How does the current employment expansion in the euro area compare with historical patterns?

Published as part of the ECB Economic Bulletin, Issue 6/2019.

This box looks at the current employment expansion in the euro area and compares it with past periods of employment growth. Employment in the euro area has grown for almost six consecutive years, from its trough in the second quarter of 2013. Since the start of the current employment expansion, employment has increased by more than 11 million people and the unemployment rate has declined by more than 4 percentage points, with the latter approaching the levels reached before the crisis. Meanwhile, labour productivity growth and real wage growth have been relatively weak. Against this background, this box aims to identify similarities and differences between the current employment expansion and previous episodes of expansion. In particular, it takes a long-term perspective to analyse the relationship between employment growth and GDP growth, the behaviour of unemployment, and the relationship between productivity growth and real wage growth. The analysis relies on annual data from the European Commission AMECO database for the first 12 countries to join the euro area[1], for the period between 1960 and 2018. These data are then partitioned into ten separate periods of consecutive positive or negative employment growth.[2] These periods, which identify employment expansions and contractions, are a useful benchmark to assess the strength and maturity of the current employment expansion.

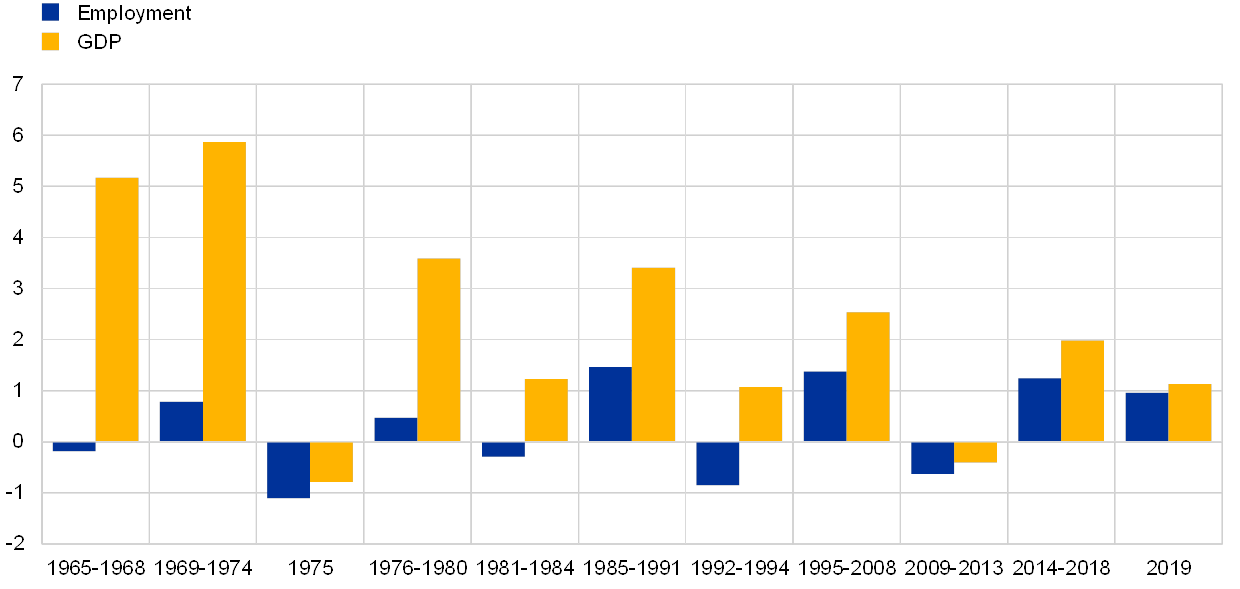

From a historical perspective, the current employment expansion has not been particularly lengthy so far, with average employment growth being marginally lower than that observed during the previous expansion. Chart A shows the average yearly employment and GDP growth for the 12 countries during the identified periods of employment expansion or contraction. The median employment expansion lasted around six years, with the 1995-2008 expansion being the longest period of consecutive employment growth over the time period analysed in this box. The median employment contraction lasted around two years. Against this backdrop, the current period of employment expansion is not particularly long. Looking at the rate of expansion, during the last three employment expansions, employment increased on average by 1.4% per year. In the current expansion, by contrast, employment rose at a rate of around 1.2% for each year between 2014 and 2018, with a lower rate being forecast for 2019.[3]

Chart A

Average annual employment growth and real GDP growth

(percentages, per year)

Sources: European Commission AMECO database and ECB staff calculations.

Note: 2019 is based on the European Commission spring forecast for the EA12 available in the AMECO database.

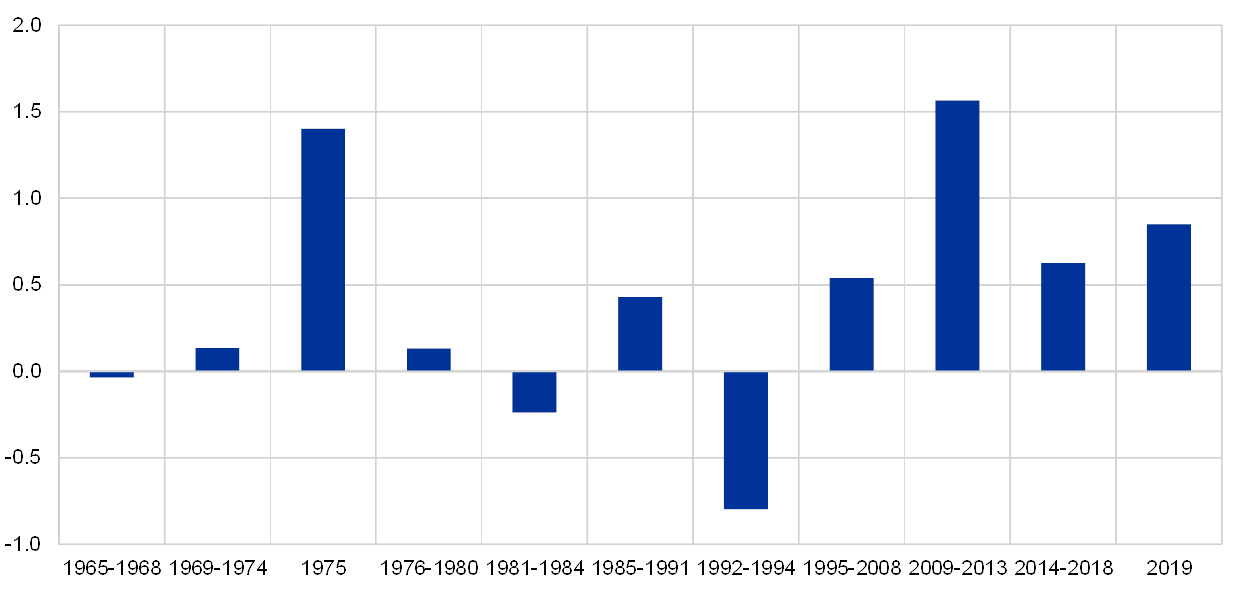

At the same time, the current expansion is more employment-rich than previous ones, when employment growth is assessed against real GDP growth.[4] Indeed, the average real GDP growth rate during the current employment expansion is the lowest observed for any of the employment expansions in the sample period, but employment growth decelerated by a smaller amount. Taking a longer-term perspective, the last three employment expansions (2014-18, 1995-2008 and 1985-91) were characterised by a significantly higher employment growth rate than the earlier expansion periods. This implies that the elasticity of employment growth (to GDP growth) strengthened during the last three employment expansions and has increased steadily over time between the expansion period 1985-91 and the current expansion (see Chart B).

Chart B

Elasticity of employment to real GDP

(percentages)

Sources: European Commission AMECO database and ECB staff calculations.

Notes: 2019 is based on the European Commission spring forecast for the EA12 available in the AMECO database. The elasticity is calculated as the ratio of cumulative employment growth to cumulative GDP growth in each period.

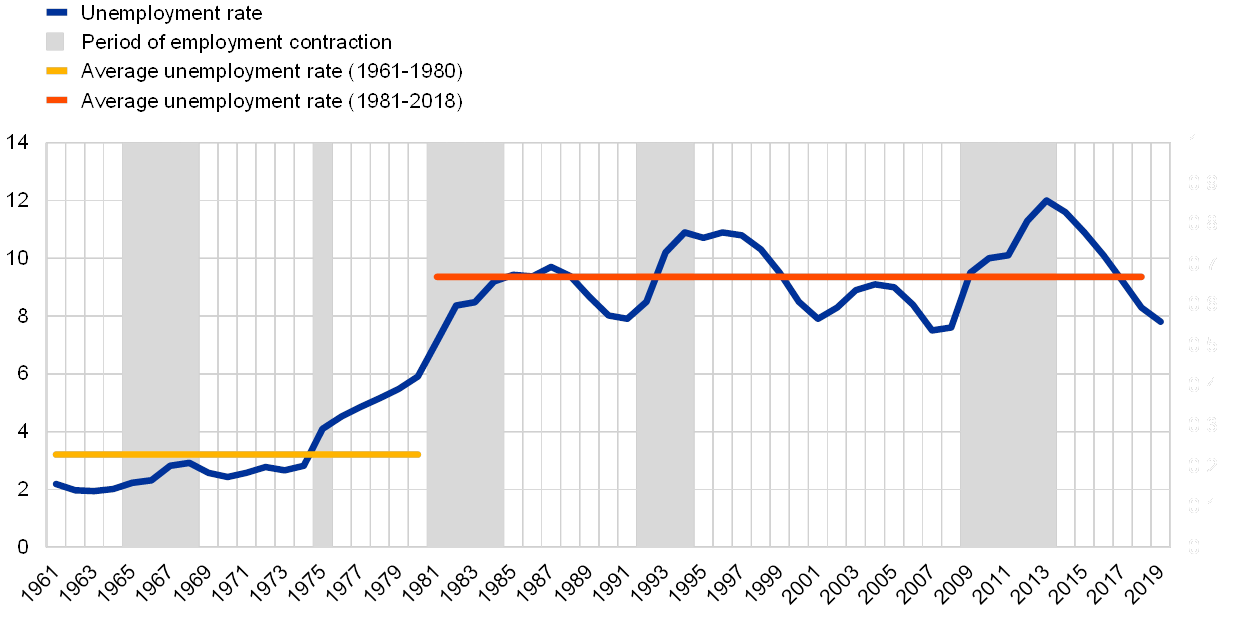

Additionally, the fall in the unemployment rate during the current expansion period has been particularly notable from a historical perspective. Over the period 2014-18 the unemployment rate declined by an average of 0.7 percentage points per year, which is the fastest rate of decline in any five-year period during the sample period (see Chart C). This fast-paced decline occurs against the backdrop of historically high levels for the unemployment rate. Taking a long-term view, a possible structural change in the unemployment rate in the group of 12 countries can be identified around the mid-1970s, when the unemployment rate moved to a substantially higher level.[5] Indeed, over the past three decades, the annual unemployment rate has rarely declined below 8%. If the unemployment rate continues to decline at the current rate, it will fall below its pre-crisis levels by 2020. However, it remains to be seen whether the unemployment rate in the euro area could decrease to levels closer to those observed before the 1980s.

Chart C

Unemployment rate

(percentages)

Sources: European Commission AMECO database and ECB staff calculations.

Note: 2019 is based on the European Commission spring forecast for the EA12 available in the AMECO database.

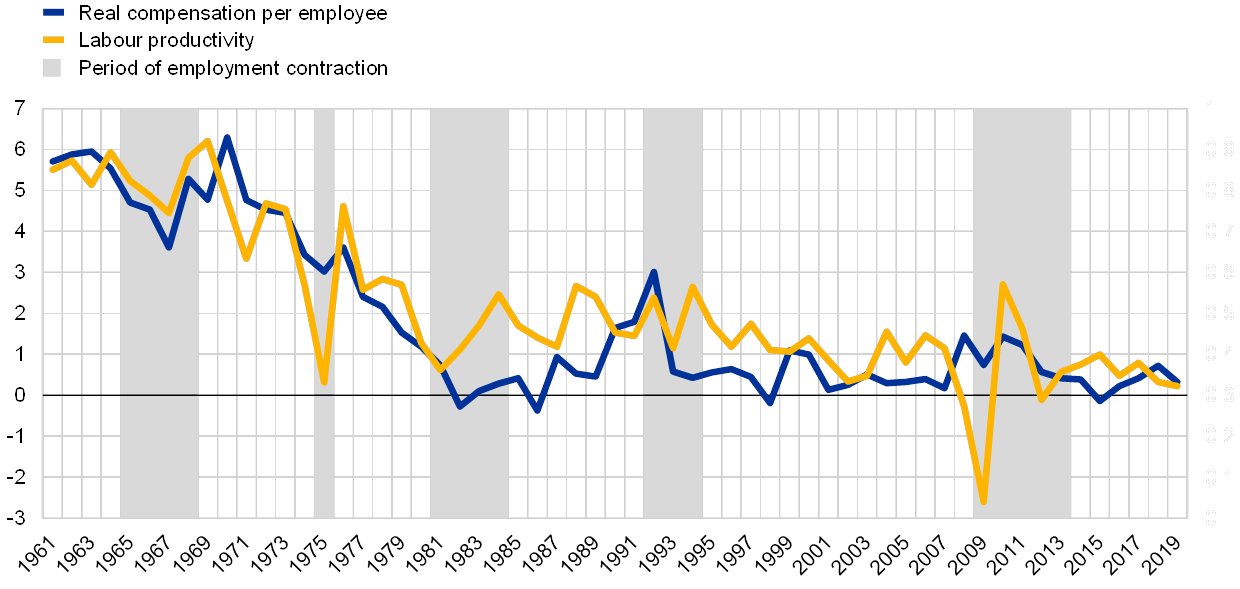

The decline in unemployment and the increase in employment in the current expansion have occurred alongside moderating labour costs, but that moderation has been weaker than that seen in the previous expansion. Real wages increased at an average rate of 0.3% per year over the period 2014-18, which is lower than the rate of 0.5% observed during the previous expansion period. However, average productivity growth during the current expansion has been only 0.7%, while in the previous expansion it stood at 1.1%.[6] Thus, real unit labour costs have continued to decline, although at a lower rate[7] (see Chart D). Taking a longer-term perspective, the decline in average GDP growth, together with the higher elasticity of employment growth to GDP growth, is associated with a slowdown in the growth rate of labour productivity per person employed. The productivity slowdown in the 12 countries in the sample has been prolonged over the course of the last four decades and has been accompanied by decelerating real wage growth. The deceleration in real wage growth was particularly marked in relation to the slowdown in productivity growth during the 1980s, leading to a sharp decline in the labour share during that period, as real wages became less responsive to labour productivity developments.

Chart D

Labour productivity and real compensation per employee

(growth rates, percentages)

Sources: European Commission AMECO database and ECB staff calculations.

Note: 2019 is based on the European Commission spring forecast for the EA12 available in the AMECO database.

Overall, this long-term analysis helps to put the recent recovery into perspective, in the context of past employment expansions and contractions. The reaction of employment to GDP growth has increased since the mid-1980s, with the current expansion being more employment-rich than past expansions. However, the elasticity of employment to GDP has historically been higher (in absolute terms) during employment contractions than during expansions, revealing some asymmetry in the way employment adjusts during upturns and downturns. The relationship between employment growth and GDP growth might have been affected by many factors, including structural reforms aimed at increasing flexibility in labour and product markets, or long-term shifts in the sectoral composition of employment and the increase in employment in the services sector. All in all, the observed changes in the long-term relationship between employment and GDP on the one hand and between real compensation per employee and productivity on the other could also reflect other factors such as a favourable shift in the schedule of labour supply, as well as unfavourable total factor productivity and/or capital productivity developments favouring a strengthening of the demand for labour relative to the demand for capital.

- The 12 countries considered in the analysis are: Belgium, Germany, Ireland, Greece, Spain, France, Italy, Luxembourg, the Netherlands, Austria, Portugal and Finland. They are referred to as the EA12.

- Using this definition, the historical data from 1960 to 2018 were partitioned into ten distinct time periods. An exception is made for 2011, which has been included in a period of contraction despite recording a slight increase in employment growth. Data for 2019 are shown separately and are based on the spring 2019 forecast of the European Commission, to ensure consistency with the analysis of historical AMECO data.

- As the purpose of the analysis is to compare employment growth with GDP growth, it does not explicitly account for population change over time. If the employment-to-population ratio is considered instead, employment developments look more pronounced for the current expansion period than for previous expansions. In particular, the employment-to-population ratio (for the 15-64 age group) reached pre-crisis levels in 2015 and its current level is the highest observed over the time period analysed in this box.

- See also the box entitled “Employment growth and GDP in the euro area”, Economic Bulletin, Issue 2, ECB, 2019.

- Various authors have tried to explain the increase in European unemployment. See, for example, Blanchard, O., “European unemployment: the evolution of facts and ideas”, Economic Policy, Vol. 21, No 45, 2006, pp. 5-59, which argues that there are several possible causes of the increase in European unemployment in the 1970s. The main explanations for the initial increase in unemployment in Europe are related to the impact of adverse and largely common shocks, such as the increase in oil prices and the slowdown in productivity growth. Moreover, different institutions have led to heterogeneous outcomes across countries; and some labour market policy responses were inadequate to address the increase in unemployment.

- Real wages are defined as real compensation per employee for the total economy, while labour productivity is defined as real gross domestic product per person employed. The conversion from nominal to real is conducted using the price deflator for GDP at market prices.

- The growth rate of real unit labour costs can be calculated as the difference between the growth rate of real wages and the growth rate of labour productivity. As such, real unit labour costs declined on average by 0.6% per year during the 1995-2008 employment expansion and are declining on average by 0.4% per year during the current employment expansion.