- THE ECB BLOG

How tariffs threaten business dynamism, productivity and growth

25 February 2026

Tariff hikes are putting European companies under strain at a time when productivity growth is already sluggish. Short-term business sentiment is not the only thing at stake. Tariffs could also dampen business dynamism, a key channel for innovation and long-term growth.

Business dynamism – the constant churn of firms entering the market, growing, contracting and then exiting – is crucial for productivity. Through “creative destruction”, new firms with better technologies and business models take the place of their older, less efficient counterparts. Meanwhile, competition compels incumbent firms to innovate, invest and stay sharp if they want to remain competitive. When this process weakens, productivity slows. This blog post focuses on how the current trade tensions are threatening incumbents in the euro area. Specifically, it looks at their risk of exit and their decisions to scale up or down. It also examines why tariffs matter for productivity and long-term economic growth and what this means for monetary policy.

Do trade tensions pose a risk to the euro area outlook?

Before we delve into the details, let’s take a step back and set the scene.

Last year’s tariff increases are already weighing on the euro area economic outlook.[1] However, beyond the immediate impact on exports lies a deeper concern: if export-oriented firms – which are typically more efficient and innovative – scale back their activity or shut down entirely due to higher tariffs, the economy will lose some of its strongest producers. This will make resource allocation less efficient. It will slow the spread of new technologies. And overall productivity will decline over time.

Uncertainty amplifies these effects. When firms cannot reliably predict conditions of trade, and hence future revenues, they tend to adopt “wait-and-see” strategies. They delay investment. They postpone their expansion plans. And they often shift innovation away from risky frontier research towards safer, more incremental projects. While these strategies may protect firms in the short term, they also slow the pace of technological progress across the economy. A prolonged period of high uncertainty and pressure on profits can therefore weigh on growth for years.

What can the firm-level data tell us?

To understand how firms respond to trade tensions, we need detailed data. Firm-level administrative records – though sometimes delayed and with larger firms over-represented – offer a window into the mechanisms that drive business creation, expansion and exit.

We draw on detailed data for Germany, Spain, France and Italy from 2008 to 2023 to examine how trade tensions affect incumbent businesses based on their exposure to international markets.[2] Exposure is identified by taking sectors whose share of sales to the United States stands above the median within each country. These are industries whose exports to the United States are greater than those of at least half of the other industries in the same country.

Our dataset combines information from Orbis and BACH, covering more than three million firms and around 27 million observations. This robust information allows us to track firm growth and exit patterns. It also enables us to control for firm characteristics, as well as country and sector-specific factors – for instance, the exceptional disruption caused by the COVID-19 pandemic.

To capture swings in global trade tensions, we use a text-based index that counts newspaper mentions of tariffs, trade disputes, retaliation and related topics.[3] Only sharp spikes – significant deviations from historical patterns – are classified as trade shocks. Unsurprisingly, the most notable episode in our sample coincides with the first Trump Administration.

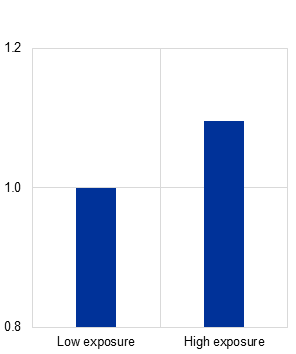

Our results show that trade shocks lowered the chances of firms expanding (Chart 1, panel a) and raised the risk of firms exiting (Chart 1, panel b). These effects were strongest for firms that were heavily exposed to the United States, although the differences between highly export-oriented firms and the rest were moderate, albeit statistically significant.

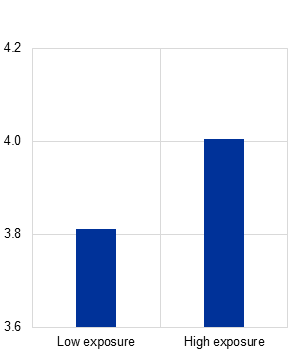

This matters because the firms that are most exposed to trade with the United States are also, on average, the most productive (Chart 1, panel c): they generate more value added per worker and are often more innovative. When these firms shrink or exit altogether, the economy loses not only jobs, but also some of its most productive capacity and dynamic elements.

Chart 1

Trade shocks and firm performance by exposure to the United States

a) Percentage change in likelihood of job creation | b) Percentage change in likelihood of firm exit | c) Productivity ratio by exposure to trade with the United States |

|---|---|---|

(percentage) | (percentage) | (ratio) |

|  |  |

Sources: BvD Electronic Publishing GmbH – a Moody’s Analytics company, Banque de France, European Commission, Durrani (forthcoming) and ECB staff calculations.

Notes: Trade shock residuals with +1 standard deviation from an AR(1) regression for the trade tensions index by Durrani (forthcoming). Low (high) exposure firms in sectors and countries with a share of sales to the United States below (above) the median. Cox proportional hazards estimates controlling for firms’ balance sheets, size, performance, and country and sector effects. Estimates statistically significant at 99%. In panel c, ratio of productivity (value added per employee) between low and high-exposure firms.

Beyond the obvious: supply chains and fragmentation

And yet, the overall impact of trade tensions on productivity may be even larger than might be suggested by firm-level churn alone. Other transmission channels include:

- supply chain disruptions and costly reorganisations that prioritise resilience over efficiency;

- trade fragmentation, which can reduce the size of export markets and impair economies of scale;

- loss of access to key inputs, undermining production efficiency;

- reduced technology diffusion, which is particularly harmful for catching-up economies.

All of these channels can slow innovation, erode competitiveness and weaken potential growth.

Why does this matter for monetary policy?

Slower productivity growth can reduce an economy’s potential output and increase inflationary pressures. This is because weaker productivity growth limits how fast an economy can expand without pushing up costs and prices. It also lowers the natural rate of interest consistent with stable inflation. This limits the room for central banks to cut interest rates during downturns. As explained in an earlier ECB Blog, weaker productivity growth can also make an economy more sensitive to financing conditions. Even small rate increases can significantly slow investment and hiring.

In short, rising tariffs and persistent trade tensions affect much more than individual firms. They reshape the macroeconomic landscape in which monetary policy operates – narrowing the room for manoeuvre and making the economy as a whole more vulnerable.

The views expressed in each blog entry are those of the author(s) and do not necessarily represent the views of the European Central Bank and the Eurosystem.

Check out The ECB Blog and subscribe for future posts.

For topics relating to banking supervision, why not have a look at The Supervision Blog?

See, for example, European Central Bank (2025), “US trade policies and the activity of US multinational enterprises in the euro area”, Economic Bulletin, Issue 4

Our dataset includes annual values of firm-level characteristics such as age, number of employees and industry, as well as financial variables (e.g. leverage – the ratio of total liabilities to assets), performance indicators (e.g. revenue growth) and the status of the firms (e.g. new entrant or exit). However, firm entry is substantially underreported in the data, which prevents a rigorous analysis of business creation. This limitation is unlikely to materially affect our analysis, as newly established firms tend to be smaller and less export-oriented. In our sample, the share of new firms exposed to US trade is around 2%, while the share of firms with 10+ years is about 60%.

To capture swings in trade tensions, we use a Durrani (forthcoming) text-based indicator constructed from local newspapers in Germany, Spain France and Italy. Each month, articles related to tariffs and trade tensions are identified using a supervised text classification model. The index is computed as the share of identified articles in total articles for a given month.