Liquidity conditions and monetary policy operations in the period from 6 May to 21 July 2020

Published as part of the ECB Economic Bulletin, Issue 6/2020.

This box describes the ECB’s monetary policy operations and liquidity developments during the third and fourth reserve maintenance periods of 2020, which ran from 6 May to 21 July 2020. During this period, the market volatility associated with the coronavirus (COVID-19) crisis abated. This was helped by the implementation of measures announced by central banks, including the European Central Bank (ECB), and the fiscal support measures introduced by governments and EU authorities.

The levels of central bank liquidity in the banking system continued to rise during the third and fourth maintenance periods of 2020. This was largely due to the settlement of the targeted long-term refinancing operations (TLTRO III) and the asset purchases conducted under the asset purchase programme (APP) and the pandemic emergency purchase programme (PEPP). The Governing Council of the ECB decided on 4 June to increase the size of the PEPP envelope by €600 billion to €1,350 billion and to extend the purchase horizon until at least the end of June 2021. Moreover, it was decided that the maturing principal payments from securities purchased under the PEPP will be reinvested until at least the end of 2022.

In response to the COVID-19 crisis, the Governing Council also decided to set up a new Eurosystem repo facility for non-euro area central banks (EUREP). This facility will provide precautionary euro repo lines to non-euro area central banks, addressing possible euro liquidity needs in case of market dysfunction resulting from the COVID-19 shock that might adversely impact the smooth transmission of ECB monetary policy. Under EUREP, the Eurosystem will provide euro liquidity to a broad set of non-euro area central banks against adequate collateral, consisting of euro-denominated marketable debt securities issued by euro area central governments and supranational institutions. EUREP complements the ECB’s bilateral swap and repo lines which provide euro liquidity to non-euro area central banks. New bilateral repo lines with Romania, Serbia and Albania were announced during the review period.

Liquidity needs

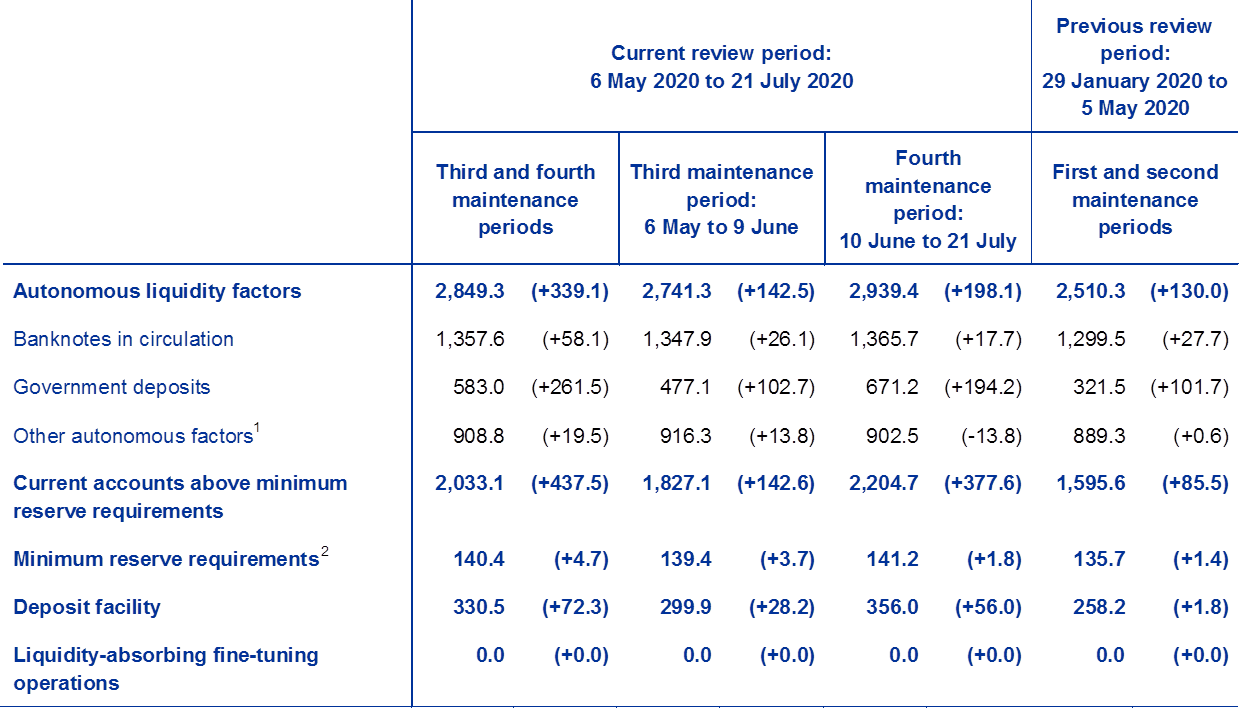

The banking system’s average daily liquidity needs, defined as the sum of net autonomous factors and reserve requirements, stood at €1,934.7 billion in the period under review. This was €321.3 billion higher than in the previous review period comprising the first two maintenance periods of 2020 (see the section of Table A entitled “Other liquidity-based information”). Net autonomous factors increased by €316.6 billion to €1,794.3 billion, while minimum reserve requirements increased by €4.7 billion to €140.4 billion.

Government deposits were by far the main autonomous factor that absorbed liquidity during the review period. Liquidity absorption by government deposits increased on average by €261.5 billion to €583 billion. Euro area government deposits stood at record highs, making up more than 9% of the Eurosystem’s balance sheet on average during the review period, compared with less than 6% during the previous review period. This growth in government deposits, which was well above trend, likely reflected fiscal measures, or the preparation thereof, undertaken by euro area governments to address the COVID-19 crisis. In addition to government deposits, banknotes and other autonomous factors contributed €58.1 billion and €19.5 billion respectively to an additional aggregate liquidity absorption of €77.6 billion compared with the previous review period. Autonomous factors that provided liquidity added €22.6 billion in liquidity relative to the previous review period, offsetting only partially the above-mentioned liquidity absorbing effect. In particular, net assets denominated in euro decreased by €37.9 billion, whereas net foreign assets increased by €60.5 billion relative to the previous review period (see the section of Table A entitled “Assets”).

On the whole, during the period under review, the supply of overall liquidity through monetary policy operations was well in excess of the liquidity absorption induced by net autonomous factors.

Table A

Eurosystem liquidity conditions

Liabilities

(averages; EUR billions)

Source: ECB.

Notes: All figures in the table are rounded to the nearest €0.1 billion. Figures in brackets denote the change from the previous review or maintenance period.

1) Computed as the sum of the revaluation accounts, other claims and liabilities of euro area residents, capital and reserves.

2) “Minimum reserve requirements” is a memo item that does not appear on the Eurosystem balance sheet and therefore should not be included in the calculation of total liabilities.

Assets

(averages; EUR billions)

Source: ECB.

Notes: All figures in the table are rounded to the nearest €0.1 billion. Figures in brackets denote the change from the previous review or maintenance period.

Other liquidity-based information

(averages; EUR billions)

Source: ECB.

Notes: All figures in the table are rounded to the nearest €0.1 billion. Figures in brackets denote the change from the previous review or maintenance period.

1) Computed as the sum of net autonomous factors and minimum reserve requirements.

2) Computed as the difference between autonomous liquidity factors on the liability side and autonomous liquidity factors on the asset side. For the purpose of this table, items in course of settlement are also added to net autonomous factors.

3) Computed as the sum of current accounts above minimum reserve requirements and the recourse to the deposit facility minus the recourse to the marginal lending facility.

Interest rate developments

(averages; percentages)

Source: ECB.

Notes: All figures in the table are rounded to the nearest €0.1 billion. Figures in brackets denote the change from the previous review or maintenance period.

1) Computed as the euro short-term rate (€STR) plus 8.5 basis points from 1 October 2019. Differences in the changes shown for the euro overnight index average (EONIA) and the €STR are due to rounding.

Liquidity provided through monetary policy instruments

The average amount of liquidity provided through open market operations increased by €824.7 billion to €4,291.9 billion (see Chart A). More than half (56%) of the increase in liquidity provided through monetary policy instruments was injected through credit operations; the remaining 44% was introduced through outright asset purchases. In particular, TLTRO III and the PEPP, with €541.5 billion and €258.7 billion respectively, contributed the largest amount of liquidity through monetary policy instruments.

Chart A

Evolution of liquidity provided through open market operations and excess liquidity

(EUR billions)

Source: ECB.

Note: The latest observation is for 21 July 2020.

The average amount of liquidity provided through tender operations increased by €464.3 billion during this review period, attributable largely to settlement of the fourth operation in the TLTRO III series (TLTRO III.4) in June 2020. The average increase of €541.5 billion provided through TLTRO III.4 was partially offset by maturities and/or voluntary repayments under the TLTRO II programme, representing a shift by counterparties to the more economically appealing TLTRO III.4. On average, maturities and repayments under the TLTRO II programme amounted to -€188.3 billion. Apart from the TLTRO II and III programmes, the newly introduced LTROs were an additional important instrument which added an average €112.4 billion in liquidity compared with the previous review period. These LTROs were introduced on 12 March 2020 as a transition instrument to provide immediate access to funding at particularly favourable conditions while allowing for a smoother rollover of funds into TLTRO III. The newly introduced LTROs matured before the end of the review period on 24 June 2020. During the review period, the ECB also conducted the first two of seven new pandemic emergency longer-term refinancing operations (PELTROs), which were announced in April 2020. These operations aimed at supporting the smooth functioning of money markets by providing an effective backstop to money market rates. These PELTROs added an average amount of €8.2 billion in liquidity. The main refinancing operation (MRO) and three-month LTROs played only a marginal role, recording an average aggregate decline of €1.3 billion compared with the previous review period.

At the same time, outright portfolios increased by €360.4 billion to €3,085.8 billion, owing to the continuation of net purchases under the APP and the PEPP. Average holdings in the PEPP amounted to an average of €285.3 billion, representing an increase of €258.7 billion in relation to the previous review period. Purchases under the PEPP represented the largest increase by far across all asset purchase programmes, followed by the public sector purchase programme (PSPP) and the corporate sector purchase programme (CSPP), with average increases of €79.4 billion to €2,230.2 billion and €18.0 billion to €217.0 billion respectively.

Excess liquidity

Average excess liquidity increased by €509.8 billion to €2,363.6 billion (see Chart A). Banks’ deposits with the Eurosystem grew by €437.5 billion to €2,033.1 billion in the current accounts in excess of minimum reserve requirements, and by €72.3 billion to €330.5 billion in the deposit facility. The partial exemption of excess liquidity holdings from negative remuneration at the deposit facility rate applies only to balances held in the current accounts. Banks therefore have an economic incentive to hold reserves in the current account instead of the deposit facility.

Interest rate developments

The €STR fell by 0.9 basis points (bps) during this review period compared with the previous review period owing to rising excess liquidity. The €STR stood on average at -54.5 bps during the review period compared with an average of -53.6 during the previous review period. The EONIA, which as of October 2019 is calculated as the €STR plus a fixed spread of 8.5 bps, moved in parallel with the €STR. ECB policy rates including the rates on the deposit facility, the main refinancing operation and the marginal lending facility were left unchanged during the review period.