Euro area banks’ sensitivity to corporate decarbonisation

Published as part of Financial Stability Review, May 2020.

As awareness of the environmental, social and economic risks from disorderly climate change has grown, so has awareness of the need for businesses to accelerate their decarbonisation. Banks need to be prepared for changes in loan performance should financial losses result from abrupt shifts in policies, technologies or consumer sentiment in response to the risks posed by climate change. While credit ratings could in principle capture such risks, in practice rating agencies have only just begun incorporating risks arising from an abrupt transition to a low-carbon economy.

This box assesses how sensitive the euro area banking system is to higher probabilities of default for corporates stemming from an abrupt carbon adjustment.[1] A first scenario examines the impact of corporate rating downgrades applied indiscriminately to climate-sensitive economic sectors.[2] A second scenario exploits firm-level data to examine the potential for downgrades within sectors, where all companies reporting high carbon emissions are reassessed by rating agencies. Both analyses are based on ECB supervisory statistics (large exposures dataset)[3] and ECB securities holdings statistics.

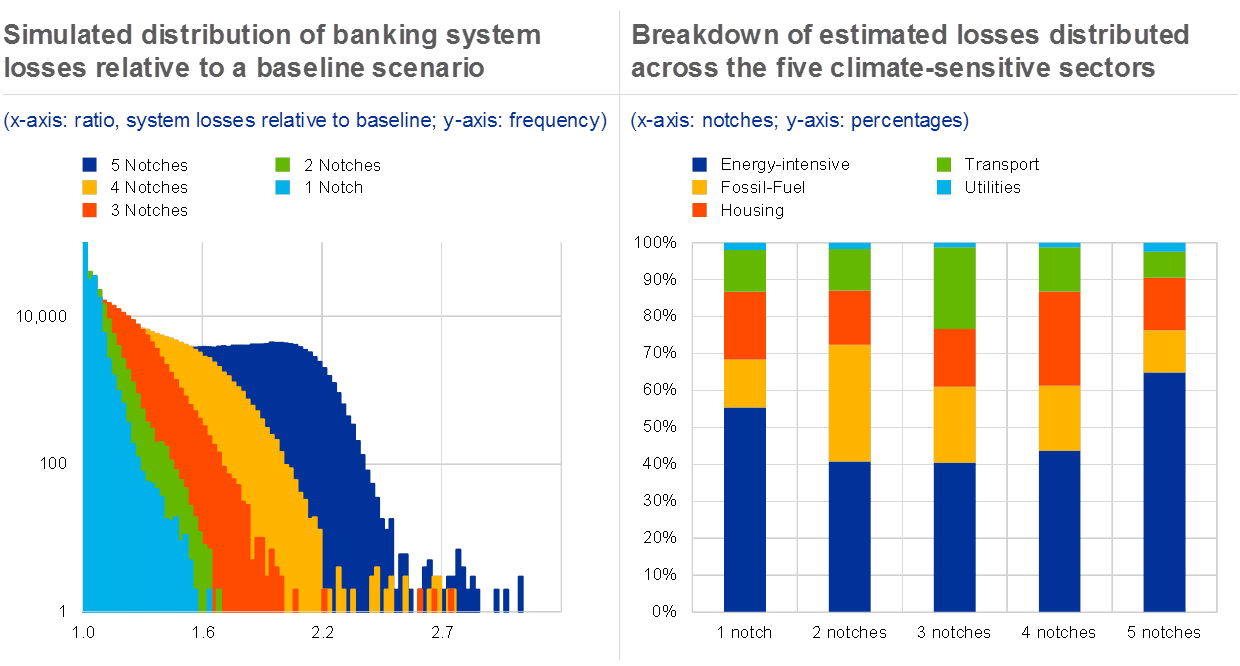

Euro area banking system losses in the event of an abrupt climate transition for carbon-intensive sectors

Sources: Moody’s and ECB calculations.Notes: The left panel presents the factor of increase in losses relative to a baseline non-stressed scenario. In the right panel, the breakdown of losses by sector at risk accounts only for losses above the baseline, i.e. arising only from the transition risk shock. Loss estimates take into account direct contagion, including second-round effects, as well as indirect contagion arising from overlapping holdings of depreciating assets. Baseline losses are the estimated losses in a scenario where probabilities of default are not stressed.

In the first scenario, losses from a one-notch downgrade triggered by climate risk could be severe for the affected sectors, but losses only lead to systemic stress if downgrades are multi-notch. For a one-to-two notch downgrade, banking system losses are estimated to increase by up to 60%. However, should a disorderly transition lead to a several-notch downgrade, losses within the euro area banking system are estimated to double, leading to a potential for financial instability (see Chart A, left panel). The energy-intensive sector22 – including e.g. mining of metals, goods manufacturing, etc. – alone contributes about half of the additional losses arising from transition risk, which is significantly more than any other sector (see Chart A, right panel).

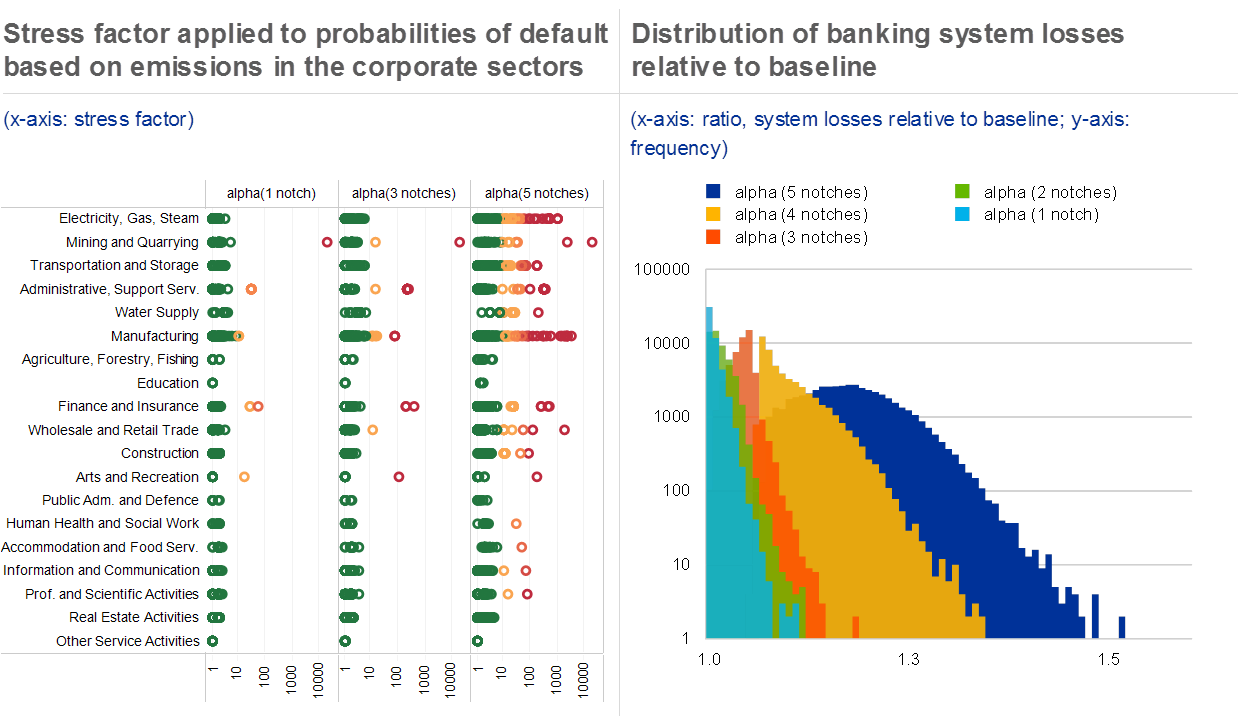

In the second scenario, while diversified exposures should shield the banking sector from large losses for the highest-emitting firms within sectors, losses could still be meaningful. Company-level data23 indicate a wide degree of dispersion of carbon transition risk within the non-financial sectors (see Chart B, left panel). Applying shocks proportional to each firm’s emissions rather than for a sector as a whole, losses in the banking system are estimated to increase by up to 10% for shocks corresponding to one-notch downgrades. In the individual firm-level exercise, system-wide losses amount to system distress only for downgrades of four notches or more (see Chart B, right panel). In the firm-level exercise, even for the highest levels of shock considered, losses within the banking system are therefore much more contained compared with the sector-based analysis. Clearly, banks with concentrated lending portfolios in particular sectors would face higher losses.

Restricting rating downgrades based on firms’ level of emissions suggests lower banking sector losses

Sources: Moody’s and ECB calculations.Notes: Stresses to probabilities of default at firm level are obtained as a function of each corporation’s emissions and a sensitivity parameter . The connection with the sectoral analysis is made based on the resulting mean stressed probabilities of default, so that for a given average probability one can find a corresponding value of . Then, refers to the level of giving the equivalent average probability across the sample as in the case of -notch downgrades in the sectoral analysis. Left panel: one-digit NACE sector classification. Sectors are placed in order based on their average emissions. The x-axis shows the factor by which probabilities of default are increased given the emissions-based downgrade. Right panel: losses relative to baseline for levels of comparable to one-to-five notch downgrades in the sectoral analysis.

This analysis provides a rationale for using firm-level information to assess the sensitivity of the banking system to downgrades related to decarbonisation. The differences in findings between the sectoral and firm-level approach to considering the carbon sensitivity of non-financial firms also indicate that the potential losses for the banking system could be reduced by implementing a targeted management of exposures to specific firms, rather than restructuring whole sectoral portfolios.

- [1]The approach is based on granular loan and securities holdings data matched to individual business information to consider the impact of both first-round direct losses incurred by individual banks and some second-round effects propagating through interbank loan networks. See Covi, G., Montagna, M. and Torri, G., “Economic shocks and contagion in the euro area banking sector: a new micro-structural approach”, Financial Stability Review, ECB, May 2019.

- [2]The identification of climate-sensitive sectors is based on Battiston, S., Mandel, A., Schuetze, F. and Visentin, G., “A Climate Stress-Test of the Financial System”, Nature Climate Change, Vol. 7, March 2017. The authors remap all four-digit NACE Rev. 2 sectors to new climate policy-sensitive sectors, combining criteria such as carbon emissions, the role of the sectors in the supply chain and the existence of traditional policy institutions for the sector.

- [3]See Financial Stability Review, ECB, November 2019, Section 3.1.