Published as part of the Macroprudential Bulletin 19, October 2022.

Against the backdrop of increasing interest rates in the euro area, it is important to understand how household LSTI ratios could be affected. To answer this question, it is useful to recall that at a given point in time the LSTI ratio consists of two payment parts: the amortisation of the loan principle and the interest payment on the outstanding loan balance: .

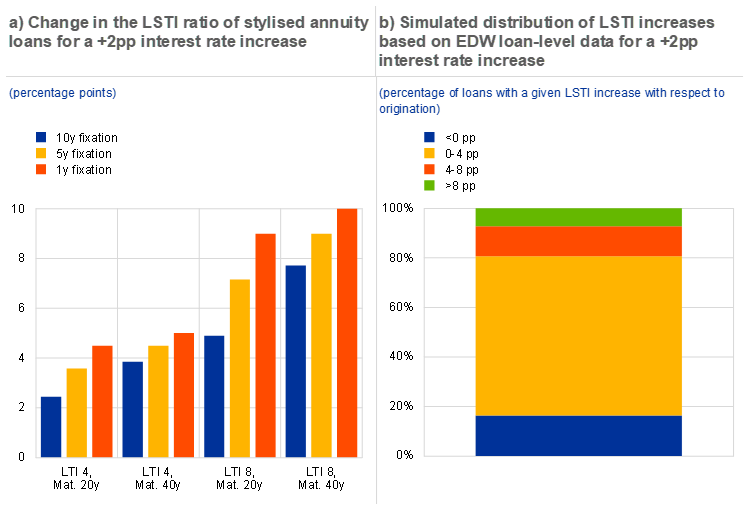

Factors that influence the LSTI interest rate sensitivity include the initial loan-to-income (LTI) ratio, the loan maturity, the interest rate fixation period and the initial interest rate. The definition of the LSTI ratio above suggests that the higher the LTI ratio at the time of interest rate resetting, the higher the LSTI sensitivity will be to a given interest rate increase.[1] In turn, the LTI ratio at the time of interest rate resetting will be higher: (1) the higher the LTI ratio at origination; (2) the lower the amortisation rate, which will depend on the loan maturity;[2] and (3) the less time that has elapsed since the loan origination, which is determined by the interest rate fixation period.[3] All three factors give rise to a higher outstanding loan balance when repricing takes place and therefore result in a larger LSTI increase for a given change in the interest rate (Chart A, panel a). Finally, a lower interest rate at origination will lead to a higher LSTI interest rate sensitivity for a given market rate, as the change in the interest rate at the time of repricing will be larger.

Given the heterogeneous impact of interest rate changes on LSTI ratios depending on the underlying lending standards, loan-level simulations are crucial to detect pockets of vulnerabilities. Simulations based on aggregate data will not be meaningful for identifying vulnerabilities, as the aggregate household debt-to-income ratio (~1 in the euro area) is many times lower than LTI ratios at the micro level (with values that are usually between 2 and 8). Although comprehensive loan-level data for households are not available for the euro area, European DataWarehouse (EDW) data on the universe of securitised household mortgage loans can be used to gain at least a partial view of pockets of vulnerabilities. With these data, the framework outlined above allows us to simulate shocked LSTIs based on the mortgage loan characteristics, including the LTI ratio and interest rate at origination, maturity, interest fixation period and amortisation type. Chart A, panel b shows a simulated distribution of LSTI increases if interest rates increase by 200 basis points from end-2021 levels. Based on this exercise, we find that LSTI increases would be manageable for most loans but pockets of vulnerabilities exist, where LSTIs of existing loans could increase by more than 8 percentage points. The granularity of the data also makes it possible to analyse expected LSTI changes across countries and over time, or to focus on a subset of exposures.

Chart A

The initial LTI ratio, loan maturity and interest rate fixation period are key factors that influence the interest rate sensitivity of the LSTI ratio

Sources: Panel a: ECB calculations. Panel b: EDW and ECB calculations.

Notes: Panel b: Only floating rate loans originated during the period 2012-2020 are included in the chart. Change in stressed LSTI compared to LSTI at origination is shown. Data available for Belgium, Germany, Spain, France, Ireland, Italy, the Netherlands and Portugal; total weighted by GDP. The chart is based on information from securitised mortgage loans, which may not accurately represent national mortgage markets, due to a potential selection bias.

We assume a fixed interest rate until time T. For a given LTI ratio, amortisation rate and market interest rate at time T this will imply: . Clearly, the higher the LTI ratio at time T, the larger the increase in the LSTI ratio will be for a given change in the interest rate. Moreover, the lower the initial interest rate at loan origination (time 0), the larger the change in the interest rate will be at the time of resetting for a given market interest rate.

A longer maturity implies a lower amortisation rate and therefore a smaller share of initial debt that is paid back in each period.

This implies fewer periods during which a given share of the initial debt (amortisation rate) is paid back.