- PRESS RELEASE

Results of the December 2023 Survey on credit terms and conditions in euro-denominated securities financing and over-the-counter derivatives markets (SESFOD)

2 February 2024

- Credit terms and conditions unchanged while expected to tighten over the period from September to November 2023

- Financing rates and maximum maturity of funding higher

- Market-making activities over the past year higher for many debt securities and derivatives

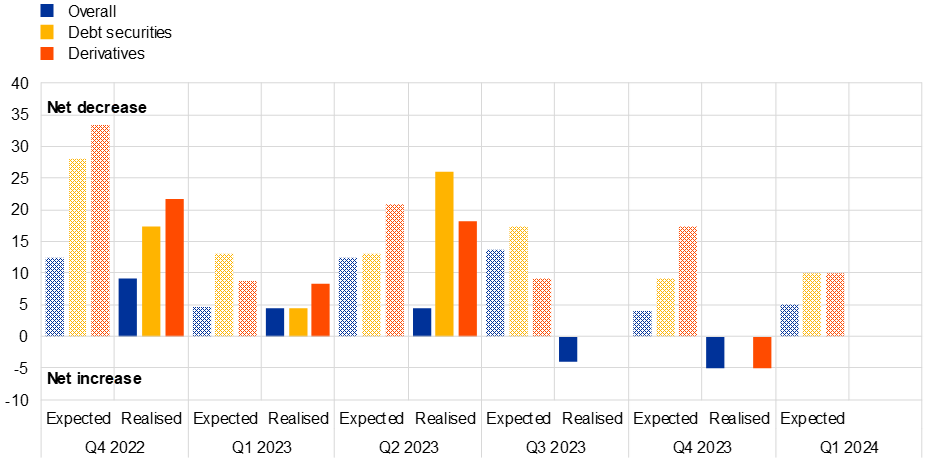

Overall credit terms and conditions offered to different counterparty types remained on balance unchanged between September and November 2023, contrasting with the expectations of further tightening expressed in the September 2023 survey. Survey respondents expected overall credit terms to tighten over the period from December 2023 to February 2024.

Chart 1

Realised and expected quarterly changes in overall credit terms and price/non-price terms offered to counterparties across all transaction types

(Q4 2022 to Q1 2024; net percentages of survey respondents)

Source: ECB.

Note: Net percentages are calculated as the difference between the percentage of respondents reporting “tightened somewhat” or “tightened considerably” and the percentage reporting “eased somewhat” or “eased considerably”.

Survey respondents reported an increase in the maximum amount of funding secured against high-quality government bonds for most-favoured clients, while the picture was more mixed as regards the maximum amount of funding offered against other euro-denominated collateral types. Respondents also reported an increase in the maximum maturity of funding secured against government bonds for most-favoured clients but few changes as regards the maximum maturity of funding for other collateral types. Haircuts applied to euro-denominated collateral either increased or remained unchanged for almost all types of collateral but decreased for government bonds. Financing rates/spreads increased significantly for funding secured against all types of collateral.

Survey participants reported an increase in the use of central counterparties (CCPs) for securities financing transactions involving collateral in the form of domestic government bonds. They reported an increase in overall demand for funding – particularly funding secured against domestic and high-quality government bonds, high-quality financial corporate bonds as well as equities. The liquidity and functioning of collateral markets deteriorated for almost all collateral types.

As for non-centrally cleared over-the-counter (OTC) derivatives, survey respondents reported that initial margin requirements had increased slightly for all derivative types except credit derivatives, for which they had remained unchanged. Respondents reported almost no changes in liquidity and trading for most derivative types. Some respondents reported that terms in new or renegotiated master agreements had eased as regards acceptable collateral while they had remained unchanged for all other elements.

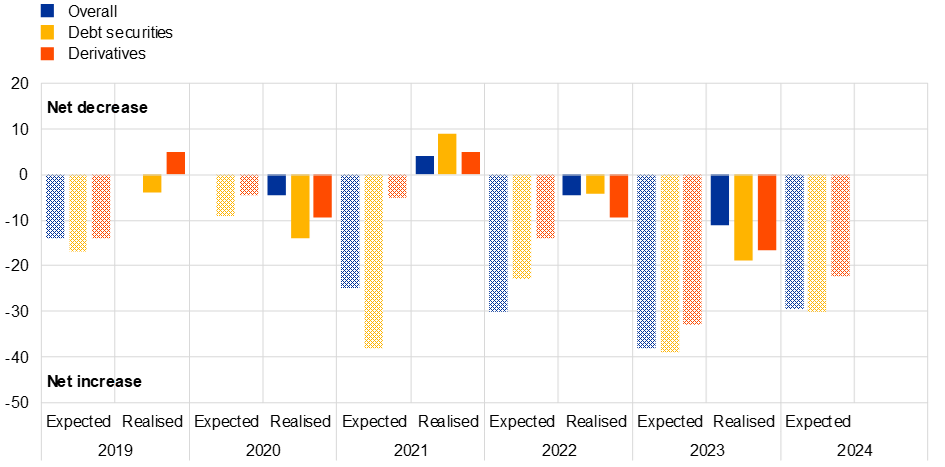

Finally, turning to the special questions about market-making activities included in each Q4 survey round since December 2013, survey respondents reported in December 2023 that their market-making activities over the past year had generally increased. Market-making activities increased in particular for domestic government bonds and high-quality non-financial corporate bonds, but decreased for convertible securities, high-yield corporate bonds and non-domestic government, sub-national and supra-national bonds. Market-making activities are expected to increase in 2024 for most types of debt securities and derivatives, except for convertible securities and non-domestic, sub-national and supra-national bonds.

Chart 2

Realised and expected annual changes in market-making activities

(2022 to 2024 net percentages of survey respondents)

Source: ECB.

Note: The net percentage is defined as the difference between the percentage of respondents reporting "decreased considerably" or "decreased somewhat" and those reporting "increased somewhat" and "increased considerably".

Survey participants cited the willingness of institutions to take on risk as the main driver of an increase in market-making activities over the past year. The willingness to take on risk, the profitability of market-making activities and the availability of balance sheet or capital were the largest factors behind expected increases in market-making activities in the year ahead.

Respondents expressed confidence in their ability to act as market-makers in times of stress for all types of debt securities and for derivatives. The current results match the expectations of the previous two surveys in terms of confidence in their market-making abilities. Willingness to take on risk remained the main reason for banks’ confidence in this regard.

The results of the December 2023 SESFOD survey, the underlying detailed data series and the SESFOD guidelines are available on the European Central Bank’s website, together with all other SESFOD publications.

The SESFOD survey is conducted four times a year and covers changes in credit terms and conditions over three-month reference periods ending in February, May, August and November. The December 2023 survey collected qualitative information on changes between September and November 2023. The results are based on the responses received from a panel of 25 large banks, comprising 13 euro area banks and 12 banks with head offices outside the euro area.

For media queries, please contact Francois Peyratout, tel.: +49 69 1344 8948.

Ευρωπαϊκή Κεντρική Τράπεζα

Γενική Διεύθυνση Επικοινωνίας

- Sonnemannstrasse 20

- 60314 Frankfurt am Main, Germany

- +49 69 1344 7455

- media@ecb.europa.eu

Η αναπαραγωγή επιτρέπεται εφόσον γίνεται αναφορά στην πηγή.

Εκπρόσωποι Τύπου