The COVID-19 crisis and its implications for fiscal policies

Published as part of the ECB Economic Bulletin, Issue 4/2020.

The coronavirus (COVID-19) pandemic has put unprecedented burdens on euro area countries’ economies and government finances, which will require a strong EU response in addition to action at national level. On 20 May the European Commission released its country-specific recommendations for economic and fiscal policies under the 2020 European Semester.[1] On 27 May it released proposals for a recovery fund to support the recovery with future investment and structural reforms.[2] This box examines how national fiscal policies are being coordinated under this year’s European Semester and explains that, in order to ensure an even recovery among euro area countries and to combat fragmentation, sizeable support will be required beyond that already provided at national level.

In response to the dramatic COVID-19 shock, all euro area countries implemented packages of fiscal measures. These packages consist of discretionary fiscal stimulus measures, state guarantees for loans to firms and other liquidity support measures. An important component of the discretionary measures relates to support for firms, in particular to preserve employment.[3] Countries have also focused on health spending and measures aimed at supporting the unemployed and other vulnerable groups through various social transfers. On the revenue side, deferrals of tax and social security contributions are aimed mainly at providing liquidity support to households and companies. According to the European Commission’s Spring 2020 Economic Forecast, the discretionary fiscal measures amount to 3.25% of GDP at the aggregate euro area level. In addition, state guarantees for loans to firms and other liquidity support measures amount to around 20% of euro area GDP, according to governments’ budgetary plans as outlined in the stability programmes published at the end of April.[4] These plans, however, reveal large differences in the size of the packages adopted across countries, most notably in the amount of state guarantees provided. Such differences raise the risk of an uneven recovery in the euro area and fragmentation between euro area economies.

To facilitate a sufficient immediate response to the exceptional crisis, the ECOFIN Council on 23 March activated the Stability and Growth Pact’s general escape clause. In the event of a severe economic downturn for the euro area or the EU as a whole, and provided debt sustainability does not become endangered, the triggering of this clause allows countries to depart from the fiscal adjustment requirement that would usually apply under the EU’s fiscal rules.[5] The ECOFIN Council stressed that the resulting support should be “designed, as appropriate, to be timely, temporary and targeted”.

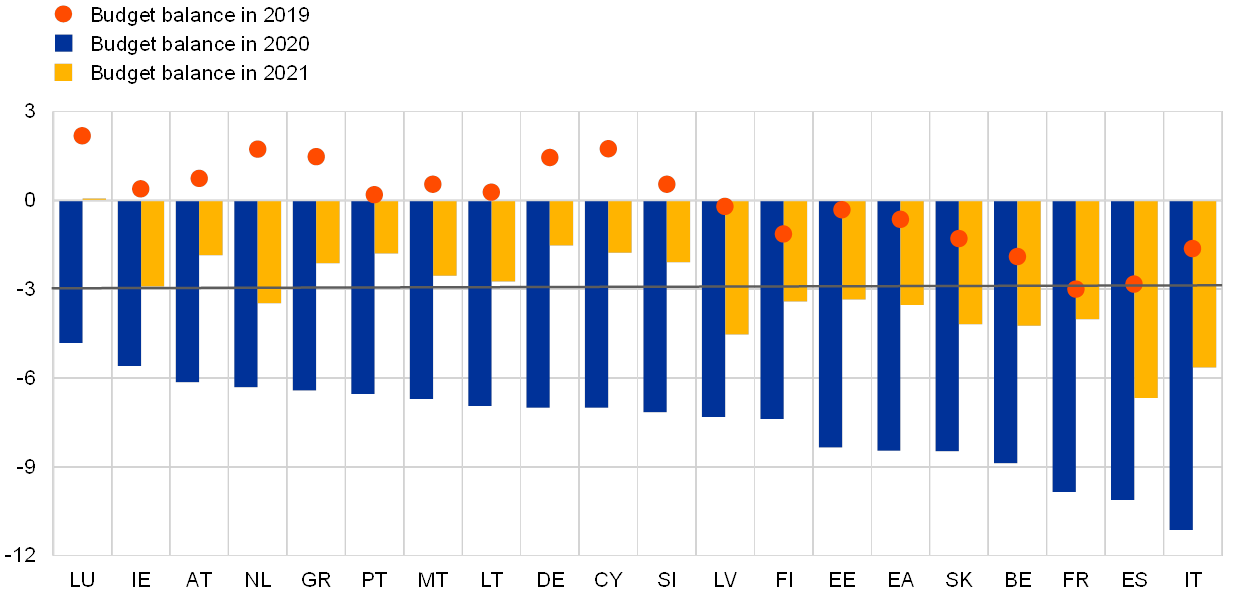

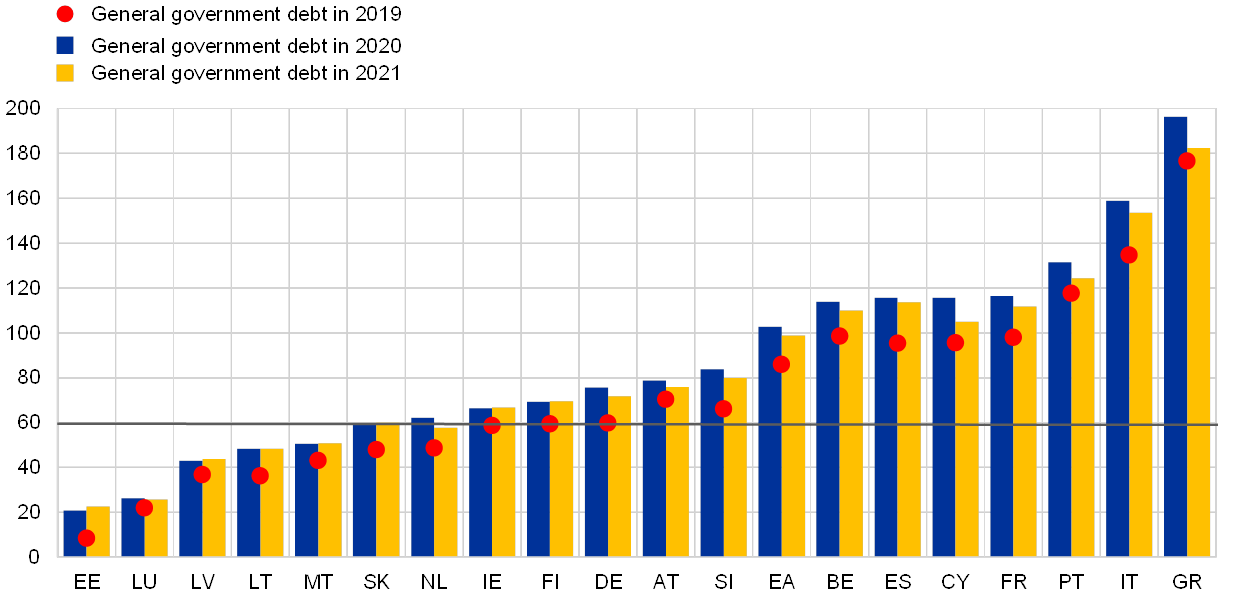

The depth of the COVID-19 shock and the size of the fiscal response have led to a drastic deterioration and heterogeneity in fiscal positions. According to the European Commission’s Spring 2020 Economic Forecast, the euro area budget deficit is expected to increase to 8.5% of GDP in 2020 from 0.6% of GDP last year. While eleven countries recorded budgetary surpluses in 2019, all euro area countries are expected to record budget deficits in excess of the 3% of GDP reference value this year. The largest deficits are forecast for Belgium, Spain, France and Italy, which were among those countries that entered the crisis with high government debt-to-GDP ratios (see Charts A and B). The euro area aggregate debt-to-GDP ratio is expected to rise steeply, by 16.7 percentage points, to 102.7% of GDP in 2020, with large heterogeneity across countries. Countries that entered the crisis with debt ratios of around 100% will experience the strongest increases in indebtedness. Only six euro area countries (Estonia, Luxembourg, Latvia, Lithuania, Malta and Slovakia) are expected to maintain debt ratios below the 60% of GDP reference value in 2020. In 2021, under unchanged policies, government deficit and debt-to-GDP ratios are expected to decline, albeit remaining far above pre-crisis levels.

According to the Commission, no euro area country is currently compliant with the Treaty’s government deficit criterion and some are also non-compliant with its debt criterion.[6] However, given the exceptionally large uncertainty regarding economic developments, “including for designing a credible path for fiscal policy”[7], the Commission is not at present recommending the opening of excessive deficit procedures. Later in the year, the Commission will reassess Member States’ budgetary situations based on its Autumn 2020 Economic Forecast and euro area countries’ draft budgetary plans for 2021.

All countries will need to continue supporting their economies to recover from the severe shock, while safeguarding medium-term fiscal sustainability. The Commission’s recommendations for fiscal policies for 2020-21 state that countries should “In line with the general escape clause, take all necessary measures to effectively address the pandemic, sustain the economy and support the ensuing recovery”. Subsequently, “When economic conditions allow”, countries are recommended to “pursue fiscal policies aimed at achieving prudent medium-term fiscal positions and ensuring debt sustainability, while enhancing investment”. When the severe economic downturn dissipates and before doubts about medium-term debt sustainability arise, use of the Pact’s general escape clause will need to be discontinued. Fiscal policies will then need to resume the adjustments provided for in the Pact.

Chart A

General government budget balances, 2019-2021

(percentages of GDP)

Sources: European Commission (AMECO database) and ECB calculations.

Chart B

General government gross debt, 2019-2021

(percentages of GDP)

Sources: European Commission (AMECO database) and ECB calculations.

A strong European response is required to support the recovery and avoid economic fragmentation in the euro area, and first steps have been taken. Safety nets for workers, businesses and sovereigns have been put in place, amounting to a package worth up to €540 billion. First, a European instrument for temporary Support to mitigate Unemployment Risks in an Emergency (SURE) will provide loans to sovereigns and is expected to unlock funding for national short-time employment schemes as well as for some health-related expenditure for the duration of the emergency. Loans totalling up to €100 billion will be granted to Member States on favourable terms, building on the EU budget as much as possible and secured by guarantees provided by Member States.[8] Second, a €25 billion pan-European guarantee fund will be created to strengthen the activities of the European Investment Bank (EIB). This could support €200 billion of financing for companies, including through national development banks.[9] Third, as a safeguard for euro area sovereigns, a Pandemic Crisis Support instrument was established, based on the European Stability Mechanism’s (ESM) existing precautionary credit line, the Enhanced Conditions Credit Line (ECCL). Access granted will be 2% of the respective Member State’s 2019 GDP, with an overall envelope of €240 billion. The sole requirement to access the credit line is that Member States requesting support “commit to use this credit line to support domestic financing of direct and indirect healthcare, cure and prevention related costs due to the COVID 19 crisis”.[10]

Nonetheless, further efforts to prepare and support the recovery at EU level are needed. On 27 May the European Commission presented its proposals for a recovery plan which includes a new €750 billion recovery instrument called “Next Generation EU”, embedded within a reinforced multiannual financial framework (MFF). Next Generation EU would consist of €500 billion in grants and €250 billion in loans to Member States, notably to support investment and structural reforms. Priority will be given to long-term strategic investments to support green and digital transition. Going forward, it is important that EU Member States reach a timely agreement on strong efforts to support their economies.

- For details, see 2020 European Semester: Country Specific Recommendations / Commission Recommendations. The recommendations were endorsed by the ECOFIN Council on 9 June.

- For details, see “Europe's moment: Repair and prepare for the next generation”.

- See also the box entitled “Short-time work schemes and their effects on wages and disposable income” in this issue of the Economic Bulletin.

- For more information, see 2020 European Semester: National Reform Programmes and Stability/Convergence Programmes.

- For details, see the Statement of EU ministers of finance on the Stability and Growth Pact in light of the COVID-19 crisis of 23 March 2020.

- The European Commission adopted reports under Article 126(3) of the Treaty on the Functioning of the European Union for all Member States except Romania (see Excessive deficit procedures – overview). These reports assess Member States’ compliance with the deficit criterion in 2020, based on their plans or on the European Commission’s Spring 2020 Economic Forecast. In all cases, apart from Bulgaria, the European Commission concludes that the deficit criterion is not complied with. In addition, the reports for Belgium, Cyprus, France, Greece, Italy and Spain also assess compliance with the debt criterion in 2019 based on outturn data. For Belgium, France and Spain, the Commission concludes that the debt criterion is not complied with, while for Cyprus and Greece, its conclusion points to compliance. For Italy, the European Commission concludes that there is “no sufficient evidence that the debt criterion … is or is not complied with”.

- See Communication from the Commission: 2020 European Semester: Country-specific recommendations.

- See Council Regulation (EU) 2020/672 of 19 May 2020 on the establishment of a European instrument for temporary support to mitigate unemployment risks in an emergency (SURE) following the COVID-19 outbreak (OJ L 159, 20.5.2020, p. 1).

- See “EIB Board approves €25 billion Pan-European Guarantee Fund in response to COVID-19 crisis”.

- See “ESM Pandemic Crisis Support”.