Published as part of the ECB Economic Bulletin, Issue 1/2023.

This box summarises the findings of recent contacts between ECB staff and representatives of 73 leading non-financial companies operating in the euro area. The exchanges took place between 4 and 12 January 2023.[1]

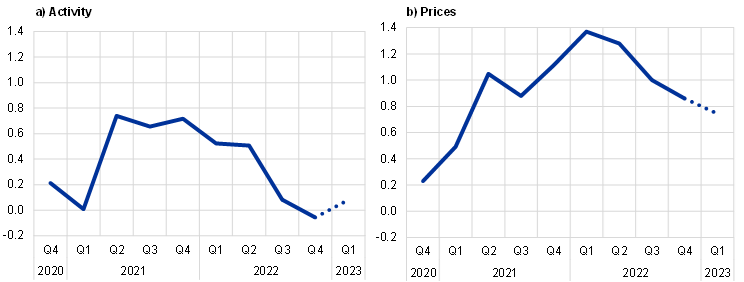

In aggregate terms, these contacts pointed to broadly stagnating or mildly contracting activity in the fourth quarter, but with notable differences across sectors. There were widespread accounts of contracting orders and sales related to both a softening in household spending and unusually large end-of-year inventory adjustment. But other factors were reported that supported ongoing growth in many sectors, including the easing of supply constraints and lingering catch-up effects.

Most industrial sector contacts reported declining activity, reflecting reduced demand for many consumer durables, weakening construction output and inventory adjustment. Demand for consumer electronics and many household items was falling owing to both higher prices (squeezing household budgets) and the fact that purchases of such items had often been brought forward during the pandemic. Construction activity (especially in relation to residential buildings) was increasingly affected by reduced demand owing to rising input costs and interest rates. Meanwhile, end-of-year inventory reduction was larger than usual, in part because high prices had made working capital more expensive, but also because previous supply disruption had caused firms to hold more inventory than usual. The combination of softening consumer demand in some sectors and inventory adjustment caused a particularly sharp contraction in demand for many intermediate goods as well as for services related to the transport and storage of goods, where shortages had been rapidly replaced by excess capacity.

By contrast, consumer demand for many non-durable goods and services was more resilient, while easing supply constraints supported the production of automotive and investment goods. Contacts in the consumer goods and retail sectors pointed to widespread evidence of consumers shifting their consumption towards less expensive items. Yet they also observed that those who had money were prepared to spend it, as reflected in good – or better than expected end-of-year sales. There was particularly strong demand for luxury goods, while passenger air travel had recovered further over the Christmas period. Meanwhile, activity in the automotive and capital goods sectors continued to be characterised by long order books and production levels that were still determined by only gradually easing supply constraints (related to the ongoing short supply of semi-conductors and related components). Consistent with this, most contacts said that for 2023 their firm’s planned levels of investment were similar to or higher than those in 2022. This partly reflected a need for investment to “catch-up” following cuts in 2020-21 as well as some strong medium-term drivers such as digitalisation, the energy transition, and efforts to make supply chains more resilient.

The short-term outlook for activity remained subdued, and the outlook for 2023 was very uncertain, but there was increased hope of a pick-up during the year. Grounds for modestly increased optimism were based on the recent fall in energy prices and high gas storage levels (alleviating concerns about energy shortages). It also reflected the fact that continued strong employment, higher wages and government support, coupled with early signs of easing inflation, would arrest the decline in real disposable income. The end of China’s zero-COVID policy was also likely to give a further boost to global demand from spring onwards.

Chart A

Summary of views on developments in and the outlook for activity and prices

(averages of ECB staff scores)

Source: ECB.

Notes: The scores reflect the average of ECB staff scores in their assessment of what contacts said about quarter-on-quarter developments in activity (sales, production and orders) and prices. Scores range from -2 (significant decrease) to +2 (significant increase). A score of 0 would mean no change. The dotted line refers to expectations for the next quarter.

There was increased caution with respect to hiring intentions and an easing of some labour shortages, but no abrupt change in labour market conditions. Many contacts said that their companies were scrutinising hiring decisions more closely and/or had postponed or scaled down new hiring, but there was little or no suggestion of significant layoffs. Instead, firms were focusing on improving the productivity of existing staff and were reluctant to let go of skilled employees who would be needed in future. Employment agencies observed lower demand for temporary staff but resilience in the market for permanent placements. Meanwhile, there were slightly fewer reports of labour shortages, which seemed to be easing in some sectors.

Selling prices continued to increase in aggregate but at a moderating pace and with more variability across sectors and a less certain outlook. In most sectors, prices had continued to rise in the fourth quarter of 2022 (or the underlying trend was still upwards), and further price increases had been implemented, were planned or would be attempted in the first quarter of 2023. The rate of price increases remained particularly elevated in the food retail and agri-industry sectors. Prices for many consumer and capital goods and for most services also remained dynamic because the pass-through of earlier and/or ongoing cost pressures (now driven by wages in particular) required higher prices to maintain margins, while in some cases prices were raised automatically through indexation clauses. Contacts also pointed to upward pressure on rental prices for housing, as the market in many countries was increasingly tight and/or indexation clauses took effect. Selling prices had started falling (from very high levels) in recent months in some sectors, including energy and many parts of the intermediate goods sector (steel, chemicals, paper, etc.). Spot freight rates in the transport sector (for haulage and container shipping) had fallen sharply, although such rates did not reflect the long-term contract prices on which most business was based.

Many companies had adopted more dynamic pricing strategies in 2022 and said that prices would continue to be reviewed more often than usual in 2023. The effective likelihood that they would increase prices would, however, depend on the ‒ increasingly uncertain ‒ evolution of input costs and (price sensitivity of) demand. Despite greater wage cost pressure and very high uncertainty regarding the future path of energy prices, most contacts expected lower price growth in 2023 than in 2022.

Wage growth was now the predominant cost concern, although wage expectations remained unchanged from the previous survey round. Most contacts expected wage growth to be higher in 2023 than it had been in 2022. Taking a simple average of the mid-points of the quantitative indications provided, contacts estimated that average wages had grown by around 3.5% in 2022, while they anticipated growth of around 5% in 2023. Some expressed concern that, unlike rising energy or raw material prices, wage increases were permanent and would thus have longer-lasting effects. Others, however, observed that wage increases were below present inflation rates and therefore fell short of what would be necessary to fuel a wage-price spiral.

For further information on the nature and purpose of these contacts, see the article entitled “The ECB’s dialogue with non-financial companies”, Economic Bulletin, Issue 1, ECB, 2021.