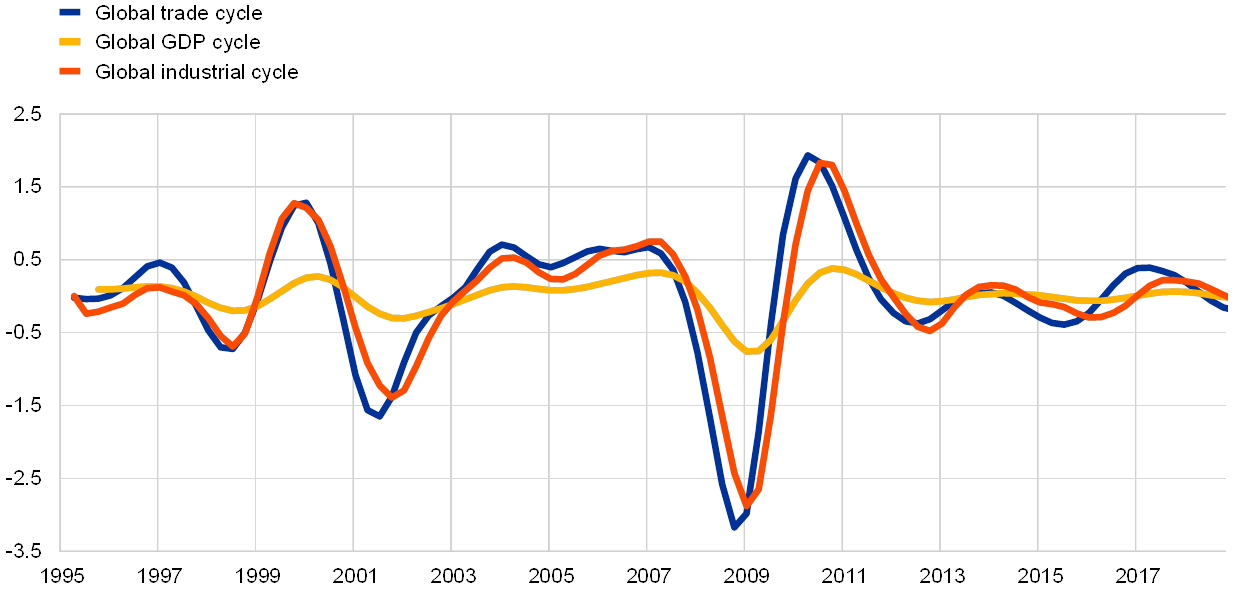

Manufacturing and trade cycles tend to be highly correlated. This implies that swings in manufacturing output can have a significantly larger impact on global trade than on activity. The manufacturing sector remains highly trade-intensive, as imports of manufacturing goods account for more than 50% of total gross global imports, but only make up 20% of total world value added. Hence, a sharp slowdown in manufacturing output leads to a more pronounced decline in global trade than in global GDP. ECB staff analysis indicates that industrial and trade cycles tend to be highly correlated, with world industrial output generally displaying higher trade elasticity than global GDP (see Chart E).

Chart E

Global trade and industrial cycles

(quarterly percentage changes)

Sources: Haver Analytics and ECB calculations based on Borin et al., “The cyclicality of the Income Elasticity of Trade”, Working Papers, No 1126, Banca d’Italia, July 2017.

Notes: Cycles are obtained by simple Hodrick-Prescott (HP) filtering on log GDP, trade and industrial production. The latest observation is for the fourth quarter of 2018.

Despite some signs of recovery, global trade is likely to remain more subdued than activity in coming quarters. High frequency indicators of world trade point to some recovery in the near term. However, this is expected to be mild, with trade growth picking up only gradually owing to a subdued outlook for investment in many economies. In addition, downside risks to the outlook for trade have partially materialised in recent months due to the implementation of higher tariffs, and the threat of a further escalation of trade tensions persists.

- For a detailed discussion of the macroeconomic implications of rising protectionism, see the article entitled “The economic implications of rising protectionism: a euro area and global perspective”, Economic Bulletin, Issue 3, ECB, 2019.

- For a detailed explanation of the benchmark methodology and data, see the box entitled “Investment dynamics in advanced economies since the financial crisis”, Economic Bulletin, Issue 6, ECB, 2017.