- 12 JANUARY 2021

- RESEARCH BULLETIN NO. 79

Can consumers’ inflation expectations help stabilise the economy?

Economists have argued that when interest rates set by policymakers cannot go any lower, the economy can be stabilised if consumers expect the rate of inflation to increase. Yet, the evidence for this stabilising effect has been very mixed. In this article we review new evidence from a monthly survey of over 25,000 individual consumers across the euro area showing that consumers are indeed more ready to spend if they expect inflation to be higher in the future. While generalised in the population, the stabilising effect is stronger when nominal interest rates are constrained at the lower bound.

Introduction

In pursuing their policy objectives, monetary policymakers in many advanced economies have set interest rates at unprecedentedly low levels that are typically understood to be close to their “effective lower bound”, i.e. at a point where they cannot be lowered any more. By lowering nominal interest rates central banks have sought to reduce also the real rate of interest, i.e. the nominal interest rate adjusted for any anticipated inflation developments, and thereby to stimulate investment and consumption.[2] However, when nominal interest rates reach their lower bound, the main factor that can further reduce the real rate of interest is a higher rate of expected inflation. In line with this, policymakers have stressed the role of inflation expectations in the effective transmission to the economy of asset purchases and other non-conventional policies. The current context of the coronavirus (COVID-19) pandemic has also given rise to risks of inflation that is too low and highlighted the need to avoid a further drop in inflation expectations as part of the process of macroeconomic stabilisation.[3]

The stabilising effect of higher inflation expectations hinges crucially on the extent to which consumers would act on their inflation beliefs and, in particular, whether they would increase current consumption when inflation is expected to be higher in the future. However, as reviewed in a paper by Candia, Coibion and Gorodnichenko (2020) at the Jackson Hole Economic Symposium in August 2020, it is fair to say that the evidence on whether or not households would behave in this way has to date been very mixed.[4] One important study by Bachmann, Berg and Sims (2015) concluded with a cautionary lesson for central banks that higher inflation expectations may even reduce current consumption when interest rates are constrained by the lower bound. Similarly, Coibion, Georgarakos, Gorodnichenko and van Rooij (2019) report experimental evidence for Dutch households showing that consumers who revise their inflation expectations upwards tend to reduce their spending on durables, at least in the short term.

In this article, we review new evidence on this important issue from our recent study (Duca-Radu, Kenny and Reuter, 2020). The evidence relates to the euro area and exploits the data-rich Joint Harmonised EU Programme of Consumer Surveys which provides quantitative data on consumers’ individual perceptions of, and expectations for, inflation and consumers’ readiness to spend. The survey provides on average 26,440 individual responses on a monthly basis that are highly representative of the populations across the euro area countries. The study documents that an increase in consumers’ inflation expectations relative to their own perceptions of current inflation is indeed associated with a positive response in the readiness to spend. This finding – which is observed with striking consistency across demographic and economic groups and individual euro area countries – supports the view that consumers’ inflation expectations can play a role in macroeconomic stabilisation.

Readiness to spend and the expected change in inflation

When studying the relationship between spending and inflation expectations, we start from a very simple observation: namely, that the decisions about spending that consumers make based on their current expectations of inflation may equally be conditioned by their most recent experience of inflation. Why would consumers’ readiness to spend be influenced by their recent experience of inflation? One possible reason is that if consumers perceive current inflation to be higher, they may perceive their real income or their real wages to be lower.

In line with the above observation, we place at the centre of our analysis the difference between consumers’ expectation of future inflation and their own perception of current inflation. As a result, according to our approach, for higher expectations to help stimulate consumption they must rise relative to a consumer’s own perception of inflation. This approach also brings important practical advantages for empirical analysis of individual consumer data. Most importantly, by focusing on the deviation of expected future inflation from perceptions about current inflation it is possible to control for unobserved factors at the individual level that could potentially distort or bias the analysis. As discussed in, for example, Arioli et al. (2017) for the euro area, such unobserved factors include consumer sentiment about the state of the economy (e.g. optimistic or pessimistic beliefs) as well as emotional survey responses or, more simply, survey measurement error. However, to the extent that both perceptions and expectations of inflation are equally influenced by such unobserved factors, their effect will be cancelled out using the proposed difference.

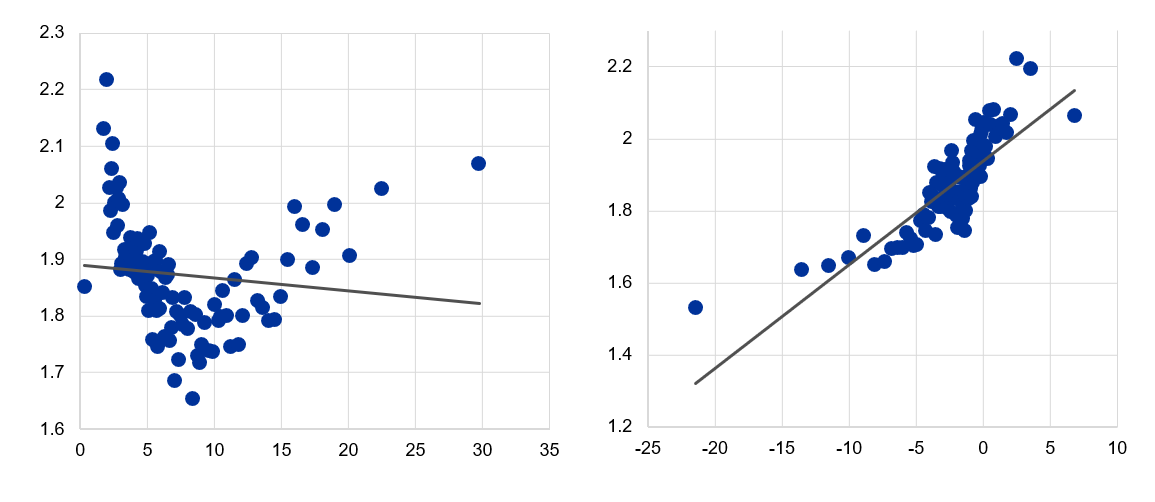

A first look at the data shows that the proposed approach brings a dramatic reassessment of the link between expected inflation and readiness to spend. Chart 1 portrays two scatter plots linking inflation expectations and consumers’ readiness to spend. In the graphical analysis, the consumers’ readiness to spend takes values from 1 to 3, with 1 indicating that they are not ready to spend and 3 indicating that they are ready to spend. To help visualise the relationships, the chart aggregates the individual survey replies by averaging across respondents in each euro area country for each month between January 2003 and December 2016. The relationship between readiness to spend and inflation expectations alone – which may be influenced by unobserved factors and consumer-specific characteristics – is on average negative and also quite unstable (left-hand side chart). However, the data clearly reveal that when normalising inflation expectations around perception about current inflation, i.e. looking at the expected change in inflation (right hand-side chart), a much more stable and positive relationship with the readiness to spend is detected.

Chart 1

Readiness to spend, inflation expectations and the expected change in inflation

(Y-axis: readiness to spend; x-axis: percentage points, inflation expectations (left-hand chart) or the expected change in inflation (right-hand chart))

Note: Binned scatterplots of country aggregates weighted by individual weights at one moment in time identified by month and year, using 100 bins. Readiness to spend is measured on the vertical axis. In the left-hand chart, the horizontal axis depicts expected inflation only while in the right-hand chart the horizontal axis depicts the expected rate of inflation minus the perceived rate of current inflation, i.e. the expected change in inflation.

The above graphical evidence is supported by evidence from a more formal empirical model that is described in detail in Duca-Radu, Kenny and Reuter (2020). One potential concern in such an analysis is that the strong positive correlation observed in the right-hand panel of Chart 1 reflects reverse causation running from consumption to the expected change in inflation and not vice versa. For example, if respondents expect their own spending to correlate also with other consumers’ spending they might expect the overall economic situation to improve and, as a result, also expect stronger inflation in the future. To address this concern, the model explicitly takes into account respondents’ expectations about their own future financial situation as well as their expectations about the overall future general economic situation. As a result, the response of spending to inflation expectations can be estimated whilst holding such additional factors constant.

Estimates using this model reveal very strong statistical evidence for the positive relationship highlighted in the right-hand panel of Chart 1. The results imply a 0.26 percentage point (pp) increase in the probability of being ready to spend in response to a 1.0 pp increase in the expected change in inflation during normal times when interest rates are not constrained, and a higher increase of 0.33 pp when interest rates are constrained by an effective lower bound. This latter value points to an even stronger potential stabilisation role of higher inflation expectations relative to current perceptions about inflation when the lower bound is constraining nominal interest rates. Equally, it points to the potentially stronger destabilising effects of a drop in expected inflation relative to current inflation perceptions in such an environment. Translating such micro evidence to more aggregate macroeconomic conclusions is challenging but our analysis suggests that the response is economically important. Holding perceptions about current inflation constant, a gradual 2.0 pp expected increase in inflation (e.g. from inflation that is too low at 0.0% to a level of 2.0%) is shown to increase euro area consumption by approximately 0.28% in cumulative terms over a three-year period when the effective lower bound is constraining policy and by 0.22% when it is not.

Results hold widely across the population and across countries

More disaggregated analysis reveals that the positive relationship between consumption and the expected change in inflation holds widely across nearly all euro area countries. There are, however, some cross-country differences in the strength of the relationship. For example, the positive spending response is stronger for consumers in countries with higher financial literacy scores – a result which suggests that the stabilising benefits might be augmented by policies aimed at increasing financial literacy. The response is also stronger for consumers in countries where people tend to save a lot and are thus more likely to have a larger stock of accumulated liquid assets which they can use to potentially adjust consumption. Findings across different demographic groups also reveal a consistently positive spending response, though employed consumers and consumers with higher incomes or higher levels of education tend to react more strongly.

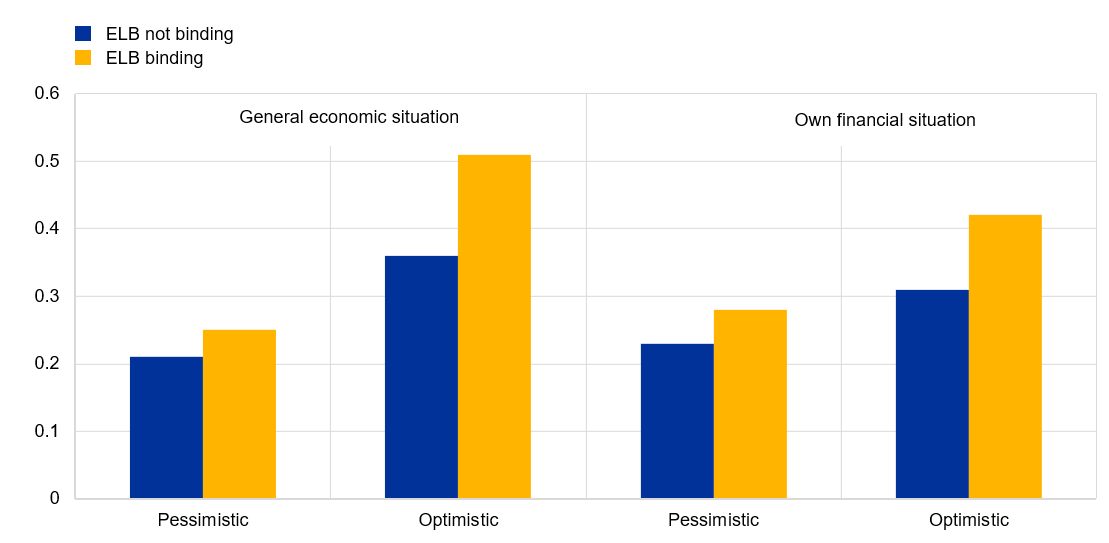

Consumers’ degree of economic pessimism or optimism and their knowledge about official inflation statistics also seem to have an impact on the strength of the spending response. Chart 2, for example, shows that more optimistic beliefs about one’s own future financial situation or about the economy more generally are associated with a stronger spending response. Chart 3 depicts how the spending response differs according to the accuracy of consumers’ inflation expectations, where accuracy is assessed by how well consumers’ inflation expectations can predict the official inflation statistics. The chart shows that consumers with the most accurate expectations, i.e. with an absolute prediction error below 2.0 pp, exhibit the strongest response. Nevertheless, even the spending of consumers with very large absolute prediction errors (above 10.0 pp) responds positively to beliefs about future inflation. Such results suggest that the stabilising benefits of higher inflation expectations might be augmented by policies aimed at increasing the public’s knowledge about official inflation. Equally, the stabilising benefits may be enhanced if beliefs about higher future inflation are associated with greater consumer optimism about the economic outlook.

Chart 2

Spending response to inflation beliefs of optimistic and pessimistic consumers

(Y-axis: change in the spending probability)

Note: ELB refers to the effective lower bound. The chart shows the effect of a unit increase in the expected change in inflation on the probability that consumers are ready to spend given current conditions. The spending probability is measured on a scale of 0 to 100. Consumers are considered optimistic when they expect their own financial situation or the general economic situation to either get a little or a lot better; otherwise they are considered pessimistic.

Chart 3

Spending response to inflation beliefs by forecast accuracy

(Y-axis: change in spending probability; x-axis: absolute mean prediction error)

Note: ELB refers to the effective lower bound. The chart shows the effect of a unit increase in the expected change in inflation or inflation expectation on the probability that consumers are ready to spend given current conditions. The spending probability is measured on a scale of 0 to 100.

Conclusions

Overall, the empirical evidence for the euro area reported here tends to support the potential economic stabilisation benefits of higher inflation expectations when interest rates are constrained. Importantly, our study has not addressed key questions related to the transmission of central bank policies and policy communication to consumers’ inflation expectations. Some recent studies, e.g. Haldane and McMahon (2018), have pointed to the potential benefits of communication strategies that are targeted at specific groups. Other studies, such as Candia, Coibion and Gorodnichenko (2020), have emphasised a risk of unintended effects especially if consumers interpret a rise in expected inflation as bad news for their future economic situation. In the case of the euro area, a new Consumer Expectations Survey[5] – currently being piloted across six euro area countries – will offer a useful research tool to further enrich knowledge on these important issues.

References

Arioli, R., Bates, C., Dieden, H., Duca, I., Friz, R., Gayer, C., Kenny, G., Meyler, A. and Pavlova, I. (2017), “EU consumers quantitative inflation perceptions and expectations: An evaluation”, ECB Occasional Paper No. 186, April 2017.

Bachmann, R., Berg, T. O. and Sims, E. R. (2015), “Inflation expectations and readiness to spend: Cross-sectional evidence”, American Economic Journal: Economic Policy, 7(1), pp. 1-35.

Candia, B., Coibion, O. and Gorodnichenko, Y. (2020), “Communication and the beliefs of economic agents”, paper presented at the Jackson Hole Economic Symposium, August 2020.

Coibion, O., Georgarakos, D., Gorodnichenko, Y. and van Rooij, M. (2019), “How does consumption respond to news about inflation? Field evidence from a randomized control trial”, NBER Working Papers, No 26106.

Duca-Radu, I., Kenny, G. and Reuter, A. (2020), “Inflation expectations, consumption and the lower bound: Micro evidence from a large multi-country survey”, Journal of Monetary Economics, forthcoming.

Haldane, A. and McMahon, M. (2018), “Central Bank Communications and the General Public,” American Economic Association Papers and Proceedings, 108, pp. 578-583.

Lane, P. (2020), “Monetary policy in a pandemic: ensuring favourable financing conditions”, speech at the Economics Department and IM-TCD, Trinity College Dublin, 26 November.

Schnabel, I. (2020), “Covid-19 and monetary policy: Reinforcing prevailing challenges”, speech at the Bank of Finland Monetary Policy webinar: New Challenges to Monetary Policy Strategies, 24 November.

- This article was written by Ioana Duca-Radu (Directorate General Market Infrastructure and Payment Systems, European Central Bank), Geoff Kenny (Directorate General Research, European Central Bank) and Andreas Reuter (DG Economic and Financial Affairs, European Commission). The authors gratefully acknowledge comments from Michael Ehrmann, Alberto Martin and Louise Sagar. The views expressed here are those of the authors and do not necessarily represent the views of either the European Central Bank or the European Commission.

- Schnabel (2020) raises the question of whether the inflation expectations of households and firms may be more relevant than expectations of financial markets in shaping macroeconomic outcomes.

- See, for example, Lane (2020), who emphasised “Tolerating a longer phase of even lower inflation than originally envisaged would be costly and risky. First, it would imply a weaker recovery of consumption and investment, as a result of higher expected real interest rates”.

- See also Duca-Radu, Kenny and Reuter (2020) for a further review of the evidence.

- See Consumer Expectations Survey.