Published as part of the ECB Economic Bulletin, Issue 7/2023.

This box discusses potential spillovers from recent negative inflation in China to euro area import prices. Economic developments in China are transmitted to euro area import prices directly via China’s export prices and indirectly via China’s important role in global demand for commodities and as a key supplier of intermediate and capital goods to the rest of the world. This box finds a tangible impact on euro area import prices, but a more limited impact on the broader euro area inflation environment.[1]

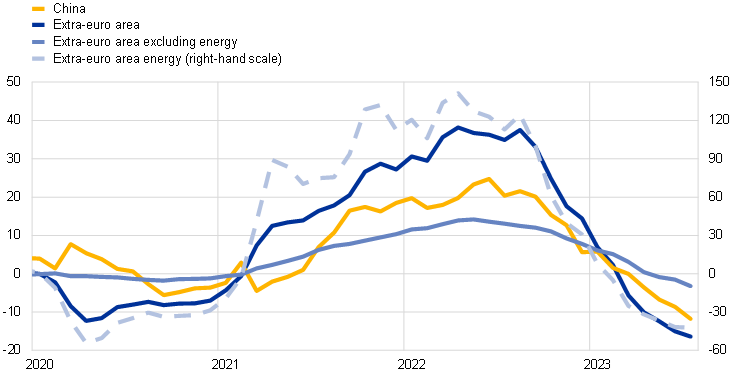

Following a surge in the past two years, euro area import prices have declined in recent months. In June 2023 annual extra-euro area goods import prices declined by 14%, largely owing to the rapid fall in euro area energy import prices. Excluding energy, extra-euro area import prices fell by around 2% (Chart A, panel a). We assess to what extent the stronger decline of import prices from China has reduced inflationary pressures in the euro area, given China’s weight in the euro area import basket (21%).

Chart A

Extra-euro area goods import prices and Chinese producer prices

a) Extra-euro area goods import prices

(year-on-year growth, percentages)

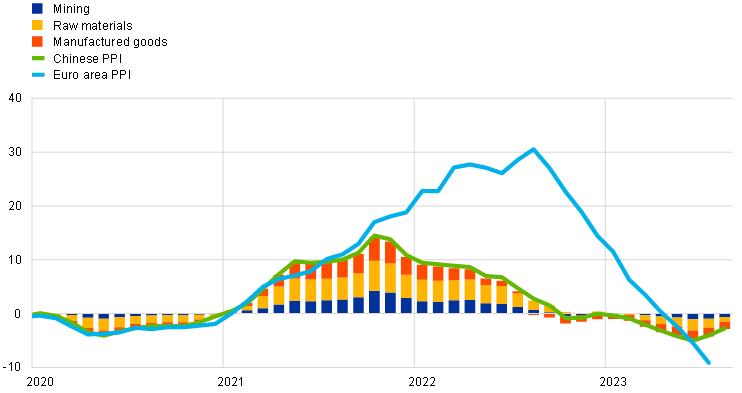

b) Chinese and euro area producer prices

(percentages and percentage point contributions to Chinese PPI)

Sources: Eurostat (for extra-euro area import prices), China National Bureau of Statistics and ECB staff calculations.

Note: The latest observations are for August 2023 for Chinese PPI and July 2023 for all other series.

Chinese producer price inflation has been on a downward trend since peaking in the last quarter of 2021, mainly reflecting a normalisation of domestic supply and demand factors during China’s recovery from the pandemic. The Chinese producer price index (PPI) rose strongly in 2021 owing to a strong rebound in activity after the 2020 pandemic shock, which pushed the price of coal (the main domestic energy source) sharply upwards as it coincided with government curbs on coal production. Subsequently, various developments suppressed China’s domestic PPI trends, while China’s export prices in 2021 and 2022 were still buoyed by global supply chain bottlenecks. China’s PPI inflation, after peaking in late 2021, declined steadily on the back of lower prices for mining, raw materials and manufactured goods (Chart A, panel b). By July 2023 China’s PPI had fallen for ten consecutive months. On the supply side, base effects stemming from China’s policy reversal on coal mining (from curbs to a sudden expansion) contributed significantly to the decrease in the PPI. On the demand side, a deep slump in the residential real estate sector, which further depressed material prices and related household goods prices, contributed to a lowering of producer prices.

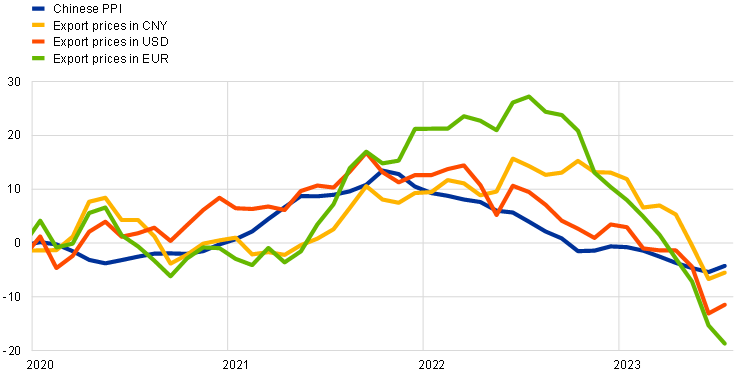

Over time, the normalisation of Chinese producer prices has helped to lower euro area goods import prices. A large share of Chinese exports are priced in US dollars, and Chinese export prices in US dollars have fallen alongside the Chinese PPI (Chart B). Translated into euro, Chinese export prices fell by 15% in June compared to the same month in the previous year. While the normalisation of Chinese producer prices is likely to have contributed to the moderation of export prices, Chinese firms also reportedly lowered prices to sustain their sales amidst a slowdown in external demand. A propagation of Chinese export price dynamics through third countries might also have influenced euro area import prices.

Chart B

Chinese producer and export prices

(year-on-year growth, percentages)

Sources: National Bureau of Statistics of China, Federal Reserve Board, General Administration of Customs of the People's Republic of China (for Chinese export prices) and ECB staff calculations.

Note: The latest observations are for July 2023.

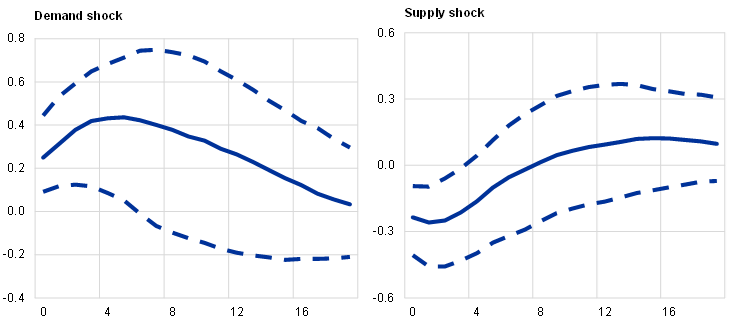

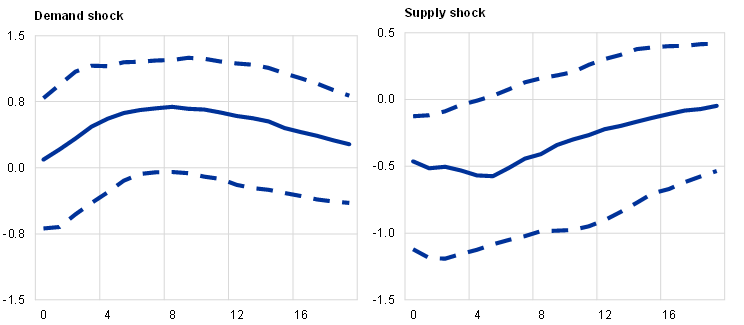

Empirical analysis confirms that Chinese demand and supply shocks may entail sizable spillovers to prices of extra-euro area goods imports. We use a Bayesian vector autoregression (BVAR) model with sign restrictions to quantify the role of Chinese demand and supply shocks in extra-euro area import prices in comparison with other key shocks, such as those related to global demand, supply bottlenecks and commodity supply.[2],[3] The results show that the median response to a Chinese demand shock which adds 1 percentage point to Chinese industrial production (IP) has a positive impact on both the Chinese PPI and extra-euro area import prices of around 0.4 percentage points, given the higher amplitude of extra-euro area import prices owing to their higher energy price component. The response of extra-euro area import prices is also affected by the indirect effect of a rise in global energy prices following the demand shock in China. A positive Chinese supply shock appears to lower the Chinese PPI by 0.3 percentage points and extra-euro area import prices by up to 0.5 percentage points, with the effect on extra-euro area import prices peaking after around six months (Chart C).[4]

Chart C

Responses to Chinese demand and supply shocks

a) Response of Chinese PPI

(x-axis: months; y-axis: percentage changes)

b) Response of euro area goods import prices

(x-axis: months; y-axis: percentage changes)

Sources: Eurostat, Haver, IMF, CPB, S&P Global and ECB staff calculations.

Notes: All series used in the empirical analysis in year-on-year growth rates except Purchasing Managers’ Index global supplier delivery times. Estimation sample from January 2006 to June 2023. Sign restrictions: Chinese demand shock (+: relative growth, Chinese IP, Chinese PPI); Chinese supply shock (0: commodity price; +: relative growth, Chinese IP; -: global supplier delivery times, Chinese PPI, extra-euro area import prices); commodity supply shock (+: commodity price, Chinese PPI, extra-euro area import prices; -: Chinese IP; 0: global supplier delivery times); global demand shock (+: commodity price, Chinese IP, global supplier delivery times; -: relative growth); global supply bottleneck shock (+: relative growth, global supplier delivery times; -: Chinese IP). Restrictions on impact. The size of the shocks is calibrated to add one percentage point to Chinese IP. Broken lines refer to 68% confidence bands.

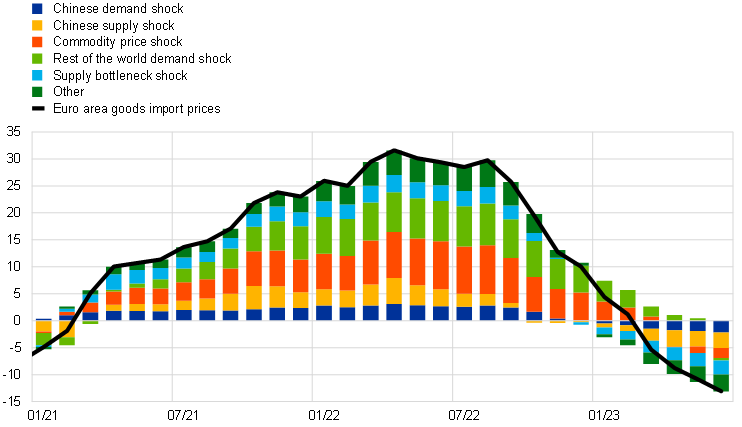

Chinese domestic shocks have played a tangible role in the surge in extra-euro area import prices since 2021 and in their reversal in recent months. Empirical results suggest that Chinese demand and supply shocks together contributed up to 8 percentage points to the rise in extra-euro area import prices in that period, which corresponds to about a quarter of the total increase (Chart D). In June 2023 developments in China contributed 5 percentage points to the decline in extra-euro area import prices. The rest of the decline is explained by weaker global demand, the easing of supply bottlenecks and negative commodity supply shocks.

Chart D

Historical shock decomposition of euro area goods import prices

(deviations from steady state, percentages and percentage point contributions)

Sources: Eurostat, Haver, IMF, CPB, S&P Global and ECB staff calculations.

The impact of lower prices in China on euro area headline inflation is more limited. A proper estimation of the impact would require a complex modelling of the product chain from import prices to consumer prices, which is beyond the scope of this box. However, a rough proxy can be derived by using estimates of the import content of euro area consumer prices, which is 29% for non-energy industrial goods (NEIG). This is the harmonised index of consumer prices (HICP) component with the highest import content across the main components (energy, food, services and NEIG) and is likely to be the most affected by developments in key trading partners such as China. This import content would imply a negative 1.5 percentage point peak impact on NEIG inflation. As NEIG accounts for about one quarter of the HICP, this would lower euro area HICP inflation by 0.4 percentage points. These tentative estimates do not provide information on the length of time over which this transmission would materialise, since a sizable share (43%) of imports from China are intermediate goods, and the impact on consumer prices may thus take some time to fully feed through.

For a forward-looking analysis of the impact of a further China downside risk scenario on the euro area, see Box 3 of “ECB staff macroeconomic projections for the euro area”, published on the ECB’s website on 14 September 2023.

The analysis includes extra-euro area import prices, Chinese industrial production and producer prices, commodity prices, the relative growth of industrial production in China and the rest of the world, and a measure of global supply bottlenecks. Chinese demand and supply shocks are identified through their different impacts on Chinese producer prices. Chinese demand and supply shocks are disentangled from global shocks by assuming that the former affect domestic production in China more than in the rest of the world. A positive Chinese supply shock is also assumed to ease global supplier delivery times.

The commodity supply shock captures movements in global energy prices that are not explained by global and Chinese demand shocks. The strong movements in euro area gas import prices over the past few years are not identifiable in this setup.

Euro area import price movements generally have a higher amplitude than the Chinese PPI series. The identified China supply shock therefore affects this volatile series more strongly than it affects the Chinese PPI.