Household income risk over the business cycle

Published as part of the ECB Economic Bulletin, Issue 6/2019.

Household income and wealth inequality have become more important in explaining the macroeconomy. Since the financial crisis, there has been increased awareness that heterogeneity across households and firms is key to understanding business cycle fluctuations (e.g. via balance sheets, credit constraints).[1] At the same time, public interest in the distributional aspects of economic policies has continued to grow. In addition, the increased availability of microdata makes it possible to document relevant microeconomic stylised facts. In this vein, this box sheds light on the relationship between business cycle fluctuations and income changes at the level of individual workers in the euro area.

Evidence suggests that household income risk varies over the business cycle and affects workers unequally. Individual earnings risk may be considered the most direct type of household income risk, before any insurance from social transfers or intra-household resource pooling. Based on this, Guvenen et al. document the variation in individual earnings risk using a large administrative micro dataset for the United States.[2] They find that the skewness of income changes is strongly procyclical: large upward earnings movements are less likely during recessions, whereas large drops in earnings are more likely. In addition, they find that aggregate shocks do not affect workers with different characteristics in the same way: the income of some workers (e.g. young, lower-wage earners) is systematically more sensitive to the business cycle than that of others. This is quite different from purely random income shocks that are mostly used when modelling household income risk.

Household income risk is important for the propagation of macroeconomic shocks and the transmission of economic policies. Several authors find that the dynamics of household income risk give rise to a cyclical precautionary savings motive that substantially raises the sensitivity of consumption to fluctuations in aggregate income.[3] Evidence also shows that the marginal propensity to consume out of disposable income (MPC) is greater in households with higher income risk, which makes aggregate consumption even more sensitive to the business cycle.[4] To the extent that incomes of households with a high MPC benefit more from macroeconomic stabilisation policies, the distribution of household income risk also amplifies the effects of fiscal and monetary policies.[5]

Variation in income risk in the euro area can be studied using survey data on income. Due to limited data availability until recently, there has so far been no systematic analysis of trends in individual earnings risk in the euro area, both over time and across individuals. To address this, the box uses the longitudinal data on individual income levels observed over a four-year period as provided by the European Union Statistics on Income and Living Conditions (EU-SILC). The analysis focuses on the four largest euro area countries. This facilitates a better understanding of microeconomic stylised facts across the euro area, while exploiting national differences in terms of economic structures and recent macroeconomic developments.[6]

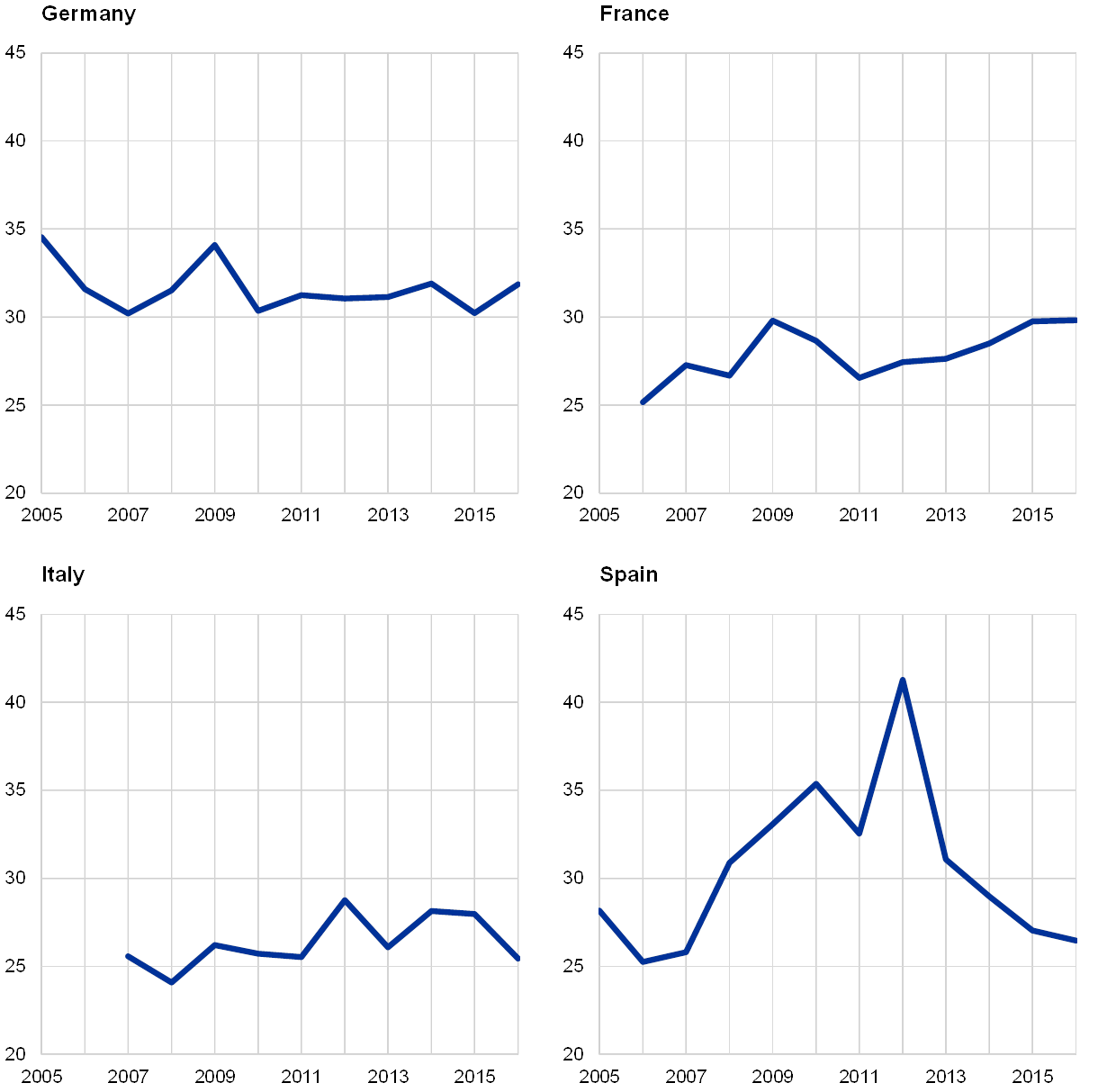

Chart A

Downward labour income risk

(percentage share of individuals experiencing a decline in labour income)

Sources: Eurostat, DIW Berlin and ECB calculations.

Note: Share of individuals aged 25-65 experiencing a decline in their labour income (based on the EU-SILC variable PY010G for gross employee cash income in the longitudinal data files; the EU-SILC longitudinal data file clone of the GSOEP is used for Germany).

Downward income risk is procyclical in the euro area, but varies significantly across countries. Chart A shows the variation in the proportion of workers experiencing a fall in labour income compared to the previous year (i.e. realised income risk).[7] As the number of workers becoming unemployed increases during recessions, the proportion of workers seeing a fall in income rises during recessions and vice versa. This is clearly visible in 2008 and 2009 during the financial crisis, but even more so in Spain in 2011 and 2012 during the sovereign debt crisis. In Spain, the higher variability of unemployment is also reflected in a higher variability of the share of workers experiencing a decline in labour income. This is much less common in Germany, France and Italy, where labour markets are known to be less fluid.

Chart B

Labour income path following a large reduction in income

(income normalised to 1 in the first year)

Sources: Eurostat, DIW Berlin and ECB calculations.

Note: Trends in the normalised labour income of men aged 26-50 experiencing a large reduction in income (defined as a drop in income of more than 15%) in 2007 or 2013 (income based on the EU-SILC variable PY010G for gross employee cash income in the longitudinal data files; the EU-SILC longitudinal data file clone of the GSOEP is used for Germany).

Downward income risk is persistent, implying a large impact on lifetime incomes. Chart B shows how following a large drop in an individual’s labour income, income also tends to be significantly lower during the two following years. This suggests that realised downward income risk is persistent, implying that job losses may significantly affect individual lifetime labour income, and thus also consumer spending.[8] In addition, the persistence also seems to depend on the state of the business cycle: drops in income since 2013, the start of the current economic expansion, seem to be less persistent than those seen at the start of the financial crisis. While there are significant differences from country to country in the variation of the proportion of workers seeing a drop in labour income, the degree of persistence seems quite comparable.

Chart C

Worker betas across the income distribution

(income elasticity in relation to GDP growth)

Sources: Eurostat, DIW Berlin and ECB calculations.

Note: Estimated elasticity of labour income to aggregate GDP growth across the household income distribution (individuals are sorted into income quintiles based on the household income in the two previous years to avoid any spurious correlation between exposure and sorting; household income is based on EU-SILC variable HY020 total disposable household income in the longitudinal data file; the EU-SILC longitudinal data file clone from the GSOEP is used for Germany). Grey areas represent 95% confidence bounds.

Income risk in the euro area differs across individual households. Chart C reports “worker betas”, as documented in Guvenen et al. for the United States.[9] Worker betas measure the elasticity of labour income in relation to changes in aggregate GDP growth. Across the income distribution, the sensitivity of labour income to changes in GDP growth is significantly higher for workers in lower-income households. This pattern is particularly visible in Germany, France and Italy. In Spain, the sensitivity of labour income within lower-income households to GDP growth is comparable to that of workers in other countries, but it does not decrease as much when households earn higher incomes. This may reflect the generally higher variability in unemployment in Spain, affecting workers across the income distribution more equally.[10] However, identifying a structural explanation for this finding is beyond the scope of this box.

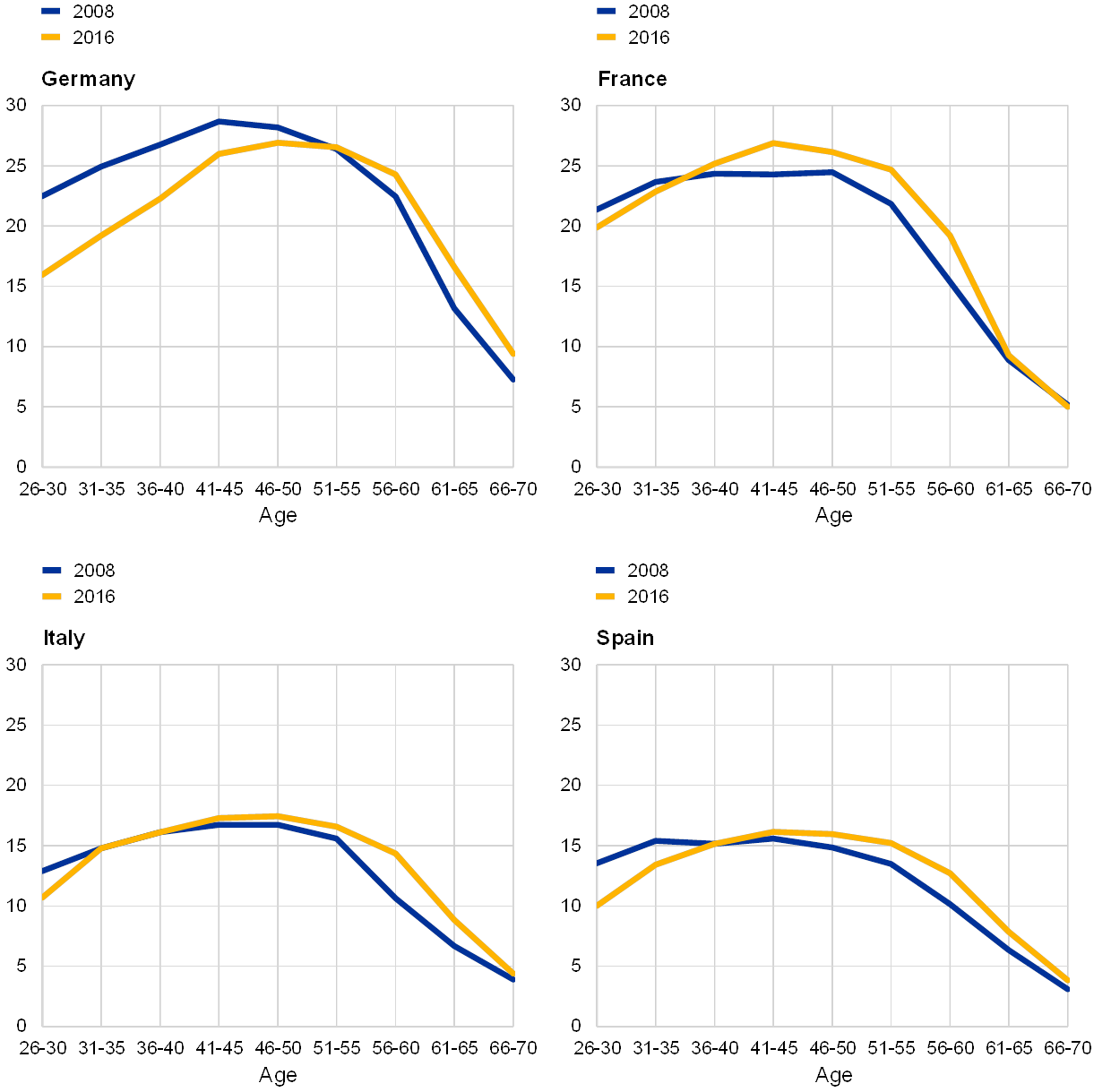

Chart D

Labour income across the age distribution

(EUR thousands per year)

Sources: Eurostat, DIW Berlin and ECB calculations.

Note: Estimated labour income of individuals aged 26-70 (in five-year age groups) in 2015 constant euro (based on the EU-SILC variable PY010G for gross employee cash income in the longitudinal data files; the EU-SILC longitudinal data file clone of the GSOEP is used for Germany).

The distribution of income risk also demonstrates who primarily bears the cost of business cycle fluctuations. There has been a long-standing debate within macroeconomics on the welfare cost of business cycles. Using a representative agent model, Lucas argued that the welfare cost of recessions is fairly small.[11] This implies that the case for using macroeconomic policies aimed at stabilising the business cycle would be quite weak. Research since Lucas has shown that understanding both the distribution of income and consumption losses and their persistence is key to assessing how harmful economic downturns are.[12] In this context, Chart D shows the distribution of real labour income across age groups in 2008 and 2016. It suggests that, since the financial crisis, the incomes of younger workers have not increased to the same extent as those of older workers. In Germany and Spain, the income of younger workers in real terms was even lower in 2016 than in 2008. Taking into account heterogeneity across individuals, the welfare costs of business cycles are therefore likely to be quite substantial in the euro area.

Household income risk behaves in a similar way in the euro area as in other economies, an insight which is useful for assessing the current economic outlook. All in all, the analysis suggests that, as in the United States, (i) individual earnings risk is strongly connected to the performance of the labour market, and (ii) in a downturn it increases much more for some groups of workers than for others. This is important for understanding how economic policy is transmitted and macroeconomic shocks are amplified. In the wake of the significant external shock that recently hit the euro area economy, the ongoing resilience in the labour market (cf. Section 3) may help to explain why household income risk has so far not amplified the macroeconomic impact of this shock.

- See Ahn, S., Kaplan, G., Moll, B., Winberry, T. and Wolf, C., “When Inequality Matters for Macro and Macro Matters for Inequality”, NBER Macroeconomics Annual 2017, Vol. 32, 2018.

- See Guvenen, F., Ozkan, S. and Song, J., “The Nature of Countercyclical Income Risk”, Journal of Political Economy, Vol. 122, No 3, June 2014, pp. 621-660.

- See McKay, A., “Time-varying idiosyncratic risk and aggregate consumption dynamics”, Journal of Monetary Economics, Vol. 88, June 2017, pp. 1-14; Bayer, C., Luetticke, R., Pham-Dao, L. and Tjaden, V., “Precautionary Savings, Illiquid Assets, and the Aggregate Consequences of Shocks to Household Income Risk”, Econometrica, Vol. 87, Issue 1, January 2019, pp. 255-290; Heathcote, J. and Perri, F., “Wealth and Volatility”, The Review of Economic Studies, Vol. 85, Issue 4, October 2018, pp. 2173-2213.

- See Jappelli, T. and Pistaferri, L., “Fiscal Policy and MPC Heterogeneity”, American Economic Journal: Macroeconomics, Vol. 6, No 4, October 2014, pp. 107-136; Auclert, A., “Monetary Policy and the Redistribution Channel”, American Economic Review, Vol. 109, No 6, June 2019, pp. 2333-2367.

- See Ampudia, M., Georgarakos, D., Slacalek, J., Tristani, O., Vermeulen, P. and Violante, G., “Monetary policy and household inequality”, Working Paper Series, No 2170, ECB, July 2018; Kaplan, G. and Violante, G., “A Model of the Consumption Response to Fiscal Stimulus Payments”, Econometrica, Vol. 82, No 4, July 2014, pp. 1199-1239.

- The longitudinal dimension of the EU-SILC data is not available for Germany. Given that the German EU-SILC data are based on the German Socio-Economic Panel (GSOEP), the analysis uses the newly developed EU-SILC clone provided with the GSOEP since version 34.

- The percentage share of individuals experiencing a decline in wage income captures a range of different phenomena: periods of unemployment, wage cuts and labour supply adjustments on both the intensive and the extensive margin. This indicator can therefore not be interpreted as a measure of wage rigidity.

- See Pissarides, C., “Loss of Skill During Unemployment and the Persistence of Employment Shocks”, The Quarterly Journal of Economics, Vol. 107, No 4, November 1992, pp. 1371-1391.

- See Guvenen, F., Schulhofer-Wohl, S., Song, J. and Yogo, M., “Worker Betas: Five Facts about Systematic Earnings Risk”, American Economic Review, Vol. 107, No 5, May 2017, pp. 398-403.

- There is evidence to suggest that the divergence in unemployment rates across euro area countries is related to the existence of different labour market institutions. See Boeri, T. and Jimeno, J., “Learning from the Great Divergence in unemployment in Europe during the crisis”, Labour Economics, Vol. 41, Issue C, 2016, pp. 32-46.

- Lucas, R., Models of business cycles, Basil Blackwell, Oxford, 1987.

- See Krebs, T., “Job Displacement Risk and the Cost of Business Cycles”, American Economic Review, Vol. 97, No 3, June 2007, pp. 664-686.