Published as part of the ECB Economic Bulletin, Issue 5/2022.

This box provides a quantitative assessment of the fiscal policy measures adopted by euro area governments in response to the war in Ukraine and their macroeconomic impact. The discretionary fiscal measures adopted by euro area governments since Russia’s invasion of Ukraine on 24 February 2022 have three main objectives: curbing the rise in energy costs, increasing defence capabilities in euro area countries and Ukraine, and addressing the refugee crisis. Some governments have also extended liquidity support in the form of guarantees, although this would, in principle, affect their budget balances only if the guarantees (contingent liabilities) are called on.[1] Moreover, several support initiatives have been adopted at the EU level, including direct help for the Ukrainian government. Against this background, this box focuses on fiscal stimulus measures that have a direct impact on the budget balance of euro area countries. It also provides estimates for the impact of such measures on euro area growth and inflation over the period 2022-24.

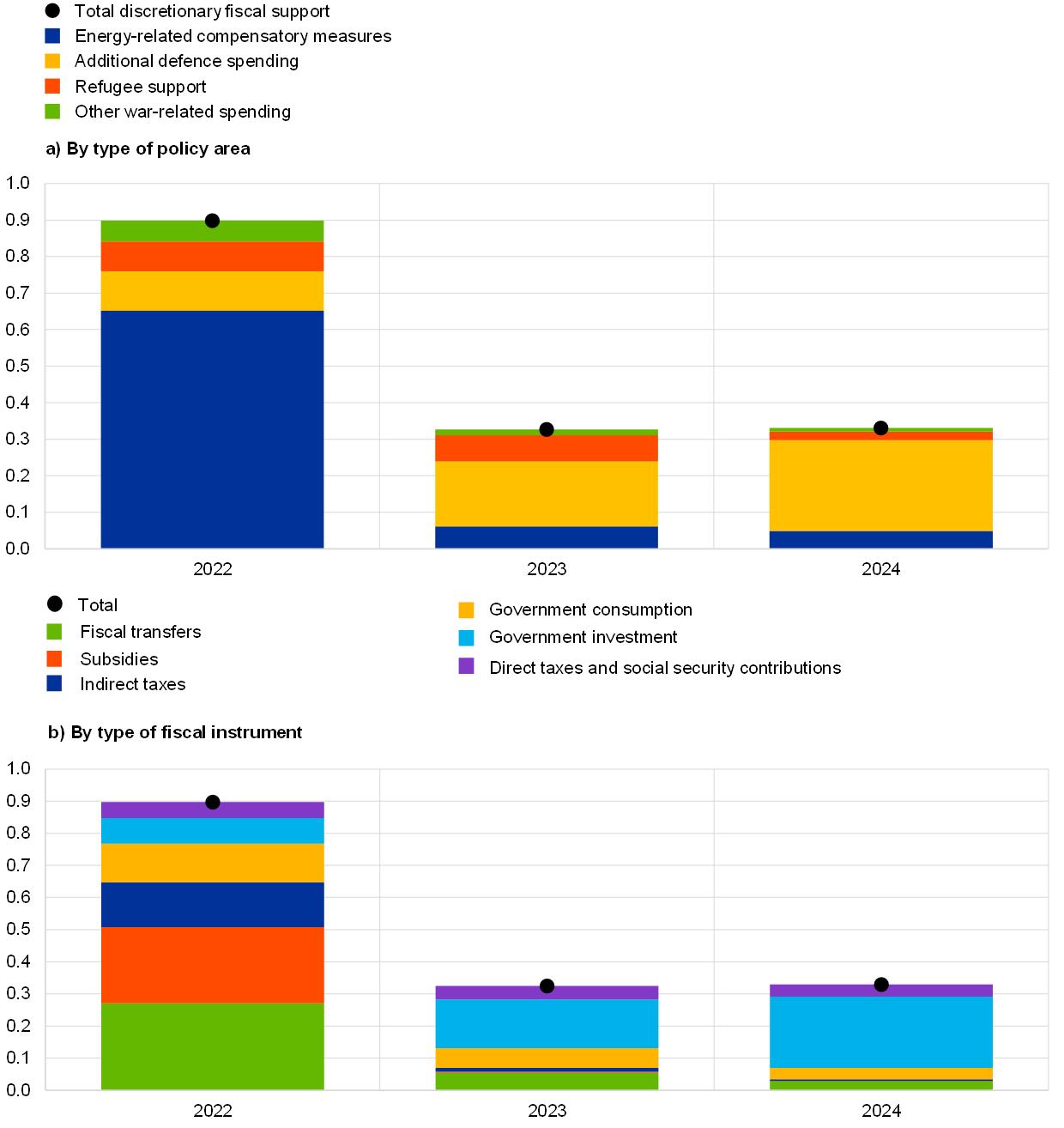

Euro area discretionary fiscal support in response to the war in Ukraine, embedded in the June 2022 Eurosystem staff baseline projections, is estimated at close to 1% of GDP in 2022.[2] Three-quarters of this support represent further compensatory measures introduced in response to the increase in energy prices after Russia’s invasion of Ukraine (Chart A, panel a). It should be noted that several euro area countries had already adopted measures to address rising energy costs before the invasion.[3] The rest of the war-related support is associated with defence spending and refugee support. A large part of the fiscal support, particularly the energy-related component, is estimated to unwind over the period 2023-24. At the same time, defence spending is projected to rise more sharply by the end of the projection horizon. Overall, based on government plans at the time of the June 2022 projections, about one-third of the stimulus is expected to continue over the projection horizon. Eurosystem staff identify the risks to these baseline assumptions to be tilted towards additional fiscal stimulus, stemming in particular from the extension of energy-related compensatory measures.[4]

In terms of composition by fiscal instrument, most of the war-related measures are on the expenditure side. More specifically, the majority of euro area fiscal support introduced in response to the war, with effect in 2022, consists of fiscal transfers and subsidies, as well as cuts in (energy-related) indirect taxes (Chart A, panel b). The bulk of the support over the period 2023-24 is currently expected to consist of government investment, primarily on defence spending. Most of the measures are estimated to be debt-financed, with some amounts intended to be covered through revenues from the EU Emissions Trading System and relatively limited offsetting discretionary measures.[5]

Chart A

Euro area fiscal measures related to the war in Ukraine

(percentage of euro area GDP)

Sources: June 2022 Eurosystem staff macroeconomic projections and ECB calculations, based on the ESCB Working Group on Public Finance (WGPF) fiscal questionnaires.

Notes: “Other war-related spending” includes other direct transfers to Ukraine, the build-up of strategic gas reserves and support for companies other than those in the three main categories identified. “Fiscal transfers” consists mainly of direct support from the general government to households and, to a lesser extent, capital transfers to firms. “Subsidies” are current unrequited payments from the general government to resident producers (firms), mainly intended to lower energy prices. The fiscal measures are shown in terms of (ex ante) budget cost, in levels, per year. The war-related compensatory energy support, broadly denoting measures approved after 24 February 2022, is hereby proxied by the revisions in the estimated budget cost compared to the March 2022 ECB staff projections.

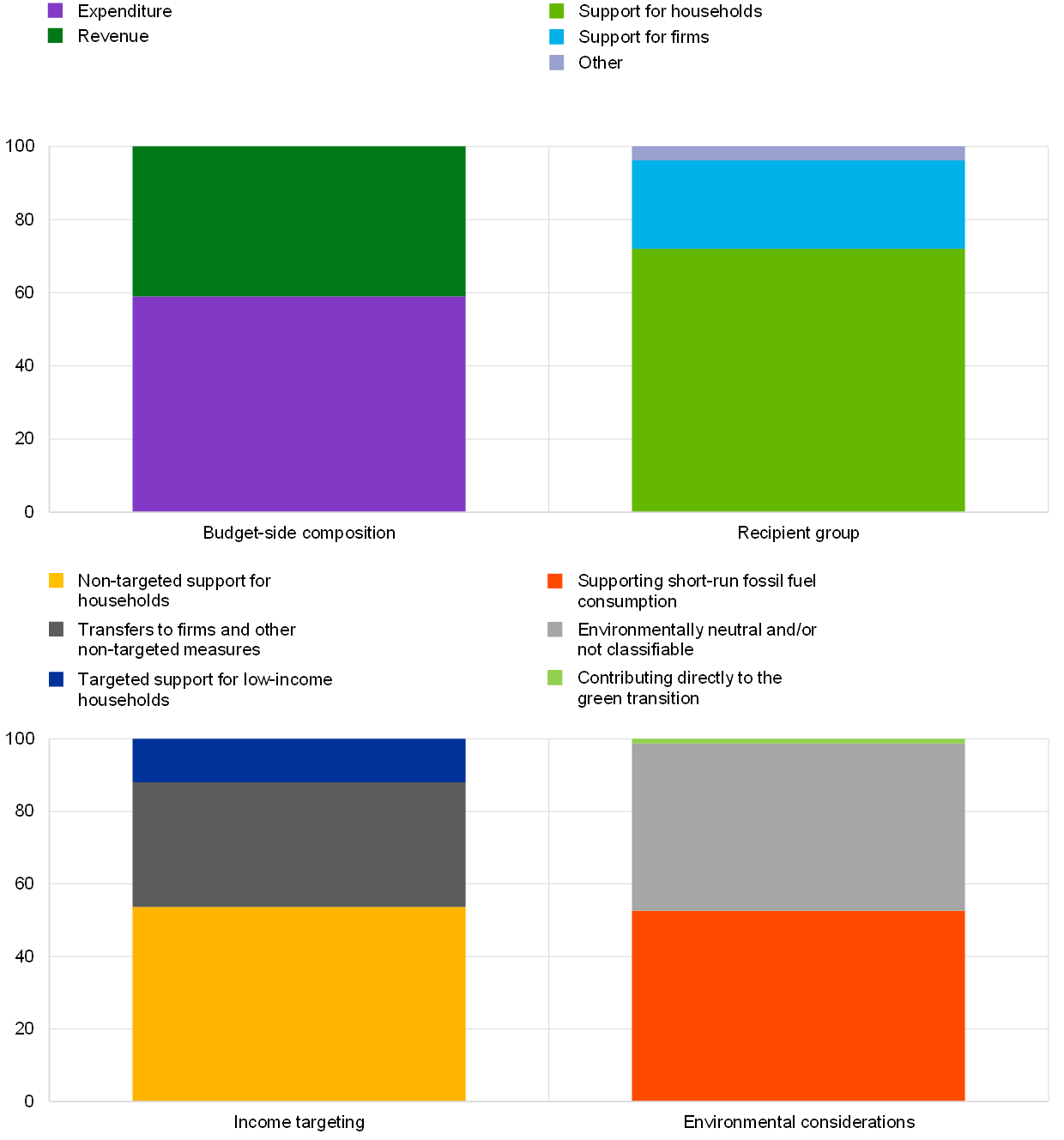

The overall energy-related compensatory measures in place in 2022 have been classified into four categories by Eurosystem staff[6] (Chart B):

- Budget-side composition: Measures on the expenditure side have a somewhat larger share in terms of euro area budgetary impact in 2022 (close to 60%).[7] They relate mostly to fiscal transfers to households and subsidies to firms. This type of spending is either linked to energy consumption or takes the form of lump-sum payments to households. Where euro area countries have introduced a freeze on energy prices, governments provide subsidies or capital transfers to energy providers or compensate for service charges/fees. On the revenue side, measures mostly relate to cuts in energy taxes (excise duties) on electricity, natural gas and solid fuels, and, to a lesser extent, cuts in VAT on energy products.[8] In addition, euro area countries have cut other taxes or fees related to energy consumption, such as environmental surcharges, network fees or system charges.

- Recipient group. Most of the measures approved for 2022 are directed at households (somewhat above 70% of the total budget impact).[9] Several countries have also extended support for firms in the most affected sectors, but this has a more limited fiscal impact.

- Income targeting. In terms of their impact, around 12% of euro area measures target low-income households (that is, measures which include clearly stipulated means-tested income criteria). These targeted measures take the form of rebates, vouchers for electricity or heating costs, and lump-sum payments to low-income households. Around 54% of the total measures are considered to represent non-targeted support for households, with the remaining 34% consisting of transfers to firms and other measures generally not targeting a certain income level.

- Environmental considerations. Based on the information available so far, slightly more than 1% of the total measures in terms of budgetary impact are estimated to contribute directly to the green transition. Around 53% of measures could be classified as supporting short-run fossil fuel consumption, while the other 46% represent “environmentally neutral” measures, including those that are currently difficult to classify. Tax cuts and subsidies for fossil fuels incentivise neither the efficient use of energy nor investment in energy-saving technology. Some countries have introduced “green measures”, including subsidies for public transport or VAT reductions and subsidies for renewable energy sources.

Chart B

Overall euro area measures to curb high energy prices in 2022

(percentage share of total based on the 2022 budgetary impact)

Sources: June 2022 Eurosystem staff macroeconomic projections and ECB calculations, based on the Working Group on Public Finance (WGPF) fiscal questionnaires and Eurosystem staff assessment.

Notes: In the “Recipient group” bar, the category “Other” includes, inter alia, the building-up of gas reserves and recapitalisations of state-owned enterprises. In the ”Income targeting” bar, the category “targeted support for low-income households” denotes the measures intended to directly support households based on clear means-tested income criteria. In the category “Transfers to firms and other non-targeted measures”, some measures (about 5% in this category) refer to support granted only to specific sectors, such as agriculture or transportation, characterised by a higher share of low-wage workers compared with other sectors.

Besides the measures to curb high energy prices, the euro area fiscal response to the war mainly involves defence and refugee spending. The increase in euro area defence spending, embedded in the June 2022 Eurosystem staff macroeconomic projections, reflects first and foremost announced additional defence spending in Germany. Several other euro area countries have announced that they plan to increase their military capacity, with many referencing the NATO commitment to invest 2% of GDP in defence spending. However, few countries have outlined their plans in detail. Finally, additional spending has been approved in several countries to address the Ukraine refugee crisis, with this spending making up a larger share of total support primarily in central and eastern European countries.

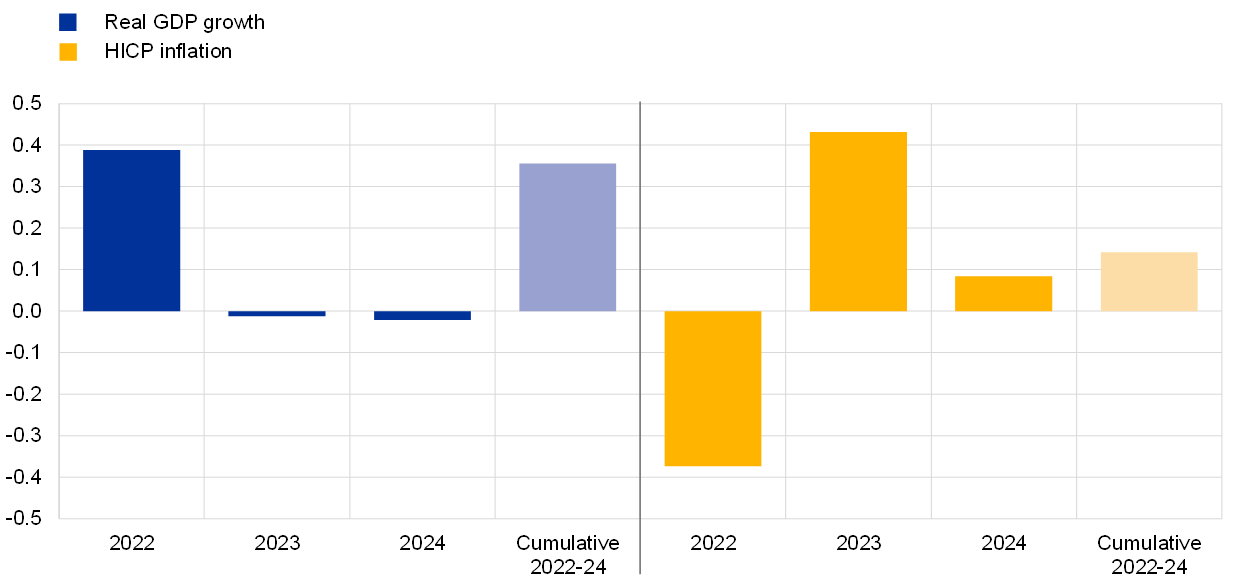

In terms of their macroeconomic impact, the war-related fiscal measures are estimated to have a positive effect on GDP growth and to temporarily reduce inflationary pressures in 2022. Harmonised country-level simulations based on the ECB and ESCB models indicate that the war-related measures described above could increase euro area GDP growth by about 0.4 percentage points and reduce HICP inflation (mainly by lowering energy price inflation) by just under 0.4 percentage points in 2022 (Chart C).[10] In 2023, the impact on growth is estimated to fade, while the impact on inflation is expected to be broadly reversed. In cumulative terms over the projection horizon, the total stimulus measures in response to the war are estimated to have an impact of almost 0.4 percentage points on overall growth and a limited impact of just over 0.1 percentage point on inflation. The harmonised simulations are subject to uncertainty. The HICP inflation impact, which feeds mainly through the energy component, will depend on how much subsidies affect consumer prices, as well as on other behavioural responses stemming from country-specific features of the measures. The growth impact will depend on the effectiveness of the measures in stimulating short-run consumption and, particularly for the period 2023-24, on the actual effect of the defence spending, which is currently expected to come mostly in the form of government investment.[11]

Looking ahead, if additional public support is required, financial resources should be used efficiently. Efforts should be made to increasingly target energy-related compensatory measures to the most vulnerable households.[12] Moreover, incentives should be geared towards reducing the use of fossil fuels and dependence on Russian energy, while maintaining sound public finances.

Chart C

Macroeconomic effects of budget support related to the war in Ukraine

(percentage points)

Source: ECB calculations.

Notes: The simulations are conducted with two sets of models regularly used in the Eurosystem’s forecasting exercises: the ECB’s New Multi-Country Model (NMCM) and the basic model elasticities (BMEs), a platform based on national central banks’ macroeconomic models. Simulations take into account only those fiscal measures with a direct budgetary impact; they do not cover other government (regulatory) measures whose direct costs may be borne by the private sector.

Several euro area countries have approved either specific guarantee schemes for firms affected by the war or have allowed these firms to benefit from the unused budgeted amounts approved in the context of the COVID-19 pandemic.

This refers to fiscal policy measures taken by the cut-off date for fiscal assumptions, namely 24 May 2022. For more details, see the June 2022 Eurosystem staff macroeconomic projections for the euro area.

Such measures introduced in 2021 are estimated at around 0.2% of euro area GDP. Some of this support was extended into 2022, while new measures were approved between 1 January and 24 February 2022. Together with the measures adopted after 24 February 2022, which represent around 0.65% of euro area GDP (Chart A), the overall energy-related fiscal support is estimated at 0.8% of GDP in 2022.

Indeed, since the cut-off date used for the June 2022 projections, several governments have already announced the extension of measures and/or the introduction of new measures beyond those considered in the baseline projections. Moreover, risks of additional fiscal policy responses may materialise in a downside scenario related to the economic impact of the war, such as the scenario presented in Box 3 of the June 2022 Eurosystem staff macroeconomic projections.

Notably, a discretionary measure specifically intended to compensate for part of the energy-related support has been approved in Italy. It is a claw-back tax on energy producers’ profits – that is, a one-off levy of 25% which will apply to net sales that rose by more than €5 million during the period October 2021-April 2022 compared with one year earlier, excluding cases where the profit margin rose by less than 10%.

It should be noted that this classification is not straightforward in some cases and is necessarily based on assumptions in these cases.

The assessment in this box considers euro area aggregate data, although it is recognised that there are variations at country level.

In the case of VAT, EU Member States may apply reduced VAT rates on energy products as long as they respect the minimum criteria laid down in the EU VAT Directive (Council Directive 2006/112/EC of 28 November 2006 on the common system of value added tax (OJ L 347, 11.12.2006, p. 1)), and they consult the VAT Committee. For excise duties, Member States can reduce their rates to the minimum defined by the current Energy Taxation Directive.

VAT cuts are mostly classified as support to households.

For a discussion of factors other than direct fiscal measures related to the impact of the war in Ukraine on the energy markets, see the box entitled “The impact of the war in Ukraine on euro area energy markets”, Economic Bulletin, Issue 4, ECB, 2022. This box also presents estimates related to the contribution of fiscal measures on the tax side to reducing HICP energy inflation as at April 2022.

Some spending may not go into productive investment, instead taking the form of other fiscal instruments such as public wages. It may not feed into the domestic production of military equipment either, but public investment could include military deliveries from abroad. As a result, the related fiscal multipliers may be lower than considered in the present simulations.

See also the European Commission’s recommendations in the context of the 2022 European Semester to “Supporting policies should be temporary and targeted to the most vulnerable in order for them to be most effective, while maintaining incentives to reduce the consumption of fossil fuels and containing their budgetary impact.”