Private markets, public risk? Financial stability implications of alternative funding sources

Private markets, public risk? Financial stability implications of alternative funding sources

Published as part of the Financial Stability Review, May 2024.

Euro area private markets have grown significantly in recent years, providing alternative funding sources for companies and diversification benefits for investors. While private markets are currently small relative to public markets and bank lending in the euro area, continued strong growth, financial innovation and opaqueness in private markets could contribute to financial stability risks. Adverse economic shocks could result in rising defaults, valuation corrections and losses for private funds and their investors. Additionally, such shocks may be exacerbated by multiple layers of leverage at company, fund and investor level, or by liquidity mismatches for some open-ended private funds. For banks, risks could arise from lending exposures to these markets, as well as from rising competition with private funds, which could incentivise lower underwriting and credit standards.

Introduction

Private markets have experienced remarkable growth in the euro area over recent years, bringing both benefits and risks for euro area financial stability. Private markets offer an alternative funding source to companies and real assets, next to public equity, corporate bond markets and bank lending. They fulfil an important economic function, as they match the financing needs of riskier economic entities with the risk-bearing capabilities of long-term investors. Their growth has been driven both by investors’ wishes for high returns, especially during the period of ultra-low interest rates, and by the need of companies for faster and more flexible sources of finance.[1] Despite their strong growth in recent years, private markets in the euro area remain relatively small compared with domestic public markets, bank balance sheets or global private markets. This special feature discusses the main developments in these markets since 2010, as well as risks to financial stability stemming from characteristics of investors, portfolio companies, the structure of intermediaries and links with the banking sector.[2]

Overview of private market segments and strategies

Private markets offer financing to companies through private equity and private credit, and for real assets (Figure C.1). Private market transactions are mainly conducted via closed-ended funds (“private funds”). Private funds include private equity, private credit and real asset funds. Private equity funds invest into firms’ equity, while private credit funds lend to firms and real asset funds invest in assets such as property. These funds are typically accessible only to institutional investors, many of which have a long investment horizon.[3] They also receive debt financing from banks (Figure C.1). When a private fund is set up, the investors commit capital which is typically called over the first years of the fund’s lifetime to finance investment opportunities.[4] Accordingly, the assets under management of a private fund can be split into the net asset value (NAV) of the fund’s portfolio and its “dry powder” – committed, but not yet called capital. Depending on the fund type, investors either receive regular income streams from these investments or are paid out as the fund exits its individual investments or when it is liquidated at the termination date. Some funds, however, have indefinite lifespans (“evergreen” funds). Private markets are regulated relatively lightly, as most funds have limited liquidity mismatches or are closed-ended and focus on institutional investors.[5]

Private equity strategies can be split by the stage of maturity of target companies and degree of equity investment. There are three main private equity strategies. First, venture capital funds typically hold minority equity stakes in young firms and engage operationally with their portfolio companies. Second, by contrast, leveraged buy-out (LBO) funds acquire controlling stakes in mature companies to raise their value by restructuring them and often also replacing their management. Such transactions are typically executed in the context of mergers and acquisitions. They involve a high degree of leverage in the form of syndicated loan financing arranged by banks or through private credit markets. Third, growth capital strategies are usually associated with taking a minority stake in the company, preferring to target mature businesses looking for capital to expand or restructure operations. Across all these strategies, private equity funds realise their returns mainly by selling a portfolio company to a strategic or financial buyer[6] or by conducting an initial public offering.

Figure C.1

Private market funds channel funding from institutional investors to the real economy

Source: ECB.

Notes: PE stands for private equity; PC stands for private credit; CLO stands for collateralised loan obligation. Banks also lend to private credit and real asset funds through NAV lending, which is not shown in the chart.

Private credit strategies differ in the seniority and purpose of lending and usually generate a constant revenue stream. The four most common strategies for funds located in the euro area are direct lending, mezzanine debt, special credit situations and distressed debt.[7] In principle, direct lending is less risky, while other strategies are associated with higher probabilities of default. Until recently, private credit loans have commonly been provided to mid-sized (“middle market”) companies, featured floating interest rates and were neither rated nor broadly syndicated.[8] Private credit loans are not considered transferable securities and are not issued via public offers. They come with lower reporting requirements than (public) corporate bond markets, thus permitting more flexible and more rapid financing. More recently, however, some private credit funds have started bundling their debt into collateralised loan obligation (CLO) vehicles, which are sold to investors in tranches (Figure C.1).

Some private equity and private credit funds are connected by ownership links and co-investments in the same portfolio companies. Most asset managers active in private markets have expanded their business from the equity space to credit, resulting in private equity and private credit funds often being managed by the same asset manager (Figure C.1).[9] The growth in private credit funds is also related to such funds increasingly moving into the business of financing the debt required by private equity funds in LBO transactions, which had traditionally been financed by syndicates of investment banks. In 2023, 81% of European LBOs were financed by private credit, compared with 56% in 2021.[10]

Real asset funds invest into real estate, infrastructure and natural resources via equity and debt instruments. While this special feature mainly focuses on the private equity and private credit subsegments, real assets are usually also considered a subsegment of private markets when investments are carried out via private transactions. This includes private real estate funds, which might be particularly vulnerable to the current downturn in the commercial real estate market.[11]

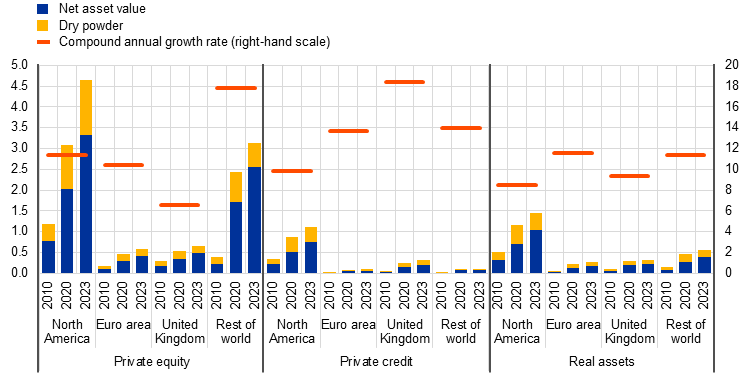

Chart C.1

Private markets remain concentrated in North America, but other jurisdictions have recently experienced significant growth

Private market funds’ assets under management, by fund location and fund type

(Q4 2010, Q4 2020, Q3 2023; left-hand scale: € trillions, right-hand scale: percentages)

Sources: PitchBook Data, Inc. and ECB calculations.

Notes: Private equity includes venture capital funds. Fund location is defined as where the fund management team is located. The red line shows the compound annual growth rate of assets under management between Q4 2010 and Q3 2023 for funds split by location and fund type. Real asset funds comprise funds investing into real estate, infrastructure and natural resources.

Although private market funds remain concentrated in the private equity segment and in North America, other segments and locations have grown significantly over recent years. In the third quarter of 2023, the lion’s share of assets under management in private funds was held by funds located in North America. Private equity funds remain the largest asset class, accounting for 68% of global assets under management in private funds, followed by real asset funds at 20% and private credit at 12%. While assets under management in private funds located in the euro area are still small compared with funds investing in public markets,[12] they have seen steep growth over the last decade. Compound annual growth rates stand at 14% for private credit funds, 12% for real asset funds and 10% for private equity funds (Chart C.1).[13]

Benefits and risks for financial stability

Private markets provide benefits to the economy. They offer an alternative source of funding, with often faster and more reliable execution. For investors, they provide a portfolio diversification option and constant income streams. For the wider economy, private markets often finance the kind of smaller, riskier and innovative firms that are important for future economic growth. In particular, the equity segment of private markets − venture capital, for instance − could play an important role in funding the innovation that is essential for the green and digital transitions.[14] In this respect, growth in euro area private markets can also support the development of the capital markets union in the euro area.

Nonetheless, the opaqueness and strong growth of private markets may give rise to financial stability risks. This special feature later assesses some potential contagion channels by reviewing the characteristics of investors into private markets, portfolio companies, the structure of fund intermediaries, and links between private markets and the banking sector.

Large institutional investors tend to be the main investors in private funds. Globally, insurance corporations and pension funds (ICPFs) account for close to 75% of investments into private equity funds and around 86% into private credit funds.[15] Focusing on entities domiciled in the euro area, the latest available data indicate that occupational pension funds had invested around 4% of their total assets into private equity funds and 2% into infrastructure funds in the third quarter of 2023, while exposures to private credit were likely substantially lower. Insurers had even smaller exposures to private equity, private credit and infrastructure funds, but they had a more substantial share of direct loans on their balance sheets (Chart C.2, panel a). While the general move of ICPFs into illiquid assets – including private funds – was to some extent driven by their search for yield during the period of ultra-low interest rates, they represent the financial sector with the highest capacity to hold illiquid exposures, given their very long-term investment horizons. ICPFs also seem well prepared for managing the liquidity needed to meet the capital calls that are a characteristic of private market investments.

Chart C.2

Uncertainty in private asset valuations might hide losses for institutional investors, who could nonetheless also profit from lower volatility

a) Share of alternative assets in total assets held by euro area insurance corporations and pension funds | b) Performance of euro area-located private credit funds vs public debt indices |

|---|---|

(Q4 2020, Q3 2023, percentages) | (Q1 2020-Q1 2024; indices, 2 Jan. 2020 = 100) |

|  |

Sources: EIOPA, Bloomberg Finance L.P., PitchBook Data, Inc. and ECB calculations.

Notes: Panel a: pension funds include only occupational pension funds. Real estate includes direct holdings of real estate (i.e. physical property) and indirect holdings (i.e. real estate fund and company shares, securities and mortgages). Direct loans exclude mortgages. Other alternative funds are alternative funds as categorised by EIOPA, which also includes private credit funds. Panel b: the performance of private credit funds is calculated as quarterly compounded median internal rates of return. The European leveraged loan index corresponds to the Morningstar European Leveraged Loan TR EUR Index. The euro high-yield bond index corresponds to the ICE BofA Euro High Yield Index. All indices are indexed to 100 as of 2 January 2020.

Despite banks’ limited direct investments into private funds, risks might spill over from private markets via their lending exposures and incentives to lower credit standards. In addition to common exposures to companies which are financed by banks and private markets, banks also lend to private funds and fund investors. These loans are usually collateralised by the funds’ NAV (“NAV lending”) or, in the case of lending to private funds, also by the funds’ dry powder. Private funds might use the additional funding from banks to support their portfolio companies, lever up returns or pay out their investors in a challenging exit environment like the current one.[16] The credit risk from such bank exposures seems contained in both cases, however. First, typical loan-to-value ratios in NAV lending range between only 10% and 15%.[17] Second, market intelligence suggests that the risk of investors defaulting on capital calls, thus undermining the value of loan collateral, is rather small, as the contractual obligation to deliver the capital is strong. Nevertheless, aside from lending exposures, growing private credit markets are increasingly competing with banks’ syndicated lending activities. This, in turn, might incentivise banks to lower their lending standards to protect their market share.

Valuation methods in private markets may disguise potential losses. The nature of holdings in private funds makes it challenging to mark these types of assets to market. In turn, private funds’ assets are valued less frequently and under more subjective model assumptions, which can conceal potential losses, underlying volatility and the correlation between the returns on private funds with other markets. This can lead to cliff-edge losses for institutional investors if private funds only recognise write-downs at the end of individual investments. At the same time, lower reported volatility artificially boosts risk-adjusted returns and might help some investors meet their internal or regulatory risk limits, another incentive for investing into these markets. Compared with high-yield bonds and leveraged loans, median returns on private credit funds did not suffer losses during the pandemic stress period or since the start of the monetary policy tightening cycle (Chart C.2, panel b).

Chart C.3

Private credit is provided to relatively stronger euro area companies than private equity

a) Private credit volume, by euro area borrower sector and geographical distribution of lenders | b) Median interest coverage ratio for private equity and private credit-backed firms, and firms in public equity and bond indices |

|---|---|

(2019-23; left-hand scale: € billions, right-hand scale: percentages) | (Q2 2023, EBITDA/interest expenses) |

|  |

Sources: PitchBook Data, Inc., Bloomberg Finance L.P. and ECB calculations.

Notes: Panel a: sector volume is calculated as the aggregated lending to each sector in 2019-23. Geographical distribution refers to the share of total lending in 2019-23, broken down by lender location. In a debt with several loan underwriters with different geographies, the debt volume is divided evenly between lenders. This is done to avoid double-counting private credit volume in geographical distribution. B2B refers to business products and services; B2C refers to consumer products and services. Panel b: ICR stands for interest coverage ratio; HY stands for high-yield debt; IG stands for investment-grade debt. The ICR of euro public HY is based on median ICRs of companies with bonds in the ICE BofA Euro High Yield Index. The ICR of euro public IG is based on companies with bonds in the ICE BofA Euro Corporate Index. Euro area private equity ICR is based on a sample of 7,093 euro area firms, while euro area private credit ICR is based on 388 euro area firms. Most private credit-backed firms are also publicly listed, but there is little overlap between private credit and private equity-backed companies in the sample considered. The sample includes firms with any available ICRs between Q2 2022 and Q2 2023.

Private lending to euro area companies mainly comes from non-euro area private credit funds and seems concentrated in more innovative sectors. Cross-border lending is an inherent feature of private credit markets, with only around 20% of the volume borrowed by euro area companies being lent by euro area borrowers (Chart C.3, panel a). While private credit funds used to focus on lending to smaller and riskier companies, market intelligence suggests that, in recent years, they have moved further up the credit quality spectrum and into larger deals. According to data from PitchBook covering a sample of 258 deals, median private credit deals in the euro area increased from €75 million in 2021 to €168 million in 2023. In addition, private credit funding seems concentrated in more innovative sectors, such as business products and services, health care and information technology.

Companies backed by private credit do not seem to have worse credit quality than their public peers. Based on available data, on average, private credit-backed companies do not appear to have lower interest coverage ratios – which indicates the extent to which earnings cover interest expenses − than their exclusively public debt-financed peers (Chart C.3, panel b). Importantly, this may suggest that the comparative advantage of private lenders is the greater flexibility and speed of execution rather than their ability to offer funding to riskier borrowers. Additionally, the use of “amend and extend” agreements might prevent defaults from materialising, although it might also add to the risk of delayed recognition of losses for funds and their investors.[18]

By contrast, private equity-backed companies tend to display worse credit quality than their public peers, which raises financial stability concerns. While interest coverage ratios of publicly listed companies average around 13.8 – i.e. on average, their earnings cover almost 14 times their interest expenses on their outstanding debt – those of private equity-backed companies are significantly lower, at 1.6 on average (Chart C.3, panel b). This is likely due to LBO strategies which lever up funds’ portfolio companies, enhancing investor returns. Higher leverage is also connected with higher probabilities of default and lower recovery rates. These vulnerabilities are more likely to materialise in an environment of slow growth and might bring material losses to lenders, including banks and private credit funds. Private equity firms might also have fewer incentives to support struggling companies than strategic investors.[19] On a positive note, globally, private equity funds currently have €2.3 trillion of dry powder available, which gives them room to act countercyclically.

A sizeable share of euro area private credit funds are open-ended funds, which may raise liquidity risks. In contrast to private equity funds, which are primarily closed-ended,[20] approximately 42% of private credit funds have an open-ended structure. Of these funds, most are domiciled in France and Luxembourg (Chart C.4, panel a). Although an open-ended fund structure may help attract investors,[21] it may also highlight potential liquidity mismatches between the illiquid nature of funds’ assets and their redemption terms. Such vulnerabilities may nonetheless be mitigated, depending on funds’ redemption frequency, presence of lock-in periods and availability of liquidity management tools (e.g. redemption gates and temporary suspensions). In addition, the role of ICPFs as main investors may limit liquidity risks for such funds, thanks to their long investment horizons (Chart C.2, panel a).

Chart C.4

Open-ended private credit funds may be exposed to liquidity mismatches, while euro area holdings of private credit CLOs remain low

a) Share of closed- and open-ended euro area private credit funds, by domicile | b) Global CLOs outstanding, by issuer area and type | c) Capital structure and share of senior loans of US CLOs, by type |

|---|---|---|

(Q3 2023, percentages) | (Jan. 2014-Mar. 2024; left-hand scale: € trillions, right-hand scale: percentages) | (Jan. 2011-Mar. 2024, percentages) |

|  |  |

Sources: PitchBook Data, Inc., ECB (investment fund list, SHS, CSDB) and ECB calculations.

Notes: EA stands for euro area; CLO stands for collateralised loan obligation; BSL stands for broadly syndicated loan; PC stands for private credit. Panel a: the sample of funds is calculated based on euro area private credit funds identified by PitchBook as well as funds with “private credit”, “middle market”, “direct lending” and “loan origination” in their name as shown in the ECB’s list of investment funds. The chart excludes approximately 5% of funds that do not report whether they are closed- or open-ended. Panel b: the euro area holdings of CLOs are identified by matching CLO issuer names from PitchBook to SHS data. The two lines show the total euro area sectoral CLO holdings as a share of total CLO amount outstanding, by type. Panel c: the bars depict the tranches’ aggregate shares of the total historical issuance of US BSL and private credit CLOs between January 2011 and March 2024. The dots represent the average share of senior secured loans within each CLO portfolio, weighted by the respective CLO size for the total BSL and private credit US CLO historical issuance.

Private credit CLOs are on the rise, although so far solely in the US market and with little exposure to euro area holders. Private credit CLOs – securities that are backed by a pool of private loans and divided into tranches with varying credit quality – have been growing rapidly in recent years. At the beginning of 2024, they accounted for 11% of all outstanding US CLOs (Chart C.4, panel b). While this segment is so far only present in the US market and exposures of euro area holders are negligible, some market observers expect a pick-up in Europe in the course of 2024.[22] Private credit CLOs typically have a larger equity tranche and a slightly smaller AAA tranche than traditional, or broadly syndicated loan, CLOs (Chart C.4, panel c), which may signal higher credit risk.[23] Moreover, unlike in traditional CLOs, private credit CLO issuers often retain the entirety of the equity tranche, which along with the tranche’s larger size, increases exposures to future potential losses. However, private credit CLOs typically have a slightly higher share of senior secured loans than their traditional peers,[24] as well as a significantly lower share of covenant-lite loans.[25] A covenant-heavy portfolio could nonetheless also increase the effective credit risk under some circumstances, as more stringent conditions applied to loans included in the CLO might increase the probability of default. In light of these considerations, it would be important to also monitor the resilience of a future private credit CLO market in Europe, were this to emerge.

Private markets still need to prove their resilience in an environment of higher interest rates as they have grown to a significant size only in the past decade. Higher interest rates might affect private markets through two channels. First, higher discount rates reduce the fundamental value of assets (affecting all private funds) and increase default risk in private credit portfolios, especially when interplaying with slowing growth. Losses might remain hidden until maturity or the exit from the investment due to the lack of marking to market. Second, it remains to be seen to what extent higher returns on safe assets will slow investor demand for alternative assets. The relatively high level of dry powder in private funds is a mitigating factor.

While financial stability risks from private markets seem contained in the euro area, some concerns remain. Aggregated exposures, opaqueness and private markets’ resilience are all elements that warrant monitoring, especially in an environment of higher interest rates. Given the limited liquidity mismatches of private funds in aggregate, and the long-term investment horizons of their main investors, risks to euro area financial stability from private markets appear limited. Still, it is conceivable that while the aggregate picture seems benign, risks may lurk in concentrated exposures. It is important to continue monitoring developments in private markets, including newer trends like the increase in private credit CLOs and NAV lending, and potential challenges from higher interest rates. However, monitoring remains hampered by opaqueness and data scarcity. This makes it all the more important to improve transparency concerning private markets.

Private credit may offer advantages over bank debt, such as higher leverage, a more flexible covenant structure and greater certainty and speed of execution; see Block, J., Jang, Y.S., Kaplan, S.N. and Schulze, A., “A Survey of Private Debt Funds”, Working Paper Series, No 30868, National Bureau of Economic Research, 2023.

Financial stability considerations from the global private credit market have been discussed recently. See, for example, “Chapter 2: The Rise and Risks of Private Credit”, Global Financial Stability Report, International Monetary Fund, April 2024.

In some jurisdictions, private market products are also increasingly offered to high-net-worth and retail clients; see “Case study on private finance and non-bank financial intermediation”, Global Monitoring Report on Non-Bank Financial Intermediation 2023, Financial Stability Board, December 2023, pp. 63-71.

A private fund’s legal documentation specifies the timing and frequency of capital calls. A private fund manager commonly has the discretion to make capital calls based on an assessment of investment opportunities and capital requirements. Investors are expected to respect their capital commitments when the fund manager makes a capital call. While relatively rare, an investor default carries very serious implications, such as reduced ownership stakes or removal from the investment.

For a more detailed discussion on the characteristics of private markets, see “The rise of private markets”, BIS Quarterly Review, Bank for International Settlements, December 2021.

A strategic buyer is a buyer within the same industry as the portfolio company. A financial buyer is often another private equity firm.

There is no consensus on what types of credit exposures should be included in the definition of private credit. Some only consider direct lending while others take a wider view, including any asset-backed structures. In addition, the private credit market can also encompass bridge financing, special situations, direct lending, distressed debt, infrastructure debt, mezzanine, real estate debt and venture debt.

These are firms with revenues between USD 10 million and USD 1 billion; see Hancock, K., “What is middle market private equity”, PitchBook Data, Inc., March 2023. In this sense, private credit loans are distinct from leveraged loans or broadly syndicated loans, which are generally loans originated by a syndicate of banks to typically larger, highly indebted companies.

According to Block, J. et al., op.cit., 40% of surveyed European private debt funds are affiliated with private equity firms.

See Q4 2023 European Credit Markets Quarterly Wrap, PitchBook Data, Inc., January 2024.

Real estate funds are important actors in the euro area commercial real estate (CRE) market and are sometimes owned by private equity firms. Their growing market footprint makes them vulnerable to a CRE market downturn, especially in the case of open-ended funds with structural mismatches between asset liquidity and redemption terms. See the article entitled “The growing role of investment funds in euro area real estate markets: risks and policy considerations”, Macroprudential Bulletin, ECB, April 2023.

As of the third quarter of 2023, assets under management of euro area private market funds stand at €960 billion, or 6% of the euro area investment fund sector’s total assets (source: ECB IVF statistics).

While the European private credit segment in particular is somewhat concentrated in the United Kingdom, growth in private credit funds in the EU may be supported by the Alternative Investment Fund Managers Directive (AIFMD) II, which establishes common rules for loan-originating alternative investment funds.

See in particular the box entitled “Making euro area equity markets fit for green and digital innovation”, Financial Integration and Structure in the Euro Area, ECB, April 2022.

See Graph 3 in “The rise of private markets”, BIS Quarterly Review, Bank for International Settlements, December 2021.

Various reports point to a slowdown in exit activity attributable to less deal-making amid tighter financing conditions, which has led to a decrease in distributions to investors (see, for example, 2024 Allocator Outlook, PitchBook Data, Inc., December 2023). Some sources point at NAV loan proceeds being used mainly for distributions − a debatable practice − while others estimate this use at only 8% of proceeds; see Case study on private finance and non-bank financial intermediation”, Global Monitoring Report on Non-Bank Financial Intermediation 2023, Financial Stability Board, December 2023, and “Is NAV Lending Good or Bad for GPs and LPs?”, Crestline Investors, Inc., October 2023.

See “NAVigating Considerations and Controversies Around NAV Loans”, PitchBook Data, Inc., December 2023.

According to PitchBook, 16% of newly originated private credit loans to euro area borrowers in 2023 were attributed to debt refinancing, up from 0% in 2022. This implies that private credit funds might enable firms to refinance and extend loans.

For further details, see, for example, the box entitled “Financial stability implications of private equity”, Financial Stability Review, ECB, May 2020.

See “EU Alternative Investment Funds 2023”, ESMA Market Report, European Securities and Markets Authority, January 2024.

See, for example, Mounguia, M.-L. and Dubar, J., Private Debt – An Expected But Uncertain “Golden Moment”?, Ernst & Young, 8 January 2024.

See, for example, Rae, M., “2024 European CLO Outlook: Steady state, with private credit on horizon”, PitchBook Data, Inc., December 2023; Rae, M., “Middle market CLOs only a matter of time for Europe, managers say”, PitchBook Data, Inc., November 2023; Thiele, V., “Stop dreaming of private credit CLOs, the arb is enough of a nightmare”, GlobalCapital, October 2023; and Tipping, N., “Why Europe still awaits a private credit CLO”, Risk.net, April 2024

In CLOs, the equity tranche is at the bottom of the priority ladder and has the highest risk and potential for return. Equity investors are the last to receive payments and the first to absorb any losses from defaults in the loan pool. However, if the performance of the first lien loans is strong, equity tranches can realise significant returns after all other tranches have been paid. After the senior and mezzanine tranches have been satisfied, the cash flows from first lien loans flow to the equity tranche.

Senior secured loans, or first lien loans, are secured by the borrower’s assets and by a first-priority claim on the collateral of the borrower. This means that in the event of liquidation, the proceeds from the sale of the collateral must first be used to repay these loans before subordinate loans.

According to PitchBook and ECB calculations, the average share of covenant-lite loans, defined as loans which have fewer or less stringent covenants than traditional loans, within US traditional CLOs weighted on their total historical issuance decreased from 70% to 60% between 2019 and 2023. At the same time, the share for US private credit CLOs increased from 10% to 20%.