Survey on the Access to Finance of Enterprises in the euro area − October 2018 to March 2019

Introduction

This report presents the main results of the 20th round of the Survey on the Access to Finance of Enterprises (SAFE), which was conducted between 11 March and 16 April 2019. The survey covers the period from October 2018 to March 2019. The total euro area sample size was 11,722 enterprises, of which 10,712 (91%) had fewer than 250 employees.[1]

The report provides evidence on changes in the financial situation of enterprises and documents trends in the need for and availability of external financing. It includes results on small and medium-sized enterprises (SMEs) as well as large firms, and examines developments both at the euro area level and in individual countries.

1 Overview of the results

Availability of skilled labour remained the dominant concern for euro area SMEs, together with the difficulty of finding customers, while access to finance was considered the least important obstacle. As in previous editions, the 20th round of the Survey on the Access to Finance of Enterprises (SAFE) also asked entrepreneurs to indicate the most pressing problem facing their company. Availability of skilled labour was considered the main problem for euro area SMEs (25%), together with the difficulty of finding customers (23%). Access to finance, on the other hand, remained the least important obstacle (8%), after cost of production and regulation (both 12%) and competition (13%). SMEs in Greece continued to be strongly affected by the lack of access to finance, with one-quarter mentioning it as their most important problem. Italy and Ireland (both 9%) and France (8%) had the second and third largest shares of SMEs reporting access to finance as their dominant concern.

A declining but still sizeable share of euro area SMEs indicated improvements in their overall financial situation during the reference period. In particular, a net[2] 21% of euro area SMEs reported higher turnover (from 25%). At the same time, however, euro area SMEs reported unchanged profits (0%, from 3%). Cross-country differences in profits were strongly correlated with turnover trends.

Euro area enterprises continued to report, on balance, rising labour and other costs amid slight improvements in their debt and investment decisions. The net percentage of SMEs indicating an increase in labour costs reached 52% (from 51%), while the net percentage of firms reporting an increase in other costs remained unchanged at 57%. In this round, a small net percentage of SMEs reported an increase in interest expenses (5%, from 4%), while declining leverage was reported by slightly fewer SMEs (-7%, from -8%). The slow growth momentum was reflected in investment and hiring decisions. In net terms, 18% of SMEs reported increases in fixed investments (unchanged), 7% in inventories and working capital (from 9%) and 12% in the number of employees (from 14%).

The external financing gap of SMEs – the difference between the change in demand for and the change in the availability of external financing – remained negative[3] at the euro area level (-3%, from -5%) and in most euro area countries (see Table A, column 10).

Demand for bank loans increased over the period under review. In net terms, euro area SMEs reported a small increase in needs for bank loans (3%, from 0%) and for credit lines (6%, from 5%) (see Table A, columns 2 and 4 respectively). About 9% of SMEs, on balance, reported an increased need for trade credit (unchanged), and 11% indicated a higher demand for leasing or hire-purchase (from 13%). Financing from external and internal sources was mainly used for fixed investment and for inventories and working capital. Moreover, SMEs used finance for hiring and training new employees and developing and launching new products.

SMEs continued to indicate improvements in the availability of external sources of finance, albeit weaker than in the previous survey. The net percentage of SMEs reporting an improvement in the availability of bank loans declined to 9% (from 11%) (see Table A, column 6). The countries in which SMEs reported the most improvement in the availability of bank loans were Spain, Ireland and Portugal.

Latest developments in SAFE country results for SMEs

(over the preceding six months; net percentages of respondents)

Notes: For “needs”, see Chart 11; for “availability”, see Chart 15; and for the “financing gap”, see the notes to Chart 17. For “financing obstacles”, see the notes to Chart 20. “18H1” refers to round 19 (April to September 2018) and “18H2” refers to round 20 (October 2018 to March 2019).

With the exception of general economic outlook and access to public support, SMEs perceived all factors examined in the survey to positively affect the availability of external finance, although with lower net percentages than in the previous round. In fact, the development in the macroeconomic outlook was perceived to have negatively affected the access to finance for SMEs (-9%, from 2%) and the downturn was widespread across countries. At the same time, SMEs continued to indicate an improvement in the willingness of banks to provide credit (a net 16%, from 17%), as well as in their firm-specific outlook (10%), capital position (17%) and credit history (16%).

The overall indicator of financing obstacles[4] for bank loans for SMEs declined to 7% (from 8%) (see Table A, column 12). While the percentages of SMEs reporting difficulty in accessing bank loans diminished in most countries, financing obstacles remained relatively large in Italy and Portugal (both 10%) and Greece (30%). In this survey round, 28% of SMEs had applied for a loan. The rate for fully successful loan applications was 73% (from 74%), while the rejection rate rose slightly to 6% (from 5%).

Concerning price terms and conditions of bank financing, SMEs reported, on balance, rises in bank interest rates (4%, up from 3%) for the second consecutive time since 2014. At the same time, 30% of SMEs (from 31%) continued to signal higher levels of other costs of financing, such as charges, fees and commissions. As for non-price terms and conditions, SMEs reported, on balance, increases in the available size (11%) and maturity (3%), but also increases in collateral requirements (13%), all of which were broadly unchanged from the previous survey round.

The financial situation of large enterprises remained better than that of SMEs, as they continued to report marked increases in both turnover and profits, although with some moderation relative to the previous survey rounds. Around 43% of large firms applied for a bank loan, with a success rate that was much higher (83%) and a rejection rate that was much lower (2%) than those of SMEs. According to the survey results, the average interest rate charged to large enterprises on credit lines was about 150 basis points lower than that paid by SMEs. Large firms therefore continued to benefit from better access to finance than SMEs.

In this survey round two ad hoc questions were included, aimed at identifying euro area SMEs’ perceptions of the business situation in their sector. The first question regarded the business situation over the last six months: both SMEs and large firms reported, in net terms, a deterioration in the business environment. The second question concerned the economic outlook over the next six months. In this case too, survey responses provided a somewhat pessimistic picture of the euro area business environment, although with lower percentages for SMEs compared with the past (-3% for the outlook, from -10% for the past) but unchanged for large firms (-7%).

In sum, the survey results are consistent with a moderation in the growth momentum, which continued to be supported by accommodative financing conditions. As a reflection of increased macroeconomic uncertainty, SMEs signalled some concerns about past developments in their business environment, together with signs of increases in funding costs. Regarding the economic outlook over the next six months, euro area SMEs do not seem to expect their business environment to change fundamentally with respect to the preceding six months.

2 The financial situation of SMEs in the euro area

2.1 Smaller improvements in the financial situation of euro area SMEs

In the period between October 2018 and March 2019, the financial situation of euro area SMEs remained consistent with a moderation in the growth momentum, which continued to be supported by accommodative financing conditions (see Chart 1).

Change in the income and debt situation of euro area enterprises

(over the preceding six months; net percentages of respondents)

Base: All enterprises. Figures refer to rounds 3 (March-September 2010) to 20 (October 2018-March 2019) of the survey.Notes: The net percentage is the difference between the percentage of enterprises reporting an increase for a given factor and the percentage reporting a decrease. From round 11 onwards (April-September 2014), the concept of “Net interest expenses (what you pay in interest for your debt minus what you receive in interest for your assets)” was replaced with “Interest expenses (what your company pays in interest for its debt)”.

Q2. Have the following company indicators decreased, remained unchanged or increased over the past six months?

Despite some increasing concerns about SMEs’ business environment (see Box 1), survey results continued to suggest an ongoing economic expansion. The net percentage[5] of euro area SMEs[6] reporting higher turnover declined to 21% (from 25% during the previous survey period[7]). As in previous survey rounds, the net percentage of firms reporting higher turnover increased with size. While, on balance, only 8% (down from 15%) of micro firms reported higher turnover, the corresponding share of large firms was 41% (down from 42%), with small (30%, up from 29%) and medium-sized firms (36%, down from 40%) falling in between.

Euro area enterprises continued to report, on balance, rising labour and other costs amid slight improvements in their debt and investment decisions. A high net proportion of euro area SMEs across all size categories continued to report rising labour costs (52% overall, up from 51%) with responses that were broadly unchanged relative to the previous survey round: 45% (unchanged) for micro, 56% (from 55%) for small, 60% (from 58%) for medium and 55% (from 59%) for large firms. As regards net increases in other costs, the reported rise was broad-based across all firm sizes: large firms (54%, from 60%) and SMEs (57% overall, unchanged).

Profits also reflected the rise in costs, as, in net terms, SMEs reported unchanged profits (0%) compared with a 3% net increase in the previous survey round. While micro firms continued to report declining profits (-9%, from -3%), lower net percentages of larger firms reported profit rises, at 9% (down from 10%) for large firms, 8% (down from 10%) for medium-sized firms and 7% (down from 8%) for small firms.

Deleveraging among euro area enterprises seems to have slowed somewhat since the previous survey round. The net percentage of SMEs indicating a decline in their debt-to-asset ratio was marginally lower (-7%, from -8%), with a lower percentage among micro firms (-4%, from -8%), and slightly higher for large (-2%, from -1%) and medium-sized firms (-8%, from -6%).

In this survey round the net percentage of SMEs reporting an increase in interest expenses rose again (5%, from 4%). However, there was some heterogeneity with regard to firm size. While the net balance of reporting higher interest costs rose to 9% for micro enterprises and 3% for small (from 8% and 2% respectively), larger enterprises continued to indicate reductions in interest expenses (-7%, from -3%, for large firms and -3%, unchanged, for medium-sized firms).

The moderating economic growth was reflected in investment and hiring decisions. On balance, euro area SMEs continued to report rising fixed investments (18%, unchanged from the previous round), increasing inventories and working capital (7%, from 9%) and a growing number of employees (12%, from 14%). These developments applied to firms in all size categories, while the net percentages for large firms were significantly higher than those for SMEs in these three areas.

The improvements in turnover moderated somewhat, but were widespread across countries. Among the large euro area countries (see Chart 2), the net percentage of SMEs indicating higher turnover was largest in Germany (29%, from 31%), followed by Spain (20%, from 24%), France (20%, from 22%) and Italy (6%, from 12%). SMEs also reported higher turnover in the other euro area countries, particularly in the Netherlands, Ireland and Austria, but also in Greece, where the net percentage of SMEs reporting increased turnover remained in double digits for a second consecutive survey round (10%, from 16%) since the beginning of the crisis (see Chart 1a in Annex 1).

Profit dynamics continued to display significant variation among countries. Among the large euro area countries, a lower but still positive net percentage of SMEs reported increasing profits in Germany (9%, from 11%), while French (-4%, from -2%) and Italian SMEs (-16%, from -10%) continued to report declines and Spanish SMEs reported, in net terms, decreasing profit for the first time since 2015 (‑4%, from 2% in the previous survey round). SMEs in Slovakia, Portugal and, in particular, Greece (-30%, from -16%) reported net decreases in profits, and in all other euro area countries, while positive, the net percentages of SMEs reporting increased profits mostly shrunk, only rising in Austria (see Chart 1a in Annex 1).

Across countries, euro area enterprises continued to deleverage. Among the large countries, on balance, SMEs in Germany (-9%, unchanged), Spain (-6%, from ‑7%) and France (-6%, from -5%) reported a reduction in the debt-to-asset ratio, while those in Italy reported a rise (1%, from -4%). SMEs in all other euro area economies also reported, on balance, lower debt-to-asset ratios, with the exception of Greece (see Chart 2a in Annex 1).

In this survey round most euro area SMEs indicated an increase in interest expenses, although country-specific developments differed. Among the large economies, the highest net percentages were recorded among Italian (14%, from 12%) and French SMEs (13%, from 10%), followed by Spanish SMEs (9%, from 8%), while German SMEs continued to report lower net interest expenditures (-6%, unchanged). Among the other countries, only SMEs in the Netherlands (-4%, unchanged) and Austria (-4%, from -3%) reported, on balance, lower net interest expenditures, while Ireland had the highest net percentage of SMEs reporting an increase in interest expenses (20%, unchanged).

Change in the income and debt situation of euro area SMEs

(over the preceding six months; net percentages of respondents)

Base: All SMEs. Figures refer to rounds 3 (March-September 2010) to 20 (October 2018-March 2019) of the survey.Note: See the notes to Chart 1.

Q2. Have the following company indicators decreased, remained unchanged or increased over the past six months?

An increase in labour and other costs (for material and energy) was visible across all countries. The net percentage of SMEs reporting an increase in labour costs was highest in Slovakia (68%, from 63%) and lowest in France (34%, from 45%). For other costs, the corresponding net percentage was highest in Ireland (66%, from 69%) and France (64%, from 61%) and lowest in Austria and Portugal (both 50%, from 51% and 54% respectively) and Greece (45%, from 40%).

On balance, SMEs in all countries reported moderate increases in fixed investment, inventories and working capital, and employment. Among the large euro area countries, a slightly lower net proportion of SMEs in Germany, France and Italy continued to report an increase in fixed investment (17%, 13% and 18% respectively, compared with 18%, 15% and 19% in the previous survey round), and a slightly higher proportion in Spain (23%, from 21%). Among the other euro area countries, the net percentage of SMEs indicating rising fixed investment was highest in Ireland (24%) and Portugal (23%). In net terms, inventories and working capital also continued to increase, but at a smaller pace in most countries. SMEs in France, Italy and Spain reported a lower net percentage increase, while it was slightly higher for those in Germany. In the other countries, only Greek SMEs continued to report declining inventories and working capital (-13%, from -5%).

Regarding employment in the large euro area countries, the net percentage of SMEs reporting an increase in the number of employees was highest in Spain (17%, unchanged) and lowest in Italy (3%, from 10%). Among the other euro area countries, the net percentage of SMEs reporting increasing employment was highest in Ireland (19%) and Portugal (18%).

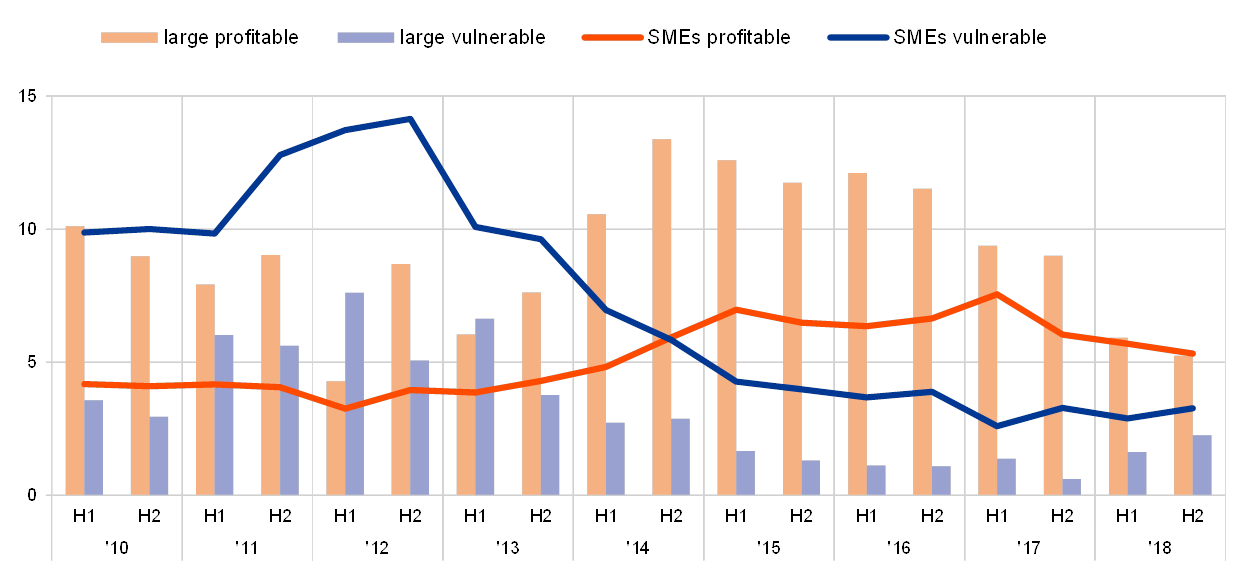

Against this background, the financial vulnerability of euro area SMEs remained broadly unchanged in this survey round. According to the two indicators of vulnerable and profitable firms[8] – which summarise the overall financial conditions of the most and least vulnerable euro area firms across firm sizes and countries – 3.3% (up from 2.9%) of euro area SMEs encountered major difficulties in running their business and servicing their debt and, as a result, might face more difficulties in accessing finance (see Chart 3). At the other end of the spectrum, the percentage of firms that were more likely to be resilient to financial shocks, tending to invest and hire more often than other firms, declined to 5.3%, down from 5.7% in the previous survey round. The net percentage of vulnerable firms, however, remained far from its historical peak of 14.2% in the second half of 2012.

Looking at size differences, smaller firms remain more vulnerable than large companies, but the gap has declined over time. In this survey round the percentage of vulnerable firms among large firms increased to 2.3%, from 1.6%. Although the financial situation of large enterprises remained better than that of SMEs, there was a decline in the net percentage of profitable large firms, which dropped to 5.3%, from 5.9% – its lowest level since 2012.

Vulnerable and profitable enterprises of euro area

(percentages of respondents)

Base: All enterprises. Figures refer to rounds 3 (March-September 2010) to 20 (October 2018-March 2019) of the survey.Note: For definitions, see footnote 8 of the report.

Q2. Have the following company indicators decreased, remained unchanged or increased over the past six months?

Focusing on SMEs, the indicators of profitable-vulnerable firms reveal some heterogeneity across countries (see Chart 4 for the euro area and the large countries). The percentage of distressed companies remained high in Italy (7.3%, up from 5.0%) followed by France (4.5%, up from 4.3%), although much lower than the peaks reached during the sovereign debt crisis. The percentage of vulnerable firms declined slightly in Germany (1.2%, from 1.6%) and Spain (3.0%, from 3.6%). The net percentage of profitable firms in turn declined in Spain, France and the euro area as whole, and among the large countries it only rose in Italy. For the trend in other euro area countries, see Chart 3a in Annex 1.

Vulnerable and profitable SMEs

(percentages of respondents)

Base: All SMEs. Figures refer to rounds 3 (March-September 2010) to 20 (October 2018-March 2019) of the survey.

Q2. Have the following company indicators decreased, remained unchanged or increased over the past six months?

To better gauge SMEs’ perceptions of the business situation in their sector, this survey round included two ad hoc questions on the developments in the business environment faced by euro area SMEs over the last six months and the prospects for the next six months. Box 1 summarised the main results.

Box 1 SMEs’ business environment: recent evolution and prospects

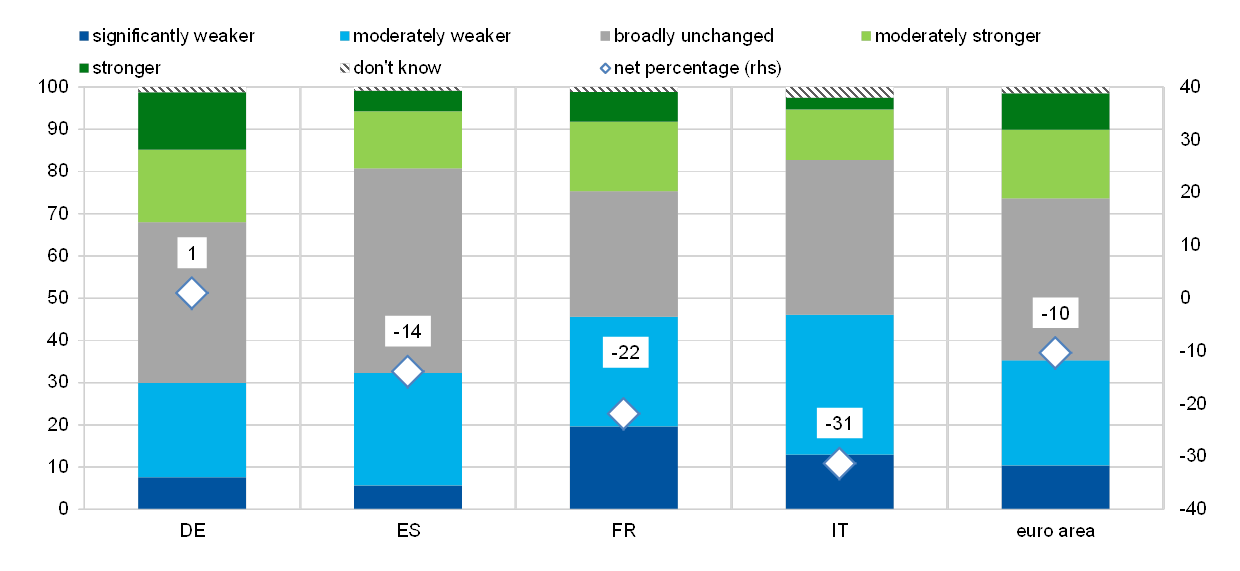

Regarding past developments, while a large share of firms perceived the economic situation as broadly unchanged, a net percentage of both SMEs and large firms reported a weaker environment (-10% and -7% respectively, see Chart A). The negative assessment of the business environment seems to be particularly influenced by micro firms (-17%), much more so than small and medium ones (-5% and -4% respectively). Among the large euro area countries, SMEs’ business environment was perceived as being weaker in Italy and France (with net percentages of ‑31% and -22% respectively), followed by Spain (-14%). Only in Germany were SMEs’ perceptions of the business situation more balanced (1%) (see Chart B).

Chart A

Past assessment of business environment of euro area enterprises

(over the preceding six months; percentage of respondents (left-hand scale) and net percentage of respondents (right-hand scale))

QA1: Over the past six months, how do you assess the general business situation in your sector?

Base: All enterprises. Figures refer to round 20 (October 2018- March 2019) of the survey.Note: The net percentage is the difference between the percentage of enterprises reporting a moderately stronger or stronger business situation in the sector in the past six months and the percentage of firms reporting a moderately weaker or significantly weaker business situation in the sector in the past six months.

Chart B

Past assessment of business environment of euro area SMEs

(over the preceding six months; percentage of respondents (left-hand scale) and net percentage of respondents (right-hand scale))

QA1: Over the past six months, how do you assess the general business situation in your sector?

Base: SMEs. Figures refer to round 20 (October 2018- March 2019) of the survey.Note: The net percentage is the difference between the percentage of enterprises reporting a moderately stronger or stronger business situation in the sector in the past six months and the percentage of firms reporting a moderately weaker or significantly weaker business situation in the sector in the past six months.

Regarding the near-term prospects for the business environment, survey responses also point to a net deterioration among SMEs across the euro area, albeit somewhat less so than was the case with their perceptions of the past (-3% for the future, compared with -10% for the past). This is true also for France (-9%) and Italy (-6%), while expectations about the future in Spain are balanced (0%). In Germany, SME expectations about future business conditions seem to have deteriorated somewhat compared with perceptions about the past (-3%, from +1%) (see Chart C). In addition, in contrast to the perceptions over the last six months, large firms appear to be, in net terms, somewhat more pessimistic about the near future (-7%) than SMEs (-3%).

Overall, however, euro area firms do not seem to expect their business environment to change fundamentally in the near future with respect to the situation they were facing over the last six months. Specifically, those firms that have already perceived a moderately weaker or significantly weaker environment recently expect the business environment to deteriorate further over the next six months (net percentages of -25% and -39%), while those that reported a recent moderately stronger or stronger environment also expect improvements to continue in the near future (25% and 38% in net terms).

Chart C

Prospects for business environment of euro area SMEs

(over the next six months; percentage of respondents (left-hand scale) and net percentage of respondents (right-hand scale))

QA2: Looking ahead, please indicate whether you think the general business situation in your sector will improve, remain unchanged or deteriorate over the next six months.

Base: SMEs answering to QA1. Figures refer to round 20 (October 2018- March 2019) of the survey.Note: The net percentage is the difference between the percentage of enterprises reporting that the business situation will improve and those reporting that the business situation will deteriorate.

At the sectoral level, SMEs in industry and trade sectors indicated in net terms that the business outlook remains negative (-8% and -10% respectively), although less so compared with the past six months (-11% and -26% respectively, see Chart D). SMEs in the construction sector instead reported, in net terms, a stronger business environment for both the past (13%) and for the future outlook (2%), while in the services sector net positive percentages were reported for the near future (1%) despite the somewhat pessimistic picture for the past (-8%). Profitable firms tend to be significantly more optimistic about the near-term business outlook (a net percentage of 13%) than vulnerable[9] ones (-20%), and higher optimism also appears to be present among innovative[10] and younger firms.

Chart D

Recent developments and future assessment of the business environment of euro area SMEs, by sector

(over the preceding six months and over the next six months; percentage of respondents (left-hand scale) and net percentage of respondents (right-hand scale))

QA1: Over the past six months, how do you assess the general business situation in your sector? Was it stronger, moderately stronger, broadly unchanged, or moderately or significantly weaker? QA2: Looking ahead, please indicate whether you think the general business situation in your sector will improve, remain unchanged or deteriorate over the next six months.

Base: SMEs. Figures refer to round 20 (October 2018- March 2019) of the survey.Note: The net percentage is the difference between the percentage of enterprises reporting that the business situation will improve and those reporting that the business situation will deteriorate. The category “stronger” for QA1 includes enterprises answering stronger or moderately stronger. The category “weaker” includes enterprises answering significantly weaker or moderately weaker.The category “stronger” for QA2 includes enterprises answering “will improve”. The category “weaker” includes enterprises answering “will deteriorate”.The last six months refer to the period October 2018-March 2019, while the next six months refer to the period April-September 2019.

Overall, the results from the two ad hoc questions are broadly in line with the answers to the rest of the questionnaire. For example, SMEs signalling an improved capital situation (26% of all SMEs), tended also to have a more positive perception of the past and near future developments in their business environment (17% and 8% respectively). Similarly, firms with an improved availability of bank loans (18% of all SMEs) had, in net terms, a positive assessment for the past and future business environment (10% and 9% respectively). These groups of firms may help moderate the slowdown in activity among SMEs in the euro area.

2.2 Access to finance ranked as SME’s least important concern

Availability of skilled labour continues to be the dominant concern for euro area SMEs, together with the difficulty of finding customers, while access to finance was considered the least important obstacle (see Chart 5). In this survey round, 25% of euro area SMEs cited “availability of skilled labour” as their main problem (marginally down from 26% in the previous survey round), followed by “difficulty of finding customers” (23%, up from 22%).

Looking at small, medium and large euro area companies, the main concern across the board was “availability of skilled labour”, with net percentages of 30%, 30% and 28% respectively, followed by “finding customers” (23% for all firm sizes). Micro firms, however, reported a somewhat higher concern regarding finding customers (23%) than finding skilled staff (20%). The differences across firm size may reflect that demand for staff is lower among micro firms, while the lack of skilled staff is a pressing problem for larger firms. “Access to finance”, in contrast, continues to be considered the least important obstacle for euro area SMEs (8%, marginally up from 7%), after “cost of production” and “regulation” (both 12%) and “competition” (13%), all broadly unchanged from the previous survey round.

Concerns about access to finance were higher for SMEs as a whole than for the large companies. While 8% of both micro and small and 7% of medium-sized enterprises signalled that access to finance was the main obstacle, only 5% of large companies did.

The most important problems faced by euro area enterprises

(percentages of respondents)

Base: All enterprises. Figures refer to rounds 3 (March-September 2010) to 20 (October 2018-March 2019) of the survey.Notes: The formulation of the question has changed over the survey rounds. Initially, respondents were asked to select one of the categories as the most pressing problem. From round 8, all respondents were asked to indicate how pressing a specific problem was on a scale from 1 (not pressing) to 10 (extremely pressing). In round 7, the formulation of the question followed the initial phrasing for one-half of the sample and the new phrasing for the other half. In addition, if two or more items had the highest score in question Q0B on “how pressing the problems were, a follow-up question (Q0C) was asked to resolve this, i.e. which of the problems was more pressing, even if only by a small margin. This follow-up question was removed from the questionnaire in round 11. The past results from round 7 onwards were also recalculated, disregarding the replies to question Q0C. In round 12, the word “pressing” was replaced by the word “important”.

Q0. How important have the following problems been for your enterprise in the past six months?

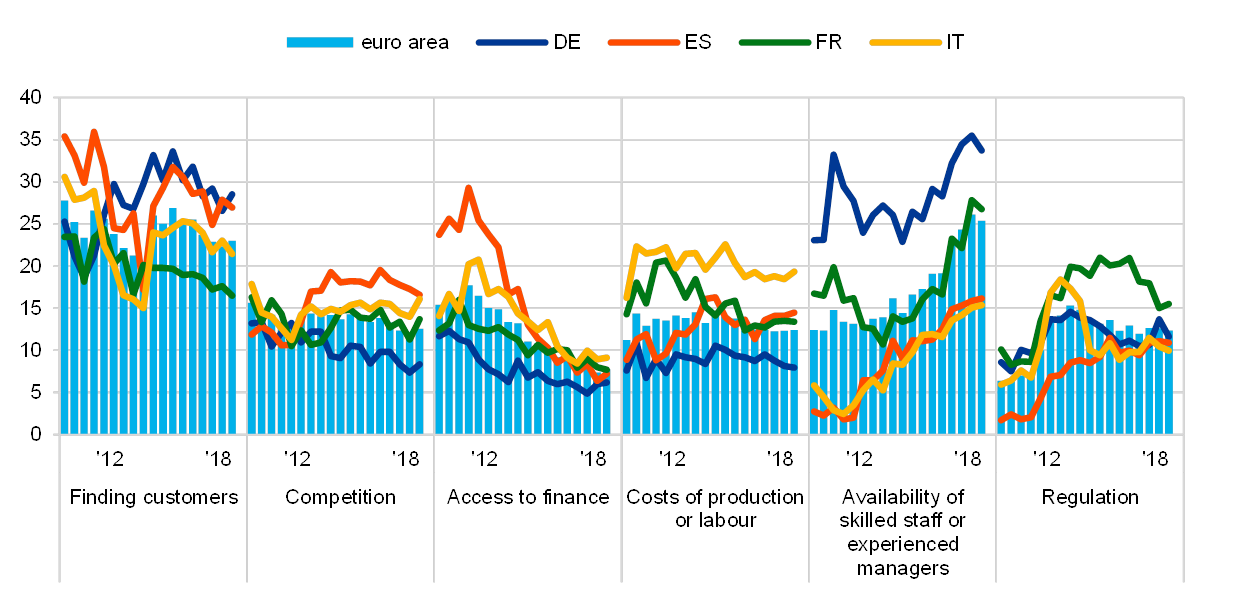

The euro area aggregate masks considerable differences across countries (see Charts 6 and 4a in Annex 1). Among the SMEs in the largest euro area countries, German (34%) and French SMEs (27%) most frequently cited the availability of skilled staff as their dominant concern, ahead of finding customers (29% and 17% respectively). Spanish (27%) and Italian (21%) SMEs instead reported finding customers as their main problem. Among other euro area countries, SMEs in Greece continued to be disproportionately affected by the lack of access to finance, with, on balance, 25% (up from 17%) of firms still citing it as their most important problem, well above the levels for the euro area as a whole (8%) and other individual countries, for all of which this criterion remained in single digits.

The most important problems faced by euro area SMEs

(percentages of respondents)

Base: All SMEs. Figures refer to rounds 3 (March-September 2010) to 20 (October 2018-March 2019) of the survey.Note: See the notes to Chart 5.

Q0. How important have the following problems been for your enterprise in the past six months?

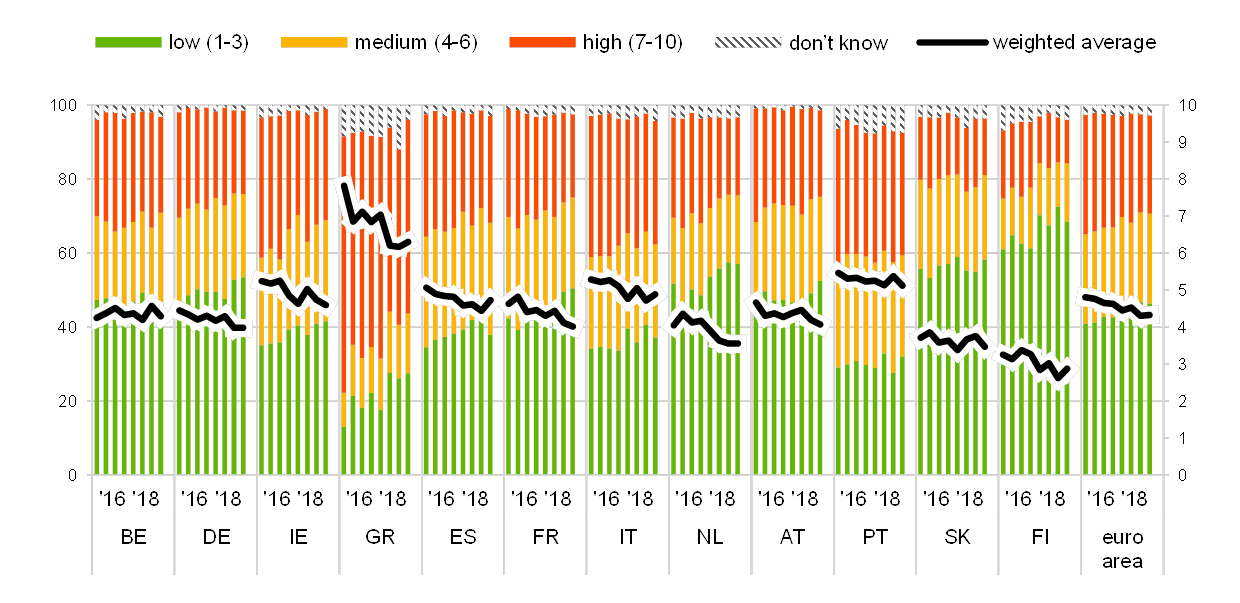

A similar picture emerges when looking at the responses, on a scale of 1-10, on whether “access to finance” is a problem in the current situation. SMEs in Greece continued to perceive it as a very important issue (rating it at 6.3 on average; see Chart 7), followed by scores of 5.1 in Portugal and 4.9 in Italy. The remainder of the countries reported scores close to or below the euro area average of 4.3, with SMEs in Finland continuing to report the lowest average score (2.9).

Importance of access to finance as perceived by SMEs across euro area countries

(left-hand scale: percentages; right-hand scale: weighted averages)

Base: All SMEs. Figures refer to rounds 13 (April-September 2015) to 20 (October 2018-March 2019) of the survey. Notes: Enterprises were asked to indicate how important a specific problem was on a scale from 1 (not at all important) to 10 (extremely important). On the chart, the scale has been divided into three categories: low (1-3), medium (4-6) and high importance (7-10). The weighted average score is an average of the responses using the weighted number of respondents.

Q0b. How important have the following problems been for your enterprise in the past six months?

3 SMEs financing needs and sources

3.1 Banks remained the most relevant source of finance

Bank-related products remained the most relevant financing source for SMEs, ahead of market-based instruments and other sources of finance (see Chart 8). For the period from October 2018 to March 2019, about half of the euro area SMEs considered bank loans and credit lines to be relevant financial instruments for their businesses (50% and 49% respectively).[11] Leasing or hire-purchase was relevant for 45% of SMEs, while 34% indicated that grants and subsidised loans (i.e. loans that involve support from public sources in the form of guarantees or other interventions) were a potential source of finance. 29% of SMEs mentioned trade credit as an important financial instrument, while 24% reported using their internal funds to finance their business activity. Finally, 18% of SMEs pointed to other loans (for example from family, friends or related companies) as a relevant source of finance. Market-based instruments, such as equity (11%) and debt securities (3%), and factoring (10%) were much less frequently considered as a potential source of finance. These responses imply very marginal changes to the sources of financing among SMEs compared with the previous survey round.

Relevance of financing sources for euro area SMEs

(over the preceding six months; percentages of respondents)

Base: All SMEs. Figures refer to round 20 (October 2018-March 2019) of the survey.

Q4. Are the following sources of financing relevant to your enterprise that is, have you used them in the past or considered using them in the future? If “yes”, have you obtained new financing of this type in the past six months?

The use of all financing instruments increased with firm size: the share of large firms that reported having used any given financing instrument was always larger than that of SMEs (see Chart 9). Short-term bank finance (credit line/bank overdraft/credit card) remained the most popular source of finance by some margin, followed by leasing and bank loans. Equity and debt securities, on the other hand, were among the least frequently used sources of finance. Those patterns were shared both among SMEs and large firms.

Use of internal and external funds by euro area enterprises, by firm size

(percentages of respondents that had used the respective instrument in the past six months)

Base: All enterprises. Figures refer to round 20 (October 2018-March 2019) of the survey.

Q4. Are the following sources of financing relevant to your enterprise, that is, have you used them in the past or considered using them in the future? If “yes”, have you obtained new financing of this type in the past six months?

Distinguishing between vulnerable and profitable SMEs[12] can help investigate the impact of the financial situation of the companies in their source of finance (see Chart 10). Vulnerable firms resorted to credit lines (48%) and banks loans (26%) as their main source of external financing, and to a much larger extent than profitable firms (29% and 14% respectively). In turn, profitable firms relied more on their internal funds, but also chose leasing or hire-purchases more frequently than vulnerable firms.

Use of internal and external funds by euro area SMEs across profitable and vulnerable firms

(percentages of respondents that had used the respective instrument in the past six months)

Base: All SMEs. Figures refer to round 20 (October 2018-March 2019) of the survey.

Q4. Are the following sources of financing relevant to your enterprise, that is, have you used them in the past or considered using them in the future? If “yes”, have you obtained new financing of this type in the past six months?

3.2 Demand for external financing among euro area SMEs remained heterogeneous

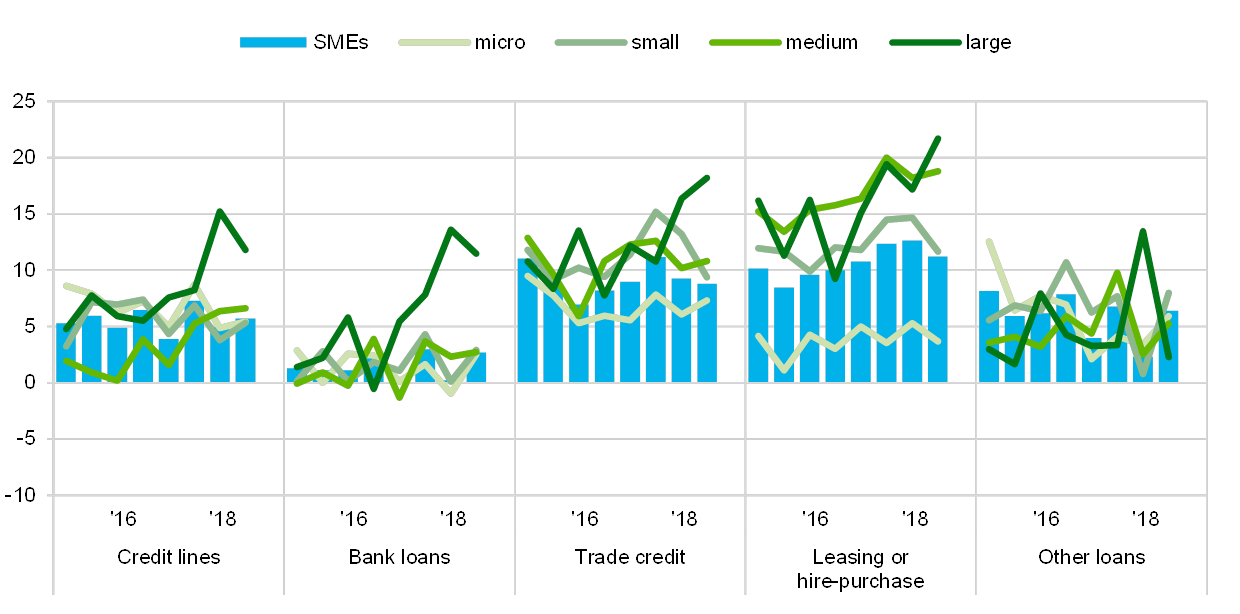

Demand for all external financing instruments among SMEs continued to rise (see Chart 11). SMEs reported an increase in their demand for bank loans[13] (3%, from 0%).A similar discrepancy across firm size is shown for credit lines, while the demand for leasing and hire-purchase increased slightly less than before (11%, from 13%), and the increase in the demand for trade credit was unchanged (at 9%).

Large firms reported a continued increase in external financing, albeit somewhat weaker than in the previous survey round. In net terms, a lower share of large firms reported increases in demand for bank loans (11%, from 14%), credit lines (12%, from 15%) and, in particular, other loans (2%, from 13%). Demand for bank credit appeared to be replaced by larger use of trade credit (18%, from 16%) and leasing activity (22%, from 17%).

Change in external financing needs of euro area enterprises

(over the preceding six months; net percentages of respondents)

Base: Enterprises for which the respective instrument is relevant. Figures refer to rounds 13 (April-September 2015) to 20 (October 2018-March 2019) of the survey.Notes: See the notes to Chart 1. The categories “Other loans” and “Leasing or hire-purchase” were introduced in round 12 (October 2014-March 2015). A financing instrument is “relevant” if the enterprise used the instrument in the past six months or did not use it but has experience of it (for rounds 1 to 10). From round 11 onwards, the respondents were asked whether the instrument was relevant, i.e. whether the enterprise had used it in the past or considered using it in the future. Given that the current concept of a “relevant” financing instrument differs from that used in the past, this might have an impact on the comparability over time for the subsequent questions. Caution should therefore be exercised when comparing the recent results with those of the previous rounds.

Q5. For each of the following types of external financing, please indicate if your needs increased, remained unchanged or decreased over the past six months.

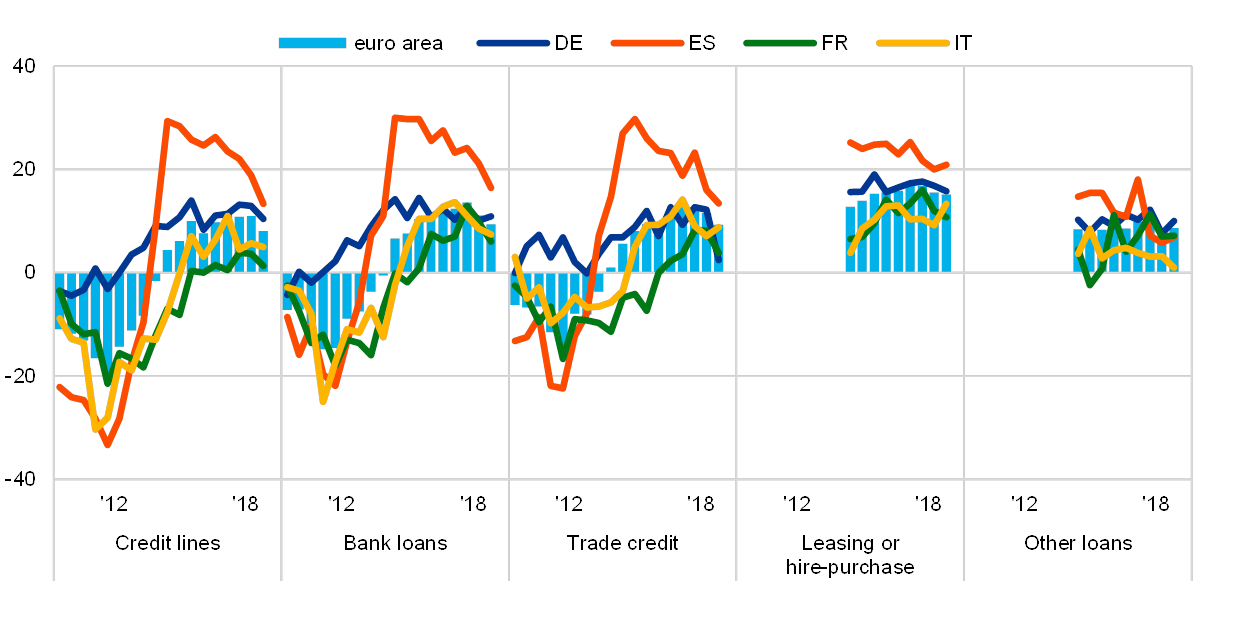

Euro area SMEs reported a higher demand for bank finance than in the previous survey round, including the four largest economies. SMEs indicated increasing needs for bank loans in France (12%, from 8%) and Italy (8%, from 6%), unchanged needs (0%) in Spain (but from decreases in the last three rounds), and while the decline in the need for bank loans continued in Germany it was somewhat less frequent across firms (-6%, from -8%, see Chart 12). The demand for credit lines also rose in Germany (5%, unchanged), France (15%, from 12%) and Italy (10%, from 7%), but declined slightly in Spain (-1%, unchanged). For other types of external financing for SMEs, there was more heterogeneity across the large euro area countries. Compared with the last survey round, SMEs reported a larger increase in the demand for other type of loans (from family, friends and related enterprises or shareholders) in France, Spain and Germany, but a somewhat lower increase in Italy when compared with the previous survey round. Trade credit demand rose in Italy (12%, from 10%), Spain (8%, from 9%) and France (4%, unchanged), but declined in Germany (-4%, from 3%). Compared with the previous round, demand for leasing and hire purchase increased most in Italy, rose at a similar speed in Spain and increased less in France and Germany.

In the other euro area countries, demand for external financing continued to be strongest in Greece. Greek SMEs’ demand for bank loans and credit lines rose to 26% (from 19%) and 32% (from 22%) respectively (see Chart 5a in Annex 1).

Change in external financing needs of euro area SMEs

(over the preceding six months; net percentages of respondents)

Base: SMEs for which the respective instrument is relevant. Figures refer to rounds 13 (April-September 2015) to 20 (October 2018-March 2019) of the survey.Note: See the notes to Charts 1 and 11.

Q5. For each of the following types of external financing, please indicate if your needs increased, remained unchanged or decreased over the past six months.

3.3 SMEs continued to use financing mostly for fixed investments, inventory and working capital

Financing from external and internal sources continued being used mainly for fixed investment, followed by inventories and working capital. Financing for hiring and training new employees and for developing and launching new products remained broadly unchanged from the previous survey round (see Chart 13). About 43% of SMEs (unchanged) reported using financing for fixed investment, while 34% (down from 36%) mentioned inventory and working capital.

Purpose of the financing as perceived by euro area enterprises

(over the preceding six months; percentages of respondents)

Base: All enterprises. Figures refer to rounds 13 (April-September 2015) to 20 (October 2018-March 2019) of the survey.Note: The figures are based on the new question introduced in round 11 (April-September 2014).

Q6A. For what purpose was financing used by your enterprise during the past six months?

The prevalence of fixed investment continued to be associated with company size. While 63% of large firms reported using funds for fixed investment, this applied to only 32% of micro firms. Investment in working capital and inventories was also related to firm size (46% for large firms, but only 31% for micro firms). Less frequently, SMEs used financing to hire and training employees (22%, unchanged), develop new products (21%, unchanged) and refinance obligations (13%, from 14%).

Among the firms in large euro area countries, German SMEs continued to stand out in terms of use of funds for fixed investment, hiring and training, and refinancing purposes. About 53% of German SMEs reported using funding for fixed investment, compared with only 35% of Spanish or 38% of French SMEs. Spanish firms continued to make strong use of financing for inventory and working capital (42%) more frequently than for fixed investment (see Chart 14).

Purpose of the financing as perceived by SMEs across euro area countries

(over the preceding six months; percentages of respondents)

Base: All SMEs. Figures refer to rounds 13 (April-September 2015) to 20 (October 2018-March 2019) of the survey.Note: See the note to Chart 13.

Q6A. For what purpose was financing used by your enterprise during the past six months?

4 Availability of external financing for SMEs in the euro area

4.1 Improved availability of external financing, with signs of increases in funding costs

4.1.1 Availability of all external financing sources increased, but less than in previous survey rounds

In the latest survey round, fewer SMEs reported improved availability of external financing sources relevant for their business (see Chart 15).[14] Particularly for bank loans, one of the most important means of funding for SMEs, the net percentage of respondents indicating improved availability declined to 9% (from 11%). For all other financing instruments, the net percentage of SMEs reporting easier access remained positive, although it declined to 8% (from 11% in the previous survey) for credit lines, 9% (from 12%) for trade credit and 15% (from 16%) for leasing and hire-purchase, and increased to 9% (from 7%) for other loans.

Change in the availability of external financing for euro area enterprises

(over the preceding six months; net percentages of respondents)

Base: Enterprises for which the respective instrument is relevant. Figures refer to rounds 3 (March-September 2010) to 20 (October 2018-March 2019) of the survey. Note: See the notes to Charts 1 and 11.

Q9. For each of the following types of financing, would you say that their availability has improved, remained unchanged or deteriorated for your enterprise over the past six months?

Large and medium-sized companies continued to be the most positive in their assessment of the availability of external financing. In this survey round, the net percentage of firms reporting better access to external funding increased for large enterprises, widening the gap with respect to smaller firms, particularly in the case of bank loans, for which only a net 4% of micro firms reported better availability, whereas a net 20% of large companies did. The differences are somewhat smaller for trade credit (8%, compared with 14%), credit lines (4%, compared with 15%), other loans (7%, compared with 9%) and leasing and hire-purchase (11%, compared with 18%).

Across countries, the differences are narrowing (see Chart 16 and Chart 5a in Annex 1). However, lower net percentages of respondents indicated better availability of bank loans, except in the case of Austrian, German, Irish, Greek and Portuguese SMEs. Similarly, fewer firms reported better access to leasing and hire-purchase, with the exception of those in Belgium, Greece, Italy, Spain and Portugal. Overall, SMEs in Ireland, Spain and Portugal were most upbeat about their external financing environment.

Change in the availability of external financing for euro area SMEs

(over the preceding six months; net percentages of respondents)

Base: SMEs for which the respective instrument is relevant. Figures refer to rounds 3 (March-September 2010) to 20 (October 2018-March 2019) of the survey.Note: See the notes to Charts 1 and 11.

Q9. For each of the following types of financing, would you say that their availability has improved, remained unchanged or deteriorated for your enterprise over the past six months?

4.1.2 External financing availability seen to rise faster than needs

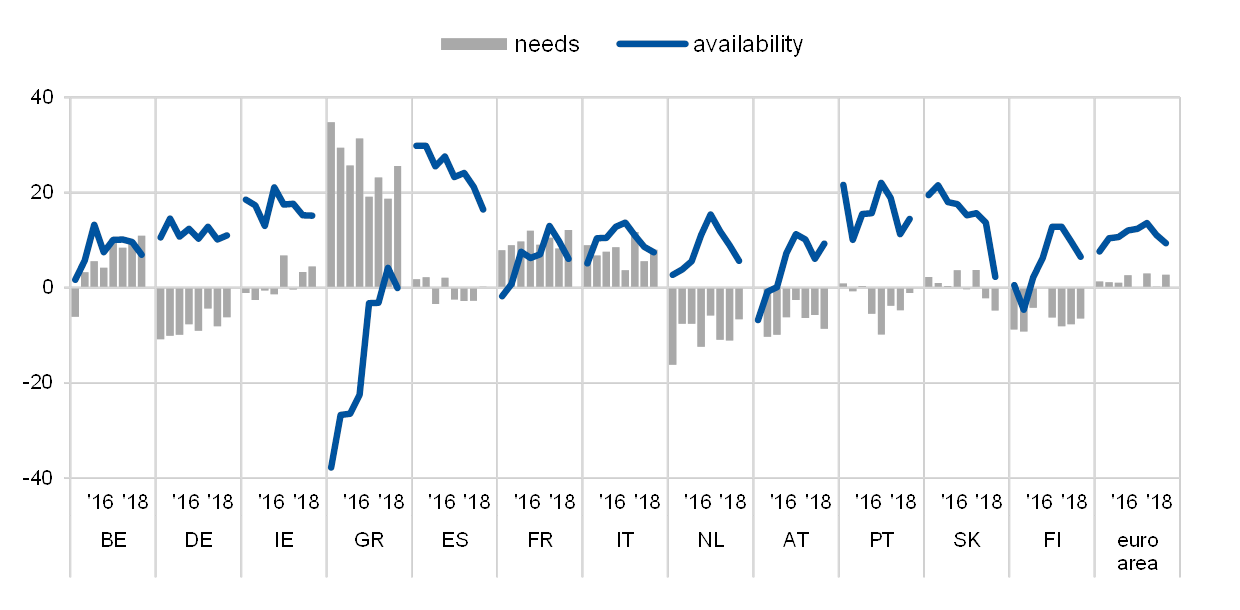

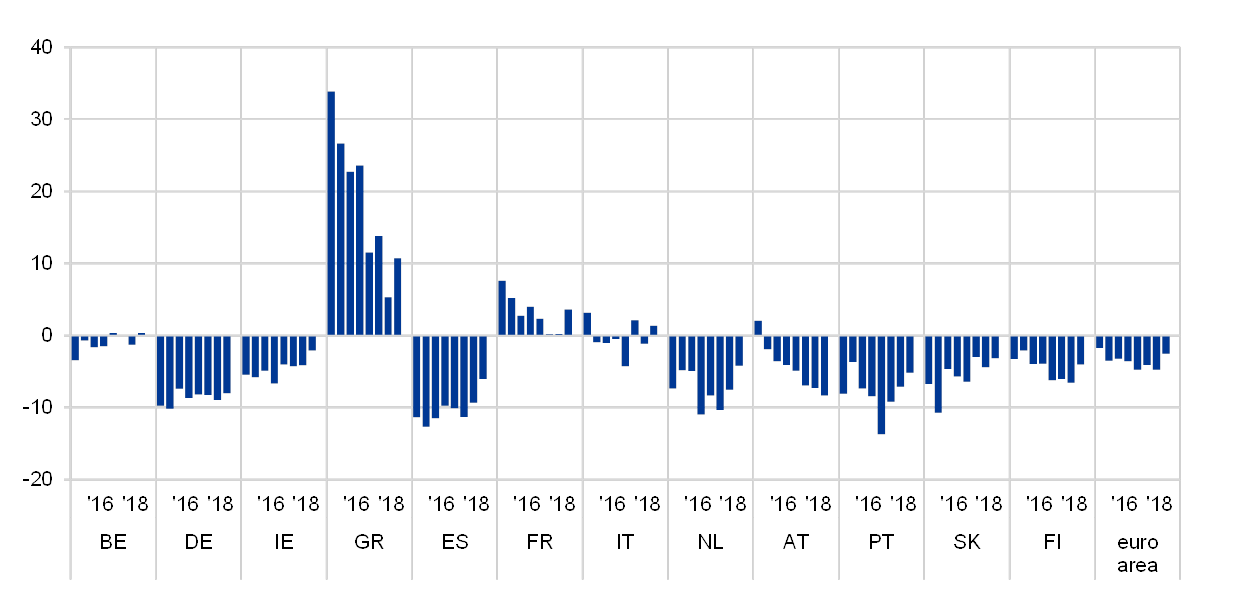

For the euro area as a whole, SMEs perceived the improvements in their access to external funds to be larger than the increases in corresponding financing needs, resulting in a negative external financing gap of -3% (see Chart 17). At the level of individual euro area countries, the financing gap was negative in the majority of cases, most notably in Germany and Austria (both -8%), Spain (-6%) and Portugal (-5%) (see also Chart 6a in Annex 1). In Belgium, external funding availability and needs were in balance in the latest survey round, while SMEs in Greece continued to remain financially constrained (11%, from 5%).

Change in the external financing gap perceived by SMEs across euro area countries

(over the preceding six months; weighted net balances)

Base: SMEs for which the respective instrument is relevant. “Not applicable” and “Don’t know” answers are excluded. Figures refer to rounds 3 (March-September 2010) to 20 (October 2018-March 2019) of the survey.Notes: See the notes to Chart 11. The financing gap indicator combines both financing needs and availability of bank loans, credit lines, trade credit, equity and debt securities at the firm level. For each of the five financing instruments, the indicator of the perceived change in the financing gap takes the value of 1 (-1) if the need increases (decreases) and availability decreases (increases). If enterprises perceive only a one-sided increase (decrease) in the financing gap, the variable is assigned a value of 0.5 (-0.5). The composite indicator is the weighted average of the financing gap related to the five instruments. A positive value of the indicator suggests an increasing financing gap. Values are multiplied by 100 to obtain weighted net balances in percentages.

Q5. For each of the following types of external financing, please indicate if your needs increased, remained unchanged or decreased over the past six months.Q9. For each of the following types of financing, would you say that their availability has improved, remained unchanged or deteriorated for your enterprise over the past six months?

4.1.3 Ongoing improvement in the willingness of banks to lend

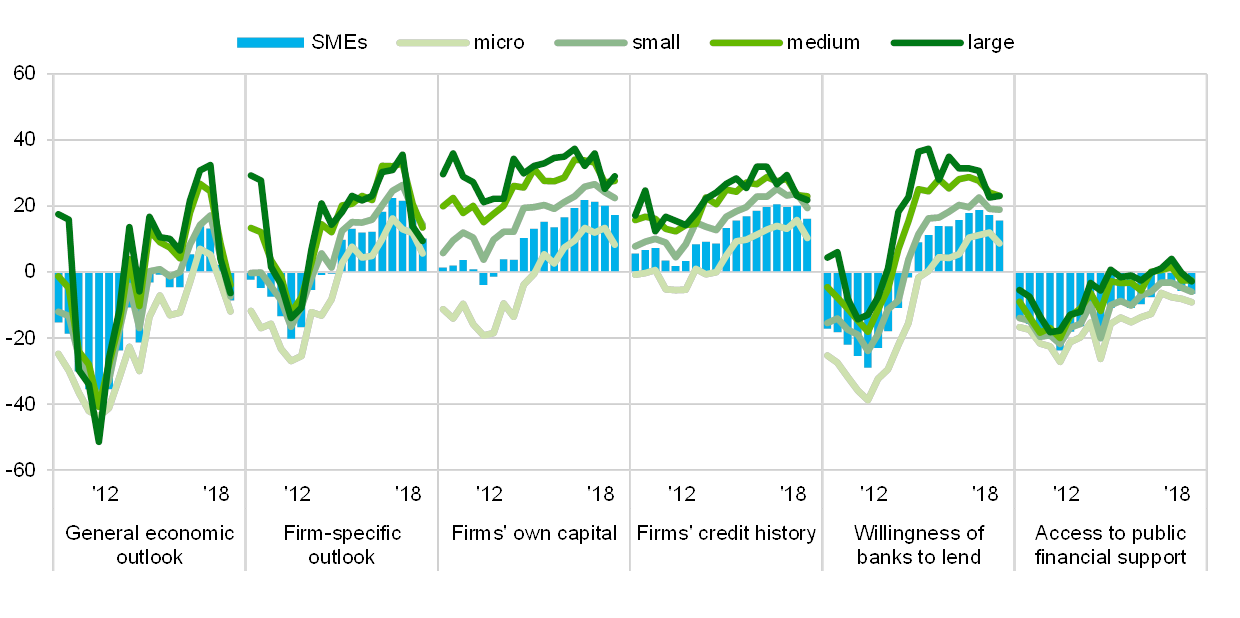

With the exception of the general economic outlook and access to public support, SMEs perceived that all other factors examined in the survey positively affected the availability of external finance, albeit with lower percentages than in the previous survey round (see Chart 18). Specifically, the firm-specific outlook (10%, from 16%), firms’ own capital (17%, from 20%) and firms’ credit history (16%, from 20%) continued to improve SMEs’ perceptions of the availability of external financing. However, in this survey round, developments in the general economic outlook were perceived to have negatively affected SMEs’ access to finance (-9%, from 2%). In addition, access to public financial support continued to register as a negative factor in net terms, as in the previous survey rounds.

Change in factors with an impact on the availability of external financing to euro area enterprises

(over the preceding six months; net percentages of respondents)

Base: All enterprises; for the category “Willingness of banks to lend”, enterprises for which at least one bank financing instrument (credit line, bank overdraft, credit card overdraft, bank loan, subsidised bank loan) is relevant. Figures refer to rounds 3 (March-September 2010) to 20 (October 2018-March 2019) of the survey.Note: From round 11 (April-September 2014), the category “Willingness of banks to provide a loan” was reformulated slightly to “Willingness of banks to provide credit to your enterprise”.

Q11. For each of the following factors, would you say that they have improved, remained unchanged or deteriorated over the past six months?

Banks’ willingness to provide credit continued to improve. In this survey round 16% of SMEs reported, in net terms, an increasing willingness of banks to lend (down from 17%), although the net percentage has remained on the high side since 2014.

Large and medium-sized enterprises generally conveyed a slightly more favourable view of the factors influencing their access to external finance. Regarding firm-specific variables, the assessment by medium and large enterprises continued to improve in net terms, albeit much less relative to the previous survey rounds. However, for the first time since 2014, they also reported that the general economic outlook might have become an impediment for their access to external finance (-4%, from 9%, for medium-sized firms, and -6%, from 4%, for large enterprises). For the willingness of banks to lend, the net percentage of micro firms indicating better conditions declined (to 9%, from 12%), while it remained almost unchanged for the other size classes, with the highest percentage for large and medium-sized enterprises (both at 23%).

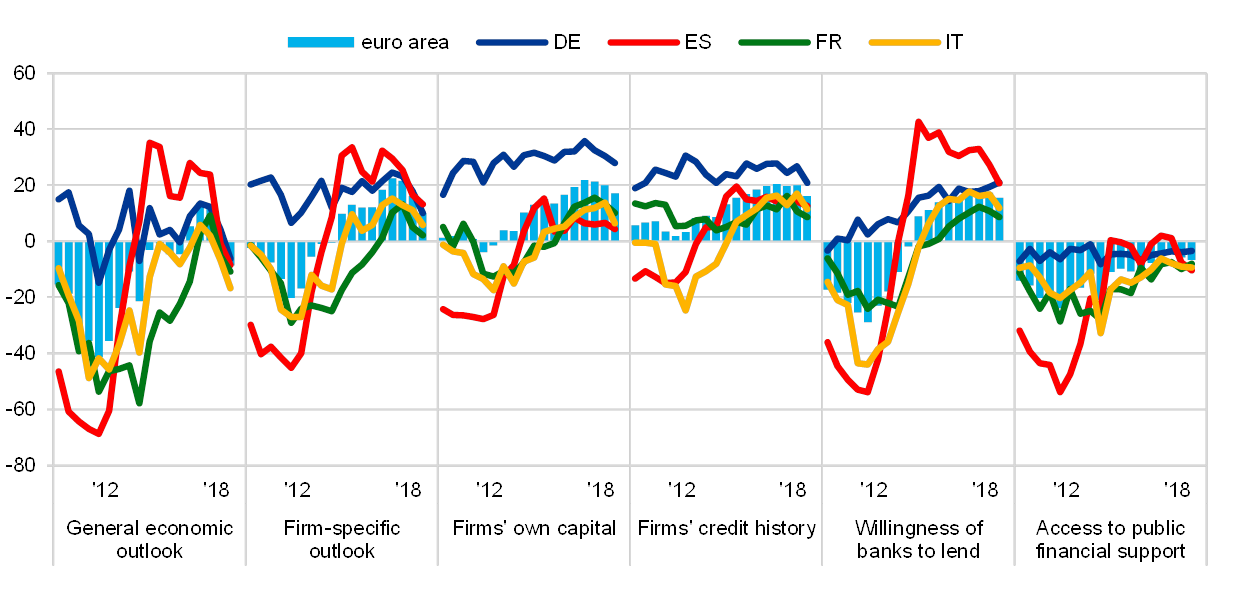

In the largest euro area countries, SMEs’ positive sentiment about nearly all factors affecting their access to external finance cooled further relative to the previous survey round (see Chart 19). In particular, the net percentages of SMEs considering more willingness of banks to lend declined in France (9%, from 11%), Italy (12%, from 17%) and Spain (21%, from 27%). By contrast, the percentage increased in Germany to 21%, from 19%.

Of greater concern, SMEs in Italy (-17%, from -7%), France (-11%, from -5%), Spain (-8%, from -1%) and Germany (-6%, from 4%) acknowledged a negative contribution of the general economic outlook to the availability of external financing.

Change in factors with an impact on the availability of external financing to euro area SMEs

(over the preceding six months; net percentages of respondents)

Base: All SMEs; for the category “Willingness of banks to lend”, SMEs for which at least one bank financing instrument (credit line, bank overdraft, credit card overdraft, bank loan or subsidised bank loan) is relevant. Figures refer to rounds 3 (March-September 2010) to 20 (October 2018-March 2019) of the survey.Note: From round 11 (April-September 2014), the category “Willingness of banks to provide a loan” was reformulated slightly to “Willingness of banks to provide credit to your enterprise”.

Q11. For each of the following factors, would you say that they have improved, remained unchanged or deteriorated over the past six months?

On balance, SME’s in the other euro area countries also considered the willingness of banks to lend to have improved, but less so than in the previous survey round. This was also the case for most firm-specific factors affecting the availability of external financing (see Chart 7a in Annex 1). In particular, the willingness of banks to lend was seen as having declined most in Greece (5%, down from 11%) and Ireland (14%, down from 18%), with the strongest increase in Slovakia (22%, up from 11%). Regarding the impact of the general economic outlook, SMEs in most economies reversed the optimism expressed about this factor since the end of 2016, with the exception of SMEs in Ireland and in the Netherlands, where positive net percentages decreased markedly, from 21% to 1% and from 25% to 3%, respectively. Greek SMEs continued to be most constrained by the factors impacting on access to external funding examined by the survey, in particular regarding the general economic outlook (-23%, from -11%), but also regarding firm specific factors like firms’ credit history (12%, from 17%), firm-specific outlook (8%, from 15%) and firms’ own capital (-7%, from 0%).

4.2 No significant changes in financing obstacles for SMEs

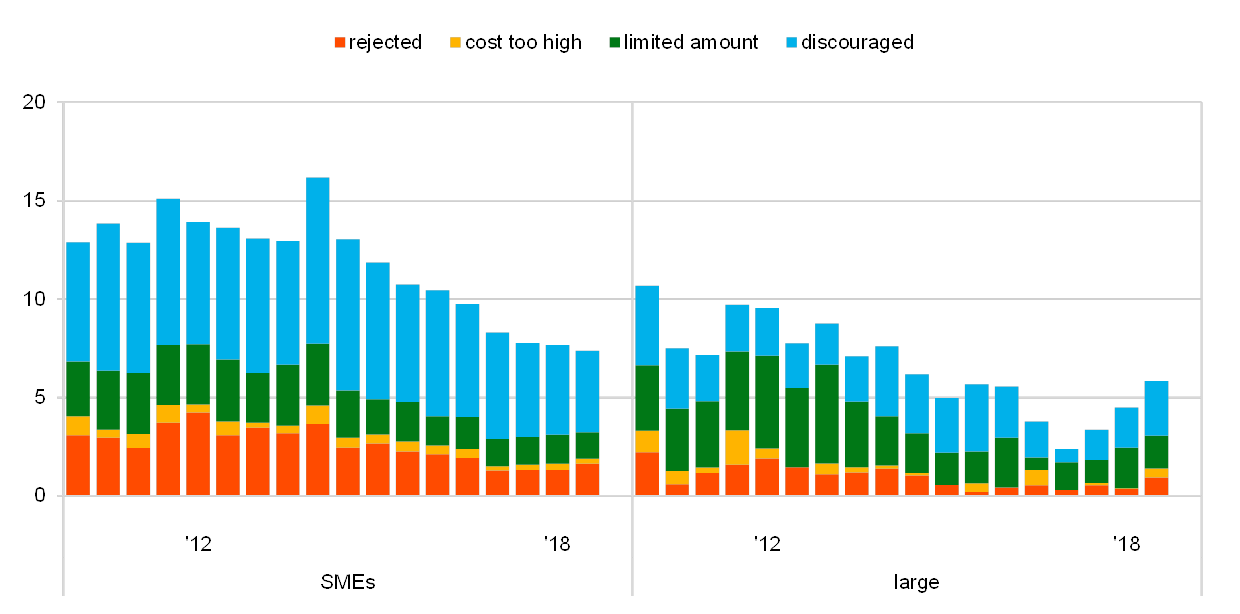

The share of SMEs reporting obstacles to obtaining a bank loan declined slightly but still remained above the corresponding figure for large enterprises (see Chart 20, panel a). Among enterprises judging bank loans relevant for their funding, 7.4% (from 7.7%) of SMEs faced obstacles to obtaining a loan; the share increased to 5.8% for large enterprises (from 4.5%). The different development was driven primarily by the proportion of SMEs discouraged from applying for a loan, which declined to 4.1% (from 4.6%), compared with an increase to 2.8% (from 2.0%) for large enterprises. At the same time, the proportion of loan applications rejected increased slightly for SMEs (1.6%, from 1.3%) and for large enterprises (0.9%, from 0.4%). By contrast, the share of firms considering the cost of a loan to be too high was similar for SMEs and large enterprises (0.3%, compared with 0.5%), while a slightly higher percentage of large companies reported receiving only a limited part of the loan amount requested (1.7%, compared with 1.3% for SMEs).

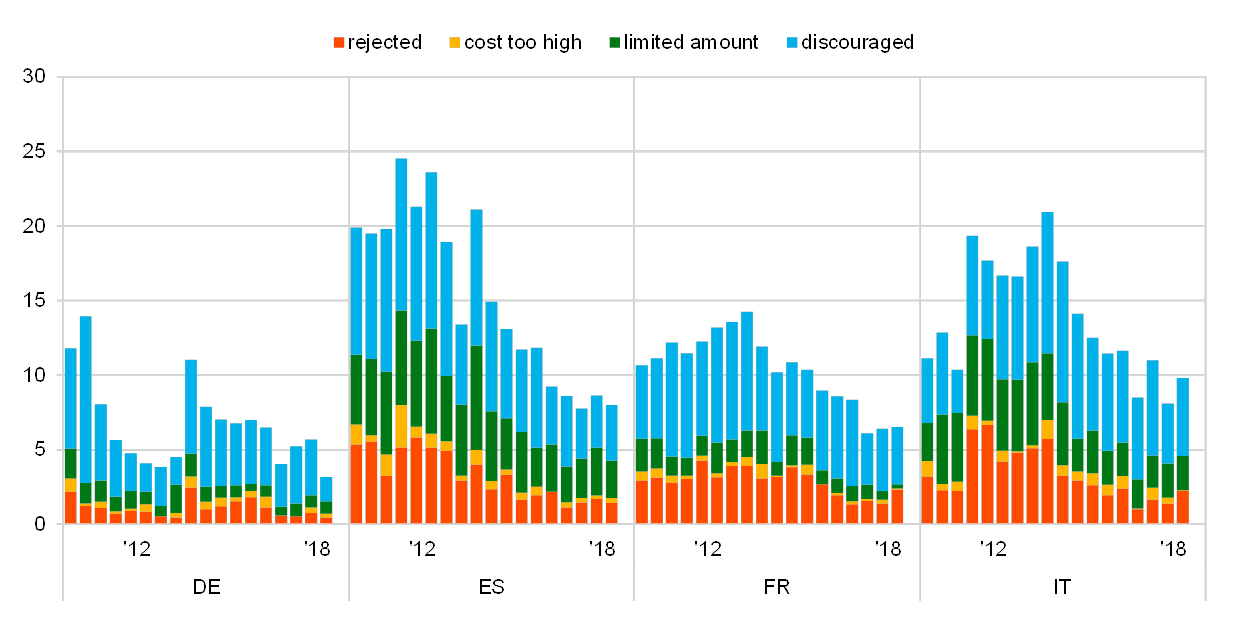

Across the largest euro area countries, the share of SMEs perceiving financing obstacles rose in Italy but declined in the other countries (see Chart 20, panel b). In Italy, increases, to 9.8% (from 8.1%), in the percentage of SMEs facing financing obstacles were a consequence of SMEs being more discouraged from applying for a loan (5.2%, from 4.0%) and receiving more rejections of their loan applications (2.2%, from 1.4%). By contrast, in Germany, SMEs reported a strong decline in financing obstacles, to 3.2% (from 5.7%), which was primarily driven by firms feeling much less discouraged from applying (1.6%, down from 3.7%). At the same time, French SMEs reported almost no changes in financing obstacles (6.5%, from 6.4%), although the share reporting bank loan rejection increased to 2.3% (from 1.4%). In the remaining euro area countries, large increases in financing obstacles were reported by Belgian (5.5%, from 3.9%) and Greek SMEs (29.9%, from 22.2%). Nonetheless, cross-country differences in the euro area continued to decrease, after the peaks observed in the October 2011 to March 2012 and April to September 2015 rounds.

Obstacles to receiving a bank loan

Panel a: Euro area SMEs and large enterprises

(over the preceding six months; percentages of respondents)

Base: Enterprises for which bank loans (including subsided bank loans) are relevant. Figures refer to rounds 3 (March-September 2010) to 20 (October 2018-March 2019) of the survey.Notes: Financing obstacles are defined here as the total of the percentages of enterprises reporting loan applications which were rejected, loan applications for which only a limited amount was granted, loan applications which resulted in an offer that was declined by the enterprises because the borrowing costs were too high, and enterprises which did not apply for a loan for fear of rejection (discouraged borrowers). The calculation of the indicator starts in 2010, when the question on applications for credit lines was first included in the questionnaire. The components of the financing obstacles indicator were affected by the amendments to the questionnaire in round 11 (filtering based on the relevance of the financing instrument and addition of the new category “My application is still pending”), and past data have been revised accordingly. The figures include the categories “My application is still pending” and “Don’t know”.

Panel b: SMEs across euro area countries

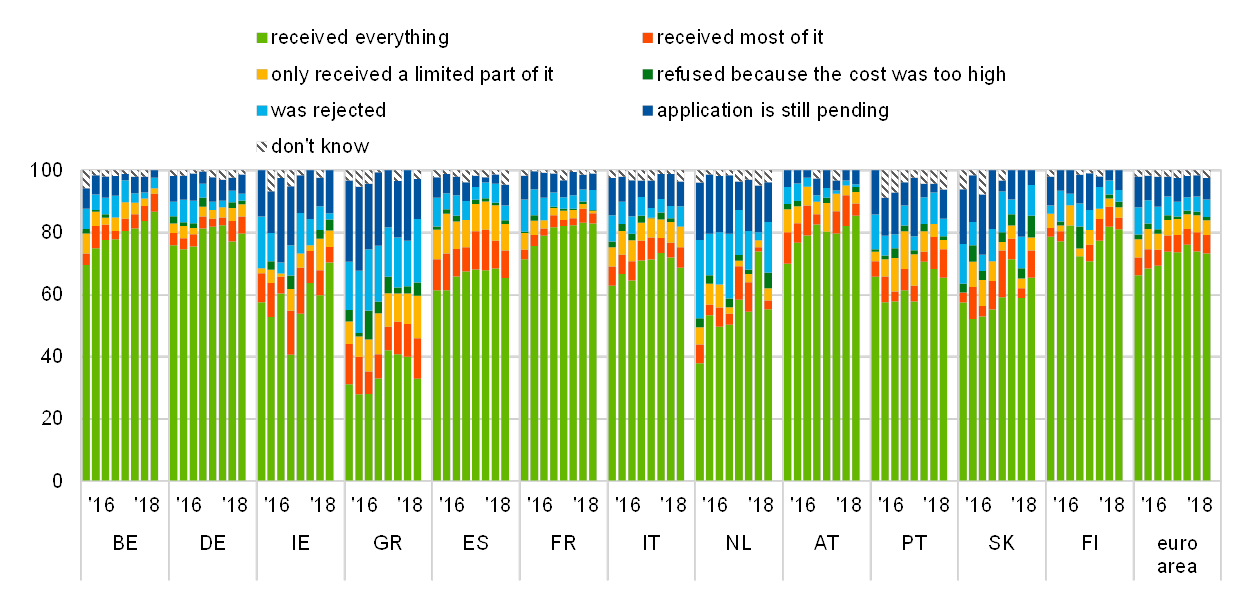

In line with past rounds of the survey, a small share of SMEs applied for a bank loan, even when focusing only on firms that deemed such financing relevant for their business (see Chart 8a in Annex 1). At the level of the euro area, 28% of SMEs applied for a loan, while 43% of SMEs did not apply because of sufficient availability of internal funds. Among firms submitting a loan application, 73% reported being successful in obtaining the full amount requested (see Chart 9a in Annex 1). Among large enterprises, 83% received the full amount requested.

4.3 Increasing interest rates and other costs of financing

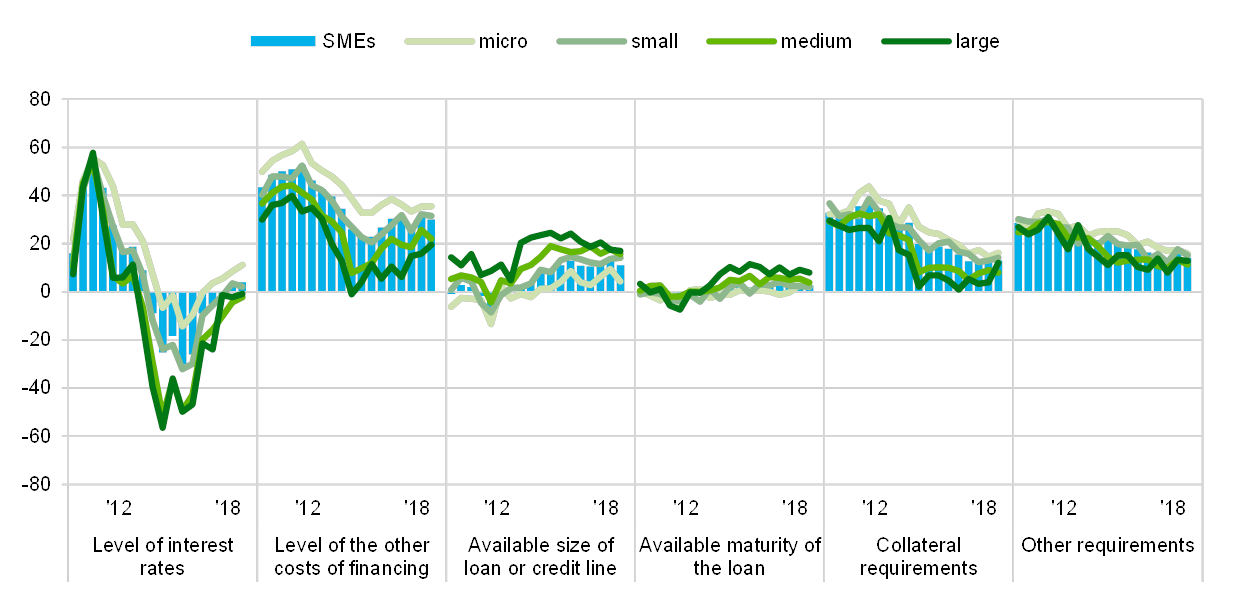

For the second consecutive time since 2014, a net percentage of SMEs reported rises in interest rates on bank loans, reaching 4% (up from 3% in the previous round), merely due to micro firms (11%, from 8%) (see Chart 21). SMEs continued to report an increase in other costs of financing, such as charges, fees and commissions, albeit slightly less than in the previous survey round (30%, from 31%). Other terms and conditions of bank loans were considered to have improved by a similar or somewhat lower net percentage of SMEs, including the available size of a loan or credit line (11%, from 13%), the available maturity (3%, unchanged), collateral requirements (13%, from 12%) and other requirements (14%, from 16%).

Change in terms and conditions of bank financing for euro area enterprises

(over the preceding six months; net percentages of respondents)

Base: Enterprises that had applied for bank loans (including subsidised bank loans), credit lines, or bank or credit card overdrafts. Figures refer to rounds 3 (March-September 2010) to 20 (October 2018-March 2019) of the survey.Note: See the notes to Chart 1.

Q10. Please indicate whether the following items increased, remained unchanged or decreased in the past six months.

Large enterprises still indicated a fall in interest rates but increases in other costs of financing. A net percentage of large enterprises reported lower interest rates on loans granted to them (-1%, from -2%). The corresponding figure for medium-sized firms was also negative (-2%). At the same time, a higher net share of large enterprises indicated rises in other costs of financing (20%, from 16%) and in collateral requirements (12%, from 4%), while the other terms and conditions remained almost unchanged with respect to the previous survey round: other requirements (13%), size of available loans or credit lines (17%) and available maturity (8%, down from 9%).

Developments in interest rates were mixed in the large euro area economies (see Chart 22). For the second consecutive survey round, the net percentage of SMEs reporting increasing interest rates jumped notably in Italy (to 27%, from 14%), while SMEs in Germany (-7%, from 1%), France (-8%, from -4%) and Spain (-1%, unchanged) reported reductions in interest rates. Likewise, a smaller share of SMEs reported increases in other costs of financing in all countries, with the exception of Italy (39%, from 33%), where SMEs also reported higher a net percentage of increased collateral requirements (12%, from 6%).

Change in terms and conditions of bank financing for euro area SMEs

(over the preceding six months; net percentages of respondents)

Base: SMEs that had applied for bank loans (including subsidised bank loans), credit lines, or bank or credit card overdrafts. Figures refer to rounds 3 (March-September 2010) to 20 (October 2018-March 2019) of the survey.Note: See the notes to Chart 1.

Q10. Please indicate whether the following items increased, remained unchanged or decreased in the past six months.

In the other euro area countries, a net percentage of SMEs in Ireland, Slovakia, Finland, Belgium, the Netherlands and Austria reported higher interest rates, while the opposite held for Greece and Portugal (see Charts 10a and 11a in Annex 1). With regard to increases in other costs of financing (charges, fees and commissions), SMEs in most countries reported some acceleration relative to the previous survey round, except in Greece, where the net percentage reported that increases declined to 22% (from 37%), Slovakia (41%, down from 48%) and Portugal (27%, from 31%). As regards the size of bank loans, in most countries SMEs reported net increases, albeit lower than in the previous survey, except in Portugal and Slovakia. SMEs also continued to report increases in the maturity of loans, but this was less marked in this survey round, except in Greece and Austria. At the same time, SMEs in the Netherlands reported a slight decrease (-1%). Increased collateral requirements were reported most strongly in Belgium and the Netherlands.

Interest rates charged by banks on credit lines and overdrafts to SMEs declined slightly in the recent survey (see Chart 23).[15] The median interest rate for SMEs dropped by 13 basis points to 2.0%. By contrast, interest rates for large enterprises remained unchanged at 1.2%, considerably below the borrowing costs for all types of SMEs, in particular when compared with micro firms (3%, down from 4%).

Interest rate charged for a credit line or bank overdraft to euro area enterprises

(percentages)

Base: Enterprises that had successfully applied for a credit line or bank overdraft or that did not apply because the cost was too high. Figures refer to rounds 13 (April-September 2015) to 20 (October 2018-March 2019) of the survey. Notes: The interquartile range is defined as the difference between the 75th percentile and the 25th percentile. The figures are based on the question introduced in round 11 (April-September 2014).

Q8B. What interest rate was charged for the credit line or bank overdraft for which you applied?

In most large euro area countries, the interest rate of bank overdrafts and credit lines either declined or remained unchanged, except in Italy, where the reported median rates rose by 16 basis points to 2.3% (see Chart 24).

Interest rate charged for a credit line or bank overdraft to euro area SMEs

(percentages)

Base: SMEs that had successfully applied for a credit line or bank overdraft or that did not apply because the cost was too high. Figures refer to rounds 13 (April-September 2015) to 20 (October 2018-March 2019) of the survey.Notes: The interquartile range is defined as the difference between the 75th percentile and the 25th percentile. The figures are based on the question introduced in round 11 (April-September 2014).

Q8B. What interest rate was charged for the credit line or bank overdraft for which you applied?

About 47% of the SMEs interviewed indicated that bank loans are not a relevant source of finance for them. In the vast majority of these cases, the SMEs had no need for financing via bank loan (77%; see Chart 25). A small percentage pointed to high interest rates or price as the primary reason for not using bank loans (6%). In Portugal (14%) and Slovakia (12%) this percentage has declined strongly since the last round (from 20% in both countries), while it has increased in some of the remaining countries, in particular in Greece (25%, up from 23%). In addition, a lack of available bank loans is still a notable factor for Greek SMEs (13%, unchanged).

Reasons why bank loans are not a relevant source of financing for euro area SMEs

(over the preceding six months; percentages of respondents)

Base: SMEs for which bank loans are not a relevant source of financing. Figures refer to rounds 13 (April-September 2015) to 20 (October 2018-March 2019) of the survey.

Q32. You mentioned that bank loans are not relevant for your enterprise. What is the main reason for this?

5 Expectations regarding access to finance

5.1 Moderate expectations of SMEs about further improvements in access to external financing

For the period from April to September 2019, SMEs are expecting moderate improvements in the availability of external financing sources (see Chart 26). Specifically, a net 5% of SMEs anticipated better access to bank loans, which is much lower than the net 9% that reported better availability in the period from October 2018 to March 2019. Expectations are similar for availability to most other external funding instruments, including credit lines (4%, compared with 8%), other loans (4%, compared with 9%) and leasing and hire-purchase (11%, compared with 15%). In the case of trade credit, the same percentage of SMEs (9%) reported improvements in the expectations and the past access. Although this survey round found a moderate resizing of the availability of debt securities issued by SMEs (-1%) and some improvements in equity issuance (7%), expectations remain on the positive side (6% and 9%, respectively). However, these figures need to be treated with some caution, as the percentage of firms answering this question in the survey remains extremely low (less than 13% of all SMEs considered market-based financing potentially relevant).

Change in euro area enterprises’ expectations regarding the availability of financing

(over the preceding six months and over the next six months; net percentages of respondents)

Base: Enterprises for which the respective instrument is relevant. Figures refer to round 20 (October 2018-March 2019) of the survey.Note: See the notes to Charts 1 and 11.

Q9. For each of the following types of financing, would you say that their availability has improved, remained unchanged or deteriorated for your enterprise over the past six months?Q23. Looking ahead, for each of the following types of financing available to your enterprise, please indicate whether you think their availability will improve, deteriorate or remain unchanged over the next six months.

Across different company sizes, large enterprises were more cautious in their expectations for most sources of external financing. In particular, the net percentage of large firms expecting improvements was generally much lower than the net percentage of those reporting actual improvements for bank-related products – bank loans (4%, compared with 20%), credit lines (6%, compared with 15%) and leasing or hire-purchase – even though they had benefited most from improvements in external financing. This was also the case for other sources of external funds, except equity investment (6%, compared with 1%).

The moderate assessment about further improvements in access to external financing was widespread across the largest euro area countries (see Chart 27). On balance, German SMEs expect a modest increase in the availability of bank loans in the next six months (3%, compared with 11% reporting increased actual availability), as is the case for SMEs in other countries (see Chart 27).

Change in euro area SMEs’ expectations regarding the availability of financing

(over the preceding six months and over the next six months; net percentages of respondents)

Base: SMEs for which the respective instrument is relevant. Figures refer to round 20 (October 2018-March 2019) of the survey.Note: See the notes to Charts 1 and 11.

Q9. For each of the following types of financing, would you say that their availability has improved, remained unchanged or deteriorated for your enterprise over the past six months?Q23. Looking ahead, for each of the following types of financing available to your enterprise, please indicate whether you think their availability will improve, deteriorate or remain unchanged over the next six months.

Annexes

Annex 1 Overview of the survey replies – selected charts

Change in turnover and profits of SMEs across euro area countries

(over the preceding six months; net percentages of respondents)

Base: All SMEs. Figures refer to rounds 13 (April-September 2015) to 20 (October 2018-March 2019) of the survey.Note: See the notes to Chart 1.

Q2. Have the following company indicators decreased, remained unchanged or increased over the past six months?

Change in debt-to-total-assets ratio and interest expenses of SMEs across euro area countries

(over the preceding six months; net percentages of respondents)

Base: All SMEs. Figures refer to rounds 13 (April-September 2015) to 20 (October 2018-March 2019) of the survey.Note: See the notes to Chart 1.

Q2. Have the following company indicators decreased, remained unchanged or increased over the past six months?

Vulnerable and profitable SMEs across euro area countries

(over the preceding six months; percentages of respondents)

Base: All SMEs. Figures refer to rounds 3 (March-September 2010) to 20 (October 2018-March 2019) of the survey.Notes: For definitions, see footnote 8 of the report. In Slovakia, the survey was initially conducted every two years (first half of 2009, 2011 and 2013). From 2014 onwards, Slovakia has been included in the sample in each survey round.

Q2. Have the following company indicators decreased, remained unchanged or increased over the past six months?

The most important problems faced by euro area SMEs across euro area countries

(over the preceding six months; percentages of respondents)

Base: All SMEs. Figures refer to rounds 13 (April-September 2015) to 20 (October 2018-March 2019) of the survey.Note: See the notes to Chart 5.

Q0. How important have the following problems been for your enterprise in the past six months?

Change in the availability of and need for bank loans for SMEs across euro area countries

(over the preceding six months; net percentages of respondents)

Base: SMEs for which the respective instrument is relevant. Figures refer to rounds 13 (April-September 2015) to 20 (October 2018-March 2019) of the survey.Note: See the notes to Charts 1 and 11.

Q5. For each of the following types of external financing, please indicate if your needs increased, remained unchanged or decreased over the past six months.Q9. For each of the following types of financing, would you say that their availability has improved, remained unchanged or deteriorated for your enterprise over the past six months?

Change in the external financing gap perceived by SMEs across euro area countries

(over the preceding six months; weighted net balances)

Base: SMEs for which the respective instrument is relevant. “Not applicable” and “Don’t know” answers are excluded. Figures refer to rounds 13 (April-September 2015) to 20 (October 2018-March 2019) of the survey.Notes: See notes to Chart 17. The financing gap indicator combines both financing needs and availability of bank loans, credit lines, trade credit, equity and debt securities at the firm level. For each of the five financing instruments, the indicator of the perceived change in the financing gap takes the value of 1 (-1) if the need increases (decreases) and availability decreases (increases). If enterprises perceive only a one-sided increase (decrease) in the financing gap, the variable is assigned a value of 0.5 (-0.5). The composite indicator is the weighted average of the financing gap related to the five instruments. A positive value of the indicator suggests an increasing financing gap. Values are multiplied by 100 to obtain weighted net balances in percentages.

Q5. For each of the following types of external financing, please indicate if your needs increased, remained unchanged or decreased over the past six months.Q9. For each of the following types of financing, would you say that their availability has improved, remained unchanged or deteriorated for your enterprise over the past six months?

Change in factors with an impact on the availability of external financing for SMEs across euro area countries

(over the preceding six months; net percentages of respondents)

Base: All SMEs. For the category “Willingness of banks to lend”, these are SMEs for which at least one bank financing instrument (credit line, bank overdraft, credit card overdraft, bank loan or subsidised bank loan) is relevant. Figures refer to rounds 13 (April-September 2015) to 20 (October 2018-March 2019) of the survey.Notes: See the notes to Charts 1 and 18. From round 11 (April-September 2014), the category “Willingness of banks to provide a loan” was reformulated slightly to “Willingness of banks to provide credit to your enterprise”.

Q11. For each of the following factors, would you say that they have improved, remained unchanged or deteriorated over the past six months?

Applications for bank loans by SMEs across euro area countries

(over the preceding six months; percentages of respondents)

Base: SMEs for which bank loans (including subsided bank loans) are relevant. Figures refer to rounds 13 (April-September 2015) to 20 (October 2018-March 2019) of the survey.Note: See the notes to Chart 11.

Q7A. Have you applied for the following types of financing in the past six months?

Outcome of applications for bank loans by SMEs across euro area countries

(over the preceding six months; percentages of respondents)

Base: SMEs that had applied for bank loans (including subsided bank loans). Figures refer to rounds 13 (April-September 2015) to 20 (October 2018-March 2019) of the survey.Note: See the notes to Chart 11.

Q7B. If you applied and tried to negotiate this type of financing over the past six months, what was the outcome?

Change in the cost of bank financing for SMEs across euro area countries

(over the preceding six months; net percentages of respondents)

Base: SMEs that had applied for bank loans (including subsidised bank loans), credit lines, or bank or credit card overdrafts. Figures refer to rounds 13 (April-September 2015) to 20 (October 2018-March 2019) of the survey.Note: See the notes to Chart 1.

Q10. Please indicate whether the following items increased, remained unchanged or decreased in the past six months.

Change in non-price terms and conditions of bank financing for SMEs across euro area countries

(over the preceding six months; net percentages of respondents)

Base: SMEs that had applied for bank loans (including subsidised bank loans), credit lines, or bank or credit card overdrafts. Figures refer to rounds 13 (April-September 2015) to 20 (October 2018-March 2019) of the survey.Note: See the notes to Chart 1.

Q10. Please indicate whether the following items increased, remained unchanged or decreased in the past six months.

Annex 2 Descriptive statistics for the sample of enterprises

Breakdown of enterprises across economic activities

(unweighted percentages)

Base: Figures refer to round 20 (October 2018-March 2019) of the survey.

Breakdown of enterprises by age of the firm

(unweighted percentages)

Base: Figures refer to round 20 (October 2018-March 2019) of the survey.

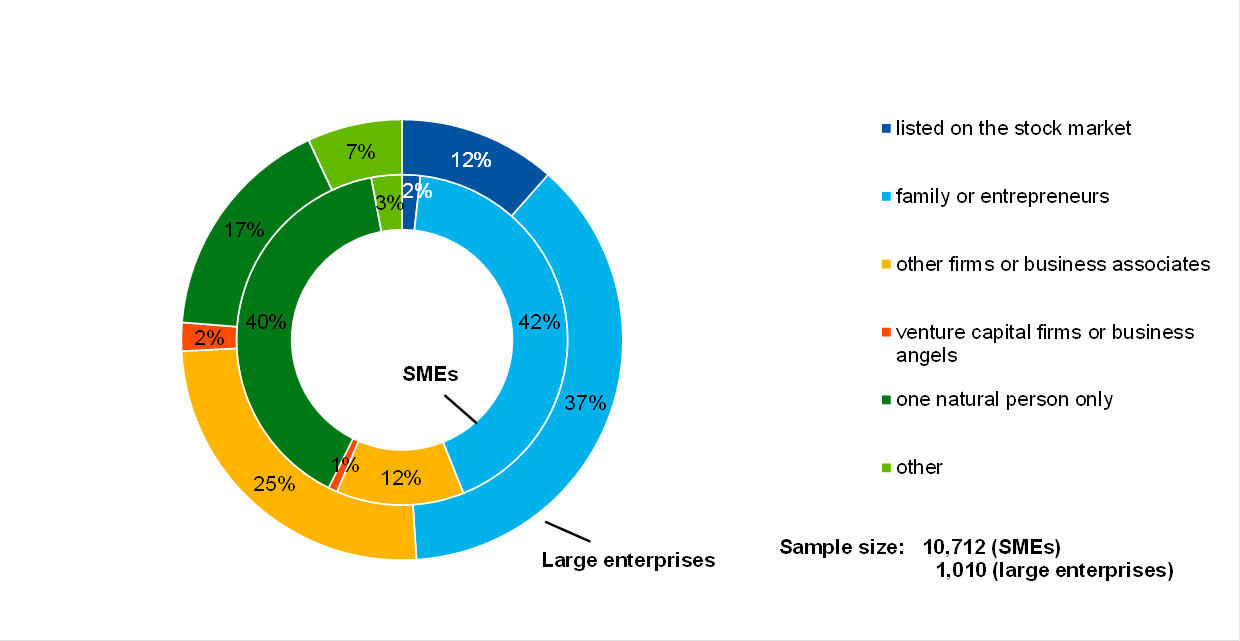

Breakdown of enterprises according to ownership

(unweighted percentages)

Base: Figures refer to round 20 (October 2018-March 2019) of the survey.

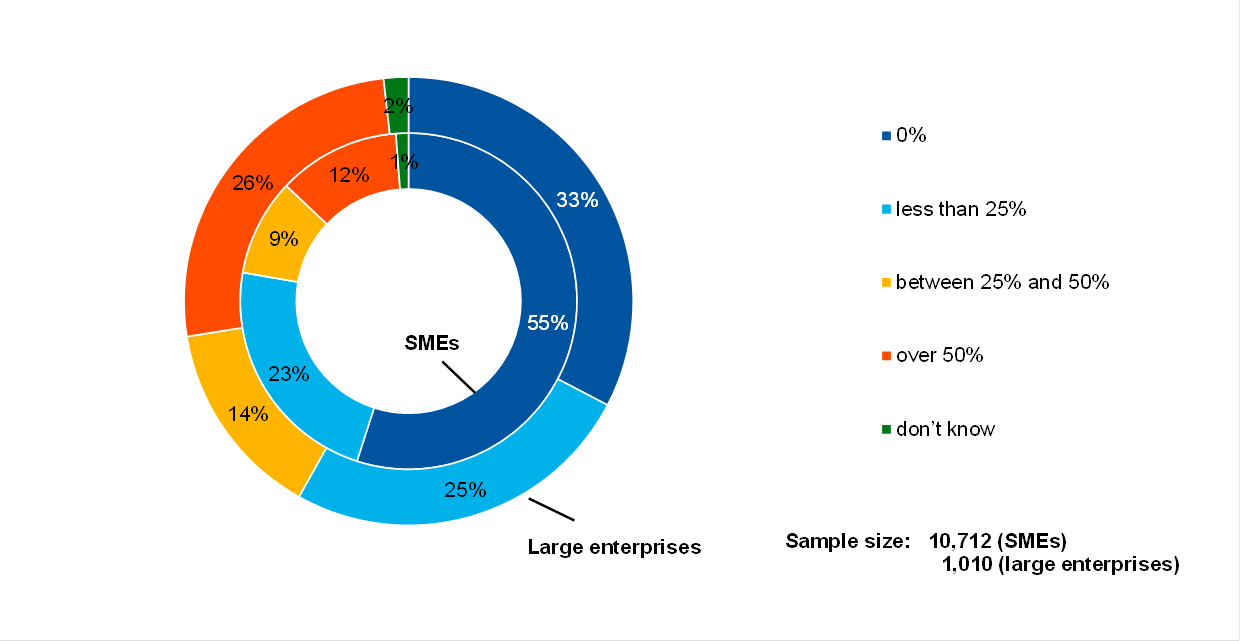

Breakdown of enterprises according to exports

(unweighted percentages)

Base: Figures refer to round 20 (October 2018-March 2019) of the survey.

Annex 3 Methodological information on the survey

This annex presents the main changes introduced in the latest round of the Survey on the Access to Finance of Enterprises (SAFE). For an overview of how the survey was set up, the general characteristics of the euro area enterprises that participated in the survey and the changes introduced to the methodology and the questionnaire over time, see the “Methodological information on the survey and user guide for the anonymised micro dataset” available on the ECB’s website.[16]

Since September 2014 the survey has been carried out by Panteia b.v., in cooperation with the fieldwork provider GDCC. To the best of our knowledge, no breaks in the series are attributable to any change of provider over the life cycle of the survey.

However, some changes in the questionnaire may have caused a break between the round covering the second half of 2013 and that covering the first half of 2014. This stems from the review of various components of the survey after ten survey rounds, covering the questionnaire, sample allocation, survey mode and weighting scheme (see Annex 4 in the corresponding report on the ECB’s website for details[17]).

With regard to the weighting scheme, up to the survey round in the first half of 2015, the calibration targets were updated with each survey round based on the latest available figures from Eurostat’s structural business statistics (SBS). Since then, with all the euro area countries participating in the survey, the weighting scheme has been updated once a year.[18]

In this survey round no major changes were made to the existing questions in the questionnaire.[19]

© European Central Bank, 2019

Postal address 60640 Frankfurt am Main, GermanyTelephone +49 69 1344 0Website www.ecb.europa.eu

All rights reserved. Reproduction for educational and non-commercial purposes is permitted provided that the source is acknowledged.The cut-off date for data included in this report was 28 May 2019.

PDF ISSN 1831-9998, QB-AP-19-001-EN-NHTML ISSN 1831-9998, QB-AP-19-001-EN-Q

- [1]See Annex 3 for details on methodological issues related to the survey set-up.

- [2]Net terms or net percentages are defined as the difference between the percentage of enterprises reporting that a given factor has increased and the percentage of those reporting that it has declined.

- [3]A negative financing gap indicates that the increase in the need for external financing is smaller than the improvement in the access to external funds.

- [4]The financing obstacles indicator is the sum of the percentages of SMEs reporting rejections of loan applications, loan applications for which only a limited amount was granted, and loan applications which resulted in an offer that was declined by the SME because the borrowing costs were too high, as well as the percentage of SMEs that did not apply for a loan for fear of rejection.