Fiscal rules in the euro area and lessons from other monetary unions

Published as part of the ECB Economic Bulletin, Issue 3/2019.

This article compares the fiscal rule framework in the euro area with the frameworks in the fiscally more integrated United States and Switzerland, with the aim of drawing lessons for ways in which fiscal rules could be reformed in European Economic and Monetary Union (EMU). Both the United States and Switzerland have a history of balanced budget rules that help stabilise government debt in individual states/cantons at moderate and broadly comparable levels. The recent shift towards balanced budget rules in the euro area is an important achievement in this direction, and has contributed to better average underlying budgetary positions. Still, the fiscal rule framework needs to be rendered more effective in reducing high levels of government debt and their dispersion across the euro area. Reducing the heterogeneity of government debt positions is also an important prerequisite for setting up a well-governed common macroeconomic stabilisation function at the centre of EMU in case of deep economic crises. This in turn would help to contain the procyclicality of fiscal rules at the country level.

1 Introduction

In European Economic and Monetary Union (EMU), the single monetary policy is complemented by fiscal policies that are under the responsibility of national governments. These budgetary policies are subject to a common set of fiscal rules and country-specific arrangements. After the recent financial and economic crisis, which followed a period of good economic times that were not used sufficiently to build up fiscal buffers, the EU’s common fiscal framework was strengthened. Among other things, the measures introduced placed a stronger focus on reducing government debt ratios to sound levels. They also included a fiscal compact, which contains a close-to-balance provision for countries’ medium-term budgetary objectives (MTOs). Countries must transpose this into national law, preferably at constitutional level.

While work to further improve the functioning of EMU continues, progress towards more fiscal integration has so far been limited.[1] The statement issued following the Euro Summit of October 2014 said that “closer coordination of economic policies is essential to ensure the smooth functioning of the Economic and Monetary Union” and pointed to the importance of preparing “next steps on better economic governance in the euro area”. Subsequently, the “Five Presidents’ Report”, issued in 2015, laid out proposals for completing EMU. It stressed that “Progress must happen [..] towards a Fiscal Union that delivers both fiscal sustainability and fiscal stabilisation”.[2] This reflects the fact that, unlike other monetary unions, EMU is not equipped with a sizeable federal budget. There is thus no separate and centralised budget in place that could be used to support fiscal stabilisation of the euro area economy in deep economic downturns. The Euro Summit of December 2018 mandated the Eurogroup “to work on the design, modalities of implementation and timing of a budgetary instrument for convergence and competitiveness [..]”, but did not ask for work on a central capacity for stabilisation.[3]

This article aims to draw lessons for the design of fiscal rules in the euro area from the fiscal rule frameworks that are in place in other, fiscally more integrated monetary unions. Specifically, it looks into the fiscal rules that are in place in the United States and Switzerland, which are examples of monetary unions with a federal structure, fiscal rules at the federal and sub-federal levels and a sizeable budget at the centre. Importantly, these monetary unions differ from the euro area in that they are also political unions, in the sense of being a single nation or federal state.

The findings show that the increased emphasis in the euro area countries on balanced budget rules has brought EMU closer to the set-up in the United States and Switzerland. These countries have a long history of balanced budget rules at the sub-federal levels, which has led to, overall, lower and less diverse government debt ratios than in the euro area. To achieve a comparable outcome, the EU’s fiscal framework still needs to be rendered more effective in reducing high national government debt burdens. This would make the countries in question less vulnerable to economic downturns and the euro area as a whole more resilient. However, balanced budget rules may make it more difficult for governments to use fiscal policy in a sufficiently countercyclical manner, particularly in deep economic downturns. In other monetary unions, such rules at the sub-federal levels are accompanied by the possibility to stabilise the economy from the centre or, to a lesser extent, through “rainy day” funds at the sub-federal level.

This article is structured as follows. Section 2 takes stock of the main fiscal rules governing fiscal policies in the euro area. It concentrates on the fiscal rules established at the country level and how they are linked with the common EU governance framework. Section 3 describes major fiscal developments since the crisis with a view to identifying whether the strengthening of the fiscal governance framework has had a perceptible impact. Section 4 captures major features of the fiscal rule frameworks that govern budgetary policies in the United States and Switzerland. On the basis of this analysis, Section 5 aims to inform the discussions on how to deepen EMU and how to rectify the shortcomings of the existing fiscal framework. Section 6 concludes.

2 Fiscal rules in the euro area

Fiscal rules are an essential part of the fiscal frameworks needed to achieve sound public finances. Sustainable fiscal positions are particularly important in a monetary union, as individual countries cannot use monetary and exchange rate policies to respond to country-specific shocks. Furthermore, as the recent European sovereign debt crisis has demonstrated, unsound fiscal positions in one country can lead to spillover effects on others, thereby affecting the monetary union as a whole. Numerical fiscal rules are widely accepted as supporting the achievement of sound fiscal policies and are therefore essential to ensure sustainable public finances. Moreover, their positive impact on public finances can be further strengthened through market discipline (see Box 1). As the experience with the sovereign debt crisis has shown, insufficient compliance with fiscal rules in favourable times may come at a high cost. If fiscal rules allow too little flexibility in recessions, however, they may constrain countries´ ability to stabilise their economies during an economic downturn. This is likely to be the case especially for countries that have not built up sufficient fiscal buffers. It is therefore important that fiscal rules ensure that fiscal policies are sufficiently countercyclical over the business cycle.[4] This calls for structural fiscal rules that correct for the impact of cyclical developments. Beyond this, however, some form of effective risk sharing, for example through a fiscal capacity at the centre of a monetary union, appears necessary to combat deep economic recessions.[5]

The rationale for fiscal rules is well established in the literature. Their main objective is to constrain the use of policy discretion in order to promote sound budgetary policy-making and to overcome the tendency of governments to allow deficit and debt levels to increase over time (known as the “deficit bias”). Numerical fiscal rules are defined for the purposes of this article as providing a permanent constraint on fiscal policy as expressed in terms of a summary indicator of fiscal performance, such as the government budget deficit, debt or a major budgetary component.[6]

Fiscal policies in the euro area countries are governed by supranational as well as national fiscal rules. For example, at the supranational level, the euro area countries are subject to nominal fiscal rules under the EU’s Stability and Growth Pact (i.e. the Maastricht Treaty’s 3% deficit-to-GDP and 60% government debt-to-GDP limits). They are also required to achieve and maintain their country-specific MTOs, which are defined in terms of the structural balance. The structural balance is a key indicator for the governance framework in the euro area and reflects a country’s underlying budgetary position, which filters out the impact of the business cycle and one-off factors on the headline budget balance. Adherence to these supranational fiscal rules is governed by the preventive and corrective arms of the Stability and Growth Pact. Unlike in other monetary unions, such as the United States and Switzerland (see Section 4), the supranational rules apply to national fiscal policies and not to a federal budget. At national level, today’s fiscal rules in the euro area are to a large extent determined by the fiscal compact, which entered into force in 2013.[7] The fiscal compact requires countries to have a rule in place to ensure a balanced general government budget in structural terms over the medium term and a correction mechanism to be automatically triggered in the event of significant deviations from the fiscal target. This rule is to be transposed into national legislation, preferably at constitutional level. In addition, several countries have also their own specific rules framework in place.

Over the past 20 years the number of national fiscal rules in place has approximately tripled in the euro area countries, reflecting in particular an increase in balanced budget rules. Whereas at the beginning of the century there were only around 20 national fiscal rules altogether in the euro area countries, the number has now increased to 62, according to the European Commission’s fiscal rules database (see Chart 1). Countries have deployed different types of numerical fiscal rules. Balanced budget rules have gained particular prominence among the euro area countries, increasing from ten in 2000 to 35 by 2017 and accounting for now almost 60% of all rules.[8] Debt rules, which existed in only three euro area countries in 2000, have also become more established over the last two decades and now account for roughly one-quarter of all rules. By contrast, expenditure rules and revenue rules play a relatively limited role in most euro area countries.

Chart 1

National fiscal rules in the euro area

(number of rules)

Sources: European Commission and ECB calculations.

Notes: The chart is based on the latest available update (2017) of the European Commission’s fiscal governance database. It includes all national fiscal rules, including those that restrict only part of the general government sector, such as the regional or municipal level.

The framework of fiscal rules has improved considerably more in qualitative terms than suggested by the increase in the number of rules alone. In many countries the fiscal rules that were in place in the earlier years of EMU have been exchanged for more sophisticated fiscal rules. In this sense, the fiscal rules have improved in at least five dimensions, i.e. in terms of coverage, strictness, plausibility, monitoring and inherent correction mechanisms. First, regarding coverage, all euro area countries now have at least one fiscal rule in place that puts a restriction on public finances at the general government level. This compares with the early years of the euro area, when a large majority of rules constrained only a small fraction of the general government sector and were sometimes linked only to regional or municipal levels. Second, rules have been strengthened in recent years by setting them at constitutional or equivalent level. This, in principle, helps to reduce the risk of short-sighted, discretionary fiscal policies, which are often seen as responsible for the accumulation of high public debt. Third, all euro area countries have at least one fiscal rule in place that is defined in structural terms and thus takes account of the impact of cyclical developments. In earlier years, countries were often constrained only by ceilings in nominal terms. Fourth, the monitoring of compliance with fiscal targets has been strengthened considerably, with independent fiscal authorities, equipped with a relatively broad mandate for surveillance, now established in all euro area countries. Fifth, although practical experience is still scarce, fiscal rules are increasingly supported by more credible enforcement mechanisms, which in some cases would be triggered automatically, for deviations from fiscal targets.

Most of these improvements in national fiscal rules have taken place during the current decade, as a result of important institutional changes at the supranational level. Most important in this respect has been the requirement to fully transpose the fiscal compact into national legislation, with the aim of increasing national ownership of the EU governance framework. This can be considered a regime shift compared with the beginning of EMU, when countries’ national fiscal rules were designed independently of each other.[9] The Budgetary Frameworks Directive, as part of the “six-pack” legislation of 2011, also required country-specific numerical fiscal rules. Moreover, in 2013 the “two-pack” Regulations specified that independent fiscal institutions should take on a more prominent role in monitoring fiscal rule compliance at national level.

As a result, national fiscal rules have become more similar across countries and are better aligned with the EU governance framework at supranational level. All euro area countries now have a balanced budget rule in place restricting the general government budget, following the institutional changes mentioned above. Moreover, the provisions in several euro area countries include an explicit reference to the Stability and Growth Pact. Some countries have de jure even stricter features than foreseen in the Pact, mostly because of a stronger automaticity of their enforcement mechanisms. At the same time, fiscal rule frameworks continue to differ across countries, mainly reflecting national preferences and different federal structures. Differences also relate to the national ownership of the fiscal rules and their effectiveness in terms of compliance.

Box 1 Rules, markets and fiscal discipline in a monetary union

There are in principle two mechanisms for curbing unsound fiscal policies: a rule-based fiscal governance framework and market discipline. The respective roles of fiscal rules and market discipline are part of the ongoing discussion on the reform of the EMU governance framework.[10] Drawing on the academic literature, this box discusses the two mechanisms and also their potential interaction.

A rule-based governance framework requires in principle two components, namely rules for fiscal policy and a means for their implementation. Fiscal rules typically take the form of numerical limits on budgetary aggregates (see Section 2). Government fiscal policies have to be assessed and their compliance with the fiscal rules ensured. The effectiveness of this process depends critically on the independence of policy assessment and powers of enforcement.[11] In EMU, the European Commission and the ECOFIN Council conduct surveillance of Member States’ budgets with the aim of preventing deficit biases. Additionally, independent fiscal institutions at the national level (“fiscal councils”) assess compliance with national fiscal provisions (see Table A, left-hand column).

The rule-based fiscal framework in EMU has drawn criticism primarily for its lack of enforceability and complexity. First, where governments retain sovereignty over their fiscal policies, it can be difficult to ensure that they abide by previously agreed rules.[12] Some of the academic literature refers to the Stability and Growth Pact as a “failure”, given the significant number of violations of its numerical fiscal rules that have gone unsanctioned.[13] Second, the success of a rule-based framework critically depends on simplicity, particularly when its enforcement depends on public scrutiny and political pressure. In EMU, the Stability and Growth Pact started with simple numerical limits for deficit and debt. The framework was then reformed and a degree of flexibility was included in the implementation of the rules in order to better account for cyclical developments, the cost of structural reforms and crisis-related, exceptional fiscal burdens.[14] This has come at the cost of less transparency and tractability.

However, empirical analyses find that rule-based fiscal governance frameworks do have a noticeable constraining effect on fiscal policies.[15] In the absence of robust enforcement mechanisms, fiscal rules rely on broad political and public support. Accordingly, “ownership” of fiscal rules is often identified as an important determinant of their effectiveness.[16] While there have been many violations of the numerical fiscal rules of the Stability and Growth Pact in EMU, average deficits have declined considerably compared with the pre-EMU period. The convergence towards agreed MTOs in many countries or the clustering of public deficits just below the 3% threshold in others provides some indication that Member States have internalised at least part of the EU’s rule-based fiscal governance framework in their fiscal policymaking systems.[17] Recommendations for consolidation under the excessive deficit procedure are translated into government fiscal plans almost in full and are implemented to a substantial extent.[18]

Turning to market discipline, this is defined as a mechanism by which governments are steered by market price signals towards sound fiscal policies, thus reducing the risk of future debt restructuring. This mechanism relies on financial markets taking into account fundamentals (current and expected fiscal policies) when determining the credit risk premia included in governments’ financing costs. Governments tend to adjust their budgets to changes in the risk premium paid on their debt.[19] It is widely accepted that for this mechanism to work there has to be – among other conditions, such as open markets and transparency of policies – some likelihood that the debt of governments pursuing unsound fiscal policies will not be repaid (see Table A, right-hand column).[20] In EMU, this is embedded in the “no-bailout clause” (Article 125 of the Treaty on the Functioning of the European Union).

The market discipline mechanism has been characterised as being “too slow and weak or too sudden and disruptive”.[21] First, in a monetary union – where close economic integration implies greater spillover effects in a crisis – there could be considerable incentives for the union to come to the aid of a member state at risk of losing market access. If a commitment not to bail out a member state is not fully credible, this could compress risk premia for governments.[22] Second, the literature finds that market interest rates do not necessarily reflect news on fiscal developments in a reliable and consistent manner, and prices can overreact, particularly in times of economic crisis.[23] It is argued that in EMU this may have contributed, on the one hand, to excessively loose fiscal policies before the sovereign debt crisis and, on the other, to overly severe austerity measures during the crisis.[24]

At the same time, however, the literature in general does find that market discipline effectively reduces the deficit bias of governments. Research on market discipline in EMU shows that market prices reflect fiscal developments, thereby providing an indication that the no-bailout clause remains credible.[25] Studies also provide evidence that European governments effectively adjust their policies to changes in market prices.[26]

While rule-based fiscal governance and market discipline are often portrayed as two separate mechanisms, they do in fact affect each other. Typically, the literature finds that the two mechanisms reinforce each other.[27] For example, fiscal rules can help governments to credibly commit to fiscal targets and thus reduce market interest rates on public debt.[28] Moreover, the assessment of fiscal developments in the context of the fiscal governance mechanism may provide useful information to market participants for the pricing of sovereign risks.[29] Vice versa, higher market interest rates as a result of higher credit risk would, all else being equal, lead to a deterioration of a fiscal position. This may make it more difficult for countries to comply with the provisions of the governance framework.

In conclusion, both rule-based fiscal governance frameworks and market discipline appear to contribute to the constraints on fiscal policies in EMU. However, both mechanisms have limitations and vulnerabilities. Against this background, institutional changes to EMU should be carefully assessed with regard to their impact on the governance framework and the market disciplining mechanism.

Table A

Mechanisms for fiscal discipline in EMU

3 Fiscal developments in the euro area

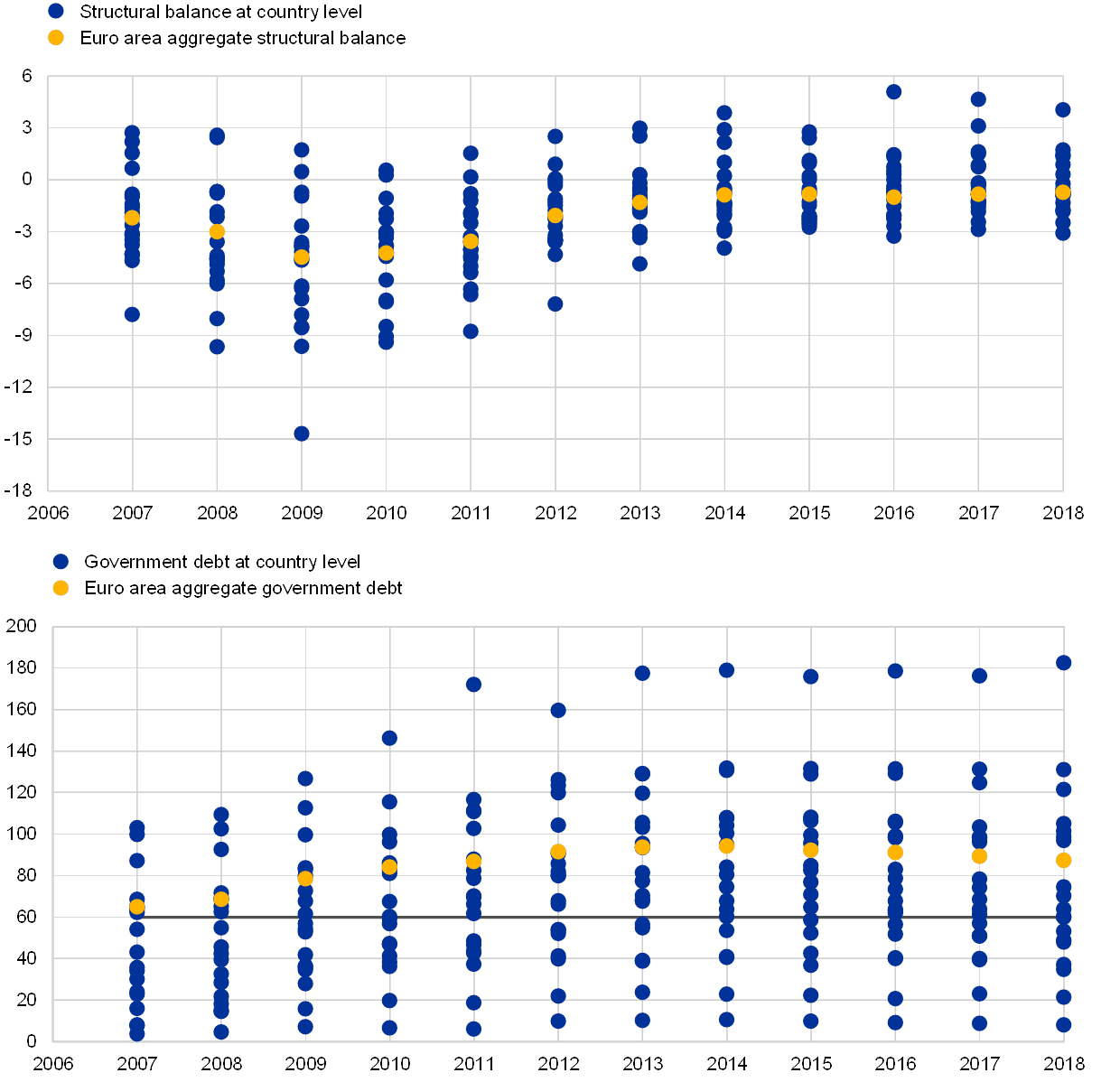

Since the peak of the financial crisis in 2009, the euro area as a whole has made significant progress towards restoring sound fiscal positions, which has coincided with the steps taken to strengthen the framework of fiscal rules. From its peak in 2009 at 4.5% of GDP, the euro area aggregate structural deficit declined to 0.7% of GDP in 2018 (see Chart 2). The euro area as a whole has thus moved to an underlying budgetary deficit that comes very close to the floor of 0.5% of GDP set by the fiscal compact. This has been an important contribution to bringing government debt in the euro area onto a downward trajectory. Indeed, the euro area aggregate debt-to-GDP ratio gradually declined from its peak of 94.2% of GDP in 2014 to 86.9% of GDP in 2018. It remains, however, far above its pre-crisis level (65% of GDP in 2007).

Chart 2

Dispersion of structural budget balances and government debt in the euro area

(percentages of GDP)

Sources: European Commission Economic Forecast, Autumn 2018, and ECB calculations.

These favourable trends for the euro area as a whole mask very heterogeneous fiscal developments at the country level. On the one hand, an increasing number of countries are assessed as recording broadly sound fiscal positions. In 2018, on the basis of the European Commission’s 2018 Autumn Economic Forecast, 11 countries are expected to have achieved structural balance positions that are in line with the lower bound set by the fiscal compact (see Chart 3). This compares with only three countries prior to the crisis in 2007.[30] This favourable trend may be taken as an indication that the increasing focus on balanced budget rules at the country level is having a first perceptible impact.[31] On the other hand, as shown in Chart 2, a number of euro area countries continue to record large structural budget deficits. These countries remain far from their country-specific MTOs and the floor enshrined in the fiscal compact, which makes it more difficult to bring their high government debt ratios down to lower levels.

Chart 3

Structural balances vis-à-vis the floor enshrined in the fiscal compact

(structural balance: percentages of GDP)

Sources: European Commission Economic Forecast, Autumn 2018, and ECB calculations.

Notes: The chart shows the number of countries whose structural balance would be in compliance with the floor set in the fiscal compact. The blue bars show the number of countries with either a government debt-to-GDP ratio above 60% and a structural balance above a floor of -0.5% of GDP or with a government debt-to-GDP ratio below 60% of GDP and a structural balance above a floor of -1%. The yellow bars depict the number of countries satisfying neither of these conditions. The number of countries complying with their country-specific MTOs may be different, however, as these can be set at levels that are more demanding than the provisions of the fiscal compact.

As can be seen from Chart 4, in some countries with high government debt (i.e. Belgium, France and Italy), structural deficits still remain far from their MTOs because, during the period from 2011 to 2018, they declined on average by less than the 0.5% of GDP benchmark adjustment foreseen in the Stability and Growth Pact. While in 2011-13 all the countries shown in Chart 4 (apart from Belgium) achieved an adjustment which was, amid financial market pressure, greater than the benchmark requirement, in more recent years none of the countries shown achieved the required adjustment. Consequently, these countries were not building the buffers that would allow them to avoid fiscal tightening in the next downturn. This can have an impact on the resilience of the euro area as a whole.

Chart 4

Structural budget balances in countries not at their MTO and with government debt- to-GDP ratios above 90%

(percentage points)

Sources: European Commission Economic Forecast, Autumn 2018, and ECB calculations.

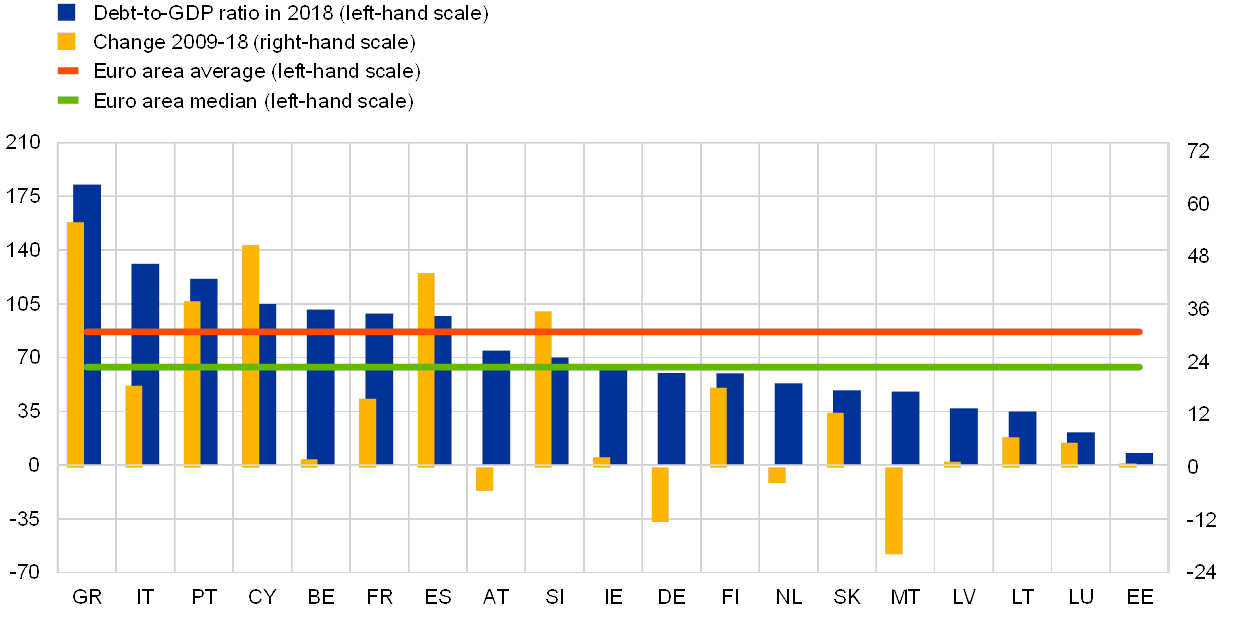

Heterogeneity in euro area countries’ fiscal positions is also visible in the dispersion of government debt-to-GDP ratios. This has increased to levels markedly above those seen ahead of the crisis (see Chart 2). In fact, since 2009 an increasing number of euro area countries have posted government debt-to-GDP ratios of above the Maastricht Treaty’s 60% reference value. While, by 2018, some countries’ debt ratios had declined to below 60% of GDP again, a number continue to record high government debt ratios of above 90% of GDP (see Chart 5). Ensuring convergence towards sound fiscal positions across countries and thus reducing vulnerabilities to shocks is a prerequisite for resilience in the euro area, and thus an important factor to support a fiscally more integrated EMU.

Chart 5

Developments in government debt

(left-hand scale: percentage points of GDP; right-hand scale: percentages of GDP)

Sources: European Commission Economic Forecast, Autumn 2018, and ECB calculations.

4 Fiscal frameworks in other monetary unions

Comparing the public finances and fiscal frameworks of the euro area, the United States and Switzerland reveals some similarities but also important differences. As in the euro area countries, balanced budget rules at the sub-federal level are well established in both the US states and the Swiss cantons, although they have been in place for a much longer period than in the euro area. However, the size and role of the central budget differs substantially between the euro area on the one hand and Switzerland and the United States on the other. This includes the stabilisation function of the central budget, which can limit the procyclicality of fiscal rules at the lower level. A better understanding of the institutional settings in these two monetary unions and how they compare with the situation in the euro area may therefore provide insights, particularly in view of the ongoing discussions on how to deepen fiscal integration in EMU. This section therefore takes a closer look at how public finances are governed in the United States and Switzerland, with a particular focus on the design, strictness and enforcement mechanisms of fiscal rules at sub-federal level.

Public finances in the United States and Switzerland differ from those in the euro area. In the United States, most of the overall general government debt, which has continuously increased over the past decades, has been generated at the federal level (see Chart 6). In Switzerland, the federal level is responsible for roughly half of total public debt, which peaked in 2005 (see Chart 7). In the euro area, there is no equivalent at the central level besides the EU budget, which is very limited in size and also has a very limited borrowing capacity. Moreover, neither in the United States nor in Switzerland is public debt at the sub-federal level as heterogeneous as across countries in the euro area (see Chart 8 and Chart 5).

Chart 6

Decomposition of general government debt in the United States, 1980-2018

(percentages of GDP)

Sources: Haver Analytics and ECB calculations.

Chart 7

Decomposition of general government debt in Switzerland, 1990-2017

(left-hand scale: CHF billions; right-hand scale: percentages of GDP)

Sources: Swiss Federal Statistical Office and ECB calculations.

Notes: The data on the general government debt-to-GDP ratio include the debt accumulated by the social security systems.

Three institutional aspects seem to play a particular role in explaining the differences in public finances across the monetary unions. First, differences relate to fiscal federalism, its main purpose and how strongly it is established in the respective monetary unions.[32] In the United States, fiscal federalism mainly takes the form of countercyclical stabilisation policies, from the centre to the state level. The US states can rely on some public risk sharing in the form of temporary transfers from the federal budget in the event of idiosyncratic shocks, complemented by “rainy day” funds established at state level (see also Box 2).[33] In Switzerland, fiscal federalism is well established in the form of a permanent transfer system between the centre and economically less strong cantons. In the euro area, however, fiscal federalism is very limited. The EU budget has very limited resources (of around 1% of total GDP), which are mainly used for redistribution purposes in the form of EU cohesion funds to foster economic convergence in poorer regions. Public risk sharing is still limited to very specific situations under strict conditionality, while there are no funds available at central level to provide a countercyclical stabilisation function for the Member States in the event of severe common or asymmetric shocks. Second, in the US states and the Swiss cantons public finances are also strongly influenced by an effective no-bailout clause.[34] Third, differences relate to the fiscal rule framework for the various layers and how effectively it works as a disciplinary device. While these three aspects are largely interrelated, and therefore all affect the cyclicality of fiscal policies, the focus in the following will be on the fiscal rules.

Chart 8

Dispersion of public debt in US states and Swiss cantons, 2016

(percentages of GDP)

Sources: Haver Analytics, Swiss Federal Statistical Office and ECB calculations.

Notes: The charts show the 2016 government debt-to-GDP ratio of the 50 US states, excluding debt at local level, and the 26 cantons, excluding debt of municipalities.

The fiscal rules in the US states are not imposed by the centre and are therefore relatively heterogeneous. The US states have full discretion in the way they set their fiscal rules. Although balanced budget rules are in place in almost all 50 states, they differ in terms of stringency. A few states have very stringent balanced budget rules which prohibit deficits being carried over into the next budget year. Other states allow more leeway during the budgetary process, for example in form of escape clauses, and compliance with rules is enforced rather loosely. In some US states the balanced budget rules just need to be complied with ex ante, while in others investment expenditure can be deducted from nominal targets, thereby providing accounting leeway. Fiscal targets are set in either annual or biennial terms. Public finances in the US states are also disciplined by a no-bailout clause, while fiscal stabilisation from the centre to the states and rainy day funds help as countercyclical devices.[35] At the federal level, the government’s borrowing capacity is restricted by a nominal debt limit, which can, however, be lifted upon parliamentary approval.

In Switzerland, the fiscal rules, which are autonomously set by the cantons, are relatively diverse. Most of the 26 cantons have balanced budget rules in place, some of which are established at constitutional level. Only a few cantons target their total cantonal budgets, while in several cantons public investment is explicitly excluded.[36] Some cantons strictly enforce compliance with their fiscal targets. For example, if the budget deficit exceeds a certain threshold, they are obliged to either increase taxes (e.g. in St. Gallen) or to specify future expenditure cuts ex ante. Rule compliance is partly also promoted through direct democratic instruments of budget control, such as referendums. Other cantons, however, have fiscal rules that are less stringent, for example with broadly defined escape clauses. At the federal level, fiscal discipline is ensured through a strict debt brake established in 2003 at constitutional level, which applies to the general government sector as a whole.

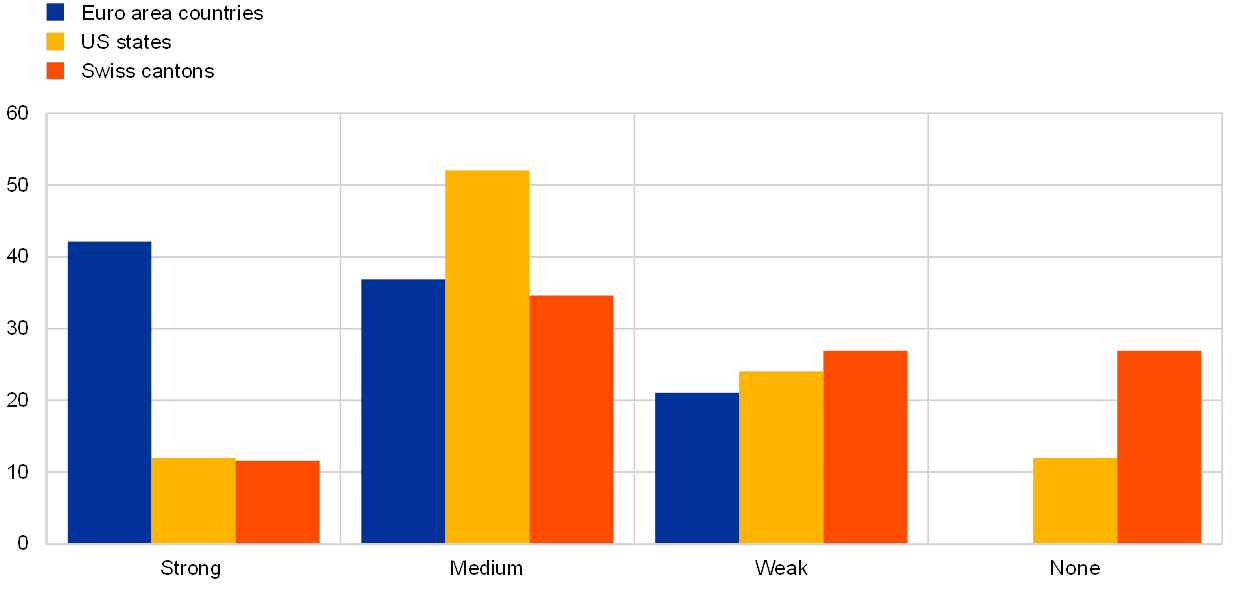

The differences in the fiscal rule frameworks of the euro area, the United States and Switzerland can be captured by a rule stringency index. As shown in Chart 9, this is a simple composite index based on publicly available indices for the three monetary unions. These are, for Switzerland, the index developed by Kirchgässner and Feld, for the US states the index developed by Hou and Smith and further by Mahdavi and Westerlund, and for the euro area countries the index of the European Commission.[37] As these studies use their own categorisation, it is necessary to translate them into a single scoring system. For reasons of simplicity and also owing to a lack of publicly available information at the same granular level across regions, the composite index shown here is closest to the index developed by Kirchgässner and Feld. Thus the composite index is derived from three criteria: (i) whether a balanced budget rule is in place, (ii) whether there is clear intra-year monitoring of the budget, and (iii) whether there is a stringent and credible enforcement mechanism. Each criterion is given a score of one, indicating that the feature is present, or zero, if not. The overall score is then found, which can be strong, medium, weak or not existent. The higher the score, the more stringent the rule.

Overall, countries’ fiscal rules in the euro area seem to be more stringent than the sub-federal rules in the other two monetary unions. On the basis of the composite index, 40% of the fiscal rules in the euro area countries are very stringent, which is a considerably higher score than for the US states or the Swiss cantons (Chart 9). In the US states, more than half of the fiscal rules in place have a medium stringency level, while those in the Swiss cantons seem to be less binding. However, the results need to be interpreted with caution as the various indices are not necessarily fully comparable since they use different criteria and considerable judgement.[38]

Chart 9

Comparison of fiscal rule stringency index

(percentages of total number of rules)

Source: ECB calculations.

Notes: The index is based on, for the euro area, the European Commission’s fiscal rules database (2017), for the United States, the fiscal rules index by Hou and Smith (2010) as well as Mahdavi and Westerlund (2011), and for Switzerland, the index by Feld and Kirchgässner (2008). It covers rules at sub-federal levels in the United States and Switzerland, and at national level in the euro area.

At first sight, the above finding that fiscal rules in the euro area are more stringent than those in other monetary unions might be surprising. Public debt in the euro area countries is on average higher and more heterogeneous than the sub-federal debt-to-GDP ratios in the United States and Switzerland. However, in contrast to the euro area countries, public finances in the US states and the Swiss cantons are able to benefit from a sizeable fiscal budget at the centre and, in the United States, rainy day funds that facilitate more countercyclical fiscal policies. Moreover, the results for the euro area can be seen as a first indication that the considerable institutional changes implemented in recent years are bearing fruit, even though their positive impact on public finances has not yet become fully visible. Furthermore, as the no-bailout clause is seen as being effective at the sub-federal levels in the United States and Switzerland, this may also explain why both federations allow themselves to have less stringent rules.

Box 2 Rainy day funds – evidence from US states

Fiscal rules are often criticised for being procyclical and for not providing sufficient incentives to build up fiscal buffers. During a recession, rules may provide insufficient fiscal room for manoeuvre to stabilise the economy. One possibility for smoothing the impact of the business cycle on fiscal positions is to create a “rainy day” fund. This is a fund dedicated to stabilising the budget by saving funds in economic good times and depleting them in economic weak times. This box looks at the experience in the United States with rainy day funds and a possible way forward for the euro area.

In the United States, almost all states are equipped with some form of rainy day fund as a countercyclical tool to complement the balanced budget requirements. The availability of such budget stabilisation funds is seen as important given that state governments – when faced with an economic downturn and related shortfalls on the revenue side of their budgets – have limited options for stabilising the economy, as their ability to borrow is constrained. Indeed, increasing taxes or cutting spending in a procyclical manner would risk worsening a downturn. The rainy day funds constitute an institutional feature of the budgetary procedures at state level. Their average size is relatively small. Over the period 2000-17, the funds accumulated in rainy day funds averaged only around 0.2% of US GDP, and peaked in 2017 at close to 0.3% of GDP. Chart A shows the evolution of aggregate US state rainy day fund balances over 2000-17 against developments in the output gap (as a proxy for national cyclical conditions). Indeed, as expected, the aggregated rainy day funds balance follows a roughly countercyclical pattern, in the sense that dissaving occurs when the output gap is worsening and vice versa. It is noteworthy that available funds were used almost in full during the 2001 recession and built up again thereafter, while aggregate funds dropped much less significantly during the Great Recession. Given the relatively small size of the funds, they are typically only sufficient to smooth normal cyclical fluctuations; more severe recessions require additional support from the federal budget. During the Great Recession significant funds derived from the American Recovery and Reinvestment Act at the federal level were used to further compensate state budget shortfalls.

Chart A

US state rainy day fund balances

(percentages of GDP)

Sources: National Association of State Budget Officers, European Commission (AMECO database) and ECB calculations.

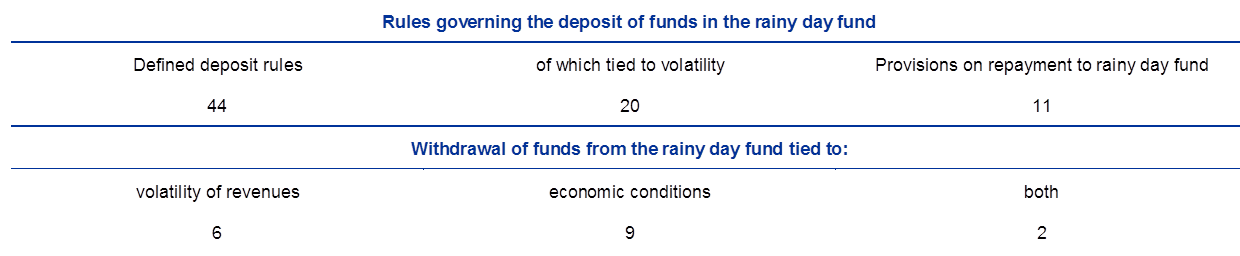

While the governance structure of rainy day funds differs widely among US states, some common patterns can be observed. As indicated in Table A, all rainy day funds are subject to specific conditions regarding the build-up and withdrawal of funds. 44 states have rules in place that make the deposit of funds in the rainy day funds dependent on a number of specified conditions; 20 states base them on measures of volatility (e.g. revenue volatility deriving from cyclical developments related to oil or housing). Nine states make the withdrawal of funds dependent on economic conditions, six on revenue volatility and two on both. Eleven states foresee a fixed period for repayment.

Table A

Rainy day funds in US states – main characteristics

(number of US states)

Source: See Bailey, S. et al. “When to Use State Rainy Day Funds”, Pew Charitable Trusts, 2017.

In the euro area, only one country has so far decided to introduce a rainy day fund. Ireland set up a rainy day fund in 2018.[39] The intention is to place around €500 million per annum (i.e. 0.2% of projected 2019 GDP) over the period 2019-21 in the fund. While Germany does not operate a rainy day fund, the German debt brake is conceptually comparable.[40] The IMF has suggested setting up a rainy day fund for the euro area as a whole to help to smooth business cycles in the event of both country-specific and common economic shocks.[41]

5 Lessons for the reform of fiscal rules in the euro area

With the increase in balanced budget rules, the fiscal rule framework in the euro area has come closer to that in the United States and Switzerland, but important differences remain. The increased reliance in the euro area countries on balanced budget rules will eventually help to bring government debt ratios to lower and less divergent levels. Though the reflection of the fiscal compact in national rules is still recent, it is thus a major achievement that should ultimately help to increase the resilience of the euro area. At the same time, an important lesson from the United States and Switzerland is that their on average much lower debt ratios at sub-federal level and lesser dispersion are the result not only of a much longer history of balanced budget rules but also of a degree of risk sharing and a fiscal stabilisation function at the central level.

The lessons for EMU are thus twofold. First, the fiscal framework needs to be rendered more effective in ensuring sound fiscal positions and reducing high levels and dispersion of government debt ratios across the euro area. As shown in Section 3, while the euro area as a whole can be considered to have achieved an underlying budgetary position of almost close to balance, some countries with high debt remain distant from such an outcome. This needs to be addressed. Second, reducing the heterogeneity of public debt positions across euro area countries would also be an important prerequisite for setting up a common macroeconomic stabilisation function at the centre in case of deep economic crises. This, in turn, would help to contain the procyclicality of fiscal rules at the country level. Against this background, the review of the “six-pack” legislation, scheduled for this year, will provide an opportunity to consider adjustments to the framework that could be conducive to further fiscal integration in the euro area.

Looking at the first lesson, shortcomings in the current application of the fiscal rules as set by the Stability and Growth Pact need to be remedied. As shown in Section 3, some countries are not building up the buffers that would allow them to avoid fiscal tightening in a downturn. This can have an impact on the resilience of the euro area as a whole, notably in the light of the absence of a central fiscal capacity.[42]

First, under the Stability and Growth Pact’s corrective arm, underlying budgetary positions need to improve faster than is currently the case. The “six-pack” legislation introduced annual nominal headline deficit targets under the excessive deficit procedure. If a country’s economic growth outpaces that foreseen in the excessive deficit procedure recommendation, it can achieve the nominal headline deficit targets with a smaller or even without the prescribed structural effort. These “nominal strategies” help to explain why, for example, Spain and France delivered a structural effort below the 0.5% of GDP benchmark requirement in the period following the 2012-13 recession (see Chart 4). Such developments harbour a risk that countries will leave an excessive deficit procedure with elevated structural deficit and debt ratios that reduce their potential to support the economy during the next downturn. This would suggest reducing the emphasis on the nominal headline deficit targets under the Stability and Growth Pact’s corrective arm.

Second, the Stability and Growth Pact’s debt rule should be reviewed to ensure a reduction of high government debt. The debt rule rightly takes account of low nominal growth and inflation as relevant factors, as these render compliance with it procyclical in a downturn. However, the current application of the rule needs to be addressed where it treats countries’ compliance with the preventive arm of the Stability and Growth Pact as the core mitigating factor. Specifically, countries that do not and/or are not expected to deliver the full structural effort towards the MTO under the preventive arm are currently still considered as being broadly compliant with the preventive arm and therefore compliant with the debt criterion. Such broad instead of full compliance with the Stability and Growth Pact delays the needed progress towards the MTO.[43]

Third, under the Stability and Growth Pact’s preventive arm, the application of flexibility needs to be reviewed to avoid an excessive slowdown in progress towards MTOs.[44] According to the common position on flexibility, which was endorsed by the ECOFIN Council in early 2016, budgetary adjustment requirements can be reduced in exchange for additional structural reforms and government investment, among other things. However, it should be ensured that the additional leeway granted is reduced if structural reforms are reversed or government investment is more limited than initially planned.

Turning to the second lesson, the experience in the United States and Switzerland suggests that rules at the level of individual euro area countries should be supported by some central stabilisation. Over the past 15 years the fiscal rule framework in the euro area has been reformed, with, overall, a shift away from nominal targets and towards a stronger recognition of the impact of the business cycle on budgetary outcomes.[45] Provided the good economic times are used effectively to build up buffers, this helps to provide stabilisation in downturns. In this respect, countries could benefit from enhancing their institutional toolbox by, for example, creating rainy day funds that could limit procyclical fiscal policies. Over the longer horizon, however, setting up a well-governed central stabilisation facility would support adherence to the strengthened fiscal framework in the euro area in deep downturns. As the overall moderate and broadly comparable government debt ratios at the state/canton level in the United States and Switzerland show, reducing high levels and the heterogeneity of government debt positions across the euro area countries appears to be an important prerequisite in this respect.

Generally, as the experiences in the United States and Switzerland have shown, once government debt ratios are relatively low and less divergent, countries might be able to afford to set their fiscal rules more autonomously. Experience in other monetary unions suggests that market discipline can reinforce the ownership of sub-federal fiscal rules. Moreover, sub-federal entities have found effective and credible fiscal rules to be in their long-term interest because unsound fiscal policies – resulting in excessively high debt levels – place a burden on future generations by increasing financing costs in the economy and undermining growth and employment. This has also led sub-federal entities to take strong ownership of their (self-imposed) fiscal rules.

Overall, experiences with fiscal rule frameworks in other fiscally more integrated monetary unions provide insights for reforms in EMU, but differences will and should remain. As also the high and rising government debt ratio at the US federal level shows, what is generally important is that fiscal rules ensure that debt ratios are sound at all levels constituting a monetary union.

6 Conclusions

This article’s main findings can be summarised as follows. A comparison of the fiscal rule framework applicable in euro area countries with that in the fiscally more integrated United States and Switzerland can provide guideposts for completing EMU. Both the United States and Switzerland have a history of balanced budget rules that help stabilise government debt in states and cantons at moderate and not overly divergent levels. The increased emphasis in the euro area on balanced budget rules is an important achievement. The fact that the majority of euro area countries are currently recording underlying budgetary positions that are in line with a balanced budget over the medium term is also a first indication that balanced budget rules have become more effective.

Still, a number of countries, notably those with high government debt, need to progress further towards their MTOs. The fiscal rule framework can be rendered more effective in this regard. Generally, if euro area countries build up buffers to avoid fiscal tightening in a downturn, national budgets can fulfil their function as stabilisation tools. Reducing the heterogeneity of debt positions across euro area countries would also be an important prerequisite for setting up a common macroeconomic stabilisation function for deep crises as in other monetary unions, thereby also supporting the single monetary policy.

- Fiscal integration is defined, for the purposes of this article, as the partial transferral of fiscal resources and competences in the area of fiscal policy to the central level of government from the lower levels. Stronger fiscal integration can be expected to eventually result in a system of fiscal federalism (see Section 4).

- For details, see Juncker, J.-C., Tusk, D., Dijsselbloem, J., Draghi, M. and Schulz, M., “Completing Europe's Economic and Monetary Union”, European Commission, June 2015.

- For details, see the Statement of the Euro Summit, 14 December 2018.

- Moreover, it can be argued that fiscal rules may help to build up fiscal space. See for example Nerlich, C. and W. Reuter, “Fiscal Rules, Fiscal Space, and the Procyclicality of Fiscal Policy”, Finanzarchiv, Vol. 72, No 4, 2016.

- A discussion of the issue of risk sharing and the need for a fiscal capacity goes well beyond the scope of this article. For further insights, see for example the article entitled “Risk sharing in the euro area”, Economic Bulletin, Issue 3, ECB, 2018.

- In line with the widely used definition based on Kopits, G. and Szmansky, S., “Fiscal policy rules”, Occasional Paper Series, No 162, International Monetary Fund, 1998.

- The fiscal compact establishes a floor for the MTO of -0.5% of GDP for countries with debt above 60% of GDP and of -1% of GDP for countries with debt significantly below 60% of GDP. It is binding legislation for the now 24 contracting parties, including all euro area countries. See also the box entitled “Main elements of the fiscal compact”, Monthly Bulletin, ECB, March 2012.

- In addition to a balanced budget rule for general government, several euro area countries, in particular those with a federal structure, also have balanced budget rules in place that restrict only sub-national layers of public finances, including for example municipalities.

- In February 2017 the European Commission published its assessment of the fiscal compact transposition, which concluded that most contracting parties had fully transposed the fiscal compact into national legislation, although only 11 at constitutional or comparable level. See “Report from the Commission presented under Article 8 of the Treaty on Stability, Coordination and Governance in the Economic and Monetary Union”, European Commission, 22 February 2017. However, this might be a relatively generous interpretation of the transposition; see the box entitled “The fiscal compact: the Commission’s review and the way forward”, Economic Bulletin, Issue 4, ECB, 2017.

- For an example, see Bénassy-Quéré, A., Brunnermeier, M., Enderlein, H., Farhi, M., Fratzscher, M., Fuest, C., Gourinchas, P.-O., Martin, P., Pisani-Ferry, J., Rey, H., Schnabel, I., Véron, N., Weder di Mauro, B. and Zettelmeyer, J., “Reconciling risk sharing with market discipline: A constructive approach to euro area reform”, CEPR Policy Insight, No 91, 2018.

- See Wyplosz C., “Fiscal Rules: Theoretical Issues and Historical Experiences”, in Alesina, A. and Giavazzi, F. (eds.), Fiscal Policy after the Financial Crisis, University of Chicago Press, 2013, pp. 495-525, and Reuter, W. H., “When and why do countries break their national fiscal rules?”, European Journal of Political Economy, 2018, pp. 1-17.

- Few fiscal federations grant their central government direct control over the fiscal policy of their sub-national entities. See Cottarelli, C. and Guerguil, M. (eds.), Designing a European fiscal union: Lessons from the experience of fiscal federations, Routledge, 2014.

- For examples, see De Haan, J., Berger, H. and Jansen, D.-J., “Why has the Stability and Growth Pact Failed?”, International Finance, Vol. 7, No 2, 2004, pp. 235-260, or Ioannou, D. and Stracca, L., “Have the euro area and EU governance worked? Just the facts”, European Journal of Political Economy, Vol. 34, 2014, pp. 1-17.

- See the box entitled “Flexibility within the Stability and Growth Pact”, Economic Bulletin, Issue 1, ECB, 2015, and Prammer, D. and Reiss, L., “The Stability and Growth Pact since 2011: More complex – but also stricter and less procyclical?”, Monetary Policy and the Economy, Oesterreichische Nationalbank, Q1 2016, pp. 33-53.

- For a recent metaanalysis, see Heinemann, F., Moessinger, M.-D. and Yeter, M., “Do fiscal rules constrain fiscal policy? A meta-regression-analysis”, European Journal of Political Economy, Vol. 51, 2018, pp. 69-92.

- Ter-Minassian, T., “Fiscal Rules for Subnational Governments: Can They Promote Fiscal Discipline?”, OECD Journal on Budgeting, Vol. 6, No 3, 2007.

- See Kamps, C. and Leiner-Killinger, N., “Taking stock of the functioning of the EU fiscal rules and options for reform”, Occasional Paper Series, ECB, forthcoming, 2019, and “Report on Public Finances in EMU 2018”, European Economy Institutional Papers, No 095, European Commission, 2019.

- See De Jong, J. and Gilbert, N., “Fiscal Discipline in EMU? Testing the Effectiveness of the Excessive Deficit Procedure”, Working Paper Series, No 607, De Nederlandsche Bank, 2018.

- See Lane, T. D., “Market Discipline”, Staff Papers, Vol. 40, No 1, International Monetary Fund, 1993, pp. 53-88.

- See Feld, L.P., Kalb, A., Moessinger, M.-D. and Osterloh, S., “Sovereign bond market reactions to no-bailout clauses and fiscal rules – The Swiss experience”, Journal of International Money and Finance, Vol. 70, 2017, pp. 319-343.

- See Report on economic and monetary union in the European Community, Committee for the Study of Economic and Monetary Union (“Delors Committee”), April 1989.

- See Bordo, M. D., Jonung, L. and Markiewicz, A., “A Fiscal Union for the Euro: Some Lessons from History”, CESifo Economic Studies, Vol. 59(3), CESifo, 2013, pp. 449-488.

- See Bergman, M., Hutchison, M.M. and Jensen, S.E.H, “Do Sound Public Finances Require Fiscal Rules, Or Is Market Pressure Enough?” Economic Papers, No 489, European Commission, 2013, and Aizenman, J., Hutchison, M. and Jinjarak, Y., “What is the risk of European sovereign debt defaults? Fiscal space, CDS spreads and market pricing of risk”, Journal of International Money and Finance, Vol. 34, 2013, pp. 37-59.

- See De Grauwe, P. and Ji, Y., “Mispricing of Sovereign Risk and Macroeconomic Stability in the Eurozone”, Journal of Common Market Studies, Vol. 50, No 6, 2012, pp. 866-880, and Pisani-Ferry, J., The Euro Crisis and Its Aftermath, Oxford University Press, 2014.

- See Bernoth, K., von Hagen, J. and Schuknecht, L., “Sovereign risk premiums in the European Government Bond Market”, Journal of International Money and Finance, Vol. 31, No 5, 2012, pp. 975-995.

- See Rommerskirchen, C., “Debt and Punishment: Market Discipline in the Eurozone”, New Political Economy, Vol. 20, No 5, 2015, pp. 752-782. See also Afflatet, N., “Public debt and borrowing: Are governments disciplined by financial markets?”, Cogent Economics & Finance, Vol. 4, No 1, 2016.

- See Manganelli, S. and Wolswijk, G., “Market Discipline, Financial Integration and Fiscal Rules: What Drives Spreads in the Euro Area Government Bond Market?”, Working Paper Series, No 745, ECB, 2007.

- A large number of empirical studies find that the adoption of numerical fiscal rules indeed reduces government borrowing costs. See Heinemann, F., Osterloh, S. and Kalb, A., “Sovereign risk premia: The link between fiscal rules and stability culture”, Journal of International Money and Finance, Vol. 41, 2014, pp. 110-127; Iara, A. and Wolff, G.B., “Rules and risk in the Euro area”, European Journal of Political Economy, Vol. 34, 2014, pp. 222-236; Thornton, J. and Chrysovalantis, C., “Fiscal rules and government borrowing costs: International evidence”, Economic Inquiry, Vol. 56, No 1, 2018, pp. 446-459; and Afonso, A. and Jalles, J.T., “Fiscal Rules and Government Financing Costs”, Fiscal Studies, Vol. 40, No 1, 2019.

- For example, the opening of an excessive deficit procedure has been found to have a significant upward effect on sovereign spreads. See Kalan, F.D., Popescu, A. and Reynaud, J., “Thou Shalt Not Breach: The Impact on Sovereign Spreads of Noncomplying with the EU Fiscal Rules”, Working Paper Series, No 18/87, International Monetary Fund, April 2018.

- The fiscal compact only entered into force in 2013.

- It should be acknowledged, however, that the structural balance may overstate the country’s underlying budgetary situation somewhat as it may reflect extraordinary revenue growth over and above the long-term trend.

- Fiscal federalism is concerned with the way the various public functions are assigned to different levels of government and how the relevant fiscal instruments are distributed to enable these functions to be carried out. Depending on the design of fiscal federalism, it can fulfil very different functions, such as providing redistribution, stabilisation or risk sharing among the sub-federal entities. See also Darvas, Z., “Fiscal federalism in crisis: lessons for Europe from the US”, Bruegel Policy Contribution, Issue 7, 2010.

- In the United States, 13% of state-specific shocks to GDP can be expected to be smoothed by the federal tax-transfer and grant system, compared with 62% through private risk-sharing instruments (i.e. market transactions). See Asdrubali, P., Sorensen, B., and Yosha, O., “Channels of Interstate Risk Sharing: United States 1963-1990”, Quarterly Journal of Economics, Vol. 111, No 4, 1996.

- In Switzerland, the no-bailout clause took effect in 2003 after the municipality of Leukerbad defaulted on its debt and the canton of Valais was not held responsible. In the United States, no state has defaulted on its debt since the default of Arkansas in 1933.

- Several empirical studies show that the fiscal stimulus provided at federal level essentially offset the procyclical tightening embedded in US states’ rules in 2009. See for example Aizenman, J. and Pasricha, G., “Net Fiscal Stimulus during the Great Recession”, Review of Development Economics, Vol 17(3), 2013, pp. 397-413; and Blöchliger, H. et al., “Fiscal policy across levels of government in times of crisis”, Working Paper, No 12, Organisation for Economic Co-operation and Development, 2010. For the role of rainy day funds, see Fatas, A. and Mihov, I., “The macroeconomic effects of fiscal rules in the US states”, Journal of Public Economics, Vol. 90(1-2), 2006, pp. 101-117.

- See Burret, H. and Feld, L., “Effects of Fiscal Rules – 85 Years' Experience in Switzerland”, CESifo Working Paper Series, No 6063, CESifo, 2016.

- See Feld, L. and Kirchgässner, G., “On the Effectiveness of Debt Brakes: The Swiss Experience”, in Neck, R. and J.-E. Sturm (eds.), Sustainability of Public Debt, MIT Press, Cambridge, 2008; Hou, Y. and Smith, D., Do state balanced budget requirements matter? Testing two explanatory frameworks, Public Choice, Vol. 145, 2010; Mahdavi, S. and Westerlund, J., Fiscal stringency and fiscal sustainability: Panel evidence from the American state and local governments, Journal of Policy Modeling, Vol. 33, 2011; and European Commission, “Fiscal rules database”, 2017.

- In fact, assessments even seem to differ of the rules within a monetary union. For the United States, for example, studies differ in their assessment of the strictness of the states’ rules. Moreover, the studies used for the index have different reference dates: for the United States the data are from 2006, for Switzerland from 2008, and for the euro area from 2017. However, in contrast to the euro area, changes in the fiscal rule frameworks in the United States and Switzerland have been marginal in recent years.

- See Department of Finance, “Rainy Day Fund – Consultation Paper”, October 2017; see for details also Casey, E. et al. “Designing a Rainy Day Fund to Work within the EU Fiscal Rules”, Working Paper Series, No 6, Irish Fiscal Advisory Council, 2018.

- Surpluses and shortfalls vis-à-vis the constitutional structural balance rule are recorded in a virtual control account, which is intended to provide flexibility in the presence of cyclical swings.

- See Arnold, N.G., Barkbu, B.B., Elif Ture, H., Wang, H. and Yao, J., “A Central Fiscal Stabilization Capacity for the Euro Area”, Staff Discussion Notes, No 18/03, International Monetary Fund, 2018.

- On 22 January 2019 the ECOFIN Council approved recommendations for the conduct of fiscal policies in the current year, highlighting the need to “rebuild fiscal buffers, especially in euro area countries with high levels of public debt”.

- The broad application of “relevant factors” needs to be reviewed. See the article entitled “Government debt reduction strategies in the euro area”, Economic Bulletin, Issue 3, ECB, 2016.

- Similar views are expressed in “Annual Report 2018”, European Fiscal Board, as well as in “Is the main objective of the preventive arm of the Stability and Growth Pact delivered?”, Special Report, European Court of Auditors, No 18, 2018.

- See Kamps, C. and Leiner-Killinger, N., “Taking stock of the functioning of the EU fiscal rules and options for reform”, Occasional Paper Series, ECB, forthcoming, 2019.