What the maturing tech cycle signals for the global economy

Published as part of the ECB Economic Bulletin, Issue 3/2019.

A maturing tech cycle has been one of the factors behind the significant trade slowdown in China at the turn of the year. The tech cycle argument rests on the fact that China and other key Asian economies, including Japan, are closely integrated through supply chains concentrated, especially, in the production of computers and other electronic devices – the tech sector[1]. The maturing tech cycle may reflect a number of factors: it could be associated with more structural sector-specific drivers, such as the possibility of an increasing level of saturation in the global market for smartphones and for new data centres; it could relate to mini-cycles linked to the launch of new models of tech products; or it may signal, more generally, a turn in the global business cycle. This box reviews basic characteristics of the Asian tech sector and shows that it has played an important role in the recent weakness in China’s trade. At the same time, the box also suggests that the trend in the global tech cycle associated with weaker trade in Asia may be bottoming out.

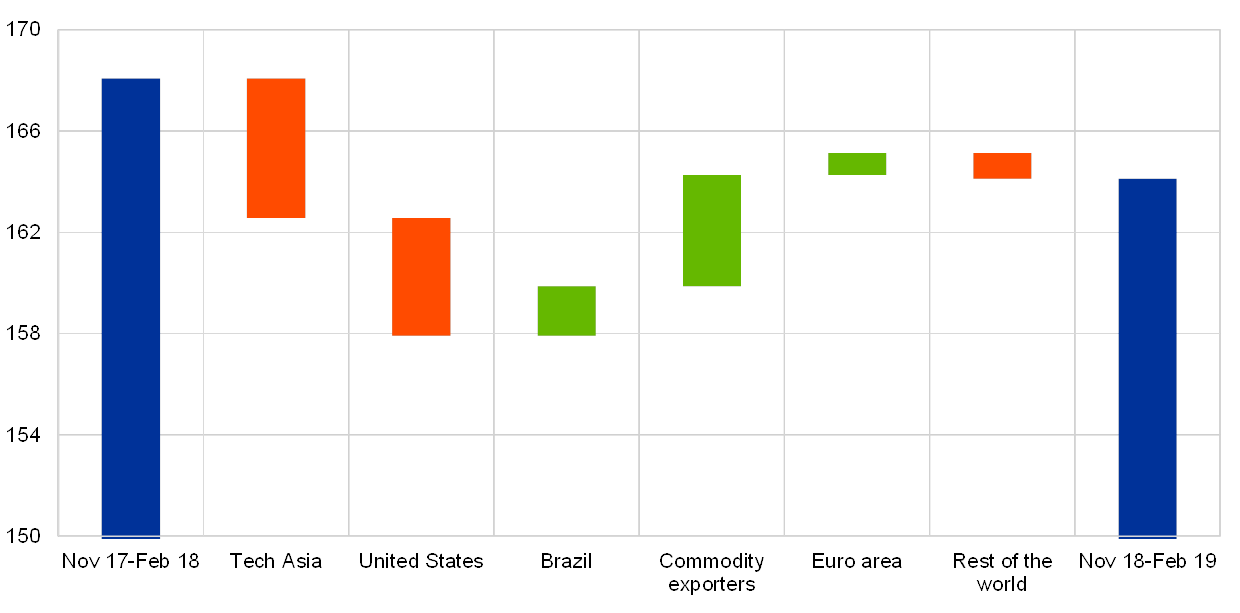

Weak merchandise imports from other key Asian economies have accounted for a substantial share of decelerating Chinese imports in recent months (see Chart A). Imports from the United States have also declined, partly as retaliatory tariffs on soybeans have diverted Chinese demand for soybeans to Brazil. At the same time, China has significantly increased imports of various commodities, including crude oil.

Chart A

Chinese imports by exporting country and regions

(USD billions)

Sources: China Customs via Haver Analytics and ECB calculations.

Notes: Total Chinese nominal imports are represented by the blue bars and exporting countries and regions by the red and green bars. Chinese imports from the respective countries and regions from the first period to the second period are represented by the red (lower) and green (higher) bars. “Tech Asia” denotes Japan, Korea, Malaysia, Singapore, Taiwan, Thailand and Vietnam. “Commodity exporters” includes all commodity-exporting emerging market economies, as well as Australia, Canada, New Zealand and Norway.

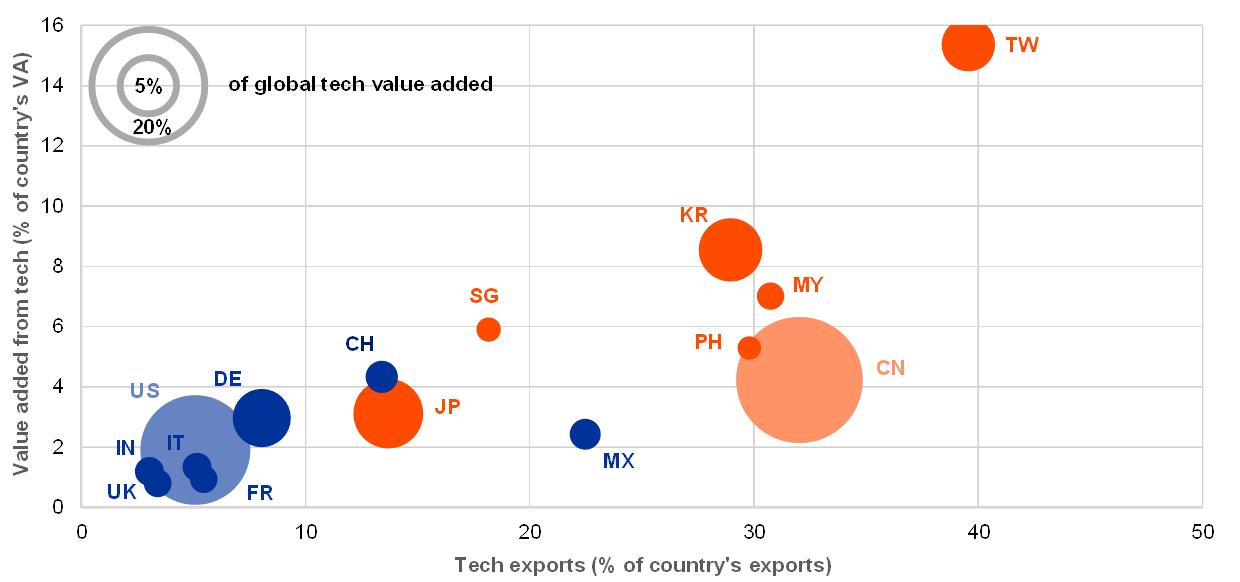

China and other Asian economies are specialised in tech sector production and satisfy around half of global demand for tech products. China alone accounts for more than a quarter of the sector’s global value added. The structure of Asian economies, with a notable exception of India, which specialises in IT services, is skewed towards tech production. This sector accounts, on average, for around 7% of total value added in the region. A high degree of specialisation in tech production is even more pronounced when looking at exports, where tech products account, on average, for more than a quarter of exported goods from the region (see Chart B). Asia dominates the tech sector also from a global perspective: it accounts for around half of the sector’s global value added and for more than two-thirds of global tech exports. Asian tech exports account for 10% of total global trade.

Chart B

Specialisation in the tech sector is common across Asian economies

(percentages; index: 2015)

Sources: OECD and ECB calculations.

Notes: “Tech sector” refers to “Computers, electronic and electrical equipment” (D26T27) in the OECD’s Trade in Value Added database. The size of the bubbles on the graph refers to the relative share of a country’s tech value added in global tech value added. Asian countries are shown in red.

The Asian tech supply chain connects advanced economies and emerging markets, with China the largest producer of final products. Japan and Korea are positioned upstream in the supply chain and, together with Taiwan, specialise in the production of semiconductors and chips. China remains the key assembler of final products in spite of a significant decline in import intensity. The import content of its tech production, which is subsequently exported, declined to 27% in 2015 from 40% only a decade ago, pointing to its declining dependence on intermediate goods sourced from the region. A country’s relative position in the supply chain determines whether domestic macroeconomic developments could provide useful signals also for global trends.

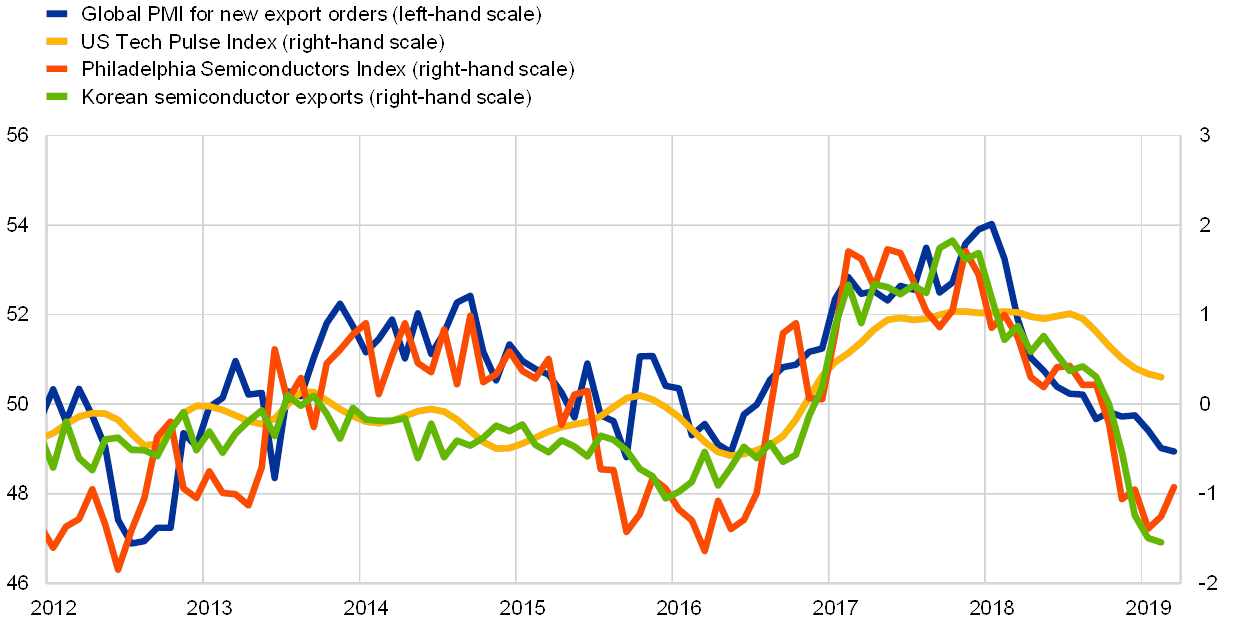

While the global tech cycle turned in early 2018, an orderly slowdown followed by some stabilisation seems the most likely scenario looking ahead. Recent indicators of the tech cycle point to a slowdown in the global tech cycle (see Chart C). However, there are some signs that suggest a stabilisation in the period ahead. First, financial market expectations for sectoral developments in the region – approximated by the Philadelphia Semiconductors Index (see Chart C, red line) – point towards some bottoming out this year, after falling in 2018. Second, while the global PMI for new export orders in the manufacturing sector has remained below the expansion-contraction threshold of 50, the pace of its decline in recent months has been significantly less steep than in the first half of 2018. Although it covers a broader set of exported products, it also shows a fairly high correlation with sectoral stock prices and thus could provide some further evidence of stabilisation in the global tech sector. And third, Korean exports of semiconductors – often used as another leading indicator of activity in the tech sector – have recently shown signs of stabilisation. Broader indices of activity in the technology sector, which are published with a somewhat longer lag and include the US Tech Pulse Index, and global trade in electronic components also suggests some limited weakening in the sector’s growth momentum. Overall, therefore, the turning of the global tech cycle seems partly to reflect a rather exceptionally strong period in 2017, related to substantial investment in expanding capacities of data centres globally. Despite a high degree of uncertainty, a soft landing currently seems a more likely scenario.

Chart C

Tracking the global “tech cycle”

(left-hand scale: diffusion index; right-hand scale: annual percentage changes)

Sources: Markit, Thomson Financial Datastream, FRED, KITA and ECB staff calculations.

Notes: The annual percentage changes for the US Tech Pulse Index, the Philadelphia Semiconductor Index and Korean semiconductor exports are mean-variance adjusted. The latest observations are for March 2019 (PMI, Philadelphia Semiconductor Index) and February 2019 (US Tech Pulse Index, Korean semiconductor exports).

- For the purposes of this box, “tech sector” is used to refer to the manufacturing of computers, electronic and electrical equipment.