Results of a special survey of professional forecasters on the ECB’s new monetary policy strategy

Published as part of the ECB Economic Bulletin, Issue 7/2021.

Along with the Survey of Professional Forecasters (SPF) for the fourth quarter of 2021, participants were asked to complete an additional special survey on the ECB’s new monetary policy strategy. The aim of that survey was to gain an insight into how the participants in the regular SPF have assessed the new strategy and into whether it has already had, or will have, an impact on their forecasts. The questionnaire, together with the aggregate results, is available on the “Background on the survey of professional forecasters” webpage. This box summarises some of the findings.

A vast majority of respondents considered the ECB’s new monetary policy strategy to be an improvement and, on balance, thought that it made it more likely that the ECB would meet its primary objective of price stability in the euro area (Chart A). Two-thirds of respondents were of the opinion that the new monetary policy strategy was either “somewhat better” or “much better”, with only a small minority viewing it as “somewhat worse”. The so-called net percentage balance[1] was clearly positive at +45%. Almost 40% of respondents thought that the new strategy would make it either “somewhat more likely” or “much more likely” that the ECB would meet its mandate, and just over half thought it would be “about the same” (i.e. neither more nor less likely). Only a few respondents thought it would make it “somewhat less likely” and none thought it would be “much less likely”. The net percentage balance was positive at +19%.

Chart A

What is your overall assessment of the ECB’s monetary policy strategy compared with the situation before and will it make it more or less likely that the ECB will meet its mandate and primary objective?

a) What is your overall assessment of the ECB’s new monetary policy strategy compared with the situation before?

(percentage of responses)

b) In your opinion, will the new strategy make it more or less likely that the ECB will meet its mandate and primary objective of price stability in the euro area?

(percentage of responses)

Source: Special SPF survey in the fourth quarter of 2021.

Note: There were 51 responses for each question.

Respondents identified the clearer 2% and symmetric inflation target as the key elements of the new strategy. They also viewed those elements as the key improvements, particularly as they made the target more understandable for the general public. Respondents also considered that they facilitated the understanding of the ECB’s reaction function. Some respondents stated that it was the practical implementation in terms of actual policy changes that would ultimately determine the success of the new strategy. When asked about negative or missing aspects, a relatively common theme was that participants saw some ambiguity in various aspects of the new strategy, such as the inclusion of owner-occupied housing and the possible extent and duration of an overshooting of the inflation target that might be tolerated. A number of respondents also thought that monetary policy might be distracted from its primary objective by the consideration of other aspects, such as climate change. Some respondents were of the opinion that the new strategy did not adequately clarify some dimensions of asset purchases (in particular possible limits on holdings).

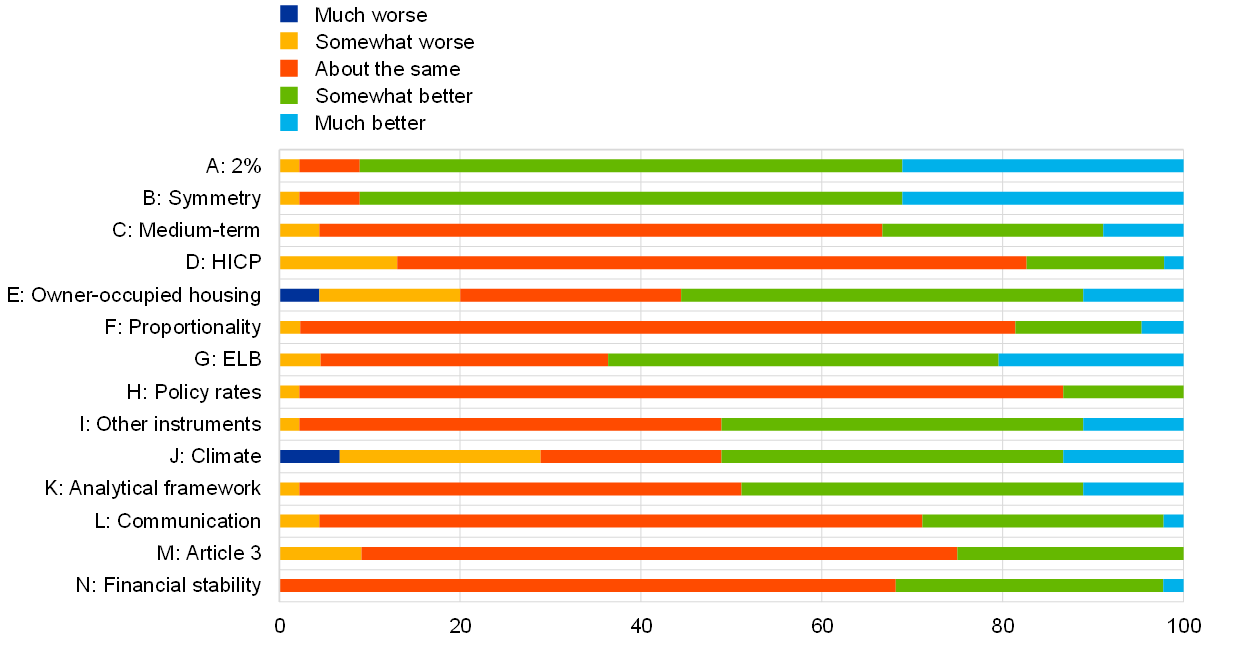

When asked explicitly about the importance of specific elements of the new strategy and whether these were better or worse, most respondents considered them all to be at least “somewhat important” and all at least “somewhat better” (Chart B). For example, with regard to the “move away from ‘below, but close to, 2%’ to ‘2%’”, a clear majority of respondents considered it to be either “very important” (44%) or “somewhat important” (50%). In terms of whether that change was viewed as an improvement or deterioration, again a clear majority thought it had made the strategy either “much better” (31%) or “somewhat better” (60%).

Chart B

Respondents were asked for their opinion of the following elements/statements in terms of their unimportance/importance and whether they represent a deterioration/improvement in the strategy.

a) What is your assessment of the following elements/statements in terms of their unimportance/importance?

(percentage of responses)

b) What is your assessment of the following elements/statements in terms of whether they represent a deterioration/improvement in the strategy?

(percentage of responses)

Source: Special SPF survey in the fourth quarter of 2021.

Notes: There were 43-48 responses for each element/statement. Element A refers to “Move away from ‘below but close to 2%’ to ‘2%’”; Element B refers to “Explicit reference to symmetry in the 2% inflation target”; Element C refers to “Confirmation of medium-term orientation”; Element D refers to “HICP remaining appropriate index for quantifying the price stability objective”; Element E refers to “Recommendation of roadmap to include owner-occupied housing in the HICP”; Element F refers to “Proportionality assessment”; Element G refers to “Especially forceful or persistent monetary policy measures when close to effective lower bound (ELB)”; Statement H refers to “Primary monetary policy instrument is the set of ECB policy rates”; Statement I refers to “Other instruments (forward guidance, asset purchases and longer-term refinancing operations) will remain an integral part of the toolkit”; Element J refers to “Adoption of climate-related action plan”; Element K refers to “Analytical framework (from two-pillar to integrated assessment of economic and monetary and financial analysis)”; Element L refers to “Communication”; Statement M refers to “Without prejudice to the price stability objective, the Eurosystem shall support the general economic policies in the EU with a view to contributing to the achievement of the Union’s objectives as laid down in Article 3 of the Treaty on European Union”; and Statement N refers to “The Eurosystem shall also contribute to the smooth conduct of policies pursued by the competent authorities relating to the prudential supervision of credit institutions and the stability of the financial system”.

In general, there was a strong correlation between the ranking of the various elements/statements in terms of their perceived importance in the new strategy and their perceived improvement on the previous strategy. Taking the percentage balance between positive and negative assessments as a summary statistic, respondents ranked the explicit reference to symmetry and the move away from “‘close to, but below, 2%’” to ‘2%’” as the two most important or relevant elements. Other elements with relatively high net percentage balances include the reference to especially forceful or persistent monetary policy action when the economy is close to the effective lower bound, the permanently expanded toolkit and climate-related action. It should also be noted that there was a positive net percentage balance for all of the elements/statements surveyed, indicating that respondents viewed them as important. In terms of their improvement on the previous strategy, the first four items (i.e. symmetry, 2%, forceful action at the effective lower bound and the toolkit) received the same ranking as for their importance.

Around one-third of respondents stated that they had changed their macroeconomic expectations more generally in response to the new strategy. Chart C lists the variables and the direction of the revisions. For headline inflation, underlying inflation and labour costs, changes to near-term forecasts were limited, while changes to longer-term forecasts were revised upwards. For real economy variables (real gross domestic product (GDP) and the unemployment rate), the changes reported were generally to medium-term forecasts. For elements of the ECB’s monetary policy toolkit (interest rates, forward guidance, asset purchases and longer-term refinancing operations (LTROs)) respondents had generally revised their forecasts in response to the new strategy in the direction of an easing of the policy stance.

Chart C

For each variable/assumption and horizon, respondents were asked to indicate the direction (down, unchanged or up) in which they had changed their macroeconomic forecasts.

(percentage of responses)

Source: Special SPF special survey in the fourth quarter of 2021.

Notes: There were 13-16 responses for each variable and horizon. For forward guidance, “shorter” is represented by “down” and “longer” is represented by “up”; for the euro exchange rate, “down (depreciation)” is represented by “down” and “up (appreciation)” is represented by “up”.

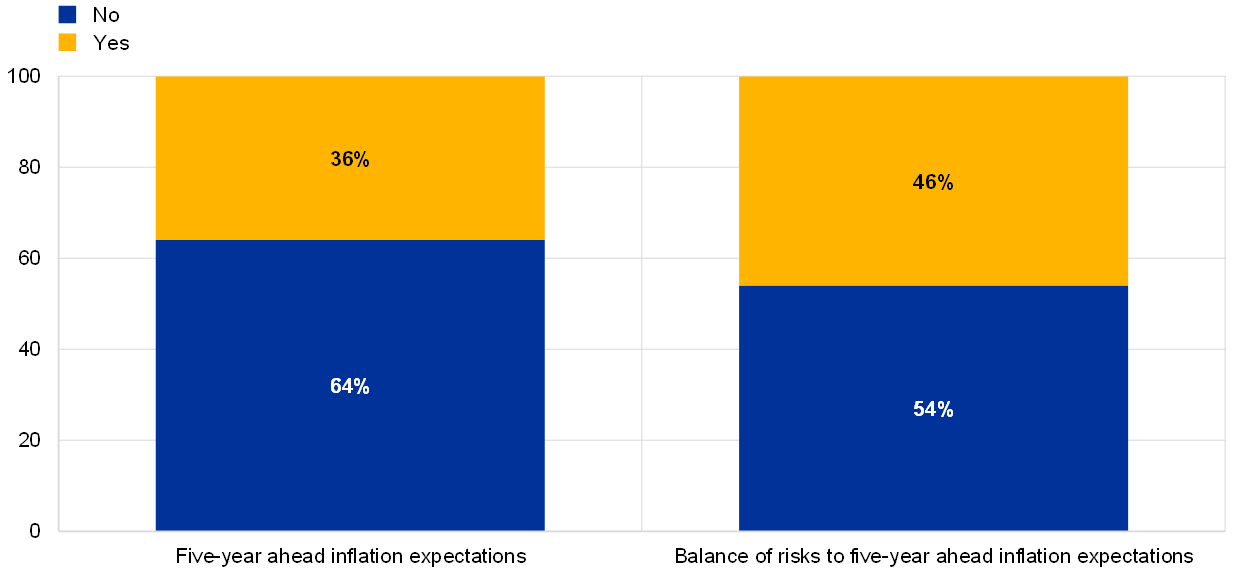

Considering longer-term inflation expectations specifically, some respondents reported that they had changed both their point longer-term inflation expectations and the balance of risks surrounding them in response to the new strategy. While a large portion (around 60%) of respondents had kept their five-year ahead inflation expectations unchanged in response to the new monetary policy strategy, over one-third had revised them upwards (Chart D). When asked how by much they had changed their five-year ahead inflation expectations, two-thirds said by 0.1 percentage points. With regard to their point expectations, more respondents (nearly half) indicated that they had revised upwards their assessment of the balance of risks to the five-year ahead inflation expectations.

Chart D

In response to the new monetary policy strategy, respondents were asked if they had revised or changed their assessments of…

(percentage of responses)

Source: Special SPF survey in the fourth quarter of 2021.

Note: There were 50 responses for each question.

- The net percentage balance is calculated as (a) the portion of respondents saying “much better” plus half of the portion saying “somewhat better” minus (b) half of the portion saying “somewhat worse” and the portion saying “much worse”. This score is bounded in the range ±100%, with +100% meaning that all respondents stated “much better” and -100% meaning that all respondents stated “much worse”. A positive (negative) net percentage balance generally indicates that more respondents thought that it was better (worse).