- 26 MAY 2023 · RESEARCH BULLETIN NO. 107

A new tool in the box: dividend restrictions as supervisory policy stimulus

ECB Banking Supervision’s recommendation for banks not to pay out dividends during the coronavirus (COVID-19) pandemic led to increased lending to non-financial corporations. Complying banks’ lending was around 2.2 percentage points stronger than lending by banks not affected by the recommendation. This effect is found to be economically significant but short-lived, and stronger for small and medium-sized enterprises (SMEs) most affected by the pandemic. It did not lead to greater risk-taking by banks. These results suggest that temporarily restricting bank dividend distributions complemented macroprudential, monetary and fiscal policies to support lending during the pandemic crisis.[2]

The ECB recommendation and its impact

On 27 March 2020 the ECB adopted a recommendation asking euro area banks not to pay out dividends, at least until 1 October 2020. The objective of the recommendation was to boost credit institutions’ capacity to absorb losses and to nudge them to continue funding households and SMEs during the pandemic.[3]

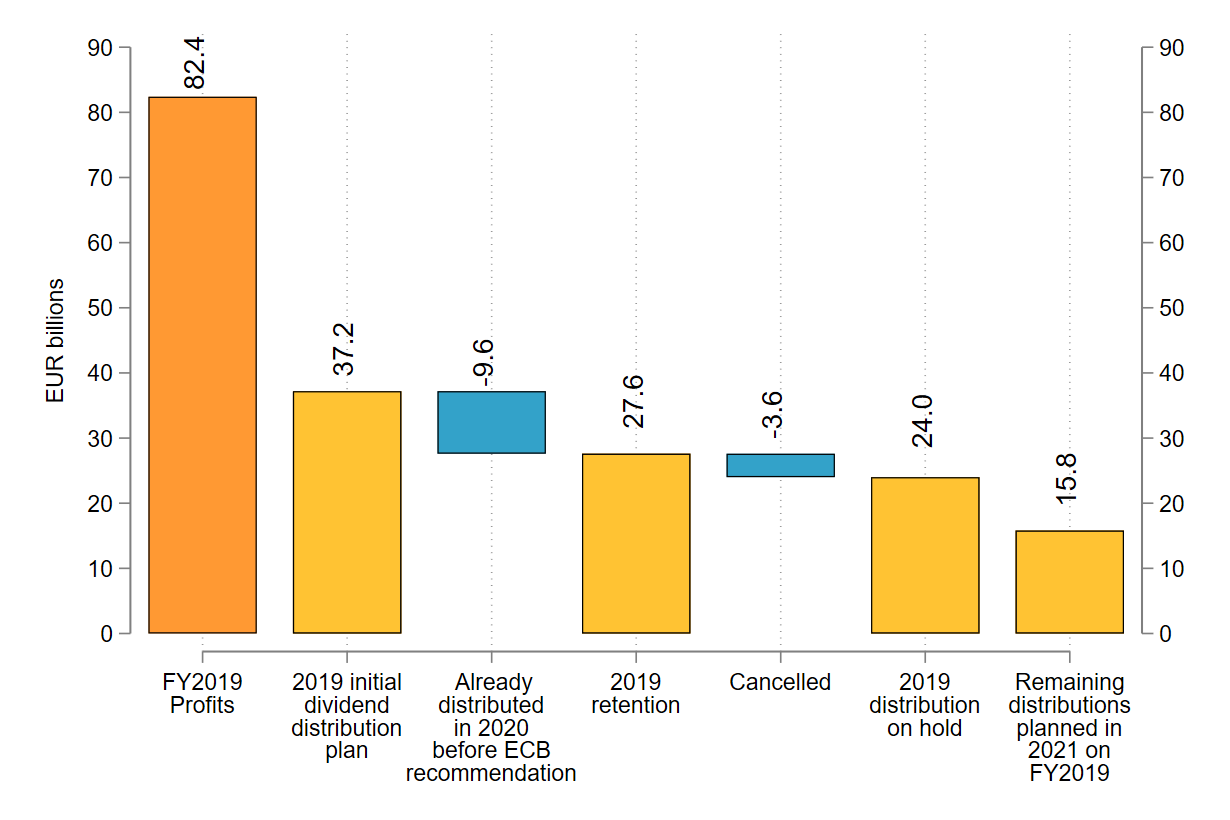

This recommendation was issued in an environment in which banks tended to distribute a substantial percentage of their earnings as dividends. Figure 1 illustrates the cumulative planned dividend distributions prior to the ECB recommendation and the extent of compliance with the policy. At the same time, in a severe crisis, and from a wider social perspective, dividend restrictions can be justified to induce banks to conserve capital and support lending to the real economy. Empirical evidence suggests that in times of crisis banks tend to expand dividend distributions to signal their strength (Acharya et al. 2012; Abreu and Gulamhussen 2013; Wu 2018).

Banks’ managers were faced with a choice of capital allocation when deciding to follow the ECB recommendation and cut dividends, with different implications for credit supply to borrowers. On the one hand, they might opt for using the surplus capital to increase lending supply, thus supporting the economy and acting countercyclically. On the other hand, they could decide to signal – and increase – their resilience to future shocks by saving capital, and/or to strengthen their loss-absorbing capacity by setting aside provisions. The impact on lending to European corporations was therefore uncertain.

Figure 1: Dividend distribution plans of significant institutions

Source: ECB Banking Supervision survey on dividend distribution plans.

Notes: The chart plots the aggregate evolution of dividend distribution plans of significant institutions in the euro area as of March 2020. From the initial plan to distribute €37.2 billion, banks had already distributed €9.6 billion in the first quarter of 2020. As of March 2020, the amount of planned but not yet distributed dividends comprised the 2019 retention.

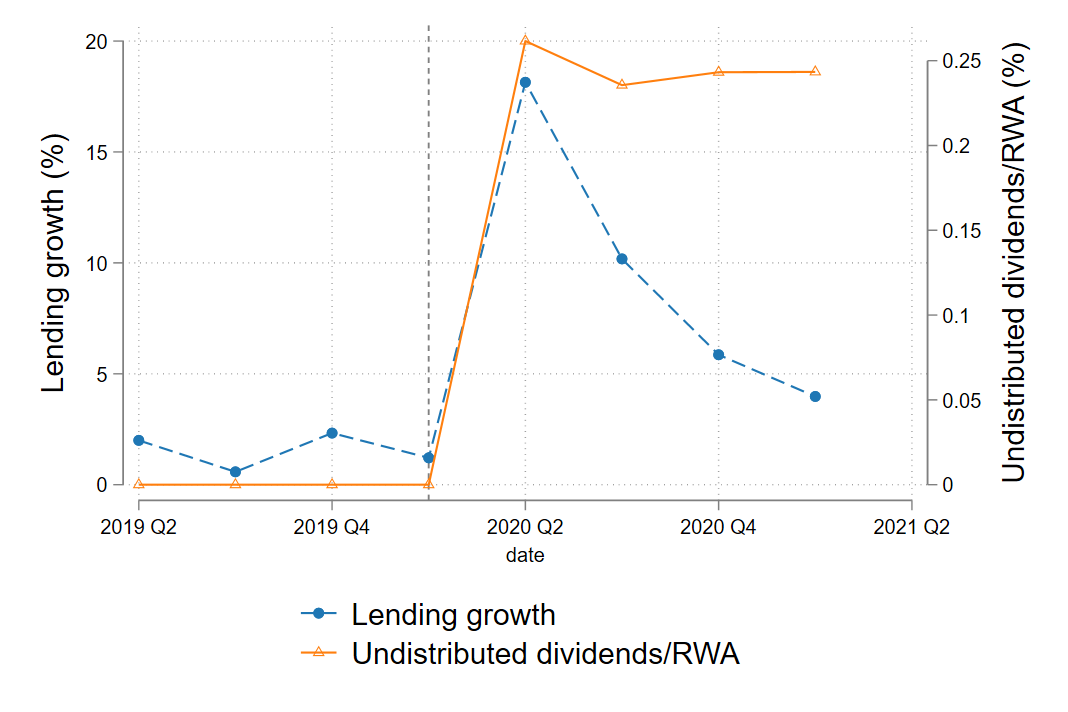

In Dautović, Gambacorta and Reghezza (2023), we compare banks that fully or partially complied with the ECB recommendation with a group of banks that did not change their plans, and we differentiate bank credit supply stemming from the dividend recommendation from credit supply stemming from other pandemic-related support measures.[4] Figure 2 shows the co-movement of credit growth and the planned but non-distributed dividends scaled by risk-weighted assets (RWAs). The growth rate of lending increased in the quarter following the pandemic outbreak, with an unconditional average of 18.1%, before declining monotonically in the subsequent quarters. The amount of non-distributed dividends over RWA spiked immediately after the ECB recommendation, remaining persistent until the end of 2020 at 0.24%.

Our results show an overall positive effect of the ECB’s dividend recommendation on euro area banks’ credit supply to non-financial corporations. The effect is greater for SMEs. The results are also stronger for sectors that were more vulnerable to the effects of the pandemic, suggesting that banks channelled the surplus capital to those firms most affected by the pandemic-related lockdowns.

Figure 2: Credit growth and undistributed dividends

Source: ECB Banking Supervision survey on dividend plans and supervisory reporting.

Notes: The chart illustrates the evolution in credit growth and the planned but not distributed dividends as a share of RWAs. The sample includes all banks. Lending growth is the percentage change compared with the previous quarter, while undistributed dividends are expressed as a percentage of RWAs. The dashed vertical line is at the first quarter of 2020, the time of the ECB dividend recommendation.

We do not find an increase in risk-taking by banks that followed the recommendation. Specifically, lending growth is estimated to be lower when a bank-firm relationship has accumulated impairments, and is null in the case of “zombie” borrowers (i.e. those having above the 95th percentile of impaired loans with a specific bank). Lending growth is lower for banks with high non-performing loan (NPL) ratios. Furthermore, we find that the impact of the ECB’s dividend recommendation is short-lived: the beneficial effect vanishes in the fourth quarter of 2020, and it is mostly concentrated in the second and third quarters of 2020.

Conclusions and policy considerations

Dividend restrictions can be an effective and proven countercyclical supervisory policy tool during times of crisis in the real sector (when non-financial corporations suffer liquidity shortages) – and potentially in financial crisis as well. They can sustain credit growth and have positive real effects, although these effects can be short-lived. The impact of the dividend recommendation tends to be stronger for SMEs and more vulnerable sectors of the economy. Additionally, dividend restrictions can enhance the effectiveness of countercyclical policies in a downturn, showing strong complementarity with government guarantees as a fiscal policy measure.

Implementing a dividend restriction policy can effectively redirect resources from inefficiently high shareholders’ consumption to credit supply. Recent evidence shows that investors’ consumption is excessively influenced by dividend distribution dates (Bräuer et al., 2022). Our results show that undistributed dividends are channelled into loans, which likely have a higher growth multiplier compared to consumption.

It is crucial for dividend restrictions to be temporary in nature to mitigate unintended policy effects, and clear supervisory forward guidance should accompany them. Transparent communication regarding their duration and the rationale behind their implementation can help minimise inefficiencies resulting from an uncertain policy environment. Falling to provide such clarity can undermine financial stability.

Dividend restrictions offer additionally policy improvements. They can simultaneously increase solvency (capital) and enhance loss-absorbing capacity (loan loss provisions). This, in turn, reduces the potential costs borne by debtholders and taxpayers in the event of a bail-in. Moreover, dividend restrictions can address concerns associated with the release and use of macroprudential buffers, as buffer releases can be (mis)used for increased dividend distribution.[5]

References

Abreu, J. F. and Gulamhussen, M. A. (2013), “Dividend payouts: Evidence from U.S. bank holding companies in the context of the financial crisis”, Journal of Corporate Finance, Vol. 22(1).

Acharya, V. V., Gujral, I., Kulkarni, N. and Shin, H. S. (2012), “Dividends and bank capital in the financial crisis of 2007-2009”, NBER Working Paper, No 16896.

Andreeva, D., Bochmann, P., and Schneider, J. (2023), “Evaluating the Impact of Dividend Restrictions on Euro Area Bank Market Values”, Working Papers Series, No 2787, European Central Bank.

Bräuer, K., Hackethal, A., & Hanspal, T. (2022). Consuming dividends. The Review of Financial Studies, 35(10), 4802-4857.

Dautović, E., Gambacorta, L. and Reghezza, A. (2023), “Supervisory policy stimulus: evidence from the euro area dividend recommendation”, Working Papers Series, No 2796, European Central Bank.

Lee, B.-S. (1995), “The response of stock prices to permanent and temporary shocks to dividends”, Journal of Financial and Quantitative Analysis, Vol. 30(1), pp. 1–22.

Todorov, K. (2020). Quantify the quantitative easing: Impact on bonds and corporate debt issuance. Journal of Financial Economics, 135(2), 340-358.

Wu, Y. (2018), “What’s behind smooth dividends? Evidence from structural estimation”, The Review of Financial Studies, Vol. 31(10), pp. 3979–4016.

This article was written by Ernest Dautović (Directorate General Research, European Central Bank), Leonardo Gambacorta (Bank for International Settlements and CEPR) and Alessio Reghezza (Directorate General Macro Prudential Policy and Financial Stability, European Central Bank). The views expressed in this paper are those of the authors and do not necessarily reflect the official positions of the European Central Bank (ECB) or the Bank for International Settlements (BIS). The authors are thankful for the helpful comments provided by Alexandra Buist, Gareth Budden and Alexander Popov.

It is worth pointing out that dividend restrictions can also have short-term negative effects on banks’ stock prices, when the lifting of restrictions is uncertain, increasing funding costs for banks. See, for instance, the recent evidence in Andreeva et al. (2021), and previous work by Lee (1995).

See the ECB press release of 27 March 2020. This was followed by a statement from the European Banking Authority on 31 March 2020. Many national competent authorities subsequently issued their own regulatory announcements in a similar vein.

To control for the confounding effects of monetary policy measures on lending we use the ECB dataset on targeted long term refinancing operations (TLTROs) to control for ECB long term funding provided to banks. We also use the deposits held by banks at the ECB as a measure of the take-up of Asset Purchase Programs (APPs) and Pandemic Emergency Purchase Programme (PEPP). To control for fiscal policy measures we match the euro area credit registry data with bank-firm level information on payment moratoria and government guarantees schemes.

The (mis)use of policy stimulus has been studied also for the case of non-financial corporates (NFCs). Todorov (2020) shows that NFCs which benefited from the ECB's Corporate Sector Purchase Program mostly increased dividend payments, rather than real investments. A dividend restriction policy at the time might have been helpful to avoid this negative externality.