Business outlook surveys as indicators of euro area real business investment

Published as part of the ECB Economic Bulletin, Issue 1/2020.

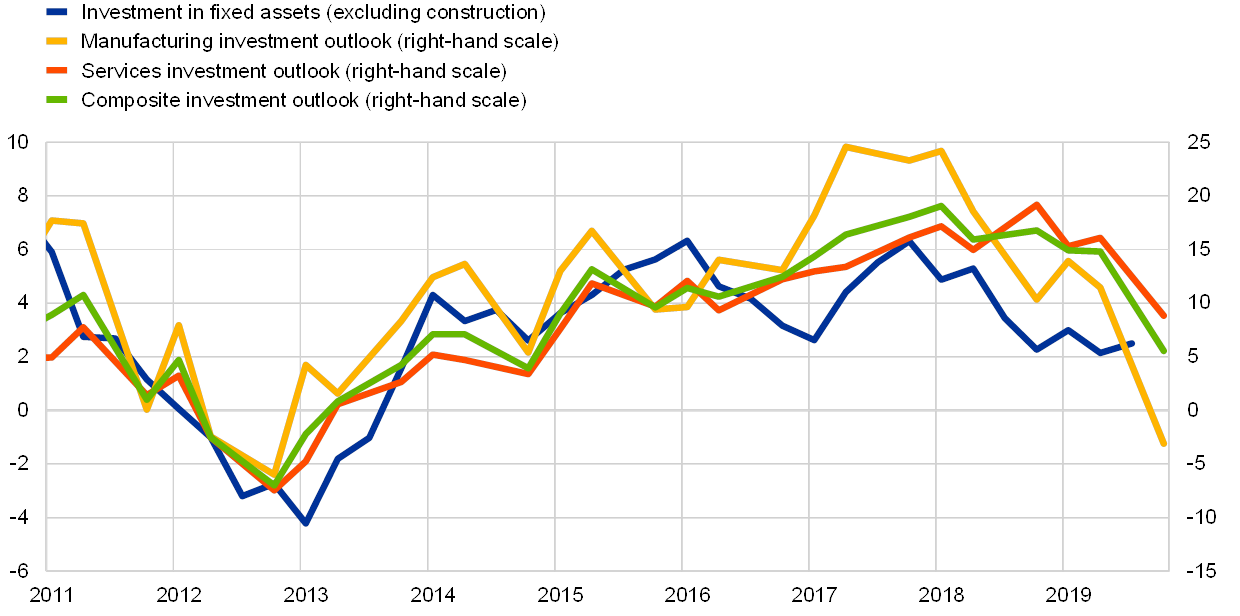

Investment survey indicators can be useful for assessing business investment developments in the euro area. The Global Business Outlook Survey on future business conditions is produced by IHS Markit on a triannual basis, with data collected in February, June and October, thus providing more timely information compared with other available investment surveys. As indicated by IHS Markit, questionnaires are sent to a representative panel of manufacturing and services sector firms, which are carefully selected to reflect the economic structure of each country in terms of sectoral contribution to GDP, regional distribution and firm size. Furthermore, its harmonised methodology allows for direct comparisons of business expectations across euro area countries, which is particularly useful for monitoring ongoing developments in business investment and policy assessments.

The outlook for manufacturing investment has deteriorated since mid-2018, indicating subdued business investment in a context of heightened global uncertainty and sector-specific challenges (see Chart A). Indicators have shown divergences in the business investment outlook across sectors over the past few years, with the sharp downward trend in manufacturing being accompanied by a delayed, and more contained, decline in the investment outlook for services. Growing uncertainty related to geopolitical events, such as Brexit and the further escalation of trade tensions, have been reported to adversely affect investment in the latest European Investment Bank’s (EIB) Investment Report and Survey.[1] The report furthermore indicates that the political and regulatory environment also appears to be weighing on the investment outlook. Moreover, muted business investment is expected owing to continued uncertainty surrounding sector-specific challenges, including those in the motor vehicle industry.

Chart A

Euro area investment outlook across sectors and real business investment

(left-hand scale: year-on-year growth rate; right-hand scale: net balance)

Sources: IHS Markit, Eurostat and ECB calculations.

Notes: Investment in fixed assets (excluding construction) represents the aggregate of the four largest euro area countries (Germany, Spain, France and Italy). Historically, they account for, on average, around 75% of the euro area-19 total business investment. The latest observations are for the third quarter of 2019 for real business investment in fixed assets (excluding construction) and October 2019 for the business investment outlook series. The net balance figure of the business investment outlook indicator is calculated by deducting the share of surveyed firms expecting a deterioration over the next 12 months from the share of respondents expecting an improvement. Net balance values vary between -100 and 100. Values above 0 therefore indicate a positive outlook amongst firms regarding business investment in the coming 12 months, while values below 0 can be interpreted as a deterioration and a value of 0 as a neutral outlook.

Business expectations available as of October 2019 point to a further deterioration in the euro area outlook for manufacturing investment in the near term. The composite investment outlook (albeit in positive territory) declined substantially in October, driven by contractionary manufacturing investment expectations (in negative territory for the first time since 2012), in parallel with a non-negligible decline in services investment expectations. This is in line with the latest evidence from the biannual European Commission’s (EC) Industrial Investment Survey, in which expectations for annual manufacturing investment growth in 2019 were revised downwards significantly in the euro area, from 4% in the April 2019 survey to -2% in November 2019.[2] According to the survey results, subdued investment is expected in most industrial sectors, with large industrial firms accounting for the downward revision to investment plans in 2019. Furthermore, according to the 2019 EIB Investment Survey, the number of manufacturing firms planning to reduce investment in 2019 had increased for the first time in the past four years.[3]

Country and sectoral-level survey results point to the German manufacturing sector as a key driver behind the waning outlook for capital expenditure. The latest Business Outlook Survey results from October 2019 suggest differences across countries and sectors, with an investment outlook that remains positive in France and Italy, while there appears to be a marked deterioration in investment expectations in Germany and Spain. Overall, business investment in the euro area is expected to remain supported by the services sector, somewhat buffering the decline in manufacturing investment (see Chart B, left-hand panel). The outlook for R&D investment is also heterogeneous (see Chart B, right-hand panel). However, survey indicators have been broadly declining in recent survey waves, both across countries and sectors, with the latest results suggesting a rather subdued picture overall. Looking ahead, the EC Industrial Investment Survey suggests a somewhat better euro area investment outlook for 2020 compared with 2019, returning to positive territory, albeit still at a slow pace.

Chart B

Business outlook for capital expenditure and investment in R&D across countries and sectors

(left-hand panel: business outlook for capital expenditure; right-hand panel: investment in R&D; net balance)

Sources: IHS Markit and ECB calculations.

Notes: ES services data are not available. The latest observation is for October 2019.

- See the EIB Investment Report 2019/2020: accelerating Europe's transformation and the 2019 EIB Investment Survey.

- See EC business and consumer surveys.

- See the EIB Investment Report 2019/2020: accelerating Europe's transformation.