Published as part of the ECB Economic Bulletin, Issue 4/2024.

Standard indicators of profits in the economy which are derived from national accounts use GDP rather than economic output as a benchmark. While “output” is often used as a synonym for GDP, national accounts make a distinction between the two. Output, unlike GDP, includes intermediate consumption, i.e. the consumption of goods and services used in the generation of GDP or the related concept of “value added”.[1] “Output” is a well-defined concept, but the quarterly national accounts do not contain timely data on output for the euro area.[2] The standard national accounts profit indicators based on GDP hence allow profit developments – measured in terms of gross operating surplus and mixed income – to be assessed in relation to labour costs but not in relation to total costs. These indicators are therefore useful for assessing how profits are currently buffering rising labour costs, but do not show precisely how this has been hampered or facilitated by developments in costs for intermediate inputs such as energy. Such insights would be provided by profit indicators based on output.

Profit indicators that consider the total cost of inputs can be approximated by replacing output with the concept of “total supply”. Total supply is defined as the sum of GDP and imports, which are both available in the euro area quarterly national accounts. The approximation of output via total supply makes use of the fact that total supply minus imports equals GDP, which is equal to output minus intermediate consumption.[3] While the value of imports is considerably lower than that of intermediate consumption, import prices and intermediate goods prices move closely together.[4] This makes total supply a reasonable proxy for output when calculating profit margin developments, which are measured as the ratio of price to cost developments. While the standard profit margin indicator is derived as the ratio between the GDP deflator at basic prices and unit labour costs, the total supply-based profit margin indicator can be computed as the ratio of the total supply deflator to total unit costs (the sum of labour and import costs per unit).[5] Profit margin indicators have a distributional focus, as these provide information on developments in profits relative to the evolution of labour costs or total costs. For instance, a positive growth rate of a profit margin indicator shows that unit profits (defined as gross operating surplus and mixed income per unit of real GDP or of real total supply) are growing at a higher pace than the unit cost component considered.

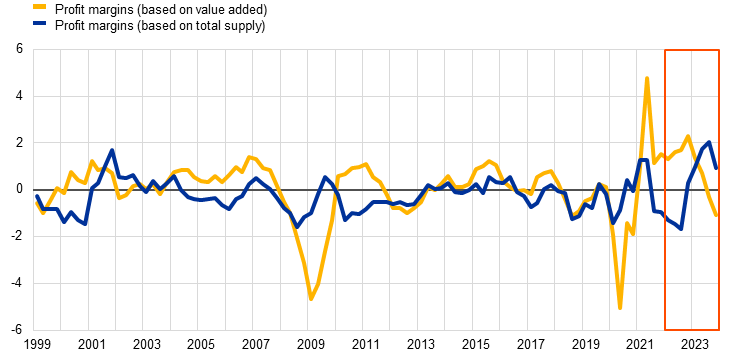

Taken together, the GDP (value added) and total supply-based profit margin indicators suggest that in 2023 profits started to buffer the impact of labour cost developments on price pressures but benefited from the decline in other costs. According to the GDP-based indicator, profit margins grew in 2022 but started contracting in 2023 in line with a buffering of labour costs in the second half of that year. [6] However, the total supply-based indicator suggests that profit margins declined in 2022 and, after increasing somewhat in the course of 2023, have started to slow more recently but remained positive.[7] In other words, it suggests that profit margins buffered total costs in 2022 when import prices surged, but increased in 2023, benefiting from the decline in import prices.

Chart A

Growth rate of profit margins based on GDP (value added) and total supply

(annual percentage changes)

Sources: Eurostat and ECB calculations.

Note: The latest observations are for the fourth quarter of 2023.

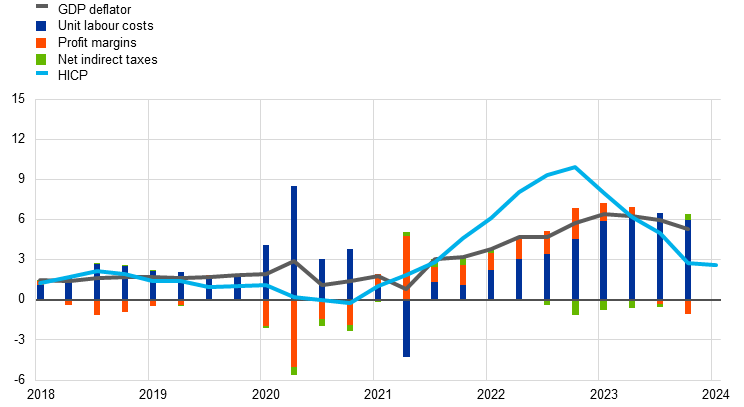

The total supply deflator, as a proxy for output prices, points to some bottoming out of overall price pressures in the euro area economy in the second half of 2023. Growth in the total supply deflator surged from 2021 to mid-2022 and then fell sharply, before showing signs of some stabilisation in the second half of 2023 (Chart B, panel a). As with the GDP deflator (Chart B, panel b), developments in the total supply deflator can be broken down into components. Its decomposition indicates the sources of the rise and fall in overall price pressures and their evolution over time. It suggests that the surge in inflation was triggered initially by a strong increase in import (input) price pressures. This was followed on the domestic side, with some delay and to a smaller extent, by a rise in profits and then in labour costs. The sequencing implies positive growth of profit margins on the basis of value added at the time of the inflation surge, but negative growth on the basis of total supply. The same sequencing is visible for the decline in price pressures, with reversed developments in profit margins. Import price pressures started to recede in mid-2022, and weakening price pressures have been visible for several quarters on the domestic side in the moderation of profit growth with the fading of the pandemic and energy crisis. In the fourth quarter of 2023, unit labour cost growth also started to decrease slightly.

Chart B

Total supply deflator and GDP deflator

a) Total supply deflator

(annual percentage changes)

b) GDP deflator

(annual percentage changes)

Sources: Eurostat and ECB calculations.

Notes: The latest observations are for the first quarter of 2024 for the HICP and for the fourth quarter of 2023 for the other data. Panel a): unit labour costs (TS) and unit imports (TS) are shown as percentage point contributions to unit total costs (TS).

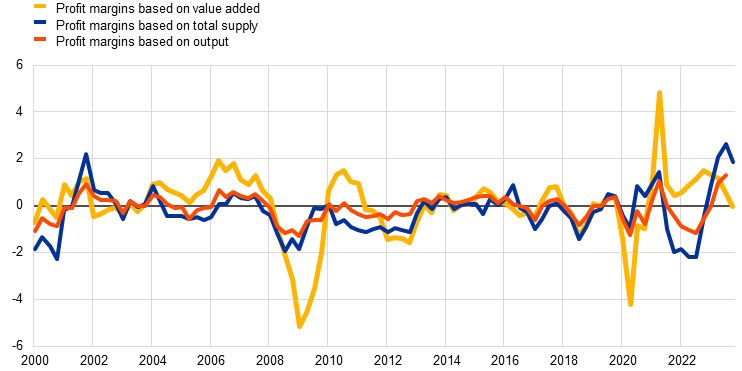

A profit indicator based on “genuine” output can be calculated for a limited sample of euro area countries, and its developments largely follow those of the indicators based on total supply. The total supply-based profit margin indicator may be an imperfect proxy for an output-based indicator if import prices develop very differently from intermediate consumption prices. The euro area quarterly national accounts provide information on output and intermediate consumption for six euro area countries, together accounting for 60% of euro area GDP.[8] This allows a direct comparison to be made between the profit margin indicators based on total supply and output respectively. For the limited sample, the two indicators have moved closely together over time and largely coincide in their periods of positive and negative growth, including in the most recent period.[9] The indicator based on output is slightly less volatile, which can be partly attributed to the fact that intermediate goods prices have recently been somewhat less volatile than the prices of imported goods. This suggests that, for the euro area as whole, the total supply-based profit margin indicator can be a reliable proxy for an output-based profit margin indicator.

Chart C

Growth rate of profit margins based on value added, total supply and output for a limited sample of euro area countries

(annual percentage changes)

Sources: Eurostat and ECB calculations.

Notes: The latest observations are for the fourth quarter of 2023 for the value added-based and total supply-based indicators and for the third quarter of 2023 for the output-based indicator. The limited sample of euro area countries comprises Germany, Estonia, Greece, France, the Netherlands and Finland.

To sum up, at times of exceptional movements in prices of intermediate inputs, a profit indicator based on total supply can complement the standard value added-based profit indicator. Looking ahead, following the relatively large deviations between the two indicators over the past two years, a fading out of the exceptional developments in import prices will likely lead to closer realignment of growth in profit margins based on value added and on total supply in terms of direction and positive/negative magnitudes.

Output is defined as the sum of gross value added and intermediate consumption. GDP is equal to the sum of gross value added and net taxes on products. See the European System of Accounts 2010 for a full description.

Data on output are available at annual frequency for the euro area. They are also available at quarterly frequency but only for a limited number of euro area countries.

For simplicity, we abstract from the role of net taxes on products.

An indication of this co-movement at the euro area level is the correlation coefficient of 0.9 between the quarterly annual rates of change of the import deflator and producer prices for intermediate goods for the period 1999 to 2023.

For a discussion of a wider set of profit indicators and the link between the concept of profits used in the national accounts (gross operating surplus and mixed income) and that of business profits, see the box entitled “How have unit profits contributed to the recent strengthening of euro area domestic price pressures?”, Economic Bulletin, Issue 4, ECB, 2023.

The large fluctuations of the standard profit margin indicator during and after the pandemic-related recession reflect large swings in some of the underlying data, such as labour productivity, during the recession.

Note that for unit profits, which is another frequently used profit indicator in the context of inflation analysis, developments in the standard indicator (gross operating surplus and mixed income divided by real GDP) and the corresponding total supply-based indicator (gross operating surplus and mixed income divided by real total supply) were very similar over the past two years. This is not surprising as there were exceptional developments in import prices but not in import volumes.

Data on output and intermediate consumption are available for Germany, Estonia, Greece, France, the Netherlands and Finland.

The developments in both the value added-based and the total supply-based profit margin indicator on the basis of the limited sample are comparable to those for the euro area aggregate (see Chart A).