The long-term effects of the pandemic: insights from a survey of leading companies

Published as part of the ECB Economic Bulletin, Issue 8/2020.

This box summarises the findings of an ad hoc ECB survey of leading euro area companies that looks at the long-term effects of the coronavirus (COVID-19) pandemic on the economy. While precipitating the largest short-term decline in economic activity for centuries, the COVID-19 pandemic has also brought about changes in the way businesses operate and consumers behave, some of which are likely to outlive the present crisis. These may in turn influence aggregates such as output, employment and prices – and the relationship between them – in the long term.[1]

The main aim of the survey was to find out how leading euro area firms perceive the long-term impact of the COVID-19 pandemic on their business. For the purpose of the survey, we defined long term as “a new normal when, owing – for example – to the development of a vaccine and/or more effective treatment, the economy will no longer be subject to significant disruption and/or abrupt change due to the virus or the measures needed to contain it”. The survey was split into three parts. The first part asked what long-term effects, if any, the COVID-19 pandemic was expected to have on the respondents’ business, e.g. in terms of business organisation or the markets they operate in. The second part asked respondents to indicate whether they agreed or disagreed with a set of statements on narratives for the pandemic-induced “new normal”. The third part asked about the expected long-term impact on aggregates such as sales, employment and prices. Responses were received from 72 leading non-financial companies, split around 60% to 40% between “industrials” and “services”. When interpreting the results, it should be borne in mind that the size and distribution of the activities of these firms most likely makes them better able to respond to the challenges posed by the pandemic than other firms.

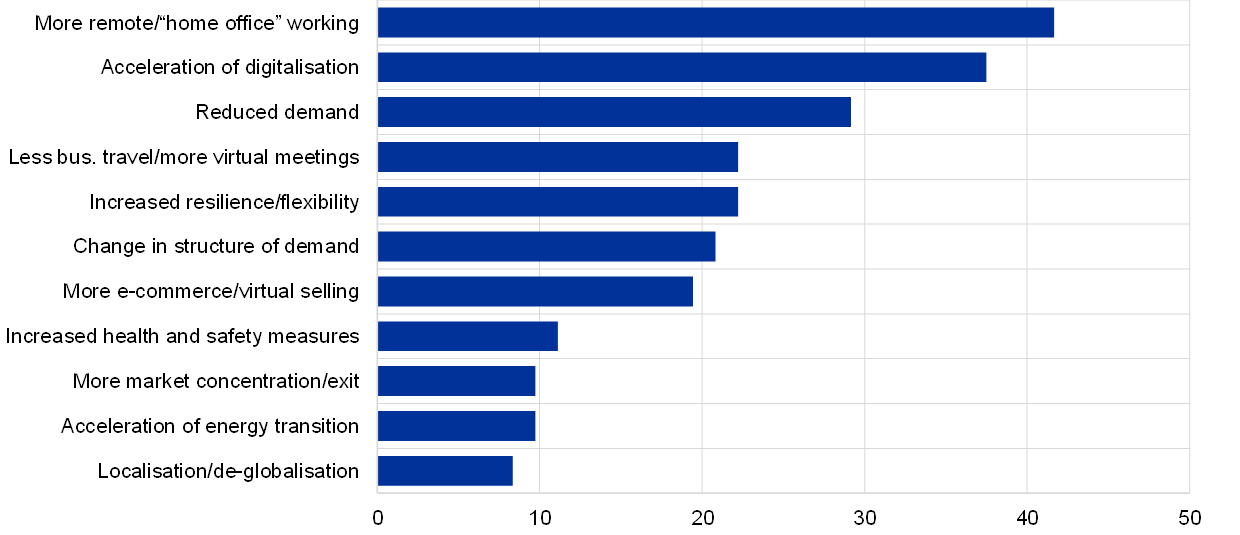

More remote working and an acceleration of digitalisation were the most frequently cited long-term supply-side effects of the pandemic. Respondents were asked to briefly explain, in order of importance, up to three ways in which the pandemic would have a long-term impact on their business, for example in relation to business organisation or the markets they operate in. Chart A summarises the responses received to this open question. More than 40% of respondents cited increased use of the “home office”, while almost as many said that the pandemic had led their company to accelerate the adoption of digital technologies, which will change the way they operate in the long term. Around one-fifth of respondents cited a more permanent reduction in business travel and/or increase in virtual meetings, and a similar number pointed to increased e-commerce or – in business-to-business segments – “virtual selling”. Around one-fifth highlighted the fact that actions taken in response to the pandemic would make their business more resilient and/or more flexible in the long term.

A significant share of respondents cited reduced demand and/or changes in the structure of demand as particular concerns. Almost 30% cited reduced demand for their products or services as one of the main long-term consequences of the pandemic for their business, while more than 20% pointed to lasting changes in the structure of demand. To a large extent, this seems to reflect a view that some changes in living and working habits brought about by the pandemic, especially the increased conduct of business and consumption online and a consequent reduction in travel, will become embedded.

Chart A

Main long-term effects of the pandemic reported by leading companies

(percentage of respondents)

Notes: The survey question put to respondents was as follows – “What long-term effects, if any, do you expect the COVID-19 pandemic to have on your business (for example, in terms of business organisation or the markets you operate in)? Please list up to three impacts in order of importance.” The replies were subsequently grouped by category.

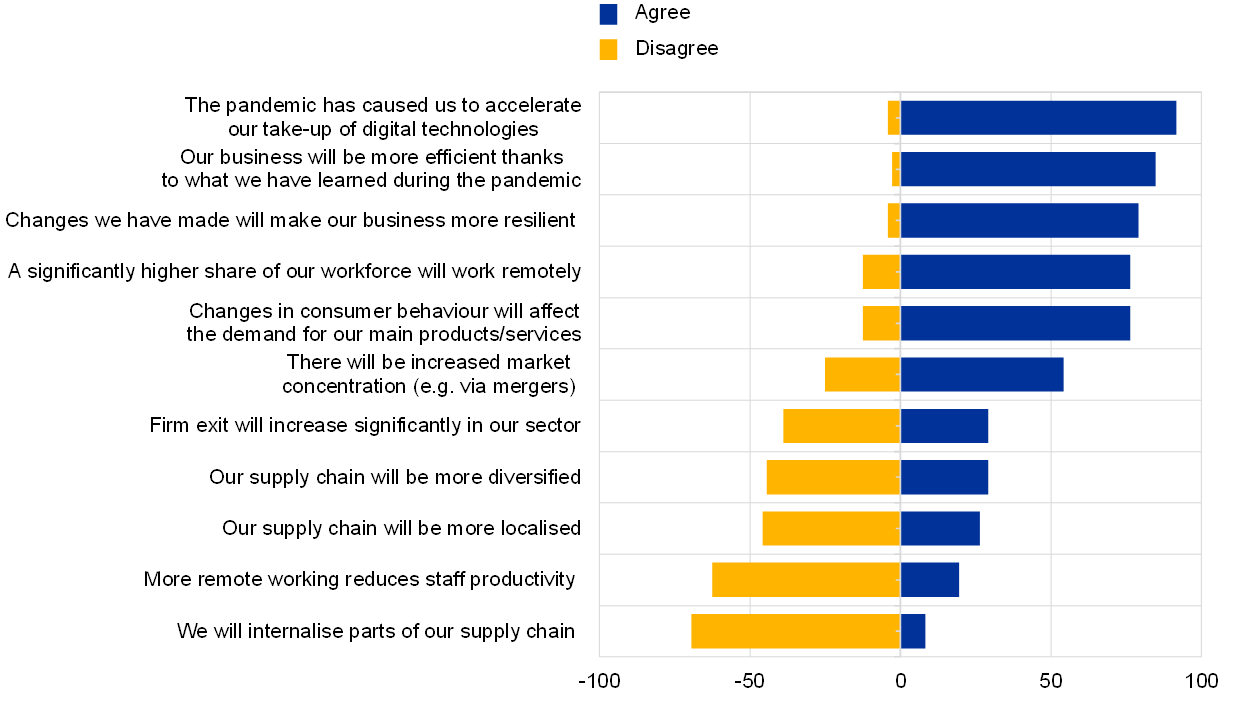

More than three-quarters of respondents agreed that their business would be more efficient and more resilient following the pandemic. Chart B summarises what respondents replied when they were asked to agree or disagree with a set of statements intended to test certain narratives about the pandemic-induced “new normal”. More than 75% agreed that what had been learned during the pandemic would make their business more efficient and that changes made would make their business more resilient. Nine out of ten confirmed that they had accelerated their take-up of digital technologies and/or automation, while more than three-quarters agreed that a significantly higher share of their workforce would continue to work remotely. Around 60% disagreed when asked if more remote working reduced productivity, compared with just 20% who agreed with the statement. In this regard, while reduced informal, personal interaction was seen as a downside, many advantages were also perceived, including the reduction in lost time due to commuting, the possibility to better juggle home and work commitments, and increased connectivity.[2]

Chart B

Testing narratives in relation to the long-term effects of the pandemic

(percentage of respondents)

Notes: The survey question put to respondents was as follows – “Please indicate whether you agree or disagree with the following statements in relation to the long-term effects of the COVID-19 pandemic.” Respondents could answer (i) agree, (ii) disagree or (iii) not sure or not relevant. In the chart, “agree” is assigned a score of 1 and “disagree” a score of -1.

The pandemic was seen as changing consumer behaviour in the long term and likely leading to increased market concentration, while having much less impact on supply chains. Three-quarters of respondents agreed that changes in consumer behaviour as a result of the pandemic would affect demand for their main product or service in the long term. More than half thought that there would be increased market concentration in their sector (compared with one-quarter who disagreed with this statement), with mergers expected to play a greater role than firms exiting the market. When asked about the long-term effect of the pandemic on supply chains, among those firms for whom these questions were relevant, a majority disagreed that their supply chain would become more diversified or localised; an overwhelming majority did not see their business seeking to internalise more parts of the supply chain.

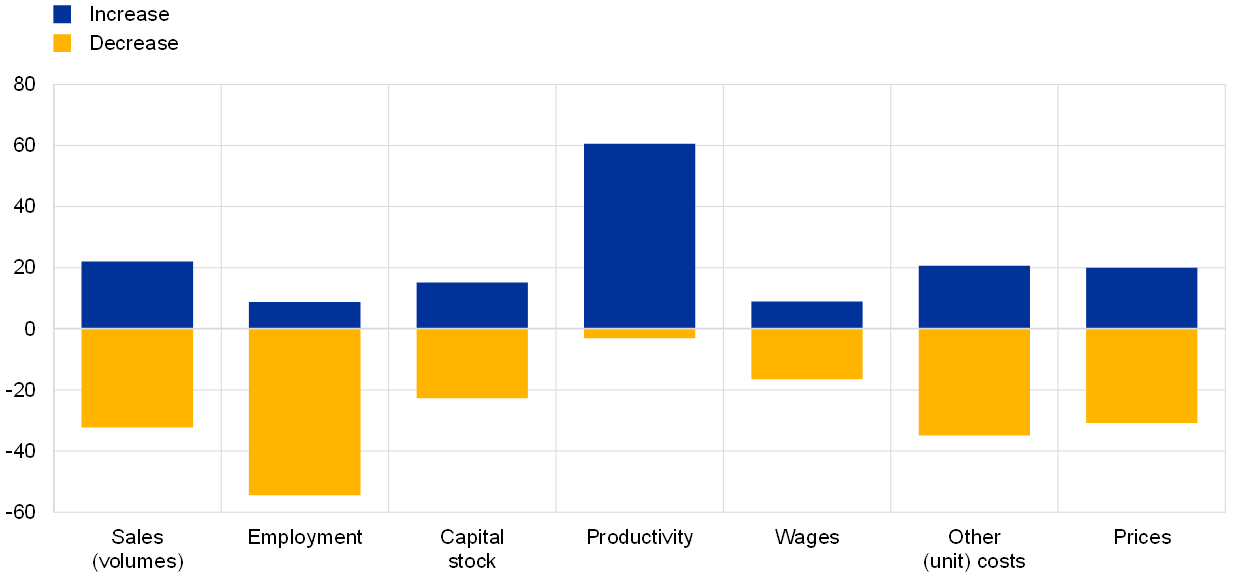

Most respondents considered that the pandemic would have a positive long-term impact on productivity but a negative impact on employment. When asked to assess the overall long-term effect on selected aggregates, 60% said that productivity in their business or sector would increase, while hardly any saw productivity decreasing as a long-term consequence of the pandemic. Conversely, 55% anticipated a negative long-term impact on employment, compared with around 10% who saw a positive effect. This would seem to reflect how businesses have learned to maintain production in spite of restrictions on labour inputs due to social distancing and the identification of related efficiency gains. Meanwhile, relatively few saw the pandemic having any long-term effect on their company’s capital stock. The anticipated long-term effect of the pandemic on sales (volumes), prices and costs was slightly negative on balance, but most respondents indicated that they did not anticipate – or were unsure about – any long-term effects.

Chart C

How respondents saw the long-term effect of the pandemic on business aggregates

(percentage of respondents)

Notes: The survey question put to respondents was as follows – “Focusing on your own business/sector, how would you assess the overall long-term effects of the COVID-19 pandemic on the following?” Respondents could answer (i) increase, (ii) decrease, (iii) no change or (iv) don’t know. In the chart, “increase” is assigned a score of 1 and “decrease” a score of -1.

- For a recent study of the long-term effects of past pandemics and how these compare to wars, see Jordà, Ò., Singh, S.R. and Taylor, A.M., “The Longer-Run Economic Consequences of Pandemics”, Federal Reserve Bank of San Francisco, Working Paper Series, No 9, 2020.

- It was noted, for example, that as a result of remote working, staff were now nearly always accessible, whereas in the past this was not the case owing to commuting or business trips. It was also noted how some functions, such as sales, had become much more productive when conducted virtually.