Published as part of the Financial Stability Review, May 2022.

While rising interest rates are expected to improve banks’ net interest income in the short term, they may also weigh on banks’ net worth in the medium term. On aggregate, euro area banks exhibit a positive duration gap,[1] which implies that if interest rates rise, assets will lose more value than liabilities, thus reducing banks’ economic value of equity. After narrowing in 2020, the duration gap started widening again as of the first quarter of 2021 (Chart A, panel a), signalling that banks were reverting closer to pre-pandemic levels of interest rate risk. Over time, derivatives have, on aggregate, played an offsetting role; in other words, banks’ interest rate risk (IRR) exposure arising from their non-derivative positioning was partly counterbalanced by their derivative positions in the banking book.

Chart A

Euro area banks’ duration gap has widened recently, increasing their interest rate risk

Sources: ECB (Supervisory Banking Statistics) and ECB calculations.

Notes: Panel a: the duration gap is computed for the euro area aggregate based on Esposito et al.* and a sample of 62 significant institutions. Panel b: the change in bank net worth is computed based on Esposito et al.* and a sample of 62 significant institutions. The left chart shows the change in net worth for euro area banks on aggregate under the interest rate scenario considered, while the right chart plots the distribution across individual banks.

*) Esposito, L., Nobili, A. and Ropele, T., “The management of interest rate risk during the crisis: Evidence from Italian banks”, Journal of Banking and Finance, Vol. 59, October 2015, pp. 486-504.

The aggregate impact of higher interest rates on bank net worth would be moderately negative, but wide variations exist at the level of individual banks. The duration gap can be translated into sensitivity of bank economic value to changes in interest rates. For example, a steepening of the yield curve by 200 basis points at the longer end in the fourth quarter of 2021 would have reduced banks’ aggregate net worth by around 4% of Common Equity Tier 1 (CET1) capital (Chart A, panel b).[2] More than 60% of the banks analysed would face a decline in their net worth under this scenario, while for 25% the net worth would decline by more than 7% of CET1 capital. This decline arises as, in the medium to long term, banks would have to pay higher funding costs to cover legacy low-yielding assets. Changes in banks’ economic value of equity do not always translate into accounting losses, but they do shed light on banks’ resilience to changes in interest rates over the long run.

An empirical analysis of bank characteristics and IRR indicates that the share of exposures with longer rate-fixation periods plays a prominent role in this relationship and shows that derivatives are used to hedge IRR. The analysis[3] finds that the decline in bank net worth under a scenario of rising rates is more pronounced when the share of lending with fixation periods in excess of ten years is higher. Furthermore, larger banks seem to face a smaller decline in their net worth, possibly reflecting reduced hedging capabilities of smaller banks.[4]

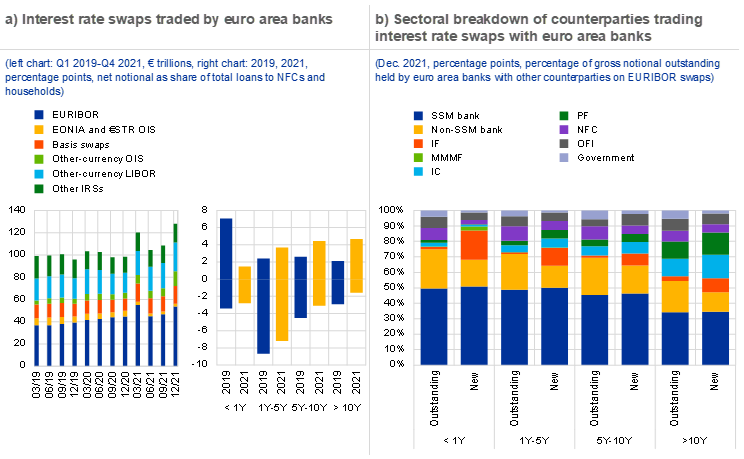

Chart B

Banks actively manage interest rate risk exposures by changing the maturity profile of IRS trading

Sources: ECB (Supervisory Banking Statistics and European Market Infrastructure Regulation) and ECB calculations.

Notes: Panel a: “Basis swaps” are IRS on floating interest rates, “EONIA and €STR OIS” are euro-denominated overnight index swaps, “Other-currency OIS” are overnight index swaps denominated in other currencies, “Other-currency LIBOR” includes GBP-, JPY-, CHF- and USD-denominated LIBOR swaps, “Other IRSs” includes fixed-to-fixed swaps, inflation swaps and other IRS. Right chart: net notional is aggregated in four maturity buckets. “NFCs” stands for non-financial corporations and “IRS” for interest rate swaps. Panel b: outstanding trades excluding intragroup transactions. Outstanding refers to outstanding contracts as of 31 December 2021, new refers to IRS trades initiated following March 2021. Trades with NCBs and counterparties with non-identifiable sectors are excluded and represent less than 2% of gross notional traded by euro area banks. Breakdown by sector: “IF” stands for investment funds, “MMMF” for money market mutual funds, “IC” for insurance companies, “PF” for pension funds, “NFC” for non-financial corporations, “OFI” for other financial institutions.

Euro area banks have held an increased volume of interest rate swaps over the last two years, suggesting more active hedging of interest rate risk. Banks enter into interest rate swaps in order to complement natural hedging, to take on more risk by means of directional exposures or to provide liquidity through market making. When they do so to mitigate risk, banks transform future cash flows generated from assets or liabilities from floating rates to fixed rates, or vice versa. By the end of 2021, the gross notional outstanding on interest rate swaps held by banks had increased to €128 trillion, while that on the most liquid euro-denominated contracts (EURIBOR swaps, EONIA OIS or €STR OIS) had risen by 30% since the start of 2019 to €56 trillion (Chart B, panel a). These contracts are more suited to reducing the volatility on banks’ balance sheets prompted by the repricing of euro-denominated cash flows. Over the last three years, banks have reduced their net notional[5] exposures to shorter-dated swap contracts (below one year), on which they pay fixed rates, and increased the volume of longer-dated contracts, on which they receive floating rates (Chart B, panel a). This evidence is consistent with the expectation of higher interest rates and the intention to hedge low-yielding assets against rate hikes.

Interest rate swaps are used to spread risk within the banking sector and to transfer it to insurance companies and pension funds. Focusing solely on euro-denominated interest rate swaps written on the euro interbank offered rate (EURIBOR), the overnight index average rate (EONIA) or the euro short-term rate (€STR), euro area banks trade most of these swaps with other banks. Concerning risk transfers to other sectors, banks’ transactions are not evenly spread across maturity buckets: insurance companies and pension funds receive fixed-rate payments for maturities over ten years given their aggregate negative duration gap, which makes them a natural counterparty for banks. For contracts initiated after March 2021, when inflation started to pick up, investment funds have assumed more risk for short maturities while, for longer maturities, the share of insurance companies and pension funds in swap trading has doubled (Chart B, panel b).

Banks’ IRR exposure appears moderate on aggregate, but wide variations exist across individual institutions. While rising rates would negatively affect the net worth of more than half of the banks analysed, their exposure has declined since 2017. Interest rate swap exposures, and particularly the volume of longer-dated receiver floating swaps, have increased since inflation started to pick up in March 2021, suggesting that euro area banks are using derivatives as hedging instruments. A normalisation of monetary policy should not be a major concern in terms of aggregate impact on the net worth of the euro area banking system, although it could have a negative effect on banks exhibiting large IRR exposures.

The duration gap measures the mismatch between the repricing timing of cash inflows (assets) and cash outflows (liabilities) of instruments which are already on banks’ balance sheet. A positive duration gap indicates that the duration of assets is larger than the duration of liabilities. In this analysis, the duration gap is computed as in Esposito et al. (see Notes to Chart A) using supervisory data on behavioural cash flows for 62 euro area banks.

This decline in net worth appears to be moderate overall, as the 2018 EBA guidelines on the management of interest rate risk in the banking book suggest that an institution is exposed to excessive IRR when its economic value of equity declines by more than 15% of its Tier 1 capital.

The analysis is based on different panel regressions covering 62 banks over the time period from Q4 2016 to Q3 2021 with time and bank fixed effects and a set of bank control variables.

Less significant institutions in Germany, such as savings banks and credit cooperatives, exhibited higher IRR than large banks; see “Financial Stability Review”, Deutsche Bundesbank, November 2016.

Net notional is computed as the difference between notional bought (pay fix) and notional sold (pay float) by each bank, on each contract, on each bucket of maturities and on each floating tenor. Intragroup transactions are excluded from net notional computations.