Crypto-assets – trends and implications

June 2019

The subject of crypto-assets is one of excitement and speculation. Will their value increase in the future? Are they a safe investment option? Are they a viable alternative to cash?

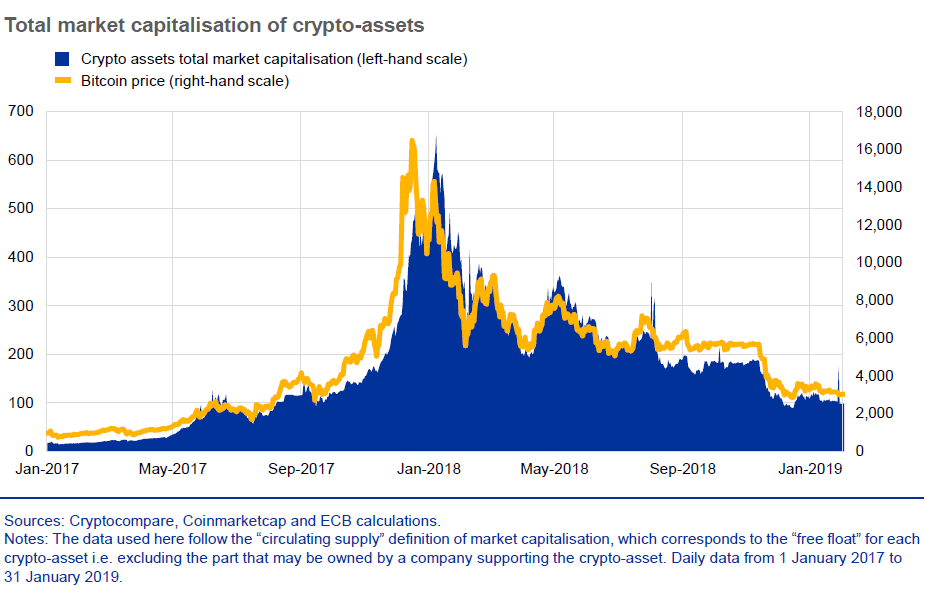

Following a period of substantial public interest, the market capitalisation of crypto-assets reached an all-time high of €650 billion in January 2018.Thereafter, it declined, standing at €96 billion just a year later (see Chart 1). Today, the combined value of crypto-assets is still small relative to the financial system and their linkages to the financial sector are limited. The current value of crypto-assets is estimated at 1.2% of the euro area M1 monetary aggregate and 0.8% of the M3 monetary aggregate.

Chart 1

Significant decrease in market capitalisation of crypto-assets from peak in January 2018

The ECB actually first started to explore trends in crypto-assets back in 2011 and published its first report on virtual currency schemes in 2012, followed by a second one in 2015. In the light of the recent increase in market interest, the ECB set up an internal task force to develop a common understanding of crypto-assets and assess their potential impact on some of its core areas of responsibility: monetary policy, financial stability, payments and market infrastructures.

“Our aim is to build a collective capability to understand, monitor and manage crypto-assets in the ECB. We need to get familiar with the underlying technology, analyse the use cases and see how they fit into the current regulatory framework,” explained Mehdi Manaa, Deputy Director General of Market Infrastructure and Payments, and Chair of the ECB Crypto-Assets Task Force. The conclusions of the task force’s analysis are set out in a dedicated Occasional Paper.

What is a crypto-asset?

There is no universal definition, but there is often some overlap between the commonly used terms, such as “crypto-asset”, “crypto token”, “crypto currency” and “virtual currency”. For the purpose of its analysis and assessment, which is summarised below, the ECB Crypto-Assets Task Force defined a crypto-asset as “a new type of asset recorded in digital form and enabled by the use of cryptography that is not and does not represent a financial claim on, or a liability of, any identifiable entity”. The emergence of crypto-assets has been facilitated by distributed ledger technology (DLT). However, their distinctive feature is the lack of an underlying claim, which makes them highly volatile and speculative.

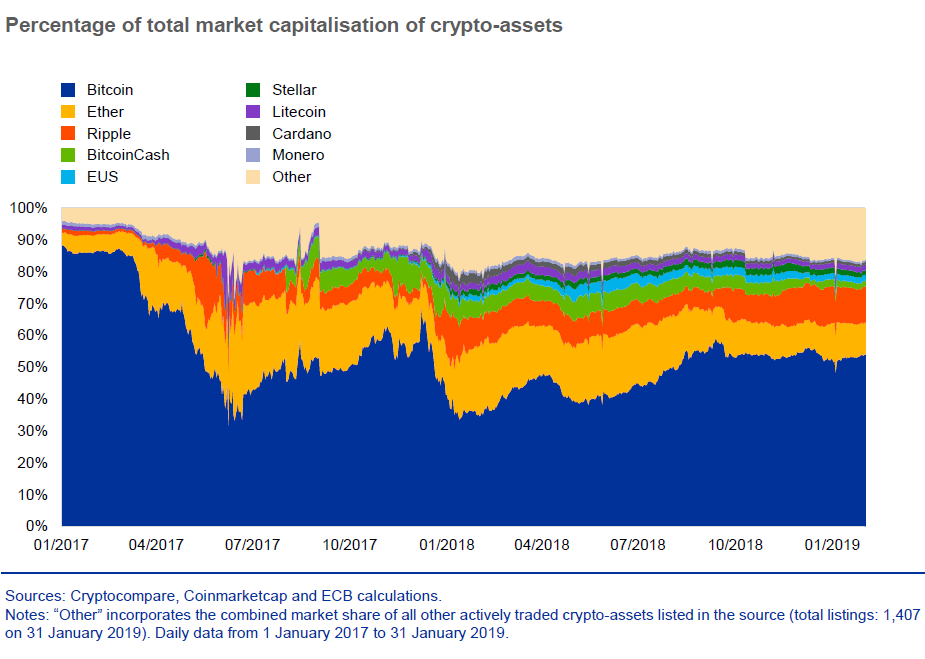

There are around 1,900 crypto-assets available on the market today. Some of the more popular ones include Bitcoin, Ether, Ripple and BitcoinCash (see Chart 2).

Chart 2

Bitcoin market share in crypto-assets currently at 54%

What are the implications for monetary policy and financial stability?

The Task Force’s analysis concluded that, at the moment, crypto-assets do not fulfil the three main functions of money, namely as a medium of exchange, a unit of account and a store of value. Their prices are still very volatile and they are not widely accepted by merchants as a means of payment. Consequently, they are not a credible substitute for cash and deposits.

Since the crypto-assets sector is still small, with very limited linkages to the wider financial system, crypto-assets neither entail significant implications for monetary policy, nor pose a material risk to financial stability in the euro area. Nevertheless, the sector requires continuous monitoring owing to its dynamics. It is important to be sufficiently prepared for a scenario in which the crypto-assets ecosystem could thrive and have an impact on the wider financial ecosystem.

What about payments and market infrastructures?

Crypto-assets in the settlement layer

Under the current regulatory framework, crypto-assets cannot be used to conduct money settlements in financial market infrastructures. The Principles for financial market infrastructures as defined by the international standard-setting bodies, the Committee on Payments and Market Infrastructures and the International Organization of Securities Commissions, and as transposed into EU legislation require the use of central bank money for settlement where practicable and available, and commercial bank money in all other cases. Therefore, being neither central bank money nor commercial bank money, crypto-assets cannot be used to carry out settlement in financial market infrastructures. Moreover, crypto-assets, as defined by the ECB Crypto-Assets Task Force, cannot be settled by central securities depositories because they do not qualify as transferable securities under the European Central Securities Depositories Regulation.

An operator of a financial market infrastructure has the flexibility to revise its risk-based participation requirements in the event that a participant involved in crypto-asset activities poses a threat to the system and its other participants. For instance, the Eurosystem, as an operator of TARGET2, is in a position to revise the TARGET2 Guidelines and to terminate participation on grounds of prudence. Should participants engage in crypto-assets activities to the point of raising concerns about the safety of the market infrastructure, this mechanism would allow the Eurosystem to keep it safe and sound.

Crypto-assets in the clearing layer

At the moment, central counterparties (CCPs) based in the EU cannot provide clearing services for crypto-asset based products because they are not qualified as financial instruments either by the national competent authorities or the European Securities and Markets Authority. Even if CCPs were authorised to clear crypto-asset based products, they would need to comply with the demanding risk management requirements set out in the European Market Infrastructure Regulation, which would make it difficult or impracticable. Furthermore, CCPs are not permitted to use crypto-assets as collateral because they are not on the list of eligible collateral under the Commission Delegated Regulation (EU) 2016/2251.

Conclusion and future developments

All in all, the risks from crypto-assets being used in financial market infrastructures are considered to be limited and manageable within the current EU regulatory and oversight frameworks. Depending on how regulation develops in the future, it may be easier for crypto-assets to be used in financial market infrastructures, leading to a deterioration in their risk profile. The ECB is committed to continue monitoring this trend, raising awareness and ensuring preparedness for potential adverse scenarios, in cooperation with other relevant authorities.