Economic Bulletin Issue 5, 2020

Update on economic and monetary developments

Summary

Incoming information since the last monetary policy meeting in early June signals a resumption of euro area economic activity, although the level of activity remains well below the levels prevailing before the coronavirus (COVID-19) pandemic and the outlook remains highly uncertain. Headline inflation is being dampened by lower energy prices and price pressures are expected to remain very subdued on account of the sharp decline in real GDP growth and the associated significant increase in economic slack. The ECB’s monetary policy measures are gradually making their way through to the euro area economy, providing crucial support to the recovery and helping to offset the pandemic-related downward shift in the projected path of inflation. At the same time, the outlook is surrounded by high uncertainty and subject to downside risks. Against this background, the Governing Council decided to leave the overall monetary policy stance unchanged and to reconfirm the full set of its existing monetary policy measures.

While containment policies have been eased across the world, the global recovery remains uneven, uncertain and incomplete. Survey data suggest that the unprecedented contraction in the global economy in the first half of 2020 has been bottoming out, while cautious consumer behaviour points to sluggish growth momentum ahead. While the recovery is proceeding in China, the outlook remains highly uncertain in the United States, although there have been some positive data surprises. In the United Kingdom and Japan, indicators also point to a bottoming-out of the contraction in some sectors, but activity levels remain very weak. In this context, global inflation remains subdued.

Over the review period, the forward curve of the euro overnight index average (EONIA) shifted slightly downwards and a mild inversion appeared at short maturities, albeit without expectations of an imminent cut in policy rates. Long-term euro area sovereign bond yields also declined on account of lower risk-free rates and sovereign spreads recorded a slight compression. Equities continued to recover from the troughs reached in March and, despite compressing further, corporate bond spreads are still wider than they were in late February. In foreign exchange markets, the euro strengthened slightly in trade-weighted terms.

Incoming data and survey results suggest that economic activity improved significantly in May and June from its trough in April, alongside the ongoing containment of the virus and the associated easing of the lockdown measures. At the same time, economic indicators remain well below the levels recorded before the pandemic, and the recovery is in its early stages and remains uneven across sectors and jurisdictions. After decreasing by 3.6%, quarter on quarter, in the first quarter of 2020, euro area real GDP is expected to have contracted even further overall in the second quarter, broadly in line with the June 2020 Eurosystem staff macroeconomic projections. Signs of a recovery in consumption have emerged, while there has also been a significant rebound in industrial output. At the same time, subdued labour market conditions and precautionary household saving are weighing on consumer spending. Weak business prospects and high uncertainty are dampening investment, while the weakness in the global economy is hampering foreign demand for euro area goods and services.

According to Eurostat’s flash estimate, euro area annual HICP inflation increased from 0.1% in May to 0.3% in June, mainly reflecting less negative energy price inflation. On the basis of current and futures prices for oil and taking into account the temporary reduction in the German VAT rate, headline inflation is expected to decline again in the coming months before rebounding in early 2021. Over the medium term, weaker demand will put downward pressure on inflation, which will be only partially offset by upward pressures related to supply constraints. Market-based indicators of longer-term inflation expectations have remained at subdued levels.

Since March 2020 the coronavirus pandemic has caused monetary dynamics to accelerate sharply, driven by businesses’ acute liquidity needs to finance ongoing expenditures and economic agents’ strong preference for money holdings on precautionary grounds. In May domestic credit remained the main source of money creation, which was driven in particular by loans to non-financial corporations and the Eurosystem’s net purchases of government securities under the asset purchase programmes. The July 2020 euro area bank lending survey shows a continued upward impact of the pandemic on firms’ loan demand, largely reflecting emergency liquidity needs. At the same time, credit standards for loans to firms have remained favourable, supported by fiscal and monetary measures. In addition, very favourable lending rates, which point to an ongoing robust transmission of monetary policy measures, are supporting euro area economic growth.

Against this background, ample monetary stimulus remains necessary to support the economic recovery and to safeguard medium-term price stability. Therefore, the Governing Council decided to reconfirm its very accommodative monetary policy stance.

The Governing Council will keep the key ECB interest rates unchanged. They are expected to remain at their present or lower levels until the inflation outlook has robustly converged to a level sufficiently close to, but below, 2% within the projection horizon, and such convergence has been consistently reflected in underlying inflation dynamics.

The Governing Council will continue its purchases under the pandemic emergency purchase programme (PEPP) with a total envelope of €1,350 billion. These purchases contribute to easing the overall monetary policy stance, thereby helping to offset the pandemic-related downward shift in the projected path of inflation. The purchases will continue to be conducted in a flexible manner over time, across asset classes and among jurisdictions. This allows the Governing Council to effectively stave off risks to the smooth transmission of monetary policy. The Governing Council will conduct net asset purchases under the PEPP until at least the end of June 2021 and, in any case, until it judges that the coronavirus crisis phase is over. The Governing Council will reinvest the principal payments from maturing securities purchased under the PEPP until at least the end of 2022. In any case, the future roll-off of the PEPP portfolio will be managed to avoid interference with the appropriate monetary policy stance.

Net purchases under the asset purchase programme (APP) will continue at a monthly pace of €20 billion, together with the purchases under the additional €120 billion temporary envelope until the end of the year. The Governing Council continues to expect monthly net asset purchases under the APP to run for as long as necessary to reinforce the accommodative impact of the policy rates, and to end shortly before it starts raising the key ECB interest rates. The Governing Council intends to continue reinvesting, in full, the principal payments from maturing securities purchased under the APP for an extended period of time past the date when it starts raising the key ECB interest rates, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

The Governing Council will also continue to provide ample liquidity through its refinancing operations. In particular, the latest operation in the third series of targeted longer-term refinancing operations (TLTRO III) has registered a very high take-up of funds, supporting bank lending to firms and households.

The monetary policy measures that the Governing Council has taken since early March are providing crucial support to underpin the recovery of the euro area economy and to safeguard medium-term price stability. In particular, they support liquidity and funding conditions in the economy, help to sustain the flow of credit to households and firms, and contribute to maintaining favourable financing conditions for all sectors and jurisdictions. In addition, the European Commission has recently published some guidelines for government guarantee schemes in order to avoid potential cliff effects during their phasing-out. At the same time, in the current environment of elevated uncertainty and significant economic slack, the Governing Council remains fully committed to doing everything necessary within its mandate to support all citizens of the euro area through this extremely challenging time. This applies first and foremost to its role in ensuring that monetary policy is transmitted to all parts of the economy and to all jurisdictions in the pursuit of its price stability mandate. The Governing Council, therefore, continues to stand ready to adjust all of its instruments, as appropriate, to ensure that inflation moves towards its aim in a sustained manner, in line with its commitment to symmetry.

1 External environment

While containment policies have eased across the world, the global recovery remains uneven, uncertain and incomplete. The global outlook remains dominated by the evolution of the coronavirus (COVID-19) pandemic. The number of new cases continues to rise globally, particularly in the United States and Latin America, as well as in several other key emerging market economies (e.g. India and South Africa). At the same time, indicators of effective lockdown measures, which reflect official policies with actual mobility data, suggest a steady and gradual opening up in most economies since end-May. This combination of the easing of containment measures and the increase in new COVID-19 cases in many countries renders the global recovery highly uncertain.

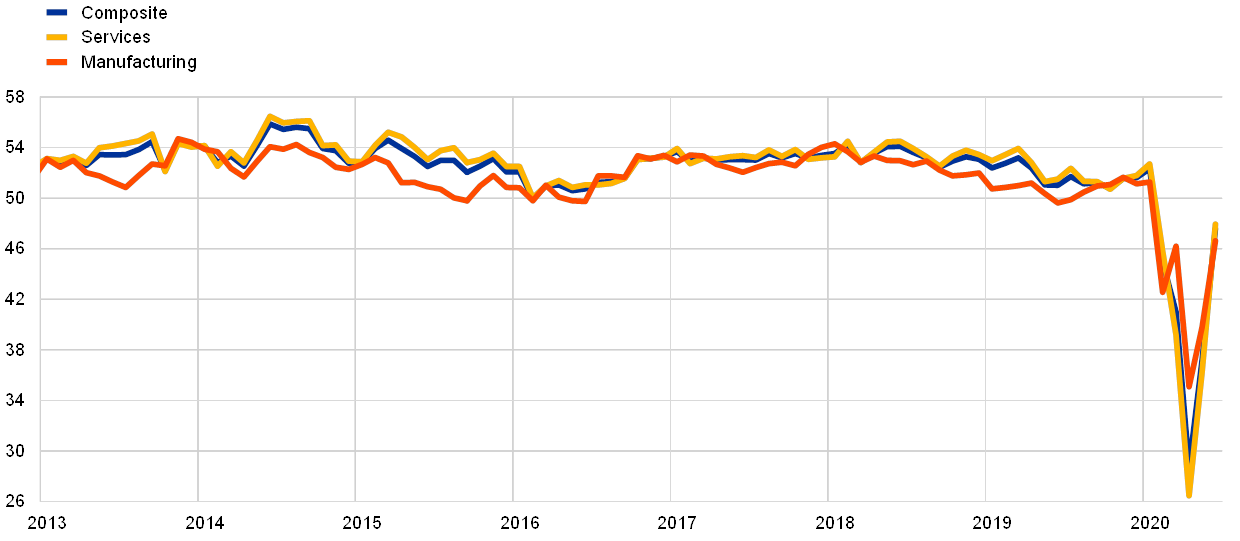

Survey data suggest that the unprecedented contraction in the global economy in the first half of 2020 has been bottoming out. The global composite output Purchasing Managers’ Index (PMI) – excluding the euro area – continued to rebound from its April trough in June, reaching 47.6 (see Chart 1). The increase in June was broad-based across all sub-components; the services sector, which had been lagging behind the manufacturing sector in terms of improvement, recovered strongly. These developments were also broad-based across almost all major advanced and emerging economies. However, PMIs for everywhere except China have remained in contractionary territory below 50, thereby pointing to continued weak activity levels globally.

Chart 1

Global composite output PMI (excluding the euro area)

(diffusion indices)

Sources: Markit and ECB calculations.

Note: The latest observations are for June 2020.

Cautious consumer behaviour points to a sluggish recovery ahead. Consumer confidence in countries where the pandemic was contained early, such as China and South Korea, has been recovering slowly but remains below pre-pandemic levels. High levels of uncertainty may imply a sluggish and fragile recovery in consumption, especially as new cases have risen globally.

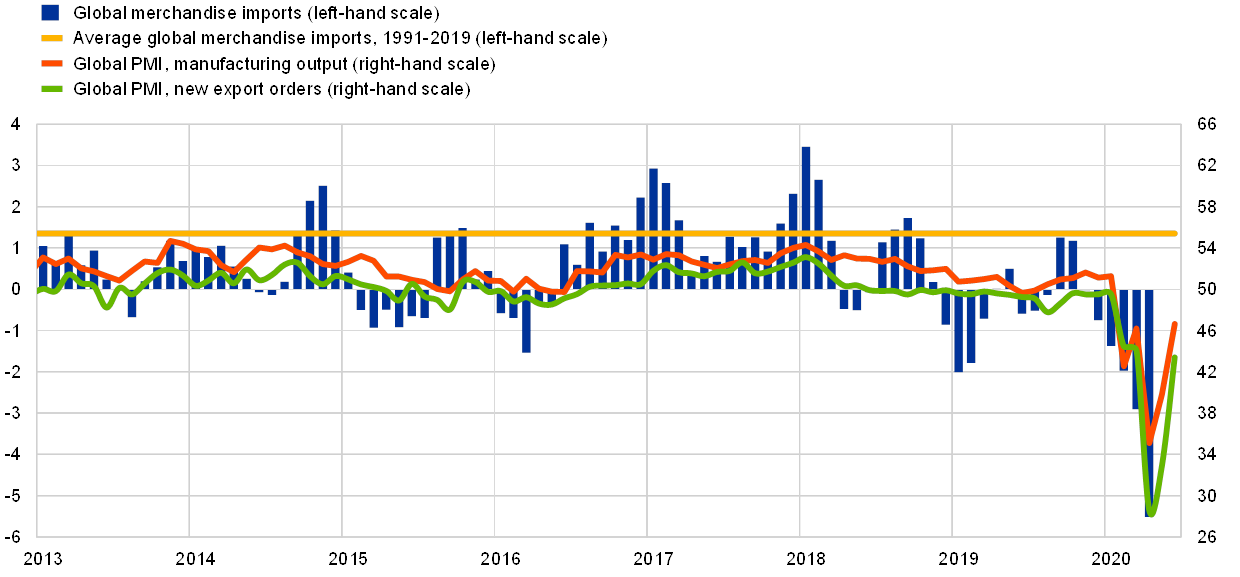

World trade remained very weak in April, pointing to an exceptional decline in the second quarter. Global merchandise imports (excluding the euro area) fell sharply in April, following two consecutive quarters of contraction. The decline in world trade coincided with a peak in the severity of containment measures worldwide. While the global PMI for new export orders (excluding the euro area) improved in May and June, it continued to signal weakness in trade (see Chart 2).

Chart 2

Surveys and global trade in goods (excluding the euro area)

(left-hand scale: three-month-on-three-month percentage changes; right-hand scale: diffusion indices)

Sources: Markit, CPB Netherlands Bureau for Economic Policy Analysis and ECB calculations.

Note: The latest observations are for April 2020 for global merchandise imports and June 2020 for the PMIs.

Global inflation slowed further in May. Annual consumer price inflation in the countries of the Organisation for Economic Co-operation and Development (OECD) declined to 0.7% in May, driven by a faster decline in energy prices, while food price inflation increased slightly. Meanwhile, inflation excluding food and energy remained stable at 1.6%. The slowdown in inflation was broad-based across most advanced economies and major non-OECD emerging market economies. Looking ahead, global inflationary pressures are expected to remain subdued as a result of both the fall in oil prices and weak demand.

Oil prices have increased by more than 10% since the last Governing Council meeting amid a rebound in economic activity and falling supply owing to cuts agreed in early May. Oil prices have been supported by a stronger than expected pick-up in oil demand on the back of the easing of lockdown measures. Oil demand is expected to remain subdued in the second half of 2020 and into 2021, with consumption set to remain below the levels seen in 2019. However, oil demand estimates have been revised upwards recently following the easing of lockdown measures in a number of countries. Besides recovering demand, reductions in supply have also been a factor in the rebalancing of oil markets. In particular, the recovery in prices has been supported by the OPEC+ agreement (i.e. the pact between major oil producers) in early May to lower supply by almost 10 million barrels per day (mbpd), and by significant shut-ins of oil production in the United States. Metal prices have also recovered strongly since mid-April, with an increase of around 2% since the last Governing Council meeting.

US data have recently surprised on the upside, but the level of activity remains weak. With lockdowns being gradually lifted, economic activity has resumed and various economic indicators have turned to the upside. Retail sales and food services rebounded sharply in May as household spending benefited from federal stimulus payments, reinforced by the return to work of some employees. Industrial production also rose in May, albeit less strongly. Labour market data also surprised on the upside. In May and June, the United States added 7.5 million jobs, regaining about one-third of the jobs lost since February. While the June figures showed the largest increase in history, labour market data currently require a cautious interpretation, as they are based on a mid-month survey and do not yet reflect newly reinforced regional lockdown measures. In spite of the further fall in the unemployment rate by 2.2 percentage points, to 11.1%, labour market slack remains at historically high levels. Overall, the latest data seem to confirm the bottoming out of the US economy indicated by other variables, rather than pointing to a substantial improvement in the economic situation. Key US indicators remain well below pre-pandemic levels, and rising numbers of new infections may trigger renewed containment measures or slow the easing of existing ones, thereby increasing the risk that the recovery will be undermined.

In Japan, the pace of economic activity has started normalising as containment measures were progressively lifted in May. Following a contraction of 0.6% in real GDP in the first quarter, the intensification of containment efforts in Japan triggered a considerable retrenchment in industrial production, external trade and private consumption in April and May. The latest Tankan survey confirmed a marked deterioration in business sentiment in manufacturing and services in the second quarter. Moreover, it also signalled a sharp cut in the investment plans of small firms, which continued to take a cautious view regarding the outlook. In its latest meeting, the Bank of Japan announced an increase in the size of its special programme to support corporate financing to JPY 110 trillion (from JPY 75 trillion). This programme includes purchases of commercial paper and corporate bonds, as well as special lending operations. The recent measures coincided with a marked acceleration in lending growth in April and May, likely reflecting an accommodative lending stance by banks and a higher demand for operating funds by Japanese firms. The government has also provided significant stimulus, approving two supplementary budgets for the 2020 fiscal year, amounting to about 10% of GDP.

In the United Kingdom, an unprecedented decline in activity is expected in the second quarter with activity resuming only slowly amid the easing of containment measures. Real GDP increased by 1.8% month-on-month in May but fell by 19.1% on a three-month rolling average basis amid stringent lockdown measures. The composite PMI output index remained below 50 throughout the second quarter, suggesting an ongoing weakness in demand, with further reductions in new orders and new export orders for the fourth month in a row. Prospects for a swift turnaround in the third quarter remain slim. Although the reopening of leisure and travel facilities at the beginning of July is helping to boost activity, business and consumer sentiment remains low compared to pre-lockdown levels. The shape of the recovery will also depend on the roadmap for future policy support. UK monetary policy remains supportive, but fiscal policy support is likely to be less substantial compared to the first half of the year, notwithstanding the additional fiscal stimulus announced in July.

The recovery in China is proceeding despite weak external demand. Amid the easing of containment measures, high-frequency indicators point to a continued normalisation of activity in June. In terms of hard data, industrial production growth turned positive in April and gained further momentum in May (up 4.4% year-on-year). While retail sales continue to decline on an annual basis, sequential growth momentum has been positive. PMI data paint a similar (albeit uneven) picture, with manufacturing having already returned to expansionary territory in March, while weaker new export orders are restraining the momentum of the upturn. Meanwhile, the Chinese authorities have provided additional fiscal and monetary stimulus to cushion the economic shock. Fiscal policy is aiming to stabilise employment and economic growth by expanding unemployment insurance, investment and tax relief. Fiscal policies are being complemented by monetary policies designed to ensure sufficient liquidity in the banking system, cuts in key policy rates and reserve requirements, and directions for banks to accommodate repayment delays by businesses.

2 Financial developments

The euro overnight index average (EONIA) and the new benchmark euro short-term rate (€STR) averaged -46 and -55 basis points respectively[1] over the review period (4 June 2020 to 15 July 2020). In the same period, excess liquidity increased by approximately €642 billion to around €2,816 billion, mainly reflecting take-up of targeted longer-term refinancing operations (TLTRO III) together with asset purchases under the pandemic emergency purchase programme (PEPP) and the asset purchase programme (APP).

The EONIA forward curve has shifted slightly downwards since early June, although markets do not seem to expect an imminent reduction in the deposit facility rate. The curve shifted downwards by an average of slightly more than 10 basis points across the maturities beyond three years. It became slightly inverted in the near term, with the EONIA rate around the end of 2021 standing around 10 basis points below its current level. Developments in the EONIA forward curve may be related to the PEPP announcement, in a context characterised by a sharp contraction of economic activity and heightened concerns about the implications of a still expanding coronavirus (COVID-19) pandemic at a global level. Overall, EONIA forward rates remain below zero for horizons up to 2027, reflecting continued market expectations of a prolonged period of negative interest rates.

Long-term sovereign yields in the euro area declined amid some bottoming out in the contraction of economic growth. Over the review period, the GDP-weighted euro area ten-year sovereign bond yield decreased by around 15 basis points to 0.07% (see Chart 3). This decline more or less mirrored a drop of 12 basis points in the ten-year overnight index swap (OIS) rate. After a small rise in the first week of the review period, rates started to decline in response to, among other factors, the Governing Council’s decision on 4 June to extend the PEPP and the announcement by the Federal Reserve on 10 June that it expected policy rates to remain near zero for a prolonged period of time. A marked rebound in incoming data relative to market expectations did not seem to have a positive impact on interest rates, perhaps because data outturns remained in line with an ongoing contraction in the business cycle, albeit at a slower pace. The complex negotiations that eventually led to the approval of the European Union’s Recovery and Resilience Facility may have influenced the developments in sovereign yields in both directions at times over the review period. Elsewhere, ten-year sovereign bond yields in the United States decreased by around 20 basis points over the review period to 0.63%, while UK yields declined by around 15 basis points to 0.17%.

Chart 3

Ten-year sovereign bond yields

(percentages per annum)

Sources: Refinitiv and ECB calculations.

Notes: Daily data. The vertical grey line denotes the start of the review period on 4 June 2020. The zoom window shows developments in sovereign yields since 1 April 2020. The latest observations are for 15 July 2020.

Movements in the spreads on euro area sovereign bond relative to the risk-free OIS rate have been relatively muted. Spreads initially rose slightly and then started to decline, ending the review period slightly below the levels prevailing in early June overall. The spread on German, Spanish and Portuguese sovereign bonds declined by between 3 and 5 basis points while French and Italian spreads fell very marginally, by just 1 basis point. Overall, the GDP-weighted euro area spread relative to the OIS rate declined by 2 basis points to just below 40 basis points.

Equity price indices rose for both euro area non-financial corporations (NFCs) and banks, thus further offsetting the sharp losses recorded since late February amid heightened COVID-19-related concerns. Over the review period, euro area NFC and bank equity prices rose by 2% and 3.2% respectively. Overall, equity prices in the two sectors remain around 5% and 30% respectively below the levels prevailing on 24 February, when valuations started to be affected by the COVID-19 outbreak outside of China, thus highlighting a marked underperformance of bank equity prices relative to other sectors. While improved earnings expectations have supported equity prices, higher risk premia, primarily associated with market participants’ concerns about the still robust expansion of the number of COVID-19 cases worldwide and a possible second wave of the pandemic, have depressed valuations.

Euro area corporate bond spreads declined over the review period. The spreads on both investment-grade NFC bonds and financial sector bonds relative to the risk-free rate declined slightly over the review period, by almost 10 basis points, to stand at 104 and 120 basis points respectively as of 15 July. Despite a significant compression from the peaks reached in early April, spreads are still at levels that are twice as high as in late February. The heightened risks compared to early 2020 that are embedded in corporate bond spreads, as well as in equity prices, may reflect market expectations of a significant rise in corporate defaults over the next few quarters.

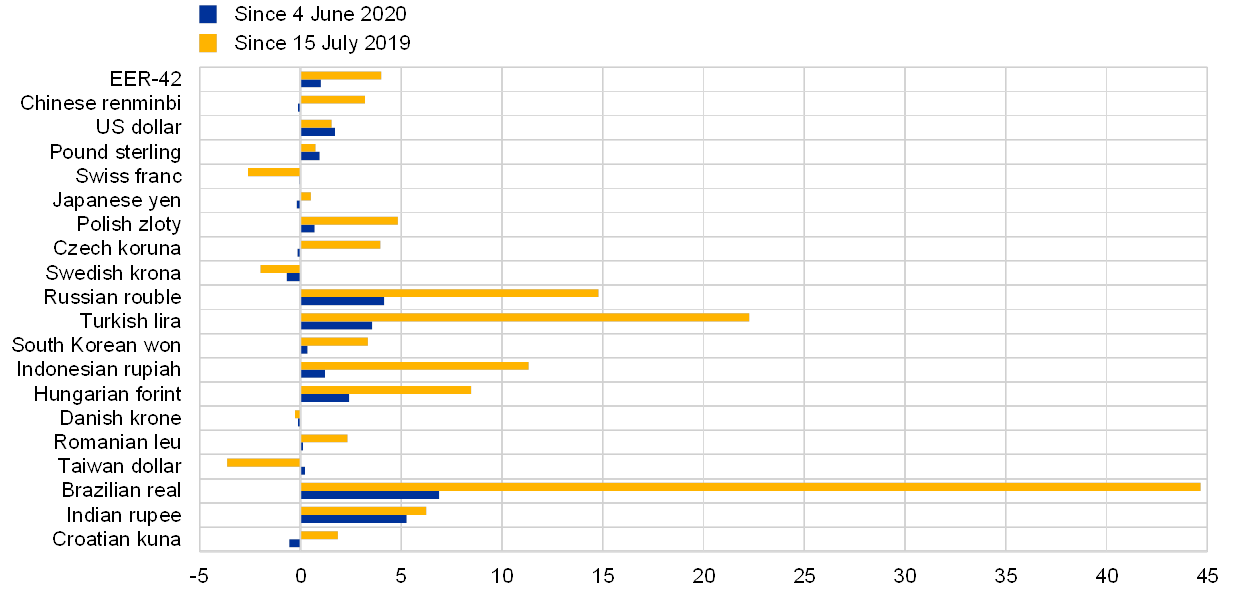

In foreign exchange markets, the euro broadly strengthened in trade-weighted terms (see Chart 4). Over the review period, the nominal effective exchange rate of the euro, as measured against the currencies of 42 of the euro area’s most important trading partners, appreciated by 1.0%. This largely reflected a strengthening in particular against the currencies of countries that were more heavily affected by the economic and financial market impact of the COVID-19 pandemic. Specifically, the euro appreciated against a number of emerging market currencies, notably the Brazilian real (by 6.9%), the Russian rouble (by 4.2%) and the Turkish lira (by 3.6%), as well as against both the US dollar (by 1.7%) and the pound sterling (by 1.0%). At the same time, the euro weakened only very slightly against the Japanese yen (by 0.2%) and the Chinese renminbi (by 0.1%) and remained virtually unchanged against the Swiss franc.

Chart 4

Changes in the exchange rate of the euro vis-à-vis selected currencies

(percentage changes)

Source: ECB.

Notes: EER-42 is the nominal effective exchange rate of the euro against the currencies of 42 of the euro area’s most important trading partners. A positive (negative) change corresponds to an appreciation (depreciation) of the euro. All changes have been calculated using the foreign exchange rates prevailing on 15 July 2020.

3 Economic activity

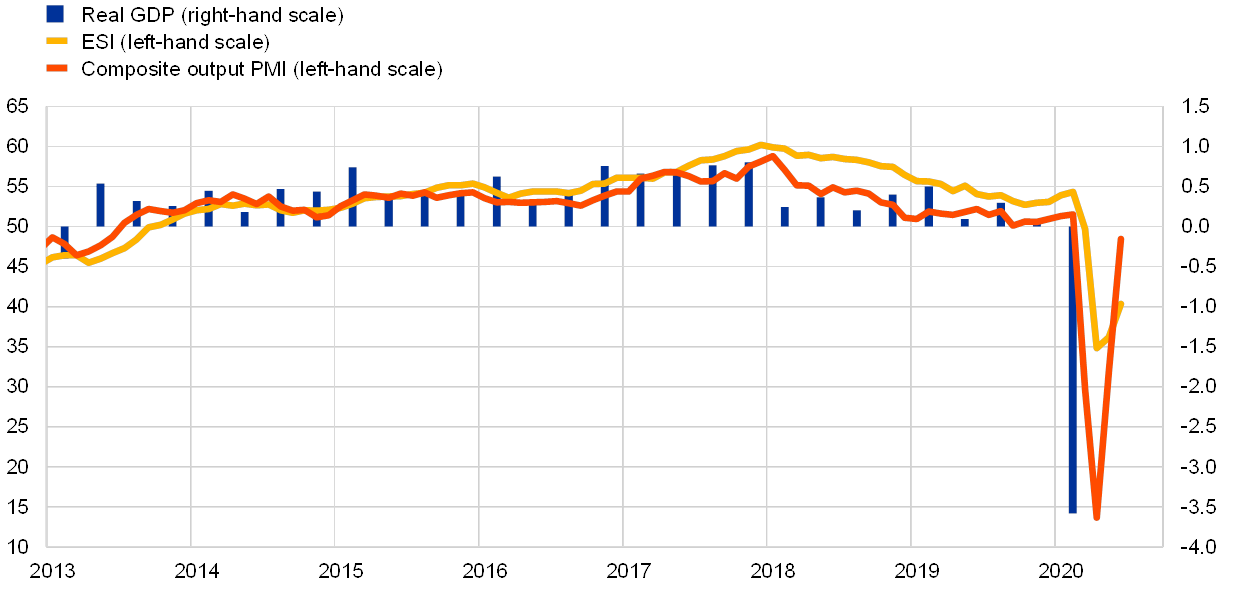

After euro area real GDP contracted sharply in the first quarter of 2020, signs of a rebound in economic activity have emerged with the gradual lifting of measures to contain the coronavirus (COVID-19) outbreak. Total economic activity declined by 3.6%,[2] quarter on quarter, in the first quarter of 2020, following growth of 0.1% in the fourth quarter of 2019 (see Chart 5). The breakdown suggests that the fall in GDP in the first quarter of 2020 was driven by both domestic demand (which made a -3.5 percentage point contribution to growth) and net trade (-0.4 percentage points), while changes in inventories provided a small positive contribution to growth (+0.3 percentage points). Economic indicators suggest that the decline in economic activity owing to the COVID-19 pandemic reached a trough in April 2020. Survey information, high-frequency indicators and hard data suggest that a recovery which is broad-based, but slow and uneven across countries, is taking place as the economy gradually reopens. Survey data point to an improvement in activity in both the manufacturing and services sectors in May and June, giving further cause for confidence that the recovery will continue in the third quarter.

Chart 5

Euro area real GDP, Economic Sentiment Indicator and composite output Purchasing Managers’ Index

(left-hand scale: diffusion index; right-hand scale: quarter-on-quarter percentage changes)

Sources: Eurostat, European Commission, Markit and ECB calculations.

Notes: The Economic Sentiment Indicator (ESI) is standardised and rescaled to have the same mean and standard deviation as the Purchasing Managers’ Index (PMI). The latest observations are for the first quarter of 2020 for real GDP and June 2020 for the ESI and the PMI.

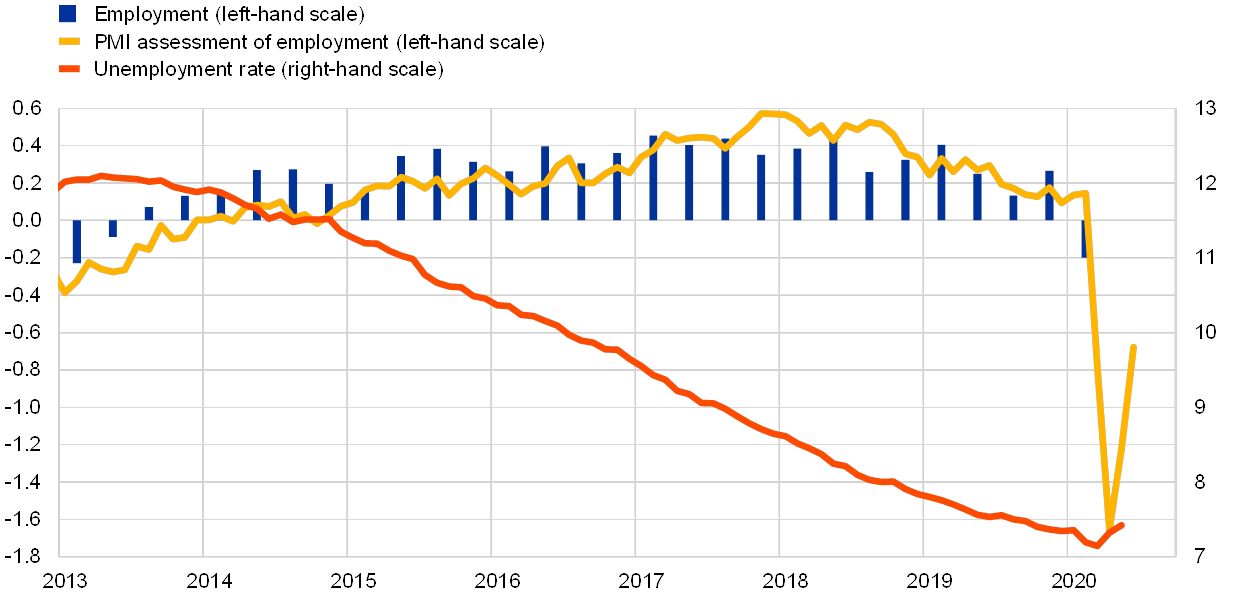

The impact of the COVID-19 pandemic on the labour market is more apparent from the fall in hours worked than from the unemployment rate. Employment declined by 0.2% in the first quarter of 2020 relative to the fourth quarter of 2019 (see Chart 6). Total hours worked declined significantly more, decreasing by 3.1%, which led to a fall of 2.9% in average hours worked per person employed. The unemployment rate increased to 7.4% in May, but still does not reflect the severity of the impact of the COVID-19 pandemic on the euro area labour market. Employment support measures, such as short-time work and temporary layoffs, are helping to contain dismissals and partly explain the muted reaction of the unemployment rate.[3]

Short-term labour market indicators have partially recovered after unprecedented falls in March and April. The Purchasing Managers’ Index (PMI) for employment increased to 43.2 in June, from 37.8 in May and 33.4 in April – when it reached its lowest level on record (see Chart 6). However, the current level of the PMI continues to suggest a sharp contraction in employment. High-frequency indicators provide some evidence that labour demand is bottoming out.[4]

Chart 6

Euro area employment, PMI assessment of employment and the unemployment rate

(left-hand scale: quarter-on-quarter percentage changes, diffusion index; right-hand scale: percentages of the labour force)

Sources: Eurostat, Markit and ECB calculations.

Notes: The PMI is expressed as a deviation from 50 divided by 10. The latest observations are for the first quarter of 2020 for employment, June 2020 for the PMI and May 2020 for the unemployment rate.

Clear signs of a recovery in consumption have emerged since May. Available indicators point to an increase in spending following the easing of the lockdowns. While retail trade declined by 12%, month on month, in April, it rose by 17.8%, month on month, in May and is expected to have risen further in June. Although still standing about 50% below their average monthly level in 2019, new passenger car registrations surged by 140%, month on month, in May following sharp declines of -45.8% in April and -57.3% in March. Consumer confidence data available up to June also suggest that consumption increased strongly in May and June, compared with April, even though spending remained far below pre-lockdown levels. Consequently, the household saving ratio reached an unprecedented high level of 16.9% in the first quarter of 2020. While precautionary motives are undoubtedly pushing up the saving ratio, forced savings seem to be the main driver of the current spike in household savings. Unlike during the great financial crisis, the spike in savings is mainly reflected in higher bank deposits, rather than lower credit flows.

Some pent-up demand effects seem likely in the period ahead, although their size remains highly uncertain. About half of the contraction in private consumption reflects expenditure components which can be postponed (e.g. purchases of electronics and cars). This suggests some potential for pent-up demand for these goods as containment measures are lifted. Pent-up demand describes a rapid increase in demand for products following a downturn, which temporarily exceeds the level of demand that prevailed before the downturn. As consumers tend to hold off making purchases during a recession and, in the current situation, they may have been forced to postpone purchases as a result of the lockdowns, they have probably built up a backlog of demand that could be unleashed as signs of a recovery emerge and the containment measures are eased. While recent retail trade data show a strong rebound in a number of product categories, it is too early to determine whether this reflects widespread pent-up demand or rather a shift in consumption baskets (e.g. towards purchases of bicycles and home office equipment) in response to the pandemic. According to the European Commission’s consumer survey, available up to June, households continue to expect to spend less on major purchases over the next 12 months compared with the previous 12 months, despite the accumulated savings. This suggests that consumers may remain cautious, in part given the higher risk of unemployment.

The downturn in business investment as a result of the lockdowns and containment measures implemented across euro area countries since March 2020 is expected to have reached a trough in April as signs of a recovery emerge. Production data for April and May exhibited a dramatic fall in manufacturing production and sales. This was driven by a combination of both supply and demand factors related to the COVID-19 pandemic and had a major, adverse impact on business investment. Production of capital goods, an indicator for non-construction investment, fell sharply in March and April, declining by 39%. The decline in the production of transport equipment over the same period was even more severe, with a drop of 69%. Furthermore, according to the industry survey of the European Commission conducted in April, capacity utilisation in the capital goods sector declined in the second quarter by 17 percentage points to stand slightly below 67%, the lowest level in the history of this series. However, recent production and survey data indicate that a recovery from these low levels started in May and intensified in June. Production of capital goods rebounded strongly in May, rising by 25.4%, and the production of transport equipment rebounded with an increase of 84%. Despite this, production levels remain significantly below the levels seen in February. Survey indicators also support the emergence of a recovery. The European Commission’s Economic Sentiment Indicator stabilised in May and recorded the strongest increase in the history of the series in June. In addition, manufacturing confidence in the capital goods sector has improved steadily since the trough in April. A similar picture is provided by the PMI manufacturing indicators. Notwithstanding the improvements in these indicators, order book levels in the capital goods sector, in particular for exported capital goods, remained at low levels in June according to surveys by the European Commission. Furthermore, euro area sectoral accounts showed a sharp decline in the gross operating surplus of non-financial corporations in the first quarter of 2020 and the ECB’s composite indicator of systemic stress remains at high levels. Moreover, substantial downside risks to firms’ investment plans – stemming from rising debt levels, potential insolvencies and corporate defaults on long-term debt commitments, as well as declining cash flows – remain despite considerable euro area and EU-wide policy efforts to provide liquidity and credit to firms.[5]

Housing investment in the euro area recorded a dramatic deterioration in the first quarter, while positive signs emerged at the end of the second quarter. Euro area housing investment dropped by 5.8%, quarter on quarter, in the first three months of 2020 – the worst growth rate since the start of the series in 1995. This bleak outcome mainly resulted from the widespread shutdown of construction sites, although it was partly alleviated by the large backlog of construction plans (especially in Germany and the Netherlands) and was accompanied by a reduction in transaction volumes with only minor effects on house prices. As containment measures intensified in several countries up to the end of April, an even deeper contraction in euro area housing investment is expected to have occurred in the second quarter. According to the European Commission survey data, construction firms faced historically high limits to production in the second quarter, mainly owing to financial conditions, potentially signalling shortages of liquidity, and to other factors, likely related to the effects of containment measures on activity. Nevertheless, after bottoming out in April, the euro area PMI for construction output showed signs of improvement in May and June amid the relaxation of containment measures, even standing slightly above the expansionary threshold in France and Italy. Survey results on companies’ assessments of order books point to moderate prospects for a recovery in the housing sector in the period ahead. Surveys on households’ intentions to build or renovate properties show a similar picture. Moreover, the uncertainty caused by the pandemic might have even greater and longer-lasting effects on activity, as it could encourage households and investors to postpone property transactions until an effective medical solution for COVID-19 is found.

After extra and intra-euro area trade fell sharply in the first quarter of 2020, extra-euro area exports and intra-euro area trade collapsed in April with the emergence of new epicentres of the COVID-19 pandemic. The measures adopted to contain the pandemic had a strongly adverse impact on both intra and extra-euro area trade in the first quarter. Extra-euro area exports fell significantly more than extra-euro area imports, resulting in a negative net trade contribution to GDP of -0.4 percentage points. Intra-euro area trade fell sharply in the first quarter driven mainly by intermediate goods, owing to disruptions of supply chains, and by capital goods. As severe lockdowns became effective across the euro area in April, nominal intra-euro area goods trade collapsed further, falling by 21.7% compared with March. Extra-euro area exports continued to be more affected than extra-euro area imports in April. While lower domestic demand in the euro area resulted in a fall in extra-euro area nominal goods imports, which declined by 13% in April compared with the previous month, the collapse in extra-euro area goods exports accelerated in April, as nominal exports of goods plummeted by 24.5% compared with the month before with the spread of the pandemic to major trading partners. In April goods export volumes to the United States were down by 32%, to China by 11% and to Brazil by 36% compared with April 2019. Leading indicators signal that the trough in terms of negative trade growth rates is likely to have occurred in April. The PMI for euro area new export orders rebounded from 18.9 in April to 42.5 in June. Manufacturing trade, in particular with regard to the automotive sector, recovered partially with the reopening of factories. While travel and transportation remain the most affected sectors, trade in these sectors is slowly recovering as travel restrictions are lifted, which is also visible in a slight increase in flight capacity starting from mid-June. Despite the partial rebound, the recovery in euro area trade is likely to be uneven and incomplete given the unsynchronised relaxation of containment measures in major trading partners and lasting effects on confidence.

While incoming economic data, particularly survey results, show initial signs of a recovery, they still point to a historic contraction in euro area output in the second quarter of 2020. The COVID-19 outbreak and the associated containment measures have had an adverse impact on activity in manufacturing and particularly in services via increasing supply constraints and rapidly falling demand. As regards recent survey data, the European Commission’s Economic Sentiment Indicator and the composite output PMI both posted record lows in April. In May and June there were strong increases in some indicators, but many remain below their long-term levels. Both the Economic Sentiment Indicator and the PMI display a broad-based rebound across both countries and economic sectors. This pick-up in economic activity is also confirmed by high-frequency indicators such as electricity consumption.

Looking beyond the disruption stemming from the coronavirus pandemic, euro area growth is resuming with the gradual lifting of containment measures, supported by favourable financing conditions, the euro area fiscal stance and a resumption in global activity. However, uncertainty remains extremely elevated, making it very difficult to predict the likely extent and duration of the recovery. The results of the latest round of the ECB Survey of Professional Forecasters, conducted in early July, show that private sector GDP growth forecasts have been revised further downwards for 2020 and have been revised upwards for 2021, compared with the previous round conducted in early April.

4 Prices and costs

According to Eurostat’s flash estimate, HICP inflation rebounded slightly, increasing to 0.3% in June from 0.1% in May 2020. This increase mainly reflects a less negative annual rate of change in energy prices, namely -9.4% in June instead of -11.9% in May. The less negative energy inflation was partly counterbalanced by a further decline in food price inflation to 3.1% in June from 3.4% in May and 3.6% in April.[6] It is important to note that HICP data are still subject to heightened measurement uncertainty due to challenges in price collection. While falling from 22% in May to 11% in June the share of imputed prices is still higher than usual, especially for services.[7]

Chart 7

Contributions of components of euro area headline HICP inflation

(annual percentage changes; percentage point contributions)

Sources: Eurostat and ECB calculations.

Notes: The latest observations are for June 2020 (flash estimate). Growth rates for 2015 are distorted upwards owing to a methodological change (see the box entitled “A new method for the package holiday price index in Germany and its impact on HICP inflation rates”, Economic Bulletin, Issue 2, ECB, 2019).

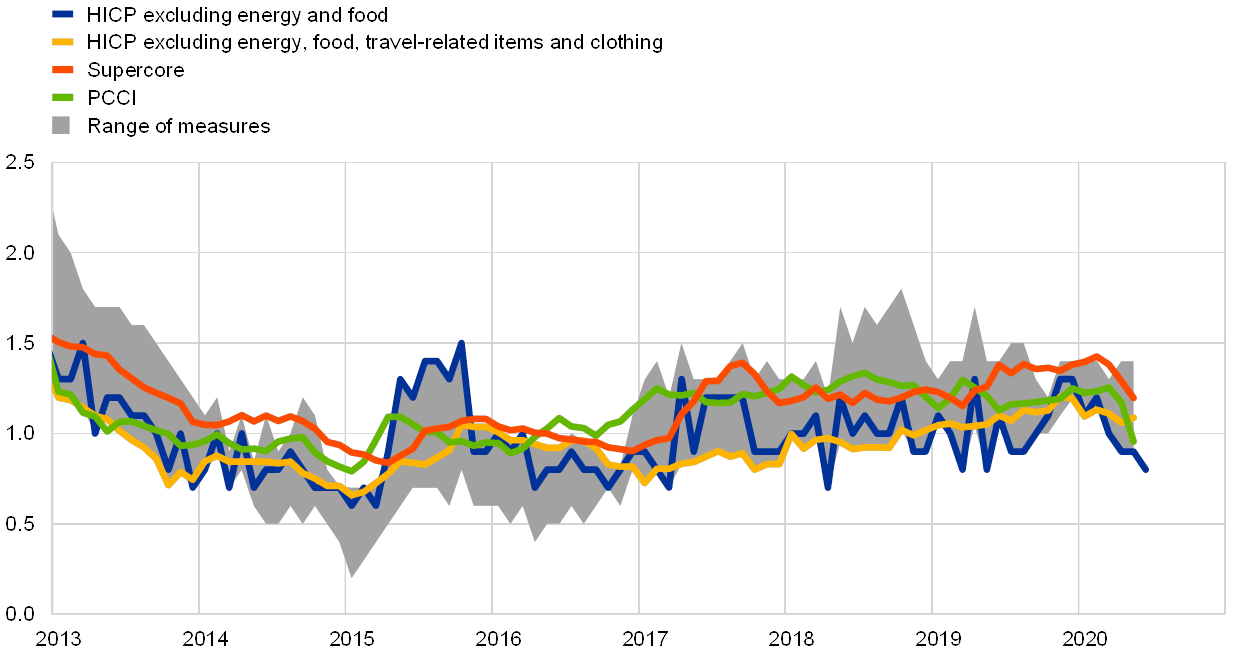

Measures of underlying inflation declined. HICP inflation excluding energy and food decreased to 0.8% in June compared to 0.9% in both May and April and 1.2% in February. This recent decline is mainly due to services inflation decreasing from 1.3% in May to 1.2% in June, while inflation for non-energy industrial goods remained unchanged at 0.2% in June. For other measures, data were only available up until May 2020. HICP inflation excluding energy, food, travel-related items and clothing remained unchanged at 1.1% in May compared to April, while the Persistent and Common Component of Inflation (PCCI) indicator decreased from 1.2% to 1.0% and the Supercore indicator[8] declined from 1.3% to 1.2%.

Chart 8

Measures of underlying inflation

(annual percentage changes)

Sources: Eurostat and ECB calculations.

Notes: The latest observations are for June 2020 for the HICP excluding energy and food (flash estimate) and for May 2020 for all other measures. The range of measures of underlying inflation consists of the following: HICP excluding energy; HICP excluding energy and unprocessed food; HICP excluding energy and food; HICP excluding energy, food, travel-related items and clothing; the 10% trimmed mean of the HICP; the 30% trimmed mean of the HICP; and the weighted median of the HICP. Growth rates for the HICP excluding energy and food for 2015 are distorted upwards owing to a methodological change (see the box entitled “A new method for the package holiday price index in Germany and its impact on HICP inflation rates”, Economic Bulletin, Issue 2, ECB, 2019).

Pipeline price pressures for HICP non-energy industrial goods were stable at the later stages of the supply chain but experienced a slight decrease at the earlier stages. Domestic producer price inflation for non-food consumer goods remained stable at 0.5% in May and the corresponding rate of inflation for imported non-food consumer goods also remained unchanged at 0.0% in May compared to April. At the earlier stages of the supply chain, inflation for domestic intermediate goods declined to -2.9% in May from -2.6% in April, while import price inflation for intermediate goods increased from -2.2% in April to -2.0% in May.

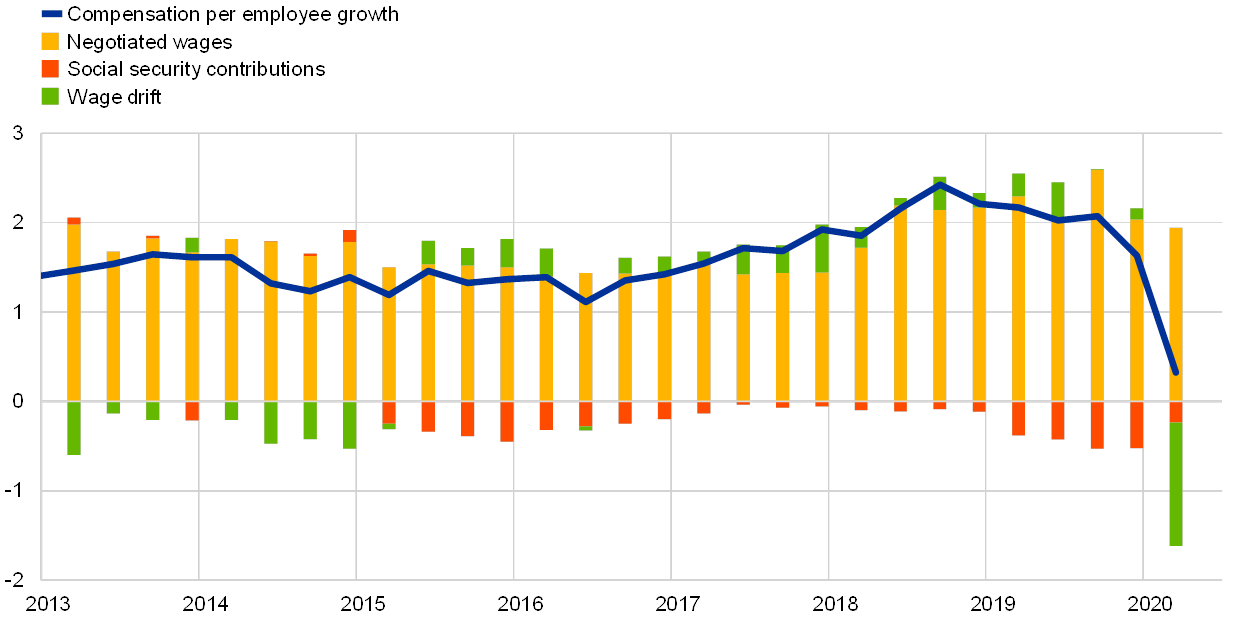

Growth in compensation per employee decreased sharply in the first quarter of 2020, essentially reflecting the fall in hours worked. The annual growth in compensation per employee fell to 0.3% during the first quarter of 2020 compared to 1.6% in the fourth quarter of 2019. The decline was broad-based across sectors and countries. The marked deceleration in euro area compensation per employee growth essentially reflects the significant reduction in hours worked per employee after the onset of the coronavirus (COVID-19) pandemic and the related lockdown and containment measures. The impact of short-time work and temporary lay-off schemes and the containment measures is also visible in the annual growth in compensation per hour, which rose to 3.1% in the first quarter of 2020 from 1.8% in the previous quarter, due to the significant reduction in actual hours worked per employee. These contrary developments reflect the impact of the short-time work and temporary lay-off schemes in buffering labour income. Negotiated wages grew by 2.0% in the first quarter of 2020, with the latest developments in compensation per employee implying a strong downward impact in the wage drift.[9] Nevertheless, the deceleration in compensation per employee exaggerates the loss in labour income, as a number of countries record government support under transfers rather than compensation for statistical purposes.[10]

Chart 9

Contributions of components of compensation per employee

(annual percentage changes; percentage point contributions)

Sources: Eurostat and ECB calculations.

Note: The latest observations are for the first quarter of 2020.

Over the review period (4 June to 15 July 2020), market-based indicators of longer-term inflation expectations have continued to increase slowly towards the levels prevailing as of late February, while survey-based indicators of inflation expectations declined slightly. The five-year forward inflation-linked swap rate five years ahead has continued to recover from the all-time low of 0.72% recorded on 23 March 2020, increasing to 1.12% on 15 July. Overall, its rise over the review period has been modest, amounting to 5 basis points. The option-implied (risk-neutral) probability of deflation occurring over the next five years declined considerably from the peak seen at the end of March 2020 to stand close to the levels prevailing in late February. The decline in the probability of deflation may to some extent also reflect the recent increase in the price of oil. Although an increase has been seen over the review period, especially in the very long term, the forward profile of market-based indicators of inflation expectations continues to indicate a prolonged period of low inflation. Reflecting the impact of the coronavirus (COVID-19) pandemic, mitigation measures and continuing uncertainties, the ECB Survey of Professional Forecasters (SPF) for the third quarter of 2020 shows a further downward revision of expectations for euro area inflation for the third quarter of 2020. Average point forecasts for annual HICP inflation now stand at 0.4% for 2020, 1.0% for 2021 and 1.3% for 2022, which represents a downward revision of 0.2 percentage points for 2021 and 0.1 percentage points for 2022. Although the change in unrounded terms was very slight, average long-term inflation expectations fell to a new historic low of 1.6%, from 1.7% in the last round.

Chart 10

Market and survey-based indicators of inflation expectations

(annual percentage changes)

Sources: ECB Survey of Professional Forecasters (SPF), Eurosystem staff macroeconomic projections for the euro area (June 2020) and Consensus Economics (8 June 2020).

Notes: The SPF for the third quarter of 2020 was conducted between 30 June and 6 July 2020. The market-implied curve is based on the one-year spot inflation rate and the one-year forward rate one year ahead, the one-year forward rate two years ahead, the one-year forward rate three years ahead and the one-year forward rate four years ahead. The latest observations for market-based indicators of inflation expectations are for 15 July 2020.

5 Money and credit

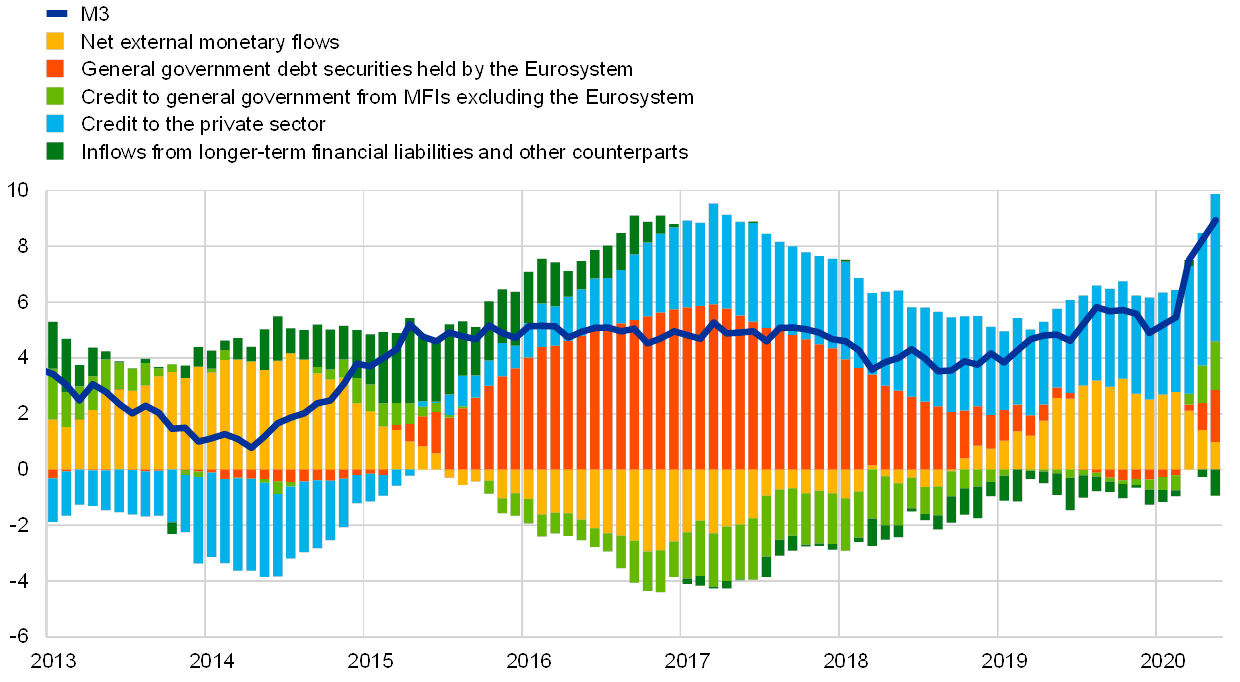

Broad money growth increased further in May. The broad monetary aggregate (M3) experienced another large inflow, signalling an ongoing strong build-up of liquidity amid uncertainty related to the pandemic crisis. The annual growth rate of M3 increased to 8.9% in May 2020, after 8.2% in April (see Chart 11). While the slowdown in economic growth dampened M3 growth, substantial support came from the extraordinary liquidity demand of firms and households. The increase in M3 was mainly driven by the narrow aggregate M1, which includes the most liquid components of M3. The annual growth rate of M1 increased from 11.9% in April to 12.5% in May 2020, which was mainly attributable to a further increase in the annual growth rates of overnight deposits. While for firms precautionary motives seem to remain an important driver of increases in their deposit holdings, in the case of households constraints still limiting spending possibilities might also have played a role. Other short-term deposits and marketable instruments made a small, positive contribution to annual M3 growth in May.

Chart 11

M3 and its counterparts

(annual percentage changes; contributions in percentage points; adjusted for seasonal and calendar effects)

Source: ECB.

Notes: Credit to the private sector includes monetary financial institution (MFI) loans to the private sector and MFI holdings of securities issued by the euro area private non-MFI sector. As such, it also covers the Eurosystem’s purchases of non-MFI debt securities under the corporate sector purchase programme. The latest observation is for May 2020.

In May 2020 domestic credit continued to be the main source of money creation. Credit to the private sector (see the blue portion of the bars in Chart 11) – the main driver of M3 growth from the counterpart perspective since 2018 – increased further, driven mainly by higher loans to non-financial corporations. In addition, the Eurosystem’s net purchases of government securities under the ECB’s asset purchase programme and the pandemic emergency purchase programme made a larger contribution to M3 growth in May than in previous months (see the red portion of the bars in Chart 11).[11] Further support to M3 growth came from an increase in credit to general government from monetary financial institutions (MFIs) excluding the Eurosystem (see the light green portion of the bars in Chart 11). The contribution from annual net external monetary flows moderated somewhat (see the yellow portion of the bars in Chart 11), largely reflecting outflows in March and April and muted flows in May. Longer-term financial liabilities and other counterparts had a small, dampening impact on broad money growth.

The dynamics of loans to firms strengthened further in May.[12] The annual growth rate of bank loans to the private sector increased to 5.3% in May 2020, after 4.9% in April (see Chart 12). This development was due to a further increase in the annual growth rate of loans to non-financial corporations (NFCs), from 6.6% in April 2020 to 7.3% in May. The growth in bank lending to firms was driven by firms’ operational financing needs, in an environment of compressed cash flows. Firms’ reliance on medium-term and long-term loans continued to increase at the expense of short-term loans, as evidence of a more protracted recovery became stronger. For the third quarter of 2020, banks’ expectations as reported in the euro area bank lending survey, which normally lead actual loan growth, point to further increases in the demand for loans to firms, albeit at a slower pace. At the same time, the annual growth rate for loans to households stabilised at 3.0% in May 2020, following two consecutive months of decline, down from 3.4% in March. The diverging developments between firms and households in May are evidenced by the results of the bank lending survey for the demand and supply of loans. The ECB’s policy measures, in particular the very favourable terms for targeted longer-term refinancing operations (TLTRO III), should encourage banks to extend loans to all private sector entities.

Chart 12

Loans to the private sector

(annual growth rate)

Source: ECB.

Notes: Loans are adjusted for loan sales, securitisation and notional cash pooling. The latest observation is for May 2020.

The July 2020 euro area bank lending survey shows a further strong upward impact of the coronavirus (COVID-19) pandemic on firms’ loan demand, largely reflecting emergency liquidity needs. In the second quarter of 2020, firms’ demand for loans or their drawing of credit lines reached the highest net balance since the start of the survey in 2003. The higher demand from borrowers for inventories and working capital more than offset the negative contribution of demand for fixed investment. At the same time, credit standards for loans or credit lines to firms remained favourable.[13] While credit standards were supported by government loan guarantees in most countries and monetary policy measures, banks continued to indicate risk perceptions (related to the deterioration in the general economic outlook and the firm-specific situation) as the main factor contributing to the tightening of credit standards. Banks also reported lower risk tolerance than in the previous survey round. For the third quarter of 2020, banks expect credit standards for firms to tighten considerably, which is reported to be related to the expected ending of the state guarantee schemes in some large euro area countries. Turning to households, net demand for housing loans and for consumer credit decreased considerably in the second quarter, on account of weaker consumer confidence, declining housing market prospects and low spending possibilities during the strict lockdown period. Credit standards on household loans tightened significantly in the second quarter of 2020. This development was attributable to a deterioration of households’ income and employment prospects owing to the COVID-19 pandemic. Banks expect the net tightening of credit standards to continue and, with an easing of lockdown restrictions, household loan demand to rebound in the third quarter of 2020.

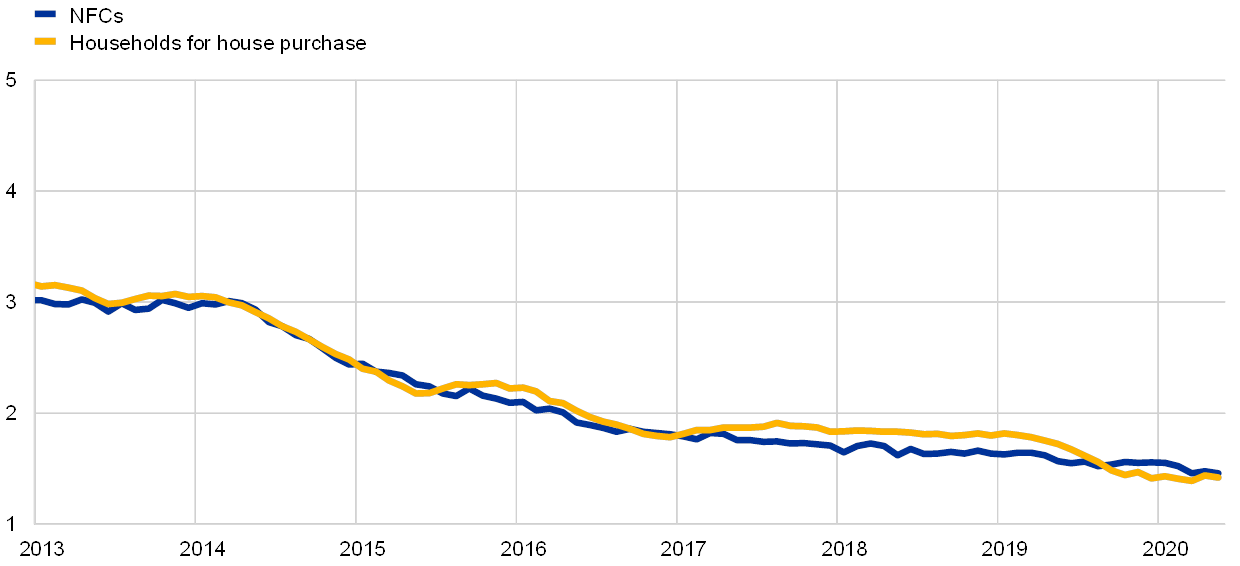

Very favourable lending rates continued to support euro area economic growth. Lending rates stabilised at their historical lows, broadly in line with developments in (longer-term) market reference rates. In May 2020 the composite bank lending rates for loans to NFCs and households remained broadly unchanged at 1.46% and 1.42% respectively (see Chart 13). While the severe economic impact of the pandemic on firms’ revenues, households’ employment prospects and overall borrower creditworthiness puts upward pressure on bank lending rates, the vigorous policy stimulus put in place in response to the pandemic-related crisis, in particular the ECB’s monetary policy measures and government loan guarantees, exerts a dampening effect on lending rates for loans to firms and households.

Chart 13

Composite bank lending rates for NFCs and households

(percentages per annum)

Source: ECB.

Notes: Composite bank lending rates are calculated by aggregating short and long-term rates using a 24-month moving average of new business volumes. The latest observation is for May 2020.

Boxes

1 US dollar funding tensions and central bank swap lines during the COVID-19 crisis

US dollar funding conditions started to become tense around the end of February 2020 when supply-demand imbalances led to rising funding premia amid volatile financial markets. This box focuses on these tensions in the foreign exchange (FX) swap market, where market participants lend funds in two currencies (e.g. the euro and the US dollar) to each other with the commitment to swap these funds back at a later date and at a pre-agreed exchange rate. The box provides evidence on the positive impact of the swap lines between central banks on the functioning of the EUR/USD FX swap market. These central bank swap lines enable the Eurosystem to provide US dollars to euro area banks.[14] The enhancement of these swap lines and the subsequent supply of US dollars via more frequent liquidity-providing operations not only helped banks to satisfy their immediate US dollar funding needs but also supported market activity, as banks participating in the US dollar operations became more willing to intermediate and passed funds borrowed from the Eurosystem on to other market participants. This was key to reducing tensions on US dollar funding conditions and restoring orderly market functioning in the EUR/USD FX swap market. The analysis is based on market transaction data gathered through the ECB Money Market and Statistical Reporting (MMSR)[15].

More2 The great trade collapse of 2020 and the amplification role of global value chains

This box assesses the economic effects of the coronavirus (COVID-19) pandemic as transmitted through global value chains (GVCs). The world economy is facing an unprecedented shock and, as the impact of the pandemic unfolds, world trade will be particularly hard hit. This box analyses the role of GVCs in the pandemic with a view to quantifying the ensuing effects on world trade. Our findings indicate that GVCs could significantly amplify the decline in world trade.

More3 The impact of the ECB’s monetary policy measures taken in response to the COVID-19 crisis

Since March 2020 the severity of the economic and financial implications stemming from the coronavirus (COVID-19) crisis has become increasingly apparent. The ECB has responded with a decisive policy package that is designed to be targeted and proportionate to the unprecedented scale of the crisis as well as temporary, as the emergency and its aftermath are expected to be reabsorbed over time. These measures have supported liquidity and funding conditions in the euro area economy, averted the most adverse feedback loops between the real economy and financial markets, and shored up confidence. They are also expected to significantly contribute to ensuring that inflation in the euro area moves towards levels that are below, but close, to 2% in a sustained manner.

More4 Euro area equity markets and shifting expectations for an economic recovery

As a result of the expected economic fallout from the global spread of the coronavirus (COVID-19) and the considerable associated uncertainty, euro area equity prices fell by more than 30% from February to mid-March 2020 (see Chart A). At the same time, liquidity conditions worsened significantly, as reflected in a pronounced widening of bid-ask spreads – a development which was not confined to equity markets.

More5 A preliminary assessment of the impact of the COVID-19 pandemic on the euro area labour market

This box analyses labour market developments in the euro area since the onset of the coronavirus (COVID-19) pandemic. The containment measures implemented from mid-March resulted in a sharp fall in euro area real GDP in the first quarter of 2020.[16] Business and consumer survey data indicate that the fall deepened in April and May. However, employment and unemployment do not appear to have been significantly affected. In this regard, the reaction of the euro area labour market to the COVID-19 pandemic appears in sharp contrast with that observed in the United States, where unemployment increased rapidly. This box examines the discrepancy between business and consumer survey indicators and the main headline labour market indicators for the euro area. In addition, we discuss the possible effects of lockdown measures on unemployment statistics in view of the internationally agreed definition of unemployment, and elaborate on the adjustment of hours worked and on the widespread use of short-time work schemes and temporary lay-offs, which are the key policies that have supported the euro area labour market since the start of the COVID-19 pandemic.

More6 High-frequency data developments in the euro area labour market

This box provides an overview of the impact of the coronavirus (COVID-19) pandemic on euro area labour markets by examining high-frequency indicators. The first part of the box analyses information from Indeed’s daily job postings and LinkedIn’s daily hiring rates for the five largest euro area countries. The number of job postings from Indeed can be used as a proxy for changes in labour demand. The LinkedIn hiring rate provides information both at the aggregate and sectoral levels about the number of job hires in the euro area. The second part of the box illustrates how the LinkedIn hiring rate can be used to perform a nowcasting of the job finding rate and make an assessment of the unemployment rate, thereby providing more timely information about labour market developments than that derived from more traditional statistical sources. That said, the information contained in these high-frequency indicators should be viewed with caution and used to complement official statistics, given that the available samples are mostly concentrated in white-collar jobs and in certain sectors.

More7 Recent developments in euro area food prices

Food prices can be an important driver of euro area headline HICP inflation, as food accounts for almost 20% of the HICP consumption basket and food price inflation is highly volatile. In the second quarter of 2020 the contribution of food to HICP inflation was around two-thirds of a percentage point, making it larger than the contribution of services or non-energy industrial goods. As food items are also a prominent example of frequently purchased out-of-pocket goods, their price movements are generally thought to have an important bearing on consumers’ perception of inflation. Against this background, this box reviews recent developments in euro area food prices in an environment that has been affected by the coronavirus (COVID-19) pandemic.

More8 Drivers of firms’ loan demand in the euro area – what has changed during the COVID-19 pandemic?

The coronavirus (COVID-19) pandemic is having multiple impacts on firms’ business plans and financing needs. In view of the importance of bank borrowing for euro area firms,[18] the euro area bank lending survey (BLS) is a rich and unique source of soft information not only on bank lending conditions, but also on the financing needs of firms.[19] When combined with hard economic and financial data, information from the BLS helps to explain developments in firms’ business plans and financing needs, as well as the driving factors behind them.[20] This box starts by discussing the long-term relationship between survey indicators from the BLS and actual developments in business investment. It goes on to examine the recent surge in firms’ demand for loans, the driving factors and the link with firms’ use of financing, in particular fixed investment, in the context of the COVID-19 pandemic. Finally, the box provides further details on this issue from a sectoral perspective.

MoreArticles

1 Consumption of durable goods in the euro area

Trends in households’ purchases of durable goods have important implications for the business cycle, which motivates the need to examine them closely from a monetary policy perspective. First, because of their marked pro-cyclicality, durables can help in tracking – and possibly anticipating – the state of the business cycle in the euro area, thus complementing the signal from other pro-cyclical demand components, such as investment.[21] Second, expenditure on durables can help us better understand cross-country heterogeneity in terms of consumption and saving habits, as well as its drivers. Third, since purchases of durables can be financed using credit, the behaviour of durable goods provides important insights into the state of financing conditions in the economy.

More2 Drivers of rising labour force participation – the role of pension reforms

Labour supply developments are a major determinant of potential output and are therefore also relevant for monetary policy. Labour supply developments in the euro area are strongly affected by population ageing, among other things.[22] Against this background, it is crucial to have a good understanding of how demographic changes in the various working-age cohorts, together with structural factors such as policy changes, will affect the labour market. Looking ahead, this understanding will be relevant when assessing the potential growth outlook, even though uncertainty has considerably increased recently due to the coronavirus (COVID-19) pandemic.

More3 Liquidity distribution and settlement in TARGET2

TARGET2, the payment system owned and operated by the Eurosystem, plays a vital role in the euro area, supporting the implementation of monetary policy as well as the functioning of financial markets and economic activity. Central banks and commercial banks use TARGET2 for monetary policy operations, interbank payments and customer payments.[24] The system processes euro-denominated payments in central bank money, on a gross basis, in real time and with immediate finality. It ensures the free flow of central bank money across the euro area, supporting economic activity, financial stability and promoting financial integration in the EU.[25] Moreover, TARGET2 has a global reach through correspondent banking,[26] which further supports the operations of EU banks and firms. Central bank liquidity – funds held by banks at the central bank, including the minimum reserves they must hold – is held on TARGET2 accounts and can be used to make payments throughout the day.

MoreStatistics

Statistical annex© European Central Bank, 2020

Postal address 60640 Frankfurt am Main, Germany

Telephone +49 69 1344 0

Website www.ecb.europa.eu

All rights reserved. Reproduction for educational and non-commercial purposes is permitted provided that the source is acknowledged.

This Bulletin was produced under the responsibility of the Executive Board of the ECB. Translations are prepared and published by the national central banks.

The cut-off date for the statistics included in this issue was 15 July 2020.

For specific terminology please refer to the ECB glossary (available in English only).

ISSN 2363-3417 (html)

ISSN 2363-3417 (pdf)

QB-BP-20-005-EN-Q (html)

QB-BP-20-005-EN-N (pdf)

- The methodology for computing the EONIA changed on 2 October 2019; it is now calculated as the €STR plus a fixed spread of 8.5 basis points. See the box entitled “Goodbye EONIA, welcome €STR!”, Economic Bulletin, Issue 7, ECB, 2019.

- Eurostat released its GDP estimate on 9 June 2020. In line with expectations of greater than usual revisions (+/-0.1 percentage points) – as some countries had to adapt their national estimation methods, by using alternative sources or different models, to address the disruption in the availability of source data and ensure the best possible quality – the availability of more complete primary source data has already led to an upward revision in the flash estimate of -0.2 percentage points as compared with the preliminary GDP flash estimate released on 30 April 2020.

- See the box entitled “A preliminary assessment of the impact of the COVID-19 pandemic on the euro area labour market” in this issue of the Economic Bulletin.

- See the box entitled “High-frequency data developments in the euro area labour market” in this issue of the Economic Bulletin.

- See the box entitled “Drivers of firms’ loan demand in the euro area – what has changed during the COVID-19 pandemic” in this issue of the Economic Bulletin.

- For more details on recent food price developments, see Box 7 in this issue of the Economic Bulletin.

- See Eurostat’s HICP methodology for more information.

- For further information on these measures of underlying inflation, see Boxes 2 and 3 in the article entitled “Measures of underlying inflation for the euro area”, Economic Bulletin, Issue 4, ECB, 2018.

- For more information on the wage drift, see the box entitled “Recent developments in the wage drift in the euro area”, Economic Bulletin, Issue 8, ECB, 2018.

- For more information, see the box entitled “Short-time work schemes and their effects on wages and disposable income”, Economic Bulletin, Issue 4, ECB, 2020.

- For further analysis of the effectiveness of the ECB’s measures, see the box entitled “The impact of the ECB’s monetary policy measures taken in response to the COVID-19 crisis” in this issue of the Economic Bulletin.

- For further information on how the pandemic is affecting bank lending conditions and firms’ financing needs from a sectoral perspective, see the box entitled “Drivers of firms’ loan demand in the euro area – what has changed during the COVID-19 pandemic?” in this issue of the Economic Bulletin.

- In the second quarter of 2020, the net percentage of banks reporting a tightening of credit standards (i.e. banks’ internal guidelines or loan approval criteria) for loans or credit lines to firms was 1%, whereas the net tightening was 20% for loans to households for house purchase and 25% for consumer credit and other lending to households.

- Swap lines between central banks allow a central bank (the ECB in this case) to receive foreign currency liquidity (US dollars) from the issuing central bank (the Federal Reserve System), which keeps the recipient currency (the euro) as collateral until maturity. In turn, the recipient central bank lends the foreign currency liquidity that it receives to domestic banks against eligible collateral. In line with the ECB's press release published on 17 June 2014, US dollar tender operations offered by the Eurosystem follow a fixed rate and full allotment procedure, i.e. the ECB satisfies all bids received from counterparties against eligible collateral. In 2011 the ECB, together with the Bank of England, the Bank of Canada, the Bank of Japan, the Federal Reserve, and the Swiss National Bank, established a network of swap lines enabling the participating central banks to obtain currency from each other. For more details, see the ECB’s website and the Federal Reserve’s website.

- The MMSR dataset consists of transaction-by-transaction data of the 50 largest euro area banks, based on the value of balance sheet assets, including their FX swap activity. For more details, see the ECB’s website.

- See the box entitled “Alternative scenarios for the impact of the COVID-19 pandemic on economic activity in the euro area”, Economic Bulletin, Issue 3, ECB, Frankfurt am Main, 2020.

- The authors would like to acknowledge the contributions from Mariano Mamertino, Séin Ó Muineacháin and Mirek Pospisil in providing the aggregate and sectoral high-frequency LinkedIn data used in this box, which are based on a joint research project. We would also like to thank Colm Bates (European Central Bank), together with Tara Sinclair and Adhi Rajaprabhakaran (Indeed), for providing the data on job postings.

- For more details, see the article entitled “Assessing bank lending to corporates in the euro area since 2014”, Economic Bulletin, Issue 1, ECB, 2020.

- See the ECB’s website for reports on the euro area bank lending survey. For more details on the BLS, see Köhler-Ulbrich, Petra, Hempell, Hannah S. and Scopel, Silvia, “The euro area bank lending survey”, Occasional Paper Series, No 179, ECB, September 2016, and the article entitled “What does the bank lending survey tell us about credit conditions for euro area firms?”, Economic Bulletin, Issue 8, ECB, 2019.

- Alternative survey indicators directly related to firms’ investment needs provide detailed complementary information but tend not to be available in a similarly timely fashion. See the box entitled “Business outlook surveys as indicators of euro area real business investment”, Economic Bulletin, Issue 1, ECB, 2020.

- . Durable goods consumption, alongside residential investment, is generally considered a strong leading indicator of business cycles. See Mian, A. and Sufi, A., “Household Leverage and the Recession of 2007-09”, IMF Economic Review, Vol. 58, No 1, 2010, pp. 74-117.

- For more details, see the article entitled “The economic impact of population ageing and pension reforms”, Economic Bulletin, Issue 2, ECB, 2018, and the article entitled “Labour supply and employment growth”, Economic Bulletin, Issue 1, ECB, 2018.

- The authors of this article are members/alternates of one of the user groups with access to TARGET2 data in accordance with Article 1(2) of Decision ECB/2010/9 of 29 July 2010 on access to and use of certain TARGET2 data. The ECB, the Market Infrastructure Board and the Market Infrastructure and Payments Committee have checked the article against the rules for guaranteeing the confidentiality of transaction-level data imposed by the Payment and Settlement Systems Committee pursuant to Article 1(4) of the abovementioned ECB Decision. The views expressed in the article are solely those of the authors and do not necessarily represent the views of the Eurosystem. The authors thank Carlos Luis Navarro Ramirez for research assistance.

- For instance, if an airline company in the Netherlands acquires an aeroplane from a company in France, the transfer of the payment can be made in TARGET2 via their banks. Other payment and securities settlement systems such as EURO1, a pan-European large-value payment system, and STEP2, a pan-European retail payment system, also settle their participants’ net positions in TARGET2.

- In 2019 TARGET2 settled an average of €1.7 trillion on a daily basis, corresponding to 344,120 transactions (see TARGET Annual Report 2019, ECB, Frankfurt am Main, May 2020).

- A correspondent bank is a bank that provides services on behalf of another bank.