US yield curve inversion and financial market signals of recession

Published as part of the ECB Economic Bulletin, Issue 1/2020.

The inversion of the US yield curve in mid-2019 led to heightened concerns about a possible US recession. The US yield curve is often seen as a predictor of recessions: a flattening or inversion of the yield curve (or negative term spread), in which interest rates at the long end are below those at the short end, has often been understood as a signal of an impending recession. In late summer 2019 the US yield curve inverted for the first time since the global financial crisis (see Chart A). Global recession analyses may help assess risks to the economic outlook. This box presents an assessment of the probability of a recession in the United States, taking into account developments that have distorted the signals derived from the current yield curve.

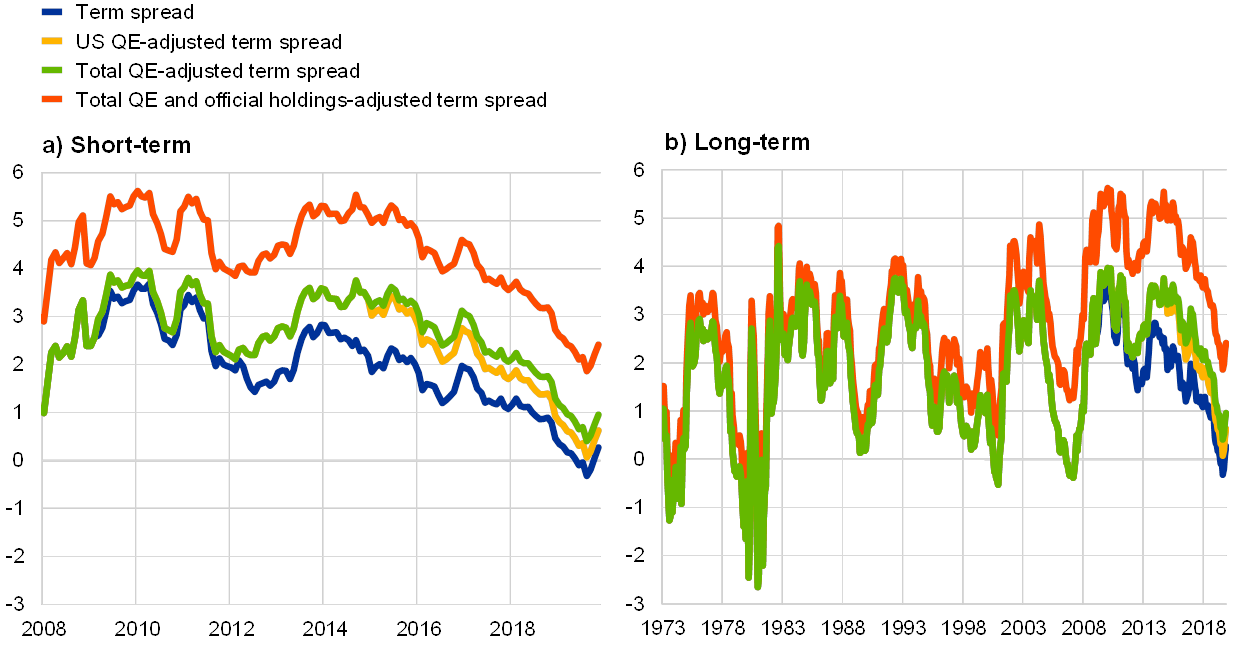

Chart A

Adjusting the term spread: short and long-term perspectives

(percentage points)

Sources: Federal Reserve System, Haver Analytics and ECB calculations.

Notes: The term spread is the spread between the three-month and ten-year US Treasury yields. The US QE-adjusted term spread is the spread adjusted for the effect of Federal Reserve QE on the ten-year yield. The total QE-adjusted term spread accounts for the effect of Federal Reserve and Eurosystem asset purchases on ten-year US Treasury yields. The total QE and official holdings-adjusted spread accounts for the effect of official holdings on the ten-year yield in addition to the effect of US and euro area QE.

The latest observation is for November 2019.

Standard yield curve-based recession probability models ignore factors that can distort the signals derived from the current yield curve.[1] Yield curve-based recession models typically relate the probability of recession to a measure of the term spread – i.e. the difference between three-month and ten-year US Treasury yields. However, the term spread can be affected by factors that have depressed the term premium in longer-term bond yields largely independently of the domestic economic outlook. First, since the global financial crisis, US long-term yields have been compressed by asset purchases by the Federal Reserve System. Although the Federal Reserve ceased purchases some time ago and, until the summer of 2019, was in the process of reducing its holdings of bonds, the stock of bonds currently held on its balance sheet has continued to depress term premia on longer-term bonds. Second, in the last few years US long-term yields have been further compressed by the asset purchase programmes of foreign central banks, such as the ECB. Foreign central banks’ asset purchases affect US yields through the international portfolio rebalancing channel of monetary policy. Third, since the early 2000s the accumulation of US Treasury holdings by foreign central banks has also compressed longer-term Treasury yields. As demand from foreign central banks is typically price-inelastic, long-term yield compression is likely to occur independently of recession risks in the US economy. As a consequence, the signals from standard recession probability models based on the yield curve may be distorted.

This box presents alternative recession probability models to deal with these possible distortions to the signals from the yield curve. Specifically, term spread measures are constructed to adjust for the effects of asset purchase programmes and foreign central bank reserve accumulation. These measures are then included in a standard logit regression model to assess the probability that a US recession will occur over a one-year horizon.[2] A logit model is used to estimate the probability of a binary event – in this case the US economy being in recession – based on a number of explanatory variables. The following term spread variants are used to estimate the probability of recession:

First, a term spread measure that corrects the US ten-year yield for the effect of the Federal Reserve’s quantitative easing (QE) programmes is constructed. To do so, the impact of the three large-scale asset purchase (LSAP) programmes, the maturity extension programme and reinvestments on the US term premium for ten-year government bond yields is assessed.[3] Adjusting the ten-year yield for the effects of QE leads to a markedly larger difference between the three-month and ten-year US Treasury yield (i.e. a wider term spread), in particular between 2012 and 2018 (see Chart A, yellow line). The adjusted term spread increases with the gradual expansion of the Federal Reserve balance sheet and peaks (at 124 basis points) in September 2014, just before the end of net asset purchases. The difference between the standard term spread and the US QE-adjusted term spread narrowed during the Federal Reserve’s balance sheet normalisation between October 2017 and August 2019, but it still remains significant.

Second, a term spread measure is derived to account for spillover effects on US yields of asset purchases by Eurosystem central banks (see Chart A, red line). To do so, the correlation coefficient of the day-on-day change in German Bund yields and US Treasury yields at ten-year maturity following ECB asset purchase programme (APP) announcements is calculated.[4] The total effect of the ECB’s quantitative easing on US yields is then calculated by applying the correlation coefficient to the estimated effect of the Eurosystem’s APP on the ten-year euro area term premium.[5][6] Finally, the US term spread is corrected for these spillovers from APP announcements by adding the estimates to the US ten-year yield.

Third, a term spread measure that also takes into account the effect of foreign official reserve holdings of US Treasury bonds is constructed (see Chart A, green line). ECB estimates suggest that an increase in foreign official holdings by 10 percentage points of the outstanding stock of US government debt leads to a 55 basis point fall in the term premium on US Treasuries.[7] Given observations of the amount of foreign official US dollar holdings as a share of total outstanding US government debt, it is possible to adjust the ten-year yield for these effects. The official holdings-adjusted term spread starts deviating noticeably from the standard term spread in the early 2000s, when China and other emerging market economies started to increasingly accumulate US dollar reserves (see Chart A). Since 2008 the term spread accounting for the effect of official holdings has on average been about 165 basis points higher than the QE-adjusted term spread.

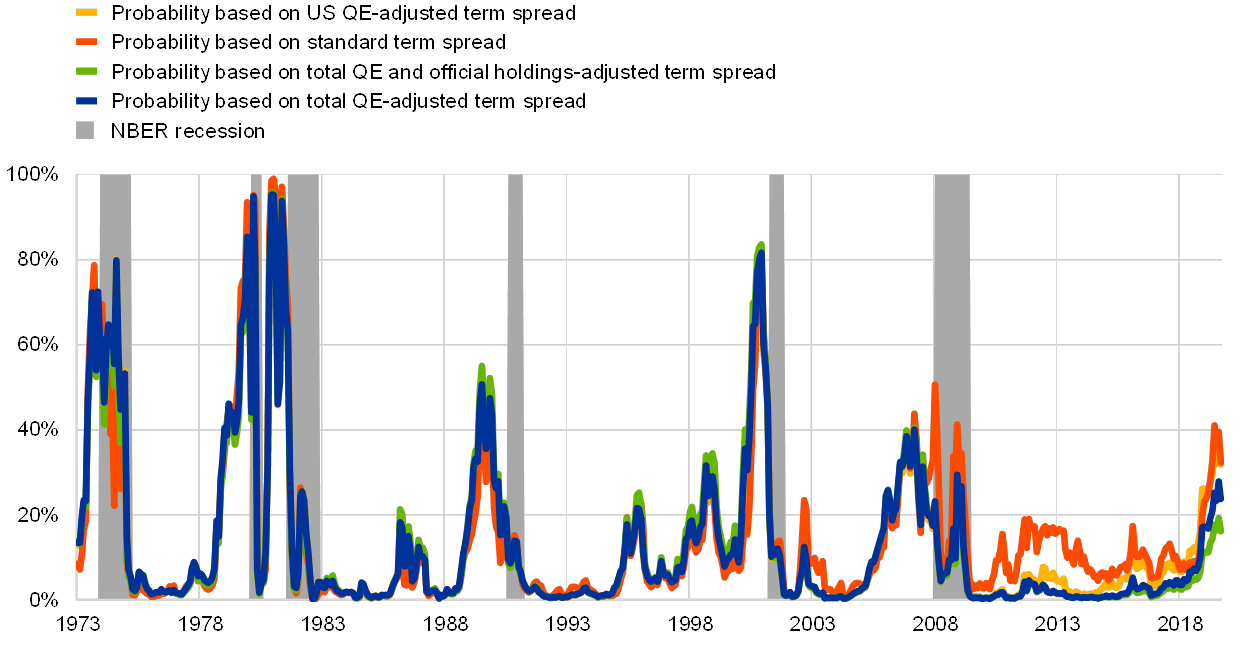

A model based on the standard term spread may potentially overstate current recession probabilities compared to models that account for the effect of asset purchases. As shown in Chart B, in August 2019, at the point of the greatest yield curve inversion, the predicted one-year-ahead recession probability based on a model using the standard term spread was 37%. In contrast, the term spread adjustments proposed here point to markedly lower probabilities. The model that uses a term spread adjusted for US QE points to a probability of 28%.[8] Once the spillover effects of the APP on the US term spread is also adjusted for, the probability falls to 21%. Further adjustment for the effects of foreign official holdings on the term spread reduces the probability to just 12%.[9]

Chart B

Recession probabilities based on term spread variants

(percentages)

Sources: Federal Reserve System, Haver Analytics and ECB calculations.

Notes: Shaded areas denote National Bureau of Economic Research (NBER) recessions. The term spread variants are explained in the notes to Chart A.

Overall, models that account for the fact that the term premium in longer-term bond yields, and thus the term spread, can be depressed by factors that are largely independent of the domestic economic outlook suggest a lower probability of a US recession than models based on the standard term spread. In August 2019, when model-based recession probabilities peaked, the correction indicates a 9 to 25 basis points lower probability of a recession one year ahead compared to the standard model. The model that accounts for US and euro area QE, which is found to be best performing in terms of statistical properties, implied a recession probability of 28%. Since August 2019 recession probabilities have declined across all models in line with a widening term spread, driven in particular by an increase in long-term government bond yields. This suggests a somewhat more benign outlook for the United States than suggested by market commentary in the summer of 2019.

- A similar point was also made in Lane, P.R., “The yield curve and monetary policy”, Public Lecture for the Centre for Finance and the Department of Economics at University College London, 25 November 2019.

- The models control for corporate bond and stock market misalignments by including the excess bond premium and the cyclically adjusted price/earnings ratio.

- Estimates of the impact on the US term premium are based on Ihrig, J., Klee, E., Li, C, Wei, M. and Kachovec, J., “Expectations about the Federal Reserve’s Balance Sheet and the Term Structure of Interest Rates”, International Journal of Central Banking, Vol. 14(2), March 2018, pp. 341-391.

- The coefficient is 0.4, suggesting that an ECB APP announcement that lowers ten-year German Bund yields by 10 basis points leads to a decline of 4 basis points in US Treasury yields with the same maturity. ECB APP announcements are based on Dedola, L., Georgiadis, G., Gräb, J. and Mehl, A., “Does a big bazooka matter? Central bank balance-sheet policies and exchange rates”, Working Paper Series, No 2197, ECB, November 2018.

- Estimates are taken from Eser, F., Lemke, W., Nyholm, K., Radde, S. and Vladu, A.L., “Tracing the impact of the ECB’s asset purchase programme on the yield curve”, Working Paper Series, No 2293, ECB, July 2019.

- This is consistent with Curcuru et al. (2018) who find that ECB policy easing substantially depresses US term premia. See Curcuru, S., Kamin, S. Li, C. and Rodriguez, M., “International Spillovers of Monetary Policy: Conventional Policy vs. Quantitative Easing”, International Finance Discussion Papers, No 1234, Board of Governors of the Federal Reserve System, August 2018.

- Estimates are based on Gräb, J., Kostka, T. and Quint, D., “Quantifying the ‘exorbitant privilege’ – potential benefits from a stronger international role of the euro”, in The international role of the euro, ECB, June 2019.

- Using standard metrics to assess the ability to forecast recessions, it can be shown that, among the models tested, the model with the total QE-adjusted term spread has the highest predictive ability.

- Swanson and Williams (2014) show that, in particular, rates at shorter horizons were unresponsive to macroeconomic news during this period. Consequently, in all models, the period when the target range for the federal funds rate was at 0% to 0.25% is excluded from the estimation. See Swanson, E.T and Williams, J.C., “Measuring the Effect of the Zero Lower Bound on Medium- and Longer-Term Interest Rates”, NBER Working Paper, No 20486, September 2014.