- PRESS RELEASE

- 14 July 2020

July 2020 euro area bank lending survey

- Credit standards for loans to firms remain favourable, supported by fiscal and monetary measures

- Surge in firms’ demand for loans continues to reflect emergency liquidity needs

- Credit standards for loans to households tighten further

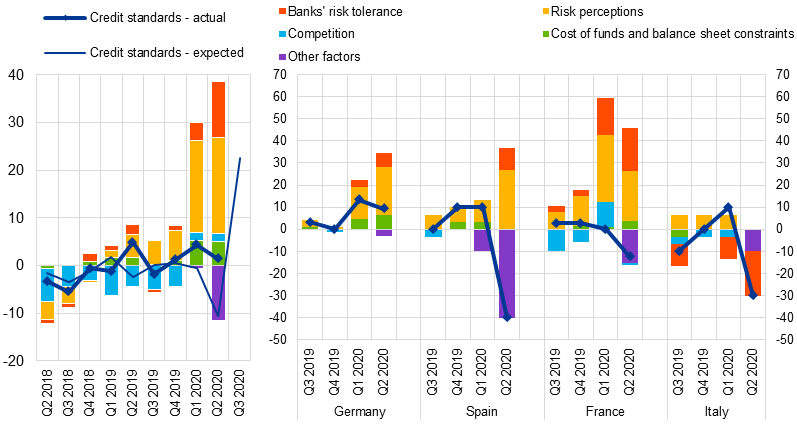

Credit standards – i.e. banks’ internal guidelines or loan approval criteria – remained broadly unchanged for loans to enterprises (see Chart 1), while tightening further for loans to households for house purchase, consumer credit and other lending to households in the second quarter of 2020, according to the July 2020 bank lending survey (BLS). Banks reported that government loan guarantees played a significant role in most countries for maintaining favourable credit standards for loans to enterprises. Credit standards for loans to households tightened further (a net percentage of 22% for loans to households for house purchase and of 26% for consumer credit and other lending to households). Banks continued to indicate the deteriorated economic outlook, worsened creditworthiness of borrowers and a lower risk tolerance as relevant factors for the tightening of their credit standards for loans to enterprises and households.

In the third quarter of 2020, banks expect a considerable net tightening of credit standards on loans to enterprises, which is reported to be related to the expected end of state guarantee schemes in some large euro area countries. At the same time, the uncertainty of the impact of the coronavirus pandemic still remains high. The net tightening of credit standards on loans to households is expected to continue in the third quarter of 2020.

Overall terms and conditions applied by banks – i.e. the actual terms and conditions agreed in loan contracts tightened slightly in the second quarter of 2020 for new loans to enterprises, while tightening more for housing loans and consumer credit.

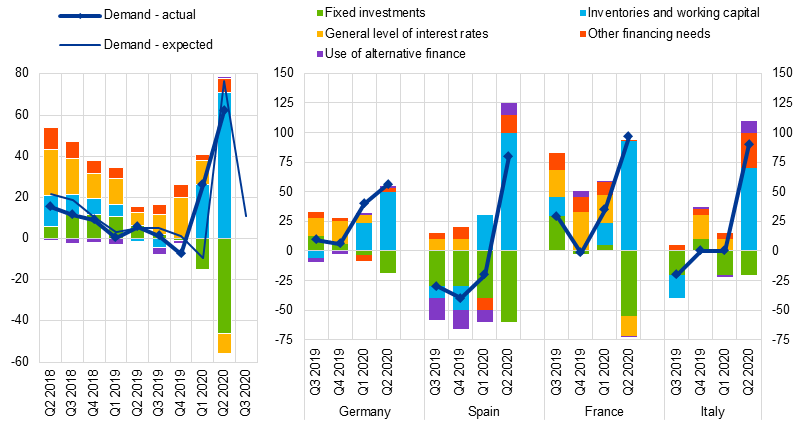

Demand from firms for loans or drawing of credit lines surged further in the second quarter of 2020, reaching the highest net balance since the survey was launched in 2003 (see Chart 2). This reflects the particularly strong emergency liquidity needs of firms and possibly precautionary build-up of liquidity buffers during the period when lockdown measures were in force across the euro area. Banks reported that financing needs for inventories and working capital were the main factor underlying the loan demand from firms, which more than offset the negative contribution to loan demand from fixed investment. Net demand for housing loans declined strongly in the second quarter of 2020 and the net demand for consumer credit and other lending to households reached a record low since the survey was launched in 2003. The demand for loans from households was dampened by weaker consumer confidence, worsened housing market prospects and lower spending on durable goods.

Banks expect that net demand for loans to enterprises will increase less in the third quarter of 2020. Banks also expect an increase in net demand for housing loans and in particular for consumer credit and other lending to households in the third quarter of 2020.

Banks reported that non-performing loans (NPLs) had a tightening impact on credit standards and on terms and conditions for all loan categories in the first half of 2020. Risk perceptions and risk aversion related to the general economic outlook and borrowers’ creditworthiness were the main drivers of the tightening impact of NPL ratios.

The euro area bank lending survey, which is conducted four times a year, was developed by the Eurosystem in order to improve its understanding of banks’ lending behaviour in the euro area. The results reported in the July 2020 survey relate to changes observed in the second quarter of 2020 and expected changes in the third quarter of 2020, unless otherwise indicated. The July 2020 survey round was conducted between 5 and 23 June 2020. A total of 144 banks were surveyed in this round, with a response rate of 100%.

For media queries, please contact Silvia Margiocco, tel.: +49 69 1344 6619.

Notes

- A report on this survey round is available at https://www.ecb.europa.eu/stats/ecb_surveys/bank_lending_survey/html/index.en.html. A copy of the questionnaire, a glossary of BLS terms and a BLS user guide with information on the BLS series keys can also be found on that web page.

- The euro area and national data series are available on the ECB’s website via the Statistical Data Warehouse (http://sdw.ecb.europa.eu/browse.do?node=9691151). National results, as published by the respective national central banks, can be obtained via https://www.ecb.europa.eu/stats/ecb_surveys/bank_lending_survey/html/index.en.html.

- For more detailed information on the bank lending survey, see Köhler-Ulbrich, P., Hempell, H. and Scopel, S., “The euro area bank lending survey”, Occasional Paper Series, No 179, ECB, 2016 (http://www.ecb.europa.eu/pub/pdf/scpops/ecbop179.en.pdf).

Changes in credit standards for loans or credit lines to enterprises and contributing factors

(net percentages of banks reporting a tightening of credit standards and contributing factors)

Source: ECB (BLS).

Notes: Net percentages are defined as the difference between the sum of the percentages of banks responding “tightened considerably” and “tightened somewhat” and the sum of the percentages of banks responding “eased somewhat” and “eased considerably”. The net percentages for the "other factors" refer to further factors which were mentioned by banks as having contributed to changes in credit standards, currently mainly related to the COVID-19 pandemic.

Changes in demand for loans or credit lines to enterprises and contributing factors

(net percentages of banks reporting an increase in demand and contributing factors)

Source: ECB (BLS).

Notes: Net percentages for the questions on demand for loans are defined as the difference between the sum of the percentages of banks responding “increased considerably” and “increased somewhat” and the sum of the percentages of banks responding “decreased somewhat” and “decreased considerably”.

Eiropas Centrālā banka

Komunikācijas ģenerāldirektorāts

- Sonnemannstrasse 20

- 60314 Frankfurt am Main, Germany

- +49 69 1344 7455

- media@ecb.europa.eu

Pārpublicējot obligāta avota norāde.

Kontaktinformācija plašsaziņas līdzekļu pārstāvjiem