Understanding the specific features of the CCyB and the SCCyB − evidence from the 3D DSGE model

Published as part of the Macroprudential Bulletin 8, September 2019.

As discussions progress on the potential design of sectoral capital buffers both at the Basel Committee on Banking Supervision (BCBS) and European levels, this article discusses the advantages and shortcomings of the sectoral application of the countercyclical capital buffer for addressing sectoral systemic risks. A dynamic stochastic general equilibrium (DGSE) model is used to explore and compare the transmission channels of the countercyclical capital buffer (CCyB) and the sectoral countercyclical capital buffer (SCCyB), as well as their role in enhancing the resilience of banks and taming the procyclicality of credit. The model-based policy exercise indicates that, if risks are confined to one particular credit sector, a SCCyB could prove more effective than the CCyB in strengthening bank resilience to the target sector and in mitigating sectoral credit imbalances.

1 Introduction

In the aftermath of the global financial crisis, the countercyclical capital buffer (CCyB) was introduced in the Basel III framework to increase the resilience of the banking sector and to reduce the procyclicality of credit. By requiring banks to build up capital buffers in the upswing of credit cycles which can be used to absorb losses during downturns, the CCyB aims to ensure the smooth provision of credit over the financial cycle. The CCyB can be considered a broad-based instrument, as it applies to banks’ total risk-weighted assets.

However, the CCyB may be too broad an instrument if exuberant credit developments are confined to specific sectors. While a growing number of studies provide evidence on the ability of the CCyB to increase the financial sector’s resilience to shocks and reduce credit procyclicality (see BCBS, 2018), a recent strand of literature finds that a sectoral CCyB (SCCyB) might entail significant benefits (see BCBS, 2019). For instance, Büyükkarabacak and Valev (2010) find that credit to households is a better predictor of banking crises than credit to corporates, suggesting that targeted policies would promote increased bank resilience without diminishing the growth enhancing effects of corporate credit. Existing evidence on the lack of synchronicity of sectoral credit cycles and the associated systemic risks (De Bakker et al., 2016, Samarina, 2015) also suggests that a more targeted design of capital requirements should be considered.

The aim of this article is to illustrate the features of the CCyB compared with its sectoral application. Following a summary of recent policy considerations at international, European and national levels, the article reviews the benefits and challenges of a SCCyB and presents the results of a quantitative policy exercise using a calibrated DSGE model for the euro area.

2 Policy considerations regarding sectoral capital buffers used as a macroprudential instrument

Based on analysis by the Basel Committee on Banking Supervision (BCBS), policymakers at European and international levels are discussing the benefits and challenges of a SCCyB. A literature review in a working paper by the BCBS (2018) indicates that, in the presence of sectoral risks to financial stability, especially in combination with low overall growth prospects, a SCCyB, as compared with the CCyB, may have (i) a more direct impact on the sector of concern, (ii) stronger signalling power, and (iii) smaller effects on the wider economy. Further research by the BCBS (BCBS, 2019) confirms that a SCCyB may be a useful addition to the CCyB framework, but also points to a number of challenges. These relate mainly to finding an appropriate balance between flexibility and efficiency gains on the one hand and the cost of increased complexity of the framework on the other. In a related article in this edition of the Macroprudential Bulletin[2], empirical evidence is presented on the relevance of sectoral cross-border bank lending both provided directly or via branches. The findings provide some support for extending mandatory reciprocity arrangements to sectoral capital buffers, including a SCCyB for those jurisdictions that plan to apply such a tool at national level, in order to ensure a level playing field between domestic and foreign banks.[3]

At the European level, the regulatory framework already includes sectoral macroprudential instruments, which are accompanied by borrower-based measures under national frameworks. For instance, Article 124 and 164 of the CRR[4] may be used to address emerging risks in the real estate sector, allowing relevant authorities to apply higher risk weights or loss given default floors for retail exposures secured by residential or commercial real estate. Sectoral capital-based measures implemented under Article 458 of the CRR are restricted to systemic risks in residential or commercial real estate sectors or intra financial sector exposures.[5] Furthermore, a number of national authorities have added borrower-based instruments linked either to the underlying collateral (e.g. loan-to-value limits) or to household income (e.g. loan-to-income, debt-to-income and debt service-to-income limits) to their macroprudential frameworks.[6]

The EU banking reform package adopted in spring 2019 will implement targeted changes to the macroprudential policy framework, with the aim of introducing more flexibility on the use of sectoral macroprudential instruments. The amendments to Articles 124 and 164 of the CRR clarify the role of national authorities in the activation of these instruments and allow a more granular application at the regional level. In addition, while up until now the systemic risk buffer (SRB) was aimed at addressing structural systemic risks for all, or a subset of, banks (Article 133 CRD IV), in CRD V[7] authorities can activate the SRB in a more flexible manner and also for sectoral exposures.

At the national level, Switzerland is the only jurisdiction where a SCCyB is already in place, while the Spanish government has recently introduced the legal basis for a SCCyB in Spain. A SCCyB was introduced in legislation in Switzerland in 2012, followed by an announcement of the Federal Council for other measures, in coordination with the Swiss National Bank which included increased down payment, shorter amortisation, and increased self-regulation.[8] Since the activation of the buffer in 2013, it has not been easy to isolate the impact of the SCCyB in order to assess its relative effectiveness. Nevertheless, the combined package of measures has helped to preserve and, in thoses cases where the additional capital requirement became a binding constraint, increase the banking sector’s resilience. Since then, Swiss residential mortgage and real estate market dynamics have gradually slowed. In Spain, authorities have introduced a SCCyB in their national macroprudential framework aimed at counteracting exuberant credit developments in particular sectors.[9]

3 Reflections on the benefits and challenges of a SCCyB

Reflections on the benefits of a SCCyB

The primary objective of a SCCyB is to ensure that banks can absorb losses related to the unwinding of sectoral imbalances. The CCyB remains the first line of defence to enhance the resilience of the banking sector during periods of excess aggregate credit growth. However, in situations where imbalances relate to specific credit segments, a sectoral application of the CCyB could allow macroprudential authorities to build up resilience in a more targeted manner, thereby reducing the risk of a generalised reduction in economic activity. In this regard, the SCCyB could be seen as a complement to the CCyB.

Owing to its targeted nature, a SCCyB may be a more effective and efficient policy instrument than its broad-based equivalent. The main advantage of a SCCyB is that macroprudential authorities could enhance banks’ resilience to the materialisation of sector-specific risks. Second, by increasing capital buffer requirements only for the specific sector where excessive credit imbalances are observed, macroprudential authorities could maximise the policy effect on the targeted segment, while reducing potential adverse side-effects on the supply of credit to unaffected sectors. This could minimise the overall costs of the policy intervention on the real economy (efficiency). Third, by increasing the relative cost of credit in the targeted sector, a SCCyB would make lending to that sector less attractive, which may also help curb sectoral credit cycles when credit dynamics in different sectors are uneven (effectiveness). In addition, unless risks are driven elsewhere in the financial system, it could also entail positive effects for financial stability by enhancing risk diversification across sectors.

Compared to a broad-based CCyB, a SCCyB applying only to a subset of exposures could be activated earlier in the credit cycle. In recognition of the high real economic costs of financial crises, a precautionary approach in macroprudential regulation is generally warranted. Owing to its targeted nature, a sectoral application of the CCyB could allow macroprudential authorities to address the identified risks in a more timely manner as imbalances are building up. The availability of a SCCyB is particularly appealing when sectoral credit imbalances arise in periods of low economic growth, as the costs of activating the broad-based CCyB are often considered too high to warrant its activation.

With a well-defined policy objective of increasing resilience towards sectoral cyclical risk, the use of a SCCyB could be conferred on macroprudential authorities. In this regard, it could be more straightforward to activate a SCCyB than in the case of risk weights pursuant to revised Articles 124 and 164 of the CRR, given the need for further coordination between micro- and macroprudential authorities in order to activate the tools. As regards the SRB pursuant to Article 133 of the CRD, European co-legislators agreed, inter alia, to remove the policy objective of the buffer to address “long-term, non-cyclical risks” from the legal text. While this introduces more flexibility in its use, it may, in principle, open up the use of the SRB for sectoral cyclical purposes. However, since the CRD V also includes a provision that the SRB cannot be used to address risks covered by the CCyB and the O‑SII/G‑SII buffer, this needs to be clarified. As a result, this could imply a more fragmented implementation across jurisdictions and possible overlaps with the CCyB and, where implemented, a SCCyB.

A SCCyB could be considered more transparent and possibly easier to communicate compared with adjustments in sectoral risk weights. Clear communication and the role of the expectations channel in altering how the public form their assessment on potential risks and take financial decisions are key for effective implementation of macroprudential policy (CGFS, 2016). In this regard, it is likely that a SCCyB would follow a quarterly risk assessment, with requirements set on top of all other capital requirements. By contrast, if risk weights were tightened for macroprudential purposes, this would increase both Pillar 1 and Pillar 2 requirements, as they are expressed as a percentage of risk-weighted assets. While national authorities can take this into account in the calibration of risk weights, the motivation for and disclosure of a SCCyB to counter sectoral cyclical risk may be perceived as more transparent by the public.

Reflections on the challenges of a SCCyB

The first challenge relates to the need to complement the existing risk assessment framework for the CCyB with an additional layer of granularity. It is likely that most of the indicators underpinning the risk assessment for the activation and calibration of the broad-based CCyB would also be used for the SCCyB. In this context, it is important to develop an overall risk assessment that is able to distinguish between sectoral versus broad-based vulnerabilities, where possible.

More granular macroprudential instruments may not internalise possible risk spillovers, which may take the form of leakages or loss spillovers. Leakages (or imbalance spillovers) may occur if activation of a macroprudential measure for banks results in a shift in lending towards unregulated or less regulated sectors or, alternatively, to credit provided by non-bank financial intermediaries. This may be desirable from a financial stability perspective if risk diversification across sectors in an economy is enhanced, but may also prove detrimental if imbalances are driven elsewhere in the system. By comparison, loss spillovers may affect untargeted sectors even in the absence of imbalance spillovers. For example, households may decide not to default on their mortgage debt during a downturn, but could react by cutting on their consumption spending, leading to credit risk materialising in other sectors of the economy.

The introduction of a SCCyB could increase the complexity of the macroprudential regulatory framework. The proliferation of a (potentially) large number of granular asset classes in the macroprudential regulatory framework would require additional layers of interaction and coordination between different authorities. As a result, the instrument’s activation process might become more burdensome and lengthy.

Any progress on the SCCyB should comply with the ongoing evaluation of the Basel III CCyB framework at the international and euro area levels. Since the financial crisis, an increasing number of countries in the European Union have activated a positive CCyB. At the international level, the BCBS has recently launched a comprehensive evaluation of post-crisis regulatory reforms, including an assessment of member jurisdictions’ experiences with the Basel III CCyB. In this regard, jurisdictions that wish to implement a SCCyB at national level should aim to comply with any guidance developed at the international and European banking supervision levels in order to avoid possible overlaps or discrepancies with existing macroprudential policy measures.

4 A comparison of the CCyB and SCCyB in the 3D DSGE model

This section presents a quantitative assessment of the relative features of the CCyB and a SCCyB in terms of increasing bank resilience in the event of credit imbalances emerging from the household sector only. The analysis is based on an extended version of the “3D” DSGE model as set out in Clerc et al. (2015).[10]

The model is a micro-founded DSGE model with financial frictions developed to quantitatively assess the impact of macroprudential policy instruments on financial intermediaries and the real economy. The three layers of default (“3D”) presented in the model make it particularly suitable for assessing risk accumulation and resilience in the household, non-financial corporation and banking sectors. In addition, the model provides an explicit rationale for macroprudential policy in the form of capital requirements owing to the presence of financial frictions and distortions. The model is calibrated to match the mean and the volatility of euro area variables from 2001 to 2014.

In the model, borrowing households, entrepreneurs and banks may all default on their liabilities.[11] Borrowing households finance house purchases with bank loans. Households default on their mortgage loans when the value of the collateral is lower than the outstanding debt obligations. Entrepreneurs engage in capital investment, financing their capital purchases with entrepreneurial wealth and bank loans. Entrepreneurs default on their loans when the return on their investments is lower than the contractual debt obligations. The financial system is populated by two types of banks, one specialised in lending to households and one specialised in lending to entrepreneurs. Each type of bank raises equity from shareholders and deposits from saving households to finance their loan portfolio. Banks fail when the realised return on the loan portfolio is lower than the banks’ deposit repayment obligations.

Capital requirements pertaining to the different sectoral credit exposures are imposed by a macroprudential authority according to a policy rule that includes a countercyclical buffer. More specifically, we compare two macroprudential policy rules. The CCyB rule implies that capital requirements (the amount of equity required per unit of loans) are increased (decreased) for all banks depending on positive (negative) deviations of total credit from the steady state. The SCCyB rule instead implies that capital requirements for banks’ lending to households (firms) increase when credit to households (firms) deviates positively from the steady state, and decrease for negative deviations of sectoral credit from the steady state.[12] The performance of the two policies is compared with respect to their effect on bank resilience and credit developments.

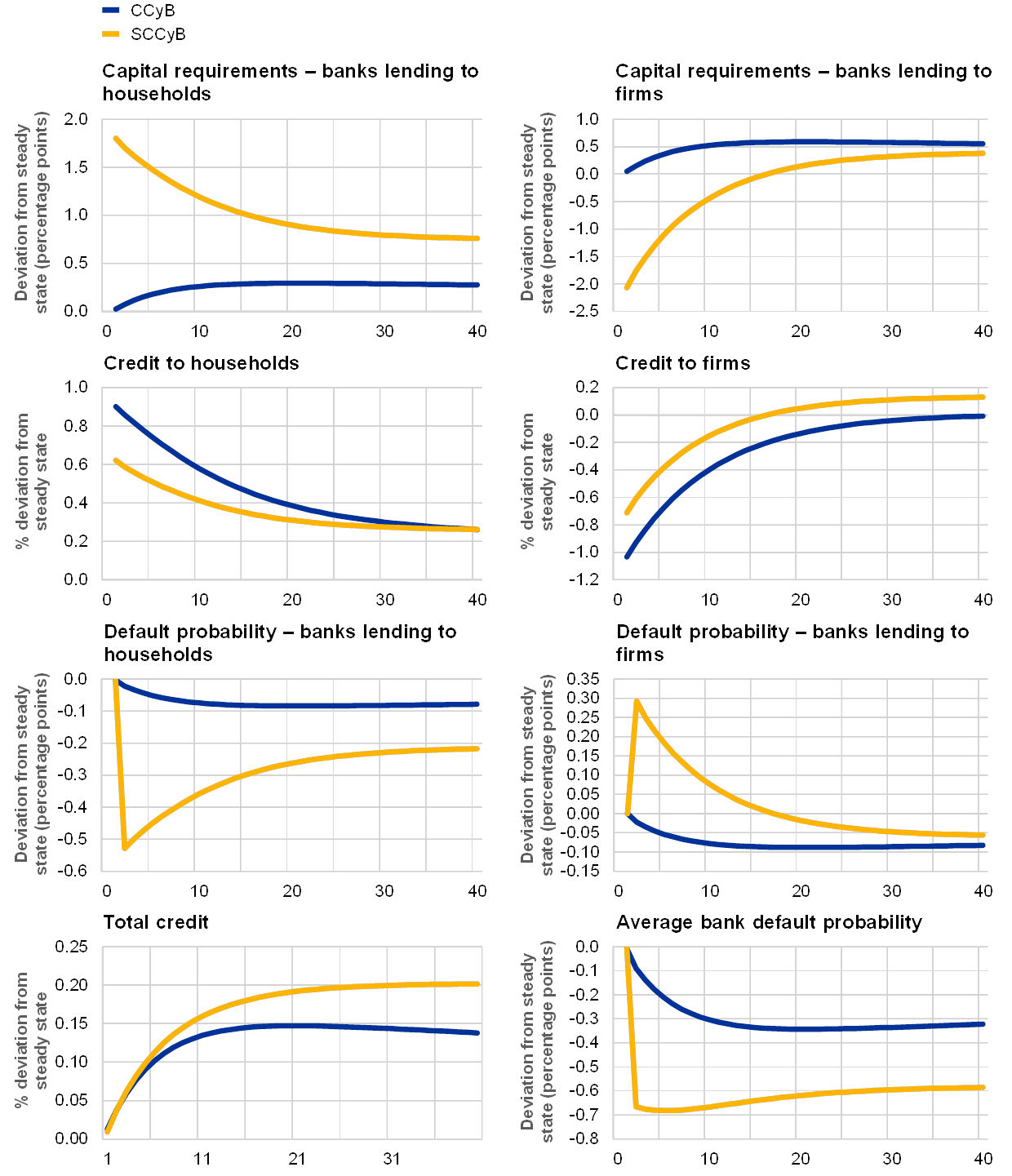

To assess the responses of key macroeconomic variables when either the CCyB or the SCCyB is activated, a shock is simulated which results in an increase in mortgage credit to the household sector. The housing preference shock considered increases households’ demand for loans for housing purposes, leading to a rise in credit to households (Chart 1). As households substitute expenditure in consumption goods with expenditure in housing (given the preference shock), the demand for consumption goods declines. The resulting drop in demand for firms’ products leads firms to cut capital investment and curtail the demand for corporate credit. Overall, the rise in credit to households dominates and total credit surges.

Chart 1

Impulse responses of model variables to a housing preference shock

Comparison of the CCyB and SCCyB policy rules

(x-axis: quarters after the shock; y-axis: percentage deviation from steady state (for capital requirements and banks’ defaults, deviation in percentage points, for average default banks annualised deviation in percentage points))

Source: own calculations.

The impulse responses of a CCyB versus a SCCyB reflect the differing impact of the two macroprudential rules on banks’ capital requirements. Since the deviation of total credit from steady state is always positive, the CCyB implies an additional positive capital requirement for both banks. This reduces the default rates of both banks’ lending to households and banks’ lending to corporates, as well as the banking sector’s average default rate. Compared to the broad-based rule, the SCCyB has a heterogeneous impact on the resilience of the two types of banks, as measured by their default rate. Given that the deviation of mortgage credit following the housing preference shock is positive and larger than that of total credit, the SCCyB imposes higher capital requirements on banks’ lending to households compared to the CCyB. As a consequence, the decline in these banks’ default rate is also relatively stronger. Conversely, as the demand for corporate credit declines as a result of the shock, the SCCyB leads to a decrease in the capital requirement for corporate exposures, as it reacts to the (negative) deviation of corporate credit (as a share of GDP) from the steady state. This leads banks’ lending to corporates to become de facto more risky because they are less capitalised, explaining their initial higher default rate. Overall, the enhanced resilience of banks’ lending to households dominates and the average default rate declines by more than under the CCyB rule.

These results show that, in the policy exercise considered, the SCCyB appears to be more effective than a CCyB in curbing sectoral credit cycles. Owing to the increase in total credit compared to the steady state, the broad-based CCyB rule implies a positive additional capital requirement for all banks in the model. On the contrary, the SCCyB rule reacts to the increase in credit to households, resulting in an increase in capital requirements that only affects banks specialising in lending to households. Because of its targeted nature, the increase (decrease) in credit in the household (corporate) sector is lower compared to the broad-based policy rule and, in this regard, the SCCyB has a smoothing effect across sectors.

5 Conclusion

The emergence of cyclical systemic risks affecting specific sectors warrants an exploration of the net benefits of introducing a SCCyB in macroprudential policy frameworks. While the CCyB is a very important policy tool to increase bank resilience and tame the procyclicality of aggregate credit, sectoral imbalances may warrant consideration of a more targeted, sectoral implementation of this instrument.

In light of ongoing discussions at the international, European and national levels, this article presents the main benefits and challenges of a SCCyB. Using a calibrated DSGE model for the euro area, the article explores and compares the effectiveness of the CCyB and the SCCyB in enhancing banks’ resilience and taming the procyclicality of credit in response to a surge in credit to households.

The quantitative evidence shows that the SCCyB could be a useful instrument to complement the CCyB in the macroprudential policy toolkit. In the event of sector-specific imbalances, the SCCyB allows policymakers to better strengthen the resilience of the targeted bank exposures and to curb sectoral credit cycles while limiting the costs in terms of foregone economic activity.

While the SCCyB may be a more effective and efficient policy instrument than its broad-based equivalent for addressing sectoral systemic risks, its introduction may result in a more complex macroprudential framework. In this regard, further work is needed to define the appropriate level of granularity of asset classes so as to balance the flexibility and complexity of the framework and formulate a framework for the activation and calibration of this instrument.

6 References

Azzalini, G., Jahn, N. and Pirovano, M., “Understanding the specific features of the CCyB and the SCCyB − evidence from the 3D DSGE model”, ECB Working Paper (forthcoming).

Basel Committee on Banking Supervision (2019), “Towards a sectoral application of the countercyclical capital buffer”, BCBS Working Paper, No 36, April.

Basel Committee on Banking Supervision (2018), “Towards a sectoral application of the countercyclical capital buffer: A literature review”, BCBS Working Paper, No 32, March.

Bernanke, B., Gertler, M. and Gilchrist, S. (1999), “The Financial Accelerator in a Quantitative Business Cycle Framework” in Handbook of Macroeconomics, Vol. 1 Part C, eds. Taylor, and Woodford, M., Elsevier, pp. 1341‑93.

Büyükkarabacak, B and Valev, N.T. (2010), “The role of household and business credit in banking crises”, Journal of Banking & Finance, Vol. 34, No 6, pp. 1247‑56.

Cantone, D., Jahn, N., and Rancoita, E. (2019), “Thinking beyond borders: how important are reciprocity arrangements for the use of sectoral capital buffers as a macroprudential tool?”, Macroprudential Bulletin, Issue 8, ECB.

Clerc, L., Derviz, A., Mendicino, C., Moyen, S., Nikolov, K., Stracca, L., Suarez, J. and Vardoulakis, A.P. (2015), “Capital regulation in a macroeconomic model with three layers of default”, International Journal of Central Banking, Vol. 11, No 3, pp. 9‑63.

Committee on the Global Financial System (2016), “Objective-setting and communication of macroprudential policies”, CGFS Papers, No 57, November.

De Bakker, B., Dewachter, H., Ferrari, S., Pirovano, M. and Van Nieuwenhuyze, C. (2016), “Credit gaps in Belgium: identification, characteristics and lessons for macroprudential policy”, Financial Stability Report, National Bank of Belgium, pp. 135‑157.

Lo Duca, M., Pirovano, M., Rusnák, M. and Tereanu, E. (2019), “Macroprudential analysis of residential real estate markets”, Macroprudential Bulletin, Issue 7, ECB, March.

Samarina, A., Zhang, L., Bezemer, D. (2015), “Mortgages and Credit Cycle Divergence in Eurozone Economies”, mimeo.

Swiss National Bank (2017), “Stance of the Basel III countercyclical capital buffer in Switzerland”.

Swiss National Bank (2012), “Financial Stability Report”.

7 Annex

In this exercise, we simulate two version of the 3D DSGE model, differing only in the specification of the macroprudential policy rule setting capital requirements. In the first case, the macroprudential authority sets capital requirements for banks’ lending to households and banks’ lending to firms according to the following rule:

Where the total capital requirement is a function of a fixed broad capital requirement and of a countercyclical capital requirement , namely the CCyB. The CCyB adjusts cyclically according to the deviations of total credit from the steady state , and the strength of this reaction is governed by the feedback coefficient .

In the second case, the macroprudential authority specifies, for each type of bank, a macroprudential policy rule in which the countercyclical component reacts to sectoral, rather than broad, credit. The macroprudential policy rules for banks’ lending to households (denoted with an H subscript) and banks’ lending to firms (denoted with the F subscript) are the following:

In these rules, the sectoral countercyclical buffers depend on sector-specific credit deviations: for F banks on deviations of credit to NFCs from the steady state value while for H banks on deviations of credit to households from the steady state value .

To compare the responses of key macroeconomic variables when either the CCyB or the SCCyB is activated, the economy is subject to a housing preference shock calibrated to obtain a 1 percentage point increase in house prices, which results in an increase in mortgage credit to the household sector. The feedback coefficient of the CCyB rule () is set to 4, while the BCR is kept at its fixed minimum level of 8%. To maximise the comparability between the two policy rules, the feedback parameters of the SCCyB applying to each banking sector (i.e. and ) are calibrated in order to minimise the deviation between the response of total credit to the shock under the CCyB rule and the SCCyB rule, and are set to 2.9. By ensuring that the response of total credit is similar under the two policy rules, this allows us to focus on the sectoral credit response to the shock under the different macroprudential policy rules. Finally, the CCyB and the SCCyB policies are implemented with the same speed of implementation, assuming a full phase-in over four quarters.

We would like to thank Gualtiero Azzalini for valuable research assistance.

See Cantone, D., Jahn, N., and Rancoita, E., “Thinking beyond borders − how important are reciprocity arrangements for the use of sectoral capital buffers?”, Macroprudential Bulletin, Issue 8, ECB, 2019.

Mandatory reciprocity would not need to apply when banks’ exposures towards the host country were below a specific de minimis threshold, to avoid an undue burden for banks, see ECB contribution to the European Commission’s consultation on the review of the EU macroprudential policy framework, p. 8.

Regulation (EU) No 876/2019 of the European Parliament and of the Council of 20 May 2019 amending Regulation (EU) No 575/2013 as regards the leverage ratio, the net stable funding ratio, requirements for own funds and eligible liabilities, counterparty credit risk, market risk, exposures to central counterparties, exposures to collective investment undertakings, large exposures, reporting and disclosure requirements, and Regulation (EU) No 648/2012.

This measure can be applied unless the Council adopts an implementing act to reject the measure upon a proposal by the European Commission.

The article “Macroprudential analysis of residential real estate markets”, Macroprudential Bulletin, Issue 7, ECB, March 2019) presents a more detailed discussion of real estate macroprudential instruments.

Directive (EU) No 878/2019 of the European Parliament and of the Council of 20 May 2019 amending Directive No 2013/36/EU as regards exempted entities, financial holding companies, mixed financial holding companies, remuneration, supervisory measures and powers and capital conservation measures.

See Swiss National Bank, Financial Stability Report, 2012, Press Release by the Federal Council, 2013, available here, Swiss National Bank, “Stance of the Basel III countercyclical capital buffer in Switzerland”, 2017.

See speech entitled “A framework for the CCyB”, by Pablo Hernández de Cos, Governor of the Banco de España, 3 June 2019.

For a more detailed analysis, see also Azzalini, G., Jahn, N., and Pirovano, M. “Understanding the specific features of the CCyB and the SCCyB − evidence from the 3D DSGE model”, ECB Working Paper (forthcoming).

All borrowers, including banks, operate under limited liability. External financing is modelled in the form of non-contingent (non-recourse) debt and is subject to costly state verification frictions as set out in Bernanke, B., Gertler, M. and Gilchrist, S. (1999). This implies that a bank’s lending premium is an increasing function of borrowers’ default probability.

See the Annex for additional details.